Coordinating Debt, Depreciation, and Exit Timing Across Multiple Assets

A strong portfolio tax plan coordinates acquisition, operating, refinance, and exit decisions before they collide.

The planning issue in one screen

Coordinating debt, depreciation, and exit timing across multiple assets is a portfolio design problem. It is not just a question of how much can be deducted this year.

The immediate planning issue is this:

Will the tax benefit created in the acquisition and operating years still make sense when debt matures, depreciation reduces basis, passive losses are tested, and one or more assets must be sold, exchanged, refinanced, or transferred?

For high-income Florida investors, that question should be answered before the next purchase, improvement, refinance, or sale. A single-asset tax projection may look clean. A multi-asset portfolio often does not.

| Planning Lever | What It Does Early | What It Can Create Later | What Should Be Coordinated |

|---|---|---|---|

| Debt | Increases acquisition capacity, may affect basis and loss capacity, and can improve cash-on-cash returns. | Interest limitation issues, refinancing pressure, reserve strain, debt replacement problems in an exchange. | Loan maturity, rate exposure, debt allocations, partner basis, liquidity reserves. |

| Depreciation | Reduces taxable income and may improve after-tax cash flow. | Lower adjusted basis, recapture exposure, unrecaptured §1250 gain, suspended passive losses. | Cost segregation timing, income classification, material participation, hold period. |

| Exit Timing | Converts deferred tax into actual tax unless deferred or managed. | Gain stacking, NIIT exposure, debt payoff pressure, rushed reinvestment. | Sale sequencing, 1031 feasibility, installment structure, charitable planning, estate timing. |

| Multiple Assets | Creates flexibility when events are staggered well. | Creates compression when gains, debt events, and liquidity needs collide. | Portfolio-level tax calendar, not one-property tax decisions. |

The article’s core framework is simple:

Model the exit before maximizing the deduction.

Match depreciation to usable income, not just projected income.

Treat debt as a timing and flexibility variable.

Sequence assets across the portfolio so one good tax move does not create a worse exit year.

For high-income taxpayers, the exit year can carry multiple layers. NIIT is 3.8% on the lesser of net investment income or the excess of modified adjusted gross income over the applicable threshold, including $250,000 for married filing jointly and $200,000 for single or head of household filers. Net investment income can include rental income, passive business income, and gains from dispositions of property, depending on the facts.

A real estate exit may also include unrecaptured §1250 gain. The IRS states that the portion of gain from selling §1250 real property treated as unrecaptured §1250 gain is taxed at a maximum 25% rate.

That is why the strongest planning question is not, “How much depreciation can we take?”

It is:

Which deduction should be accelerated, which basis should be preserved, and which future exit year are we trying not to overload?

Explore how exit timing, debt payoff, recapture, and NIIT can collide when multiple assets mature in the same window.

Why this matters more in multi-year planning

Debt, depreciation, and exits are often handled in different advisory lanes.

A lender focuses on leverage and underwriting. A cost segregation provider focuses on accelerating deductions. A broker focuses on transaction timing. An attorney focuses on entity structure and closing mechanics. A preparer records the tax year after the facts are mostly fixed.

That division of labor can be useful. It can also create fragmented planning.

A high-income investor may end up with the right loan, the right cost segregation study, the right LLC, and the right sale price, yet still have a weak tax strategy because those decisions were never sequenced together.

A multi-year plan connects the acquisition year, operating years, refinancing years, and exit years. It asks:

Are the deductions usable now, or are they likely to be suspended?

Does the debt structure support the intended hold period?

Does the entity structure preserve sale, exchange, transfer, and partner-level flexibility?

Could two or three assets create taxable events in the same calendar year?

Is a future 1031 exchange economically realistic, or only technically possible?

Would paying some tax now preserve more flexibility than deferring everything?

For Florida taxpayers, the federal layer carries extra weight. Florida law reflects that no income tax is levied on natural persons who are residents and citizens of the state, which means the planning focus for many high-income Florida individuals is often federal income tax, NIIT, depreciation, capital gain, estate planning, property tax economics, and liquidity rather than state income tax arbitrage.

Key takeaways

Accelerated depreciation is most valuable when the deduction is usable, well-timed, and consistent with the expected exit.

Debt can improve acquisition economics, but it can also reduce flexibility if refinancing, reserve needs, or exchange debt replacement are ignored.

The exit year is where weak planning becomes visible. Gain, recapture, NIIT, debt payoff, and reinvestment pressure can all arrive together.

Portfolio sequencing often matters more than asset-level optimization. The best answer for one property may be the wrong answer for the balance sheet.

Florida planning should account for federal tax exposure, real estate concentration, property tax resets, insurance costs, casualty risk, and liquidity reserves.

A strong plan preserves options. It does not assume every asset will be held forever, exchanged perfectly, or sold in a low-income year.

Start with the exit before choosing the deduction

Most planning around depreciable assets starts too late and too narrowly.

The common starting point is:

“How much can we deduct this year?”

The better starting point is:

“What are the realistic exit paths for this asset, and what happens to the portfolio under each one?”

A property expected to be held for 20 years, refinanced conservatively, exchanged repeatedly, or transferred through an estate raises different planning questions than a property likely to be sold in three years because of redevelopment value, partnership friction, insurance pressure, or a maturing loan.

The depreciation decision may still be favorable in both cases. The sequencing should not be the same.

| Likely Path | Depreciation Posture | Debt Posture | Exit Planning Focus |

|---|---|---|---|

| Long-Term Hold | Accelerated depreciation may be useful if losses are usable or can shelter passive income. | Favor durable fixed or hedged debt, reserves, and reinvestment capacity. | Refinance discipline, basis tracking, estate planning. |

| Medium-Term Sale | Be selective with acceleration if the sale is likely before benefits compound. | Match debt maturity to a realistic sale window. | Recapture modeling, NIIT management, gain spreading. |

| 1031 Exchange Path | Depreciation can help, but replacement property quality and timing matter. | Plan replacement debt and equity before the sale process begins. | Identification risk, boot, debt replacement, portfolio fit. |

| Uncertain Hold Period | Preserve flexibility rather than maximizing first-year deductions by default. | Avoid leverage that forces a tax-disadvantaged sale. | Compare hold, sale, exchange, refinance, and transfer cases. |

Depreciation has a time signature. A deduction taken in Year 1 may reduce taxable income today, but it also reduces basis and changes the tax profile of a future sale.

That trade-off is not inherently bad. It is bad when it is accidental.

The right plan identifies the expected exit before deciding how much depreciation to accelerate, how much debt to carry, and how much liquidity to preserve.

Debt is not just financing. It is a tax timing variable.

Debt affects more than purchase power.

In a multi-asset plan, debt can influence:

whether losses are currently usable

whether interest is deductible

whether partners have sufficient basis to absorb allocations

whether cash flow can support the intended hold period

whether a future exchange requires replacement debt

whether a refinance creates flexibility or simply delays a forced sale

whether a partner or family member can exit without forcing a portfolio-wide tax event

For larger businesses and real estate groups, the business interest limitation under §163(j) can also matter. When the limitation applies, deductible business interest expense generally cannot exceed business interest income plus 30% of adjusted taxable income plus floor plan financing interest expense. The IRS also notes that the limitation applies at the partnership level for partnerships and at the S corporation level for S corporations.

This makes leverage a structural decision, not just a loan decision.

A property may look tax-efficient because depreciation offsets rental income. But if interest deductions are limited, passive losses are suspended, or debt service weakens reserves, the tax result may not translate into usable cash.

Debt also affects exits. In a 1031 exchange, replacing relinquished-property debt can be necessary to avoid taxable boot, but taking on replacement debt only to preserve deferral may create a weaker long-term position. In a partnership, debt allocation can affect outside basis, loss absorption, distribution capacity, and gain recognition on exit.

This is where tax planning and capital planning should meet. A loan that works at acquisition may fail the plan if it creates a refinance deadline in the same window as a likely sale, business liquidity event, or major capital improvement.

Depreciation should be matched to income type, not just income amount

For sophisticated taxpayers, the limiting question is often not whether depreciation exists. It is whether the taxpayer can use it in the intended year and against the intended type of income.

Rental activities are generally passive even when the taxpayer materially participates, unless the taxpayer qualifies under the real estate professional rules and materially participates in the rental real estate activity. The passive activity and at-risk rules can limit losses from rental or other income-producing activities, and the at-risk rules are applied before the passive activity rules.

Short-term rental activity can raise a different classification analysis. IRS guidance describes exceptions where an activity is not treated as a rental activity, including average customer use of seven days or less, or average customer use of 30 days or less when significant personal services are provided.

That distinction matters for Florida investors with vacation-market properties, short-term rentals, mixed-use real estate, and service-heavy rental models.

The planning question is not simply:

“Will this asset generate depreciation?”

It is:

“Will this depreciation offset income in the right bucket, in the right year, without creating a future tax stack we have not modeled?”

A high-income physician with W-2 income, passive rental losses, and no real estate professional status may not receive the same current benefit as an investor with passive income from other properties. A business owner with active operating income may benefit from depreciation in one structure but not another. A short-term rental may create a different analysis depending on average stay, services, participation, and documentation.

This is one of the places where a reader who already has a CPA can still have a planning gap. The tax return may report the loss correctly. The planning question is whether the loss should have been created in that asset, in that year, in that ownership structure.

The “works early, breaks later” pattern

A common failure mode looks like this:

Year 1: The investor acquires several assets with leverage and accelerates depreciation. The tax result looks strong.

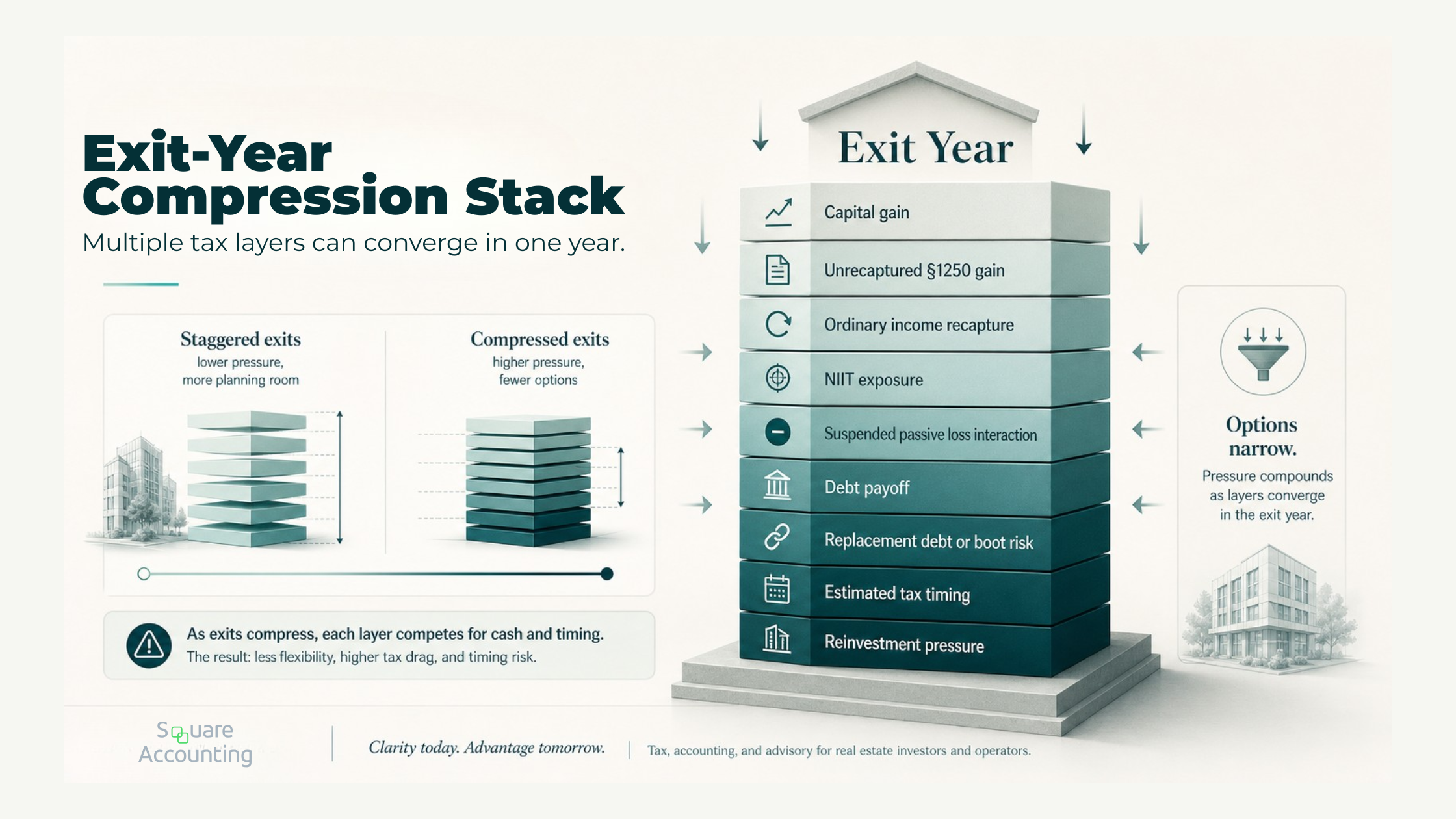

Exit-year compression is where isolated tax decisions become a portfolio-level liquidity and timing problem.

Year 2: Insurance, repairs, interest, vacancy, or management costs change the economics. Some losses are suspended because of passive activity limitations. Cash flow is tighter than the acquisition model suggested.

Year 3: A refinance is less attractive than expected, a partner wants liquidity, or one asset receives an offer that is economically hard to ignore.

Exit year: Gain, recapture, NIIT, debt payoff, estimated tax payments, and reinvestment pressure arrive together. The earlier deductions reduced taxable income, but they did not create enough flexibility to manage the unwind well.

This is the “works early, breaks later” pattern.

It does not mean the original strategy was wrong. It means the original strategy was incomplete.

The deeper issue is exit-year compression. A portfolio can tolerate deferral when future income events are staggered and liquidity is planned. It becomes fragile when multiple loans, properties, gains, suspended losses, and personal income events converge in the same year.

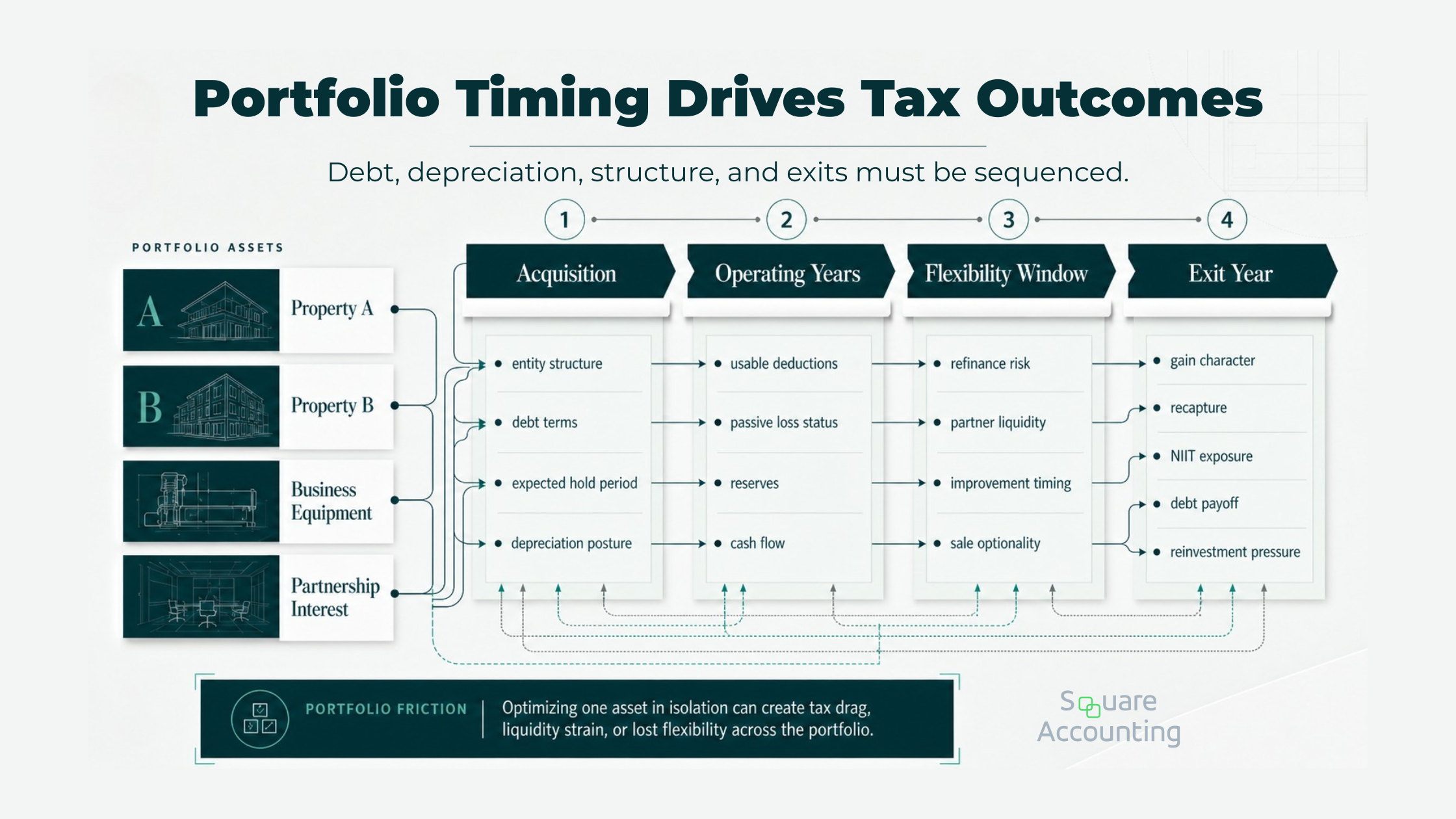

A better planning model evaluates each asset in four columns:

| Asset | Current-Year Tax Benefit | Future Tax Burden | Exit Flexibility |

|---|---|---|---|

| Property A | Depreciation usable against passive income. | Recapture and gain if sold. | Strong 1031 candidate if replacement property is planned early. |

| Property B | Losses likely suspended. | Basis reduced without current cash-tax benefit. | Sale risk if insurance or repairs change economics. |

| Business Equipment | Immediate deduction may be available. | Recapture may be ordinary income on sale. | Tied to business sale or replacement cycle. |

| Partnership Interest | Allocations depend on debt and agreement. | Gain may include debt relief and allocation effects. | Limited control if exit rights are poorly drafted. |

Once the portfolio is mapped this way, the conversation changes. The goal is no longer to maximize depreciation asset by asset. The goal is to deploy depreciation where it is usable, preserve basis where flexibility matters, and avoid bunching taxable exits into the same year.

Bonus depreciation makes sequencing more important, not less

Accelerated depreciation can be powerful, but current rules make sequencing more important because the front-end benefit can be larger.

IRS Publication 946 states that, unless a taxpayer elects out, certain qualified property acquired and placed in service after January 19, 2025, is eligible for a 100% special depreciation allowance. The same IRS guidance also describes an election to take a 40% special depreciation allowance for certain qualified property acquired and placed in service after January 19, 2025, in the first tax year ending after that date, instead of the 100% allowance.

The key word is certain. Bonus depreciation does not apply to every asset in a real estate deal. It generally becomes relevant through qualifying components, improvements, personal property, or other eligible property identified through proper classification.

When a taxpayer can deduct more sooner, the temptation is to treat maximum acceleration as the default. For a high-income investor, that may be the right choice when the deduction offsets income that would otherwise be taxed at a high marginal rate and the asset has a durable hold period.

But maximum acceleration may be less attractive when:

the loss will be passive and suspended

the asset may be sold soon

the taxpayer expects higher income in a future year

the deduction creates a low-income year that wastes other planning opportunities

the exit is likely to occur in the same window as other large gains

the deduction reduces basis in an asset that may need to be sold for liquidity

the ownership structure makes future allocations or buyouts harder to manage

The planning choice is not always “depreciate or do not depreciate.” It may be whether to elect out for a class of property, whether to time improvements differently, whether to place assets in service in a different year, or whether to pair depreciation with income recognition, charitable deductions, Roth conversion planning, passive income planning, or gain harvesting.

The strategic point is that larger front-end deductions require a more serious back-end model.

We can review whether accelerated depreciation is usable now, likely to be suspended, or better coordinated with a future exit.

Exit timing is where debt and depreciation finally meet

A sale is not just a capital gains event.

For a depreciated, debt-financed asset, the exit may involve:

capital gain

unrecaptured §1250 gain for depreciated real property

ordinary income recapture for certain property

NIIT exposure

suspended passive loss release or continued deferral

debt payoff

taxable boot in an exchange

replacement property pressure

partner-level or entity-level allocation issues

estimated tax payment timing

liquidity needs outside the asset itself

Like-kind exchanges can help defer gain when real property used in a business or held for investment is exchanged for other qualifying real property. IRS guidance states that, generally, gain or loss is not recognized in a like-kind exchange under §1031. The IRS also states that for 2018 and later years, §1031 treatment applies only to exchanges of real property held for use in a trade or business or for investment, other than real property held primarily for sale.

That makes 1031 planning valuable, but it should not be treated as a last-minute rescue plan.

An exchange must work economically, not only technically. The replacement property must fit the investor’s debt tolerance, income needs, geographic exposure, estate plan, liquidity requirements, and family objectives. Replacing debt simply to avoid taxable boot can create a worse long-term outcome if the investor is forced into leverage or property quality they would not otherwise accept.

The same is true for installment sales, charitable planning, partial exchanges, and sale sequencing. Each can be useful. Each can also fail if introduced after the economics are already locked.

The exit year is where debt and depreciation finally settle the account. Planning should begin before the buyer appears.

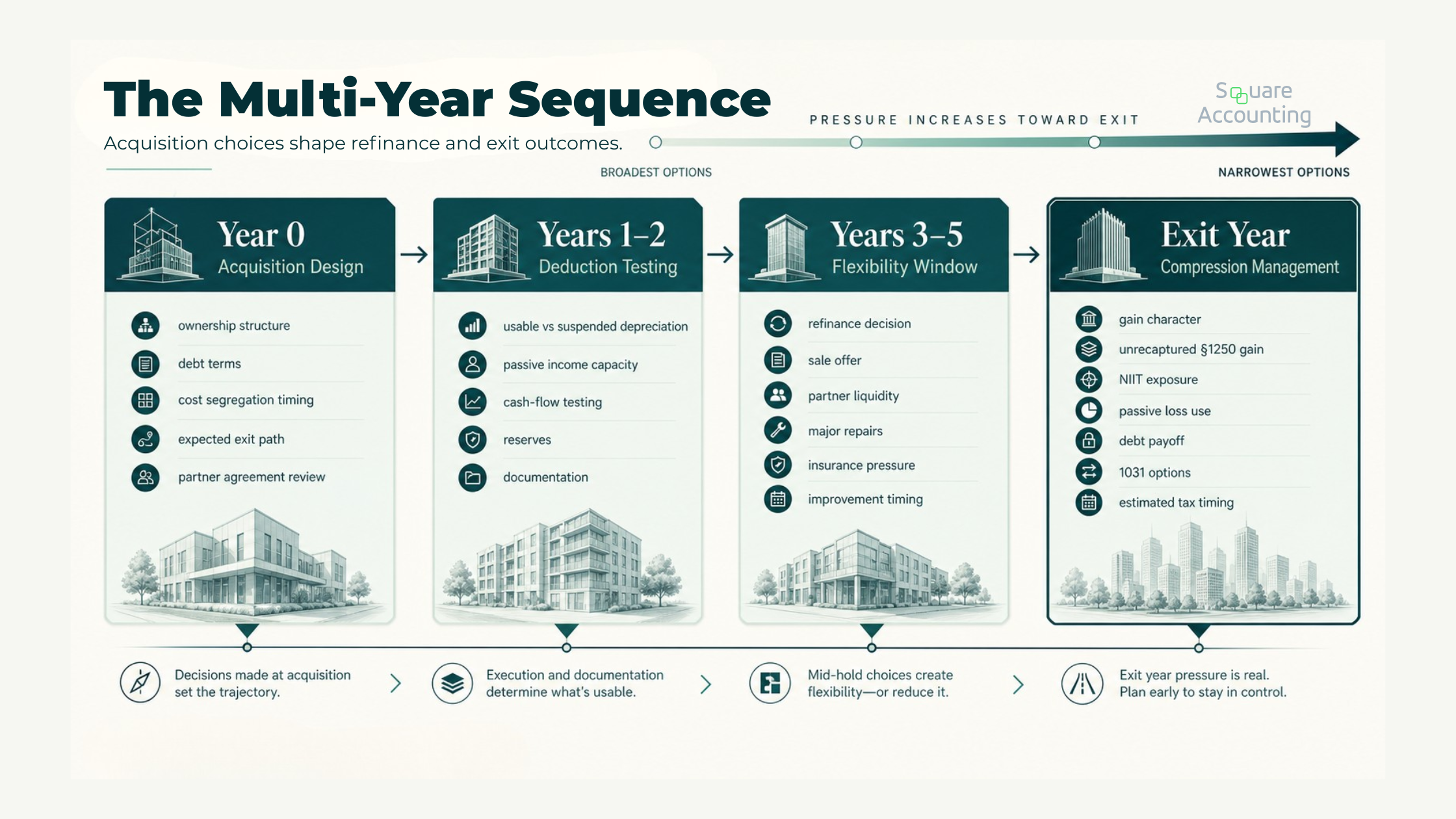

A practical multi-year sequencing framework

A coordinated plan should separate the portfolio into four planning windows, even if the exact dates are uncertain.

Multi-year sequencing helps determine whether today’s deduction creates future flexibility or future pressure.

Year 0: Acquisition design

Before closing, determine:

who should own the asset

whether the entity structure preserves exit flexibility

whether debt allocations support the intended tax result

whether depreciation will be usable or suspended

whether a cost segregation study should be done now or later

whether improvements should be timed before or after acquisition

whether the likely exit is sale, refinance, exchange, charitable transfer, estate transfer, or long-term hold

whether the operating agreement supports the intended allocations, buyouts, and timing decisions

This is also when partnership agreements should be reviewed. Tax allocations, debt sharing, preferred returns, capital account provisions, buy-sell rights, drag-along rights, and management control can determine whether the tax plan survives partner disagreement.

A plan that depends on a 1031 exchange, for example, should not ignore whether the partners will still want the same replacement property when the time comes.

Years 1 and 2: Deduction and cash-flow testing

After acquisition, compare projected tax benefits with actual operating performance.

A good Year 1 result is not simply a lower tax bill. It is a lower tax bill supported by durable economics.

This is where we test:

whether losses are usable or suspended

whether passive income exists to absorb passive losses

whether debt service is pressuring reserves

whether insurance, repairs, and property taxes are changing the hold thesis

whether depreciation is being used against the right income

whether income from other assets can absorb losses

whether documentation supports the intended activity classification

whether the taxpayer’s broader income profile has changed

If the strategy only works when the original projections are perfect, it is not robust enough for a multi-asset portfolio.

Years 3 through 5: Flexibility window

Many problems surface before the planned exit.

A loan may reset. A partner may want liquidity. A property may require a major capital project. A market buyer may appear early. A short-term rental market may soften. Insurance may change the net yield. A business owner may receive an acquisition offer in the same period that a property is ready to sell.

This is the window to decide whether to preserve, refinance, improve, exchange, sell, or hold.

It is also the window to coordinate assets against each other. Selling one asset may make sense if another asset has suspended losses. Holding one property may make sense if another exit will already push the taxpayer into NIIT exposure. Refinancing may make sense if it preserves control, but not if it simply delays an unavoidable taxable exit into a worse year.

Waiting until an asset is under contract narrows the tax options.

Exit year: Compression management

The exit year should be modeled before the exit year begins whenever possible.

The model should include:

taxable gain by character

depreciation recapture or unrecaptured §1250 gain

NIIT exposure

passive loss utilization

debt payoff and replacement debt needs

charitable giving capacity

installment sale feasibility

1031 exchange alternatives

interaction with business income, bonuses, Roth conversions, or other asset sales

post-sale reinvestment quality and liquidity

The aim is not to eliminate tax in every case. Sometimes the better decision is to recognize gain, pay tax, and redeploy capital with more flexibility.

The aim is to avoid recognizing gain accidentally, inefficiently, or in the same year as several other avoidable tax events.

We can help organize acquisition, operating, refinance, and exit years into one coordinated planning calendar.

Florida-specific planning considerations

Florida’s lack of personal income tax does not make planning simple. It changes where the pressure sits.

For a Florida taxpayer with substantial real estate or business interests, the main tax friction may come from federal capital gains, NIIT, depreciation, business interest limitations, estate planning, entity structure, property tax changes, insurance costs, and liquidity.

The absence of state personal income tax can make investors more willing to recognize gain. That may be reasonable. It can also be misleading when federal gain, unrecaptured §1250 gain, NIIT, and debt payoff stack into one year.

Florida real estate also creates planning issues that do not appear on a depreciation schedule.

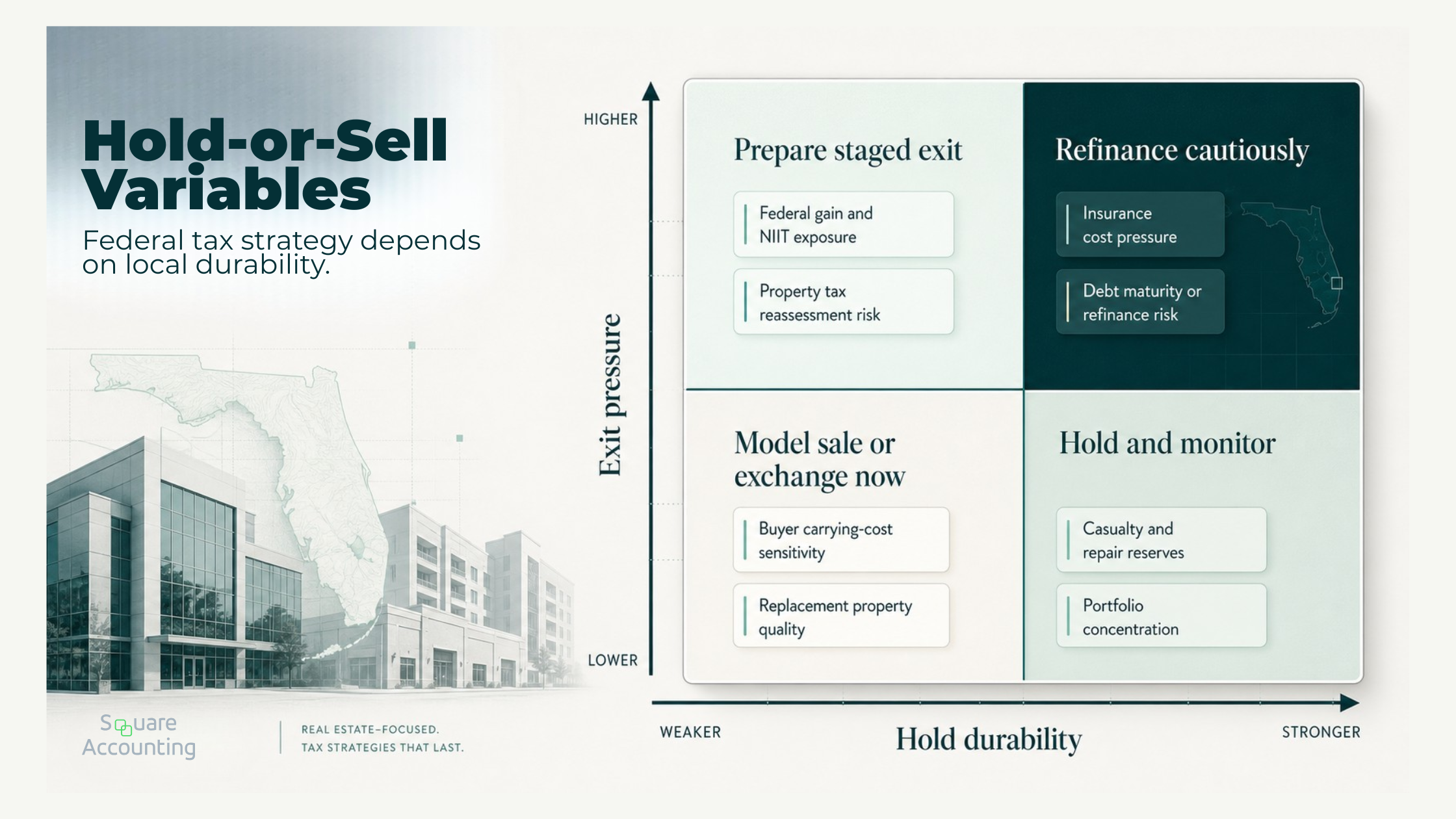

Homestead versus non-homestead economics

Florida’s Save Our Homes assessment limitation generally limits annual increases in assessed value for homestead property to 3% or the change in CPI, whichever is lower, after the first year the home receives the homestead exemption and is assessed at just value.

Non-homestead property is different. Florida non-homestead property can receive a 10% assessment limitation, but the cap does not apply to school district taxes and can be removed upon certain changes in ownership, control, or qualifying improvements.

For investors, this means property tax economics may change after a sale, change in control, change in use, or significant improvement. A buyer’s carrying cost may not match the seller’s. A hold-versus-sell analysis should account for the future owner’s property tax burden, not only the current owner’s tax bill.

This can affect value, buyer underwriting, and timing. A sale that looks attractive before reassessment may be less compelling after transaction costs, debt payoff, federal tax, and buyer-side property tax economics are modeled.

Insurance, casualty risk, and reserve planning

Florida investors also need to treat insurance, casualty exposure, and reserves as tax timing variables.

A depreciation strategy may assume a long hold. But if insurance costs, deductible exposure, storm damage, repairs, or financing pressure shorten the hold period, the taxpayer may face gain and recapture sooner than expected.

The planning question is not only whether the property is profitable today. It is whether the owner has enough liquidity and insurance durability to hold through the tax plan’s intended timeline.

This matters more when a portfolio is concentrated in similar geography or property type. If several assets face insurance increases, repair needs, or financing pressure at the same time, the investor may lose the ability to choose which asset exits first.

Florida concentration risk

Many Florida high-net-worth taxpayers have concentrated exposure to local real estate, closely held businesses, professional practices, and investment property within the same economic environment.

That concentration can magnify exit-year compression.

A professional with practice income, two rental properties, a short-term rental, and a commercial building may not have five separate tax problems. They may have one portfolio-level timing problem.

If two properties sell, a practice buyout occurs, and a refinancing becomes unattractive in the same year, the tax impact can be materially different from selling one asset in isolation.

A Florida plan should therefore include a liquidity calendar, a debt maturity calendar, and a tax event calendar. The value is not in predicting every event. The value is in knowing which events should not collide.

Common misuses and oversights

1. Treating cost segregation as a stand-alone strategy

Cost segregation can be valuable, especially when accelerated deductions are usable. But it should not be evaluated as a stand-alone win.

The real question is what happens after the study:

Are the deductions currently usable?

Do they offset passive income, active income, or nothing yet?

Is the asset likely to be sold before the benefit compounds?

Will the taxpayer have a plan for the recapture profile?

Does the study fit the debt and exit strategy?

Does the ownership structure support the intended allocation of benefits and burdens?

A study that creates suspended losses may still have value, but it is a different value than a study that reduces current tax on high-rate income.

2. Assuming debt automatically improves the tax result

Leverage can increase returns, but it can also reduce flexibility.

The wrong debt structure can force an asset sale in a poor tax year, limit refinancing options, or require replacement debt in a 1031 exchange that no longer fits the investor’s risk tolerance.

Debt should be stress-tested with tax included. A loan that looks efficient before tax may be fragile after interest limits, reserves, insurance costs, and exit-year gain are modeled.

3. Selling the best tax asset first

Sometimes investors sell the asset with the best market offer without asking which asset should be sold first from a tax standpoint.

The better candidate for sale may be the asset with:

lower recapture exposure

released passive losses

stronger basis

weaker long-term cash flow

fewer exchange complications

a buyer pool that supports installment planning

less strategic value to the family or operating business

Market price matters, but so does after-tax redeployment.

The question is not simply “Which asset received the best offer?” It is “Which sale improves the portfolio after tax, after debt payoff, after reinvestment, and after the next three years of expected events?”

4. Using 1031 exchanges as a reflex

A 1031 exchange can be an excellent tool. It can also trap an investor in a rushed replacement purchase, unwanted debt, poor diversification, or a property that does not fit the family’s long-term needs.

Deferral is not always superior to recognition. The decision should compare after-tax sale proceeds, replacement property quality, estate objectives, cash needs, debt tolerance, management burden, and the investor’s appetite for continued real estate exposure.

A partial exchange, taxable sale, installment sale, or planned recognition year may sometimes produce a better long-term result than forcing full deferral into a weak replacement asset.

5. Ignoring passive activity classification

For high-income taxpayers, classification often controls whether the plan works.

A deduction that cannot be used currently may still be useful later, but it should not be presented as current-year tax savings. The plan should distinguish passive losses, nonpassive losses, suspended losses, and income from activities that may fall outside standard rental treatment.

This is particularly important for short-term rentals, grouped activities, real estate professional status, and mixed operating businesses.

The classification must be planned and documented before the return is prepared. Once the year has closed, the facts may be harder to repair.

6. Letting entity structure dictate strategy instead of support it

Entity structure should preserve planning choices. It should not accidentally block them.

Partnerships, S corporations, disregarded entities, tenancy arrangements, trusts, and holding companies can all affect debt allocation, loss utilization, sale mechanics, transfer planning, and control over timing.

A structure that is easy at acquisition may be restrictive at exit.

For example, a partnership may create flexibility for pooling capital, but it may also create tension if partners disagree on whether to sell, exchange, distribute cash, or hold. A trust may support estate planning, but it can complicate income tax, control, and basis planning if not coordinated. An S corporation may be appropriate for an operating business, but it can be a poor fit for certain real estate holding patterns.

The structure should be tested against the exit plan, not only the acquisition.

The coordinated planning model we prefer

A strong plan should show the taxpayer, asset by asset and year by year:

Taxable income before planning

Usable depreciation versus suspended depreciation

Debt service and refinancing exposure

Projected basis and gain

Exit-year tax character

NIIT exposure

Cash after debt payoff and tax

Alternative exit paths

Entity and ownership constraints

Estate and transfer implications

What must happen before year-end

Which future years should not be overloaded

The goal is not precision for its own sake. The goal is decision clarity.

A high-income investor does not need a projection that looks sophisticated but never informs action. They need a planning model that answers practical questions:

Should we accelerate depreciation this year or preserve basis?

Should we sell one property now and hold another?

Should we exchange, pay tax, or partially exchange?

Should we refinance before sale planning begins?

Should we group or separate activities?

Should we change ownership before a liquidity event?

Should we recognize income now to avoid a worse year later?

Should we stagger exits even if the market offers are attractive now?

Should we accept a taxable result because the replacement property market is poor?

This is the difference between tax preparation and coordinated tax strategy. Preparation records what happened. Strategy shapes what happens next.

Bring us the assets, debt terms, ownership structure, projected tax profile, and likely exit windows so we can evaluate the plan as a portfolio.

Depreciation, Exits, and Florida Planning: What the Bracket Doesn't Tell You

A high tax bracket makes depreciation more valuable — but only if the deduction is actually usable. If the loss is suspended, the property may sell soon, or acceleration creates a larger problem at exit, maximum depreciation is not automatically the right answer. The better question is whether the deduction lands in the right year, against the right income, with a modeled path to disposition.

The same discipline applies to 1031 exchanges. A properly structured exchange defers gain, but it does not erase the underlying tax history. Basis, depreciation history, debt replacement, boot, and future exit obligations carry forward. The exchange is a continuation strategy — not a permanent resolution — and should be evaluated as one.

NIIT compounds both issues at exit. When modified adjusted gross income exceeds the applicable threshold, real estate gains and passive rental income may fall within net investment income. A sale that looks manageable on its own can produce a materially different result when it lands in the same year as business income, a bonus, portfolio gains, or a Roth conversion. The sale year is a planning variable, not just a closing date.

For Florida investors, the absence of state income tax shifts attention toward federal depreciation, NIIT, estate planning, and property-level economics — not away from planning entirely. Homestead and non-homestead assessment rules, insurance exposure, casualty reserves, liquidity, and concentration in local markets all remain consequential. Tax efficiency at the federal level still has to hold up against the real cost of ownership.

Conclusion

Coordinating debt, depreciation, and exit timing across multiple assets is a portfolio-level discipline.

Debt determines how long an investor can hold and what flexibility exists at refinance or sale. Depreciation determines when deductions are taken, whether they are usable, and how basis is reduced. Exit timing determines when deferred tax costs become real and whether they arrive in a manageable year or collide with other income events.

For Florida high-net-worth taxpayers, the lack of state personal income tax does not remove the need for planning. It increases the importance of federal coordination, especially when real estate, business income, passive activity rules, NIIT, insurance risk, property tax economics, and entity structure all interact.

The best plan is not the one with the largest deduction in the current year. It is the one that sequences deductions, debt, liquidity, ownership, and exits so the taxpayer keeps more control over timing, cash flow, and long-term after-tax wealth.

We help Florida investors coordinate debt, depreciation, liquidity, and exits before tax decisions become transaction deadlines.

Multi-Asset Portfolio Exit Planning FAQs

Key questions for Florida real estate investors coordinating asset sales, suspended losses, depreciation, debt, entity structure, and exit-year liquidity.

How should we decide which asset to sell first in a multi-asset portfolio?

We would not start with the highest offer alone. The better sequencing question is which sale produces the strongest after-tax and after-debt result across the full portfolio. That means comparing basis, depreciation history, suspended losses, debt payoff, reinvestment options, NIIT exposure, and whether another asset may already create income in the same year. A lower headline price can sometimes produce a better planning result if it releases losses, reduces concentration risk, or avoids stacking multiple taxable events into one exit year.

Can suspended passive losses change the timing of a real estate exit?

Yes, but they should be modeled carefully rather than assumed to solve the exit-year tax problem. Suspended passive losses may become strategically important when an asset is sold or when passive income exists elsewhere in the portfolio. The planning issue is whether those losses align with the gain, activity classification, and ownership structure involved. We would look at whether the losses are tied to the asset being sold, whether other passive income exists, and whether the exit year already includes other gains or business income.

When should depreciation planning be coordinated with debt refinancing?

Depreciation planning should be revisited before a refinance, not only after acquisition. A refinance can change cash flow, reserve capacity, leverage, and the investor’s ability to hold through the intended tax timeline. If accelerated depreciation lowered current taxable income but the property later faces higher debt service or tighter liquidity, the strategy may become fragile. We would connect projected depreciation benefits with loan maturity, rate exposure, insurance costs, repair needs, and likely exit windows so the tax plan is not dependent on an unrealistic hold period.

How do entity and ownership structures affect exit timing?

Entity and ownership structure can control whether an exit is flexible or constrained. Partnerships, disregarded entities, trusts, S corporations, and holding companies can affect debt allocations, basis, loss utilization, control rights, transfer planning, and partner-level tax outcomes. The issue is not only who owns the asset today. It is whether that structure supports a future sale, exchange, refinance, buyout, or transfer. We would test the structure against realistic exit paths before assuming the portfolio can be unwound cleanly.

Should a Florida investor ever choose to recognize gain instead of deferring it?

Yes, in some cases recognizing gain can be more strategic than forcing deferral. A 1031 exchange or other deferral approach should fit the investor’s debt tolerance, replacement-property quality, liquidity needs, estate objectives, and concentration risk. If deferral requires rushed reinvestment, unwanted leverage, or a weaker asset, paying tax and redeploying capital may be more durable. We would compare the after-tax sale result against the economic quality of the deferral path, not just the tax saved in the transaction year.

How should we plan when several assets may exit in the same year?

The first step is building a tax event calendar before any asset is under contract. We would identify expected gains, depreciation recapture exposure, NIIT exposure, debt payoff, passive loss availability, and other income events in the same year. Then we would test whether one sale should move earlier or later, whether a partial exchange is realistic, whether charitable planning or installment terms fit, and whether refinancing preserves flexibility. The goal is to avoid exit-year compression where several manageable events become one crowded tax year.

How do Florida property taxes and insurance risks affect tax strategy?

They affect the durability of the hold period. A depreciation or deferral strategy may assume the investor can hold an asset for years, but Florida property tax changes, insurance costs, casualty exposure, repairs, and reserve needs can shorten that timeline. If a property must be sold earlier than expected, prior depreciation and debt decisions may produce a different exit result than planned. We would treat these Florida-specific costs as timing variables, not merely operating expenses, because they can influence when and whether the tax strategy works.

What should we review before ordering a cost segregation study?

Before ordering a study, we would review whether the resulting deductions are likely to be usable, whether the asset has a durable hold period, and how the study affects future exit modeling. The study may be valuable, but its value depends on classification, passive income availability, ownership structure, debt terms, and likely sale or exchange timing. We would also consider whether creating larger deductions now could reduce basis in an asset that may need to be sold sooner than expected.