Coordinating Retirement Contributions With Business Profit Volatility

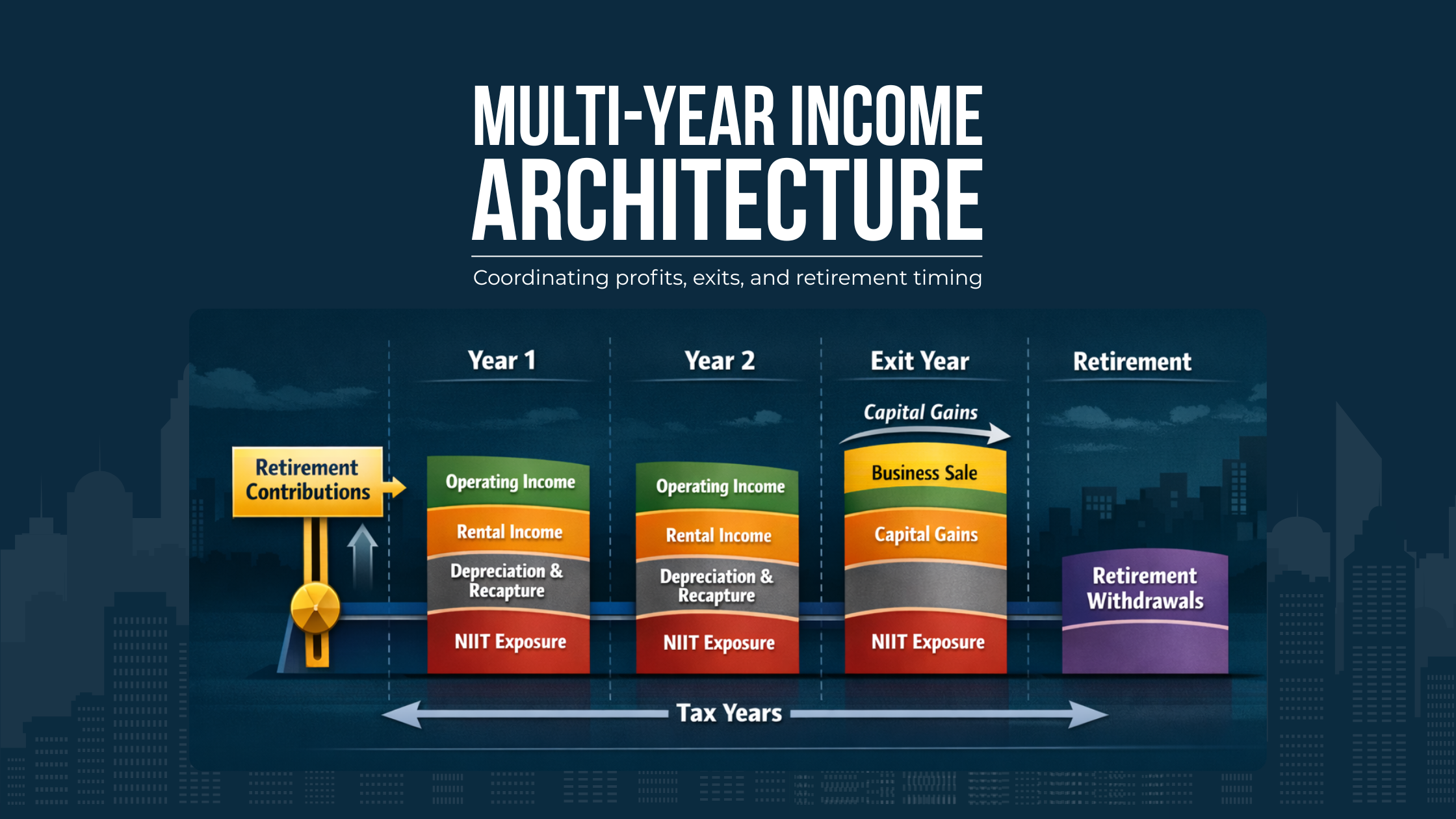

Retirement contributions are one component of a broader income architecture that must be sequenced across operating and exit years.

High-income business owners and real estate investors in Florida rarely earn the same income two years in a row. One year may include a large property disposition, carried interest payout, or unusually strong operating margins. The next may reflect reinvestment, cost segregation losses, or expansion.

Yet retirement contributions are often decided reactively. A CPA calculates available contribution room after year-end and frames the decision as a deduction opportunity rather than a capital allocation decision inside a multi-year tax architecture.

For sophisticated taxpayers paying six figures in federal tax, this fragmented approach creates avoidable bracket compression, NIIT exposure, and recapture inefficiency. In a state with no income tax, the entire retirement strategy sits inside the federal system. That magnifies the impact of income stacking, exit timing, and entity design.

Coordinating retirement contributions with business profit volatility is not about maximizing a single-year deduction. It is about shaping the lifetime tax arc of your income, assets, and exits.

Key Takeaways

Retirement contribution timing should follow multi-year income sequencing, not profit spikes.

NIIT exposure can change the real marginal value of pre-tax contributions in passive-heavy years.

Exit years with depreciation recapture and unrecaptured §1250 gain require pre-transaction modeling, not after-the-fact deferral.

Entity structure determines both contribution capacity and flexibility during volatile cycles.

Defined benefit and profit-sharing plans can backfire when funding obligations collide with real estate capital demands.

The objective is bracket smoothing across decades, not one-year tax minimization.

We’ll assess how unrecaptured §1250 gain and NIIT layering could reshape your bracket in a planned or potential exit year.

The Real Planning Problem: Profit Volatility Meets Static Contribution Limits

Retirement contribution limits are statutory. Business profits are not.

For pass-through owners, real estate investors, and professional practices earning $250k+ annually, income volatility is driven by:

Dispositions and partial portfolio exits

Cost segregation and accelerated depreciation

Refinances and recapitalizations

Promote income and performance bonuses

Insurance proceeds or casualty gains

Expansion or contraction cycles

Contribution limits, whether under a 401(k), profit-sharing plan, or defined benefit structure, do not automatically adapt to these fluctuations.

This creates a strategic tension:

In a peak-income year, maximizing contributions may reduce top-bracket exposure.

In a moderate year, the same contribution may reduce income that would otherwise fall into lower marginal brackets.

In an exit year, contributions may offset recapture but have limited impact on capital gain stacking.

The error is assuming that “maximum allowed” equals “optimal.” In volatile income environments, optimal depends on where income will land over a three- to ten-year arc.

Income Stacking Across Tax Years: Smoothing the Bracket Arc

Contribution timing should respond to income compression and expansion across multiple tax years.

High earners should evaluate retirement contributions through the lens of income stacking.

Ordinary income layers in this order:

W-2 wages (including S corporation wages)

K-1 business income

Rental income (if non-passive)

Depreciation recapture

Other ordinary inclusions

Capital gains and unrecaptured §1250 gain stack differently, but they still interact with adjusted gross income and surtax thresholds.

In a high-profit operating year without dispositions, pre-tax contributions often offset income that would otherwise be taxed at the highest marginal ordinary rate. That can be efficient.

However, if a significant exit is expected in the near term, smoothing income across years may be more powerful than maximizing deductions early.

Second-order sequencing effects to consider:

Large contributions in Year 1 may suppress income below certain phaseout thresholds, but if Year 3 includes recapture and capital gains, marginal rates may spike despite earlier deferrals.

If Year 2 includes cost segregation that temporarily suppresses income, pre-tax contributions in that year may generate lower marginal benefit than in Years 1 or 3.

If installment sale treatment is available for part of an exit, spreading gain may alter which year retirement contributions create the highest lifetime benefit.

Multi-year modeling should compare:

High contribution in Year 1 vs. increased contribution in Year 3

Evenly distributed contributions across three years

Partial Roth contributions in low-income years

Bracket smoothing, not deduction maximization, is the objective.

Understanding NIIT in Volatile Income Years

The Net Investment Income Tax adds a 3.8% surtax layer on certain passive and investment income once income exceeds statutory thresholds. For high-income taxpayers, this often means that rental income, portfolio income, and capital gains are effectively taxed at a higher marginal rate.

Retirement contributions reduce modified adjusted gross income. That can indirectly:

Reduce the amount of investment income subject to NIIT

Prevent additional gains from being pulled into NIIT exposure

Lower overall effective marginal rates on passive income

However, classification drives outcomes.

If you materially participate in a short-term rental activity that qualifies as non-passive under current rules, that income may not be included in net investment income. In that case, reducing MAGI may not meaningfully change NIIT exposure for that activity.

Conversely, if real estate income is passive, NIIT layering increases the marginal benefit of deductions that reduce AGI.

Advanced planning considerations:

In a year dominated by passive capital gains, pre-tax retirement contributions can reduce the base against which NIIT is calculated, but they do not recharacterize the nature of the income.

In an exit year with both recapture (ordinary) and capital gain components, modeling must separate how each layer interacts with NIIT.

For partnership investors receiving K-1 income from multiple sources, netting rules matter. Retirement contributions reduce overall income but do not isolate specific income streams.

The strategic question is not whether NIIT applies. It is how contribution timing shifts the stacking interaction between ordinary income, capital gains, and the NIIT layer.

We can map how passive vs active classification and NIIT exposure affect the real marginal value of your retirement deferrals.

Exit Planning: Depreciation Recapture and Unrecaptured §1250 Gain

Real estate exits often create more ordinary income than expected.

Accelerated depreciation increases the recapture component upon sale. To the extent prior depreciation reduced ordinary income, that benefit may reverse through depreciation recapture at exit. In addition, unrecaptured §1250 gain applies to certain real property depreciation and is taxed at a special capital gain rate, distinct from standard long-term capital gain treatment.

In a high-income exit year:

Recapture stacks on top of operating income.

Unrecaptured §1250 gain stacks within the capital gain structure.

NIIT may apply to the gain components if income exceeds thresholds.

Pre-tax retirement contributions reduce ordinary income, which can offset recapture. That is often where the largest marginal benefit sits in an exit year.

The value of retirement contributions shifts depending on how recapture and capital gains stack in the exit year.

However, several second-order issues require modeling:

If suspended passive losses are released at disposition, they may already offset some of the gain. Additional retirement contributions may have diminished incremental value.

If multiple properties are sold in the same year, recapture may compress into a single high-income spike, overwhelming contribution capacity.

If an installment sale is used, only the gain portion recognized in that year interacts with retirement deferral.

Planning should occur before signing a purchase agreement. Once the tax year closes, sequencing flexibility narrows.

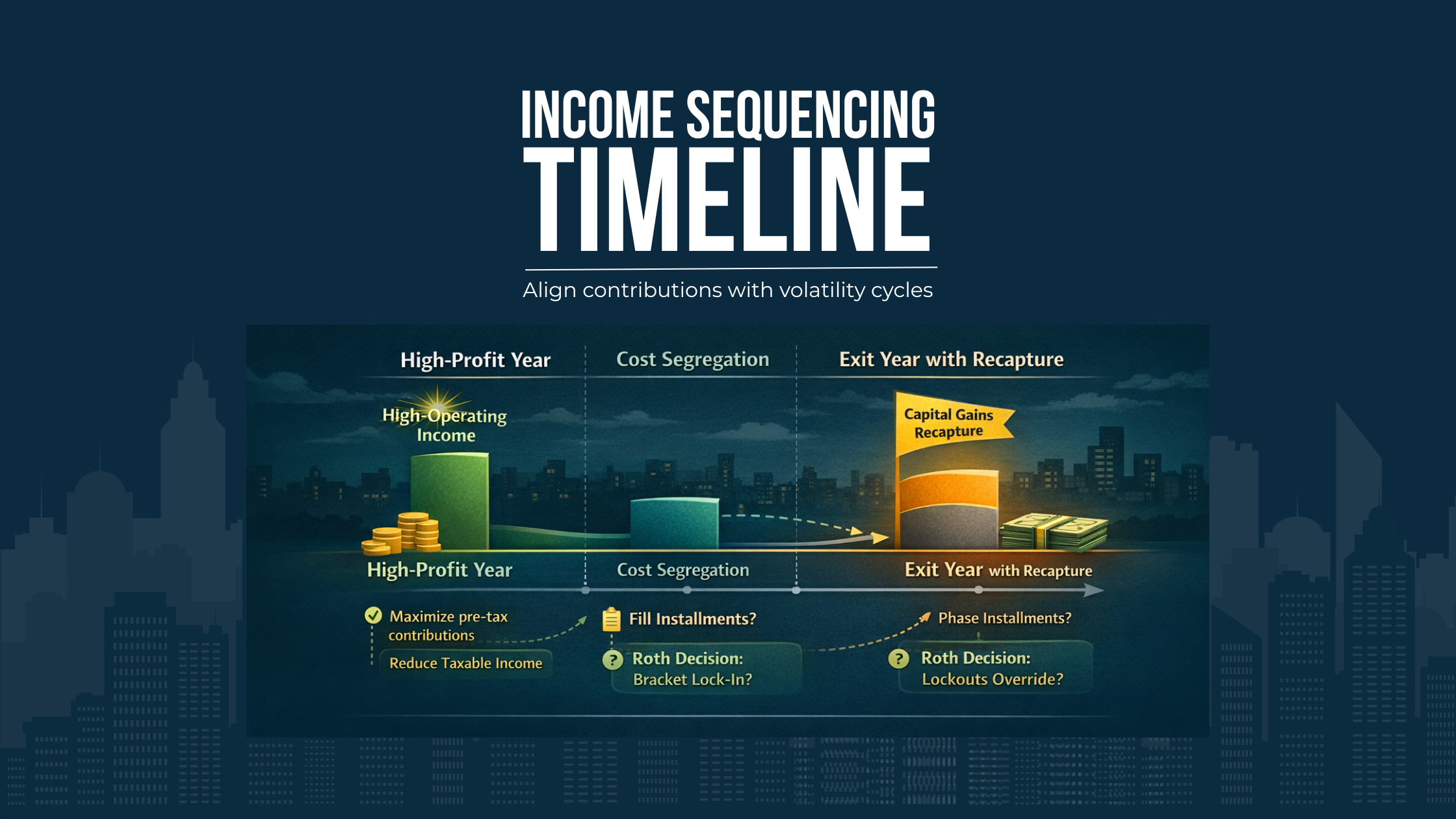

Cost Segregation as a Planning Lever, Not a Tactic

Cost segregation accelerates depreciation into earlier years. That reduces taxable income upfront but increases recapture exposure later.

When layered into retirement tax planning, cost segregation changes the income profile across holding periods.

If Year 1 and Year 2 income are suppressed through accelerated depreciation:

Pre-tax retirement contributions may offset income that is already in lower brackets.

The marginal benefit of additional deferral may be modest.

But at exit:

Recapture may create a surge of ordinary income.

Retirement contributions may have greater value in that year.

Failure modes include:

Maximizing retirement contributions during already low-income years created by bonus depreciation.

Underestimating future recapture and entering an exit year without adequate contribution capacity or liquidity.

Cost segregation is not just a deduction. It is a timing shift. Retirement contributions should respond to that shift.

Entity Structure and Contribution Capacity

Entity design governs both contribution limits and cash flow flexibility.

S corporation owners must consider:

Reasonable compensation levels, which affect wage-based contribution components.

Distribution vs wage balance, which influences self-employment tax and contribution calculations.

Partnerships and LLCs taxed as partnerships introduce:

Allocation variability across partners.

K-1 timing considerations.

Less predictable income patterns tied to asset-level performance.

Defined benefit plans can permit large deductible contributions in high-income years. But they introduce:

Required funding obligations in future years.

Actuarial assumptions that may not align with volatile profit cycles.

Liquidity constraints during downturns.

Second-order considerations:

If a defined benefit plan is established during a peak year and profits decline, required contributions may coincide with capital calls or renovation cycles.

If an S corporation reduces wages to manage payroll taxes, contribution limits tied to compensation may shrink unexpectedly.

Ownership restructurings before a sale can alter who has contribution capacity in an exit year.

Contribution strategy must align with ownership structure and anticipated volatility, not just current-year profit.

Let’s examine whether your entity structure and compensation design support flexible retirement contributions across volatile profit cycles.

Active vs Passive Treatment: Binding at Exit

Activity classification affects both current-year taxation and exit-year economics.

If you materially participate in a rental or short-term rental activity:

Income may be treated as non-passive.

NIIT may not apply to that stream under current law.

If the activity is passive:

Income and gains may fall within NIIT exposure.

Suspended passive losses accumulate.

At exit, suspended passive losses are generally released and can offset gain from the disposition of that activity.

Implications for retirement coordination:

If large suspended losses are expected to offset much of the gain, incremental retirement contributions may provide less marginal benefit.

If participation levels change before exit, classification may shift, altering NIIT exposure.

For investors in syndicated real estate deals, passive treatment is common, and NIIT layering must be assumed in modeling.

Classification analysis is not academic. It changes the marginal effectiveness of contribution timing.

Cash Flow vs Long-Term Tax Efficiency

Maximizing pre-tax contributions reduces liquidity.

For Florida investors, cash flow volatility is real:

Insurance premiums can rise sharply.

Non-homestead property taxes can increase annually.

Capital expenditures tied to storm resilience or code updates may be required.

Short-term rental income can fluctuate with tourism cycles.

A contribution strategy that ignores operating resilience can create pressure to:

Take distributions to fund obligations.

Borrow unnecessarily.

Defer necessary capital improvements.

Long-term tax efficiency sometimes means moderating contributions in order to:

Maintain reserves.

Preserve flexibility for opportunistic acquisitions.

Avoid forced asset sales during weak markets.

Tax efficiency and liquidity must be balanced, not traded blindly.

Retirement, Pensions, and Future RMD Coordination

Pre-tax deferral assumes lower tax brackets in retirement. For real estate-heavy investors, that assumption often fails.

If you retain rental properties into retirement:

Rental income continues.

Depreciation may be limited if properties are fully depreciated.

RMDs add another layer of ordinary income.

RMDs begin at a statutory age under current law. They force distributions regardless of whether funds are needed.

Second-order considerations:

RMDs can push adjusted gross income higher, increasing exposure to NIIT if investment income persists.

Higher AGI can increase Medicare premium surcharges.

If a large real estate exit occurs after RMD age, stacking effects intensify.

In years where taxable income is temporarily suppressed, partial Roth contributions or conversions may reduce long-term RMD stacking risk.

The decision is not simply “pre-tax or Roth.” It is how today’s deferral shapes mandatory income decades from now.

Asset-Based Planning vs Deduction-First Planning

Deduction-first planning asks how to reduce this year’s taxable income.

Asset-based planning asks how assets generate income across their lifecycle:

Acquisition and depreciation

Refinancing and recapitalization

Holding period cash flow

Exit via sale, exchange, or installment

Retirement contributions should reflect that lifecycle.

For example:

If the long-term strategy is repeated §1031 exchanges, recapture may be deferred indefinitely, shifting retirement coordination toward operating income management.

If the strategy includes a portfolio unwind within a defined horizon, exit-year modeling becomes central.

Asset-based planning integrates:

Exit timing

Contribution capacity

Entity restructuring

Capital gain recognition patterns

It replaces annual reaction with structural design.

Coordinating Short-Term Rental Income

Florida’s short-term rental market introduces both opportunity and volatility.

Depending on facts and participation:

Income may be treated as non-passive.

NIIT exposure may differ from long-term rental treatment.

STR income can swing significantly year to year due to:

Seasonality

Market competition

Regulatory shifts

Weather-related disruptions

Planning implications:

In peak STR years, pre-tax retirement contributions may meaningfully offset high ordinary income.

In weak years, maximizing contributions may provide limited marginal benefit and strain liquidity.

Casualty events can trigger insurance proceeds and potential gain recognition, altering income stacking unexpectedly.

STR operators should evaluate contribution timing in light of both income volatility and exit probability.

Multi-Year Modeling: A Three-Year Illustration

Consider a Florida business owner with:

An operating company generating variable profits.

Two rental properties with prior cost segregation.

A planned sale of one property in Year 3.

Year 1 – High Operating Profit

No asset sales.

Strategy: Utilize profit-sharing flexibility. Model defined benefit feasibility but avoid overcommitting if volatility remains high.

Year 2 – Depressed Taxable Income

Large accelerated depreciation from new acquisition.

Strategy: Consider partial Roth contributions or conversions if marginal rates are temporarily lower.

Year 3 – Exit Year

Sale triggers recapture and capital gain.

Strategy: Maximize pre-tax contributions to offset recapture. Model NIIT interaction and evaluate installment sale treatment to manage stacking.

Refinements:

If suspended passive losses exist, incorporate them before deciding contribution magnitude.

If multiple exits are possible, stagger transactions where commercially feasible.

If entity restructuring is planned before sale, align compensation design with contribution capacity.

This is coordinated sequencing, not reactive filing-season planning.

Correcting Common Misuse and Oversights

Even high-income taxpayers make recurring errors:

Treating retirement contributions as automatic deductions without modeling future exit years.

Using cost segregation aggressively without planning for recapture concentration.

Establishing defined benefit plans during peak years without stress-testing down cycles.

Ignoring NIIT layering when evaluating marginal rates.

Assuming retirement income will be lower despite ongoing rental income and RMDs.

Failing to align S corporation wage design with contribution objectives.

Overlooking installment sale or phased disposition strategies that could smooth income.

The consistent pattern is fragmentation. Each strategy is evaluated in isolation rather than inside a unified income model.

Florida-Specific Planning Considerations

Federal Planning Carries Greater Weight

Florida has no state income tax. As a result:

Federal marginal rates and NIIT dominate the analysis.

Retirement contributions reduce federal exposure only.

There is no state-level bracket arbitrage to offset planning errors.

This increases the importance of precise federal income sequencing.

Real Estate Concentration and Recapture Risk

Florida investors often hold multiple properties, increasing cumulative depreciation and potential recapture.

If insurance pressures, market shifts, or portfolio rebalancing trigger multiple sales in a short window:

Recapture can concentrate into a single tax year.

Contribution limits may be insufficient to meaningfully offset the spike.

Staggered exits, installment treatment, and pre-transaction modeling become essential.

Florida’s no state income tax environment heightens federal sequencing risk, especially when insurance and property volatility compress holding periods.

Homestead vs Non-Homestead Property Dynamics

Primary residences benefit from homestead-related property tax protections. Investment properties do not receive equivalent caps.

Rising property taxes on non-homestead assets can:

Accelerate sale decisions.

Compress holding periods.

Alter anticipated exit sequencing.

These shifts affect when recapture and gain materialize, which in turn affects retirement contribution strategy.

Insurance, Casualty, and Climate Volatility

Insurance markets in Florida can introduce:

Premium volatility

Coverage changes

Unexpected capital expenditures

Casualty gains or insurance proceeds can create taxable events depending on how funds are used.

Planning implications:

Maintain liquidity to avoid forced retirement account loans or premature distributions.

Model how unexpected income spikes interact with contribution limits.

Incorporate risk-adjusted holding periods into exit-year projections.

Florida-specific volatility makes flexible, forward-looking coordination more important.

We’ll design a coordinated strategy that sequences retirement contributions, exit timing, and recapture management across multiple tax years.

Conclusion: Retirement Contributions as a Sequencing Tool

Coordinating retirement contributions with business profit volatility requires moving beyond annual deduction logic.

For high-income Florida taxpayers, the dominant variables are:

Income stacking across years

NIIT layering

Depreciation recapture and unrecaptured §1250 gain

Entity structure and compensation design

RMD stacking and long-term bracket trajectory

Retirement plans are powerful tools. But they are not stand-alone solutions.

When contributions are sequenced with cost segregation timing, exit modeling, and liquidity planning, they smooth marginal rates and support lifetime efficiency. When used reactively, they simply reduce one year’s tax bill while leaving structural exposure untouched.

The objective is coordinated, multi-year design. Not maximum deduction. Not isolated tactics. In a Florida environment where federal tax is the primary variable, sequencing decisions carry more weight. A deliberate alignment between how your business and real estate generate income and how your retirement structure absorbs it over time is what ultimately drives sustainable lifetime efficiency.

Frequently asked questions

How far in advance should we model retirement contributions before a planned liquidity event?

Ideally, we begin modeling at least one to two tax years before a potential sale or recapitalization. That allows us to evaluate installment treatment, staggered closings, compensation adjustments, and contribution capacity under different income scenarios. Waiting until the transaction year often limits flexibility. Sequencing decisions such as accelerating income, deferring gain recognition where commercially feasible, or adjusting entity compensation structure require lead time. Retirement contributions are most effective when integrated into the transaction timeline, not layered on after closing.

Should we ever intentionally reduce retirement contributions in a high-income year?

Yes, depending on projected income in adjacent years. If a large exit or recapture event is expected soon, preserving contribution flexibility for that higher-income year may produce better lifetime bracket smoothing. In other cases, high operating income may justify strong pre-tax contributions. The decision turns on multi-year modeling, not emotion. We also evaluate liquidity needs, capital calls, and potential restructuring that could affect contribution limits. Contribution restraint can be strategic when it supports better sequencing later.

How do suspended passive losses change exit-year retirement strategy?

When passive losses have accumulated over time, they are often released upon disposition of the related activity. Those losses may offset gain in the exit year, reducing the amount of ordinary income and capital gain exposed. If much of the gain is already offset, additional retirement contributions may deliver less marginal benefit than anticipated. Before deciding on contribution levels, we model how passive loss release interacts with recapture, unrecaptured §1250 gain, and overall income stacking.

Can installment sale treatment improve coordination between exit gains and retirement contributions?

In certain transactions, installment reporting may spread gain recognition over multiple years rather than concentrating it in one tax year. That can create opportunities to align retirement contributions with the years in which income is recognized. However, installment treatment generally does not apply to every component of gain, including certain recapture elements, and commercial terms drive feasibility. We evaluate whether spreading income recognition enhances bracket smoothing and NIIT management, while also weighing credit risk and liquidity considerations.

How do multi-entity ownership structures complicate contribution planning?

When income flows from multiple entities—such as an operating S corporation, partnership investments, and direct real estate holdings—contribution limits may depend on wages, guaranteed payments, or net earnings from self-employment. Ownership changes, reallocations, or new partners can alter contribution capacity unexpectedly. We also consider controlled group rules and aggregation concepts that may affect retirement plan testing and funding obligations. Multi-entity investors require coordinated modeling so contribution decisions reflect total economic exposure, not a single entity’s income.

Does Florida’s lack of state income tax change how aggressively we should defer income?

Florida’s no state income tax environment increases the relative importance of federal bracket management and NIIT exposure. There is no state-level offset to soften federal spikes. At the same time, Florida investors often hold real estate subject to insurance volatility, non-homestead property tax increases, and potential casualty events. These factors can accelerate exits or create unexpected income. We weigh federal deferral benefits against liquidity needs and real estate concentration risk unique to Florida’s market dynamics.

How should retirement planning adapt if we expect to hold real estate into retirement?

If significant rental income continues into retirement, required minimum distributions may stack on top of ongoing ordinary income. That can compress brackets rather than reduce them. In that scenario, exclusive reliance on pre-tax deferral may not produce the intended long-term result. We evaluate partial Roth strategies in lower-income years, diversification of account types, and projected exit timing to reduce future stacking risk. Retirement coordination must reflect anticipated asset retention, not assume a lower-income retirement by default.