When Tax-Motivated Leverage Increases Long-Term Financial Risk

A durable plan treats leverage as portfolio architecture—where sequencing, structure, and exit modeling determine long-term outcomes.

High-income Florida investors rarely borrow because they lack capital. They borrow because the tax code appears to reward it.

Interest expense can be deductible. Depreciation can suppress taxable income. Cost segregation can front-load deductions. Refinancing can create liquidity without immediate recognition. Those mechanics are real, and for sophisticated taxpayers they can be powerful.

But the planning question is not whether leverage creates deductions. The planning question is whether tax-motivated leverage increases long-term financial risk when you zoom out across multiple tax years, multiple assets, and a realistic exit path.

In Florida, the sequencing stakes often rise. With no state income tax, your planning leverage is concentrated at the federal level: ordinary income stacking, capital gains stacking, depreciation-related gain character, and NIIT layering. If debt and depreciation are pursued primarily for current-year relief, the “cost” often shows up later as constrained optionality: forced timing, higher effective tax in exit years, and cash-flow fragility when conditions shift.

This is not a debate about whether leverage can work. It can. The point is that leverage becomes a long-duration decision with second-order effects: how deductions shift income between years, how status changes impact NIIT and passive loss utilization, how entity structure controls exit flexibility, and how Florida-specific risk factors can compress holding periods and force taxable events.

Key Takeaways

Interest deductions and accelerated depreciation are timing tools. They often reduce current taxable income, but they can increase exit-year exposure through gain character, recapture dynamics, and NIIT layering.

Income stacking is the real determinant of “effective tax.” Exit-year gains rarely land in a vacuum; they stack on top of business income, W-2, portfolio income, and sometimes retirement distributions.

NIIT is not a footnote. For high-income taxpayers, NIIT commonly applies to rental income and disposition gains unless you’ve built and maintained the right activity profile and structure.

Cost segregation amplifies both upside and unwind risk. The more aggressively you front-load deductions, the more disciplined you must be about holding period, refinancing plans, and a credible exit strategy.

Entity and ownership structure decide whether “tax efficiency” is portable. Basis, allocations, grouping, and participation status can either preserve flexibility or create trapped outcomes at exit.

Cash flow is the risk multiplier. Debt service plus Florida insurance volatility, reserves, and casualty risk can force timing decisions that convert a “tax plan” into a taxable liquidation.

We’ll run unwind scenarios that quantify depreciation recapture and unrecaptured §1250 gain exposure under different sale-timing outcomes.

The Psychology Behind Tax-Motivated Leverage

Tax-motivated leverage usually starts with a true observation: in high-income years, every additional dollar of taxable income is expensive. When you’re already paying six figures in federal tax, the marginal dollar feels punitive, and a large interest deduction or accelerated depreciation schedule can feel like control.

The problem is that the tax benefit is visible immediately, while the risk is delayed and often distributed. It shows up later as:

fewer deductions available when you actually need them,

larger depreciation-related gain exposure at exit,

tighter cash flow that reduces timing flexibility,

more dependence on favorable market conditions to refinance or hold.

For sophisticated investors, the most expensive planning mistakes are not “wrong code sections.” They are wrong assumptions about time: assuming you’ll hold longer than you do, assuming your income will be lower at exit, assuming participation status will remain constant, or assuming liquidity will be available when the market is less forgiving.

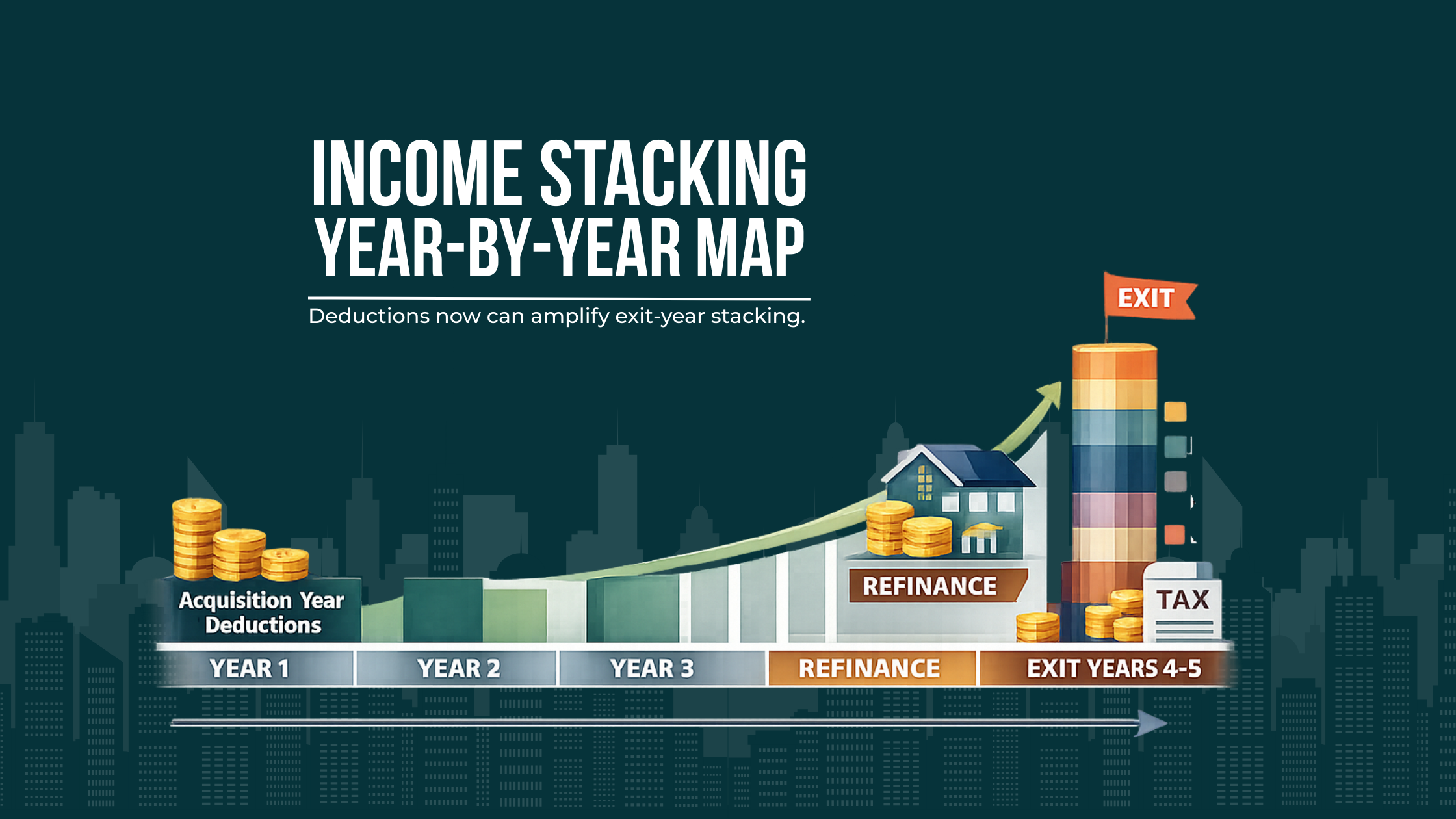

A disciplined leverage strategy begins with a different question: What sequence of years are we trying to build? Acquisition year, stabilization years, refinance years, and exit years are not interchangeable. Tax outcomes vary dramatically by sequencing.

How Income Stacking Changes the Math Over Time

Most investor math is written in a single-year frame:

Sequencing controls effective tax: the exit-year stack is the test, not Year 1 deductions.

“This loan creates interest deductions and reduces this year’s taxable income.”

That’s incomplete because tax rates and surtaxes operate on stacking, not on isolated line items. For high-income taxpayers, the same dollar has different after-tax value depending on what else is happening in that year.

Why exit years are rarely “low-income years”

In real portfolios, exits often coincide with other high-income events:

a business sale or recapitalization,

a concentrated equity portfolio trim,

a professional income spike,

a change in filing status,

retirement distributions beginning (including RMDs),

multiple property sales clustered for operational reasons.

In those years, real estate gain is not simply “capital gain.” It is often a blend of:

long-term capital gain,

depreciation-related gain (including unrecaptured §1250 gain),

potential ordinary-income recapture components (often influenced by prior depreciation methods and cost segregation classifications),

and potentially NIIT on part or all of the investment income.

A sequencing example that matches how HNW investors actually behave

Year 1 (Acquisition + cost segregation):

You buy a property, choose higher leverage, and accelerate depreciation. Taxable income drops meaningfully. You feel the benefit immediately.

Year 2 (Stabilization + refinance):

Cash flow improves, but debt service stays high. Deductions are still strong, but smaller than Year 1. You refinance to access liquidity.

Year 3 (Exit prompted by opportunity or risk):

Insurance costs jump, reserves are strained, or you see a better deployment opportunity. You sell sooner than originally modeled. Now you recognize gain that stacks on top of already-high income, and the accelerated depreciation you “pulled forward” becomes part of the exit-year character problem.

The conclusion is not “don’t do it.” The conclusion is: leverage is a sequencing decision, and the exit-year stack is the test. If your plan doesn’t model the exit-year stack against your likely income trajectory, you’re not doing multi-year planning. You’re doing current-year optimization.

Multi-year planning lens: what we model before adding leverage

Before increasing leverage for tax reasons, we want a credible view of:

how many years you realistically plan to hold (and how often those plans change),

the probability of an exit in a high-income year,

how many other assets could exit in the same window,

whether you’re building suspended losses that are actually usable when you expect them to be,

whether you’re creating a “recapture footprint” that will concentrate later.

This is where tax-motivated leverage increases long-term financial risk: it increases the portfolio’s sensitivity to timing errors.

NIIT Exposure: The Hidden Layer in Leveraged Real Estate

For many high-income taxpayers, NIIT is the difference between “looks fine” and “surprise, it’s expensive.” Competitor content often treats NIIT as a simple surcharge. In planning, NIIT behaves more like a classification and sequencing tax.

When NIIT typically shows up for real estate investors

NIIT generally applies to net investment income, which commonly includes:

net rental income from passive activities,

interest, dividends, and portfolio gains,

and in many cases, gain from disposition of investment property.

Where sophisticated planning gets complicated is that NIIT treatment can hinge on how the activity is classified and how consistently that classification is maintained.

If rental activity is passive, net income is usually exposed to NIIT. If the activity rises to a non-passive trade or business under the rules (and is properly supported), the NIIT analysis can change. The disposition analysis can also change depending on whether the property was held in a non-passive trade or business and whether you materially participated.

We’re careful with language here because the real answer is conditional: NIIT often applies, and the exceptions depend on facts, structure, and activity profile. The planning failure mode is assuming NIIT is irrelevant because you “are active,” without building the documentation and structural consistency that makes the position durable.

Why leverage can increase NIIT sensitivity

Leverage influences NIIT exposure indirectly:

Operational years: Interest expense and depreciation can reduce net rental income, which may reduce NIIT exposure in those years. That feels like “NIIT solved.”

Exit year: Disposition gain can be large and may be included in net investment income, especially when the property is treated as an investment activity. If your modified AGI is already high, NIIT may apply to a large portion of the gain.

Stacking amplification: When gain, depreciation-related components, and other income layers are recognized together, NIIT becomes harder to manage with simple deductions.

NIIT planning that goes beyond “avoid it”

For HNW Florida investors, the practical NIIT conversation is rarely “How do we eliminate NIIT?” It’s more often:

When will NIIT predictably apply, and to which components?

Can we shift recognition into years with less stacking?

Are we maintaining a consistent activity profile (especially if we’re relying on non-passive positioning)?

Do our entity structures and grouping decisions support the classification we’re relying on?

If we expect a business liquidity event, do we want the real estate exit in the same year?

Leverage doesn’t automatically create NIIT risk. But tax-motivated leverage increases long-term financial risk when it causes you to rely on classification assumptions that aren’t engineered to survive the exit-year scrutiny.

Exit Planning: Depreciation Recapture and Unrecaptured §1250 Gain

A common investor narrative is: “Depreciation is free money until I sell, and then I’ll deal with it.” That is a timing mindset, not a plan.

Depreciation changes basis. Basis changes gain. Gain character changes effective tax. And the exit year is where those components become visible all at once.

The exit-year character problem

When you sell real property that has been depreciated, your gain is often segmented into different character buckets. Two concepts matter operationally:

Depreciation recapture mechanics (the “give back” concept that increases taxable gain attributable to prior depreciation)

Unrecaptured §1250 gain (the depreciation-related portion of gain on real property that is taxed differently than standard long-term capital gain)

We intentionally keep this conceptual rather than quoting rates, because the planning impact is not the rate by itself. The planning impact is that depreciation you used to shelter ordinary income can later create gain components that do not enjoy the same favorable treatment as pure appreciation.

Why cost segregation makes unwind harder

Cost segregation can shift portions of a building into shorter-life property. That often increases the share of deductions taken earlier and can increase the portion of gain subject to less favorable character on disposition.

If you hold for a long time, the present value of early deductions can be attractive. If you sell sooner than expected, you may have engineered a larger depreciation-related gain footprint than your exit plan can comfortably absorb.

Unwind scenarios we plan for before increasing leverage

Debt itself doesn’t create recapture. But high leverage often correlates with strategies that accelerate depreciation, reduce current taxable income, and then rely on refinance or long holds to make the math work. The unwind scenarios that create risk include:

Shortened hold period: You sell in year 3–5 instead of year 10–15.

Forced sale: Insurance cost spikes, major capital repair, casualty, or vacancy forces a sale.

Partnership friction: A partner wants liquidity; the asset sells even if you’d prefer to hold.

Refinance constraints: Rates, underwriting, or property performance prevents a refinance that was assumed in the plan.

In each case, the exit-year stack tends to be worse than modeled in a “steady state” plan.

A durable exit plan models not only “the ideal sale,” but also “the likely sale,” “the early sale,” and “the forced sale.”

Cost Segregation and Bonus Depreciation as Planning Tools — Not Tactics

Cost segregation is often presented as a universal good: accelerate depreciation, reduce taxable income now, increase after-tax cash flow. For the right taxpayer and holding profile, that can be true.

But cost segregation is not a strategy. It’s a lever. It magnifies whatever strategy you already have.

The real decision: deduction velocity versus flexibility

Accelerating deductions increases deduction velocity. That can be valuable when:

current income is high,

you expect high taxable income to persist,

you have a credible long-term hold or exchange strategy,

and you have sufficient cash reserves to avoid selling into a bad year.

It can be harmful when:

you’re buying with thin cash flow margins,

your holding period is uncertain,

your portfolio has concentrated insurance and casualty risk,

you’re likely to exit during a business liquidity event.

Bonus depreciation: treat as conditional, not permanent

Bonus depreciation rules can change, phase down, or be modified by Congress. Rather than anchoring planning to any single percentage, we treat bonus depreciation as a conditional input:

If bonus depreciation is favorable when you place property in service, it can accelerate deductions.

If it is less favorable later, it can reduce your ability to create deductions in later years.

Either way, the exit-year character impact remains a core consideration.

A planning guardrail: “exit-first” cost segregation

Before we recommend cost segregation in a leveraged acquisition, we want an “exit-first” view:

What is the likely exit window?

What other income is expected in those years?

Are we planning a taxable sale, a like-kind exchange, or an estate-hold outcome?

How will depreciation-related gain be managed across the portfolio, not just this asset?

When cost segregation is evaluated within that framework, it becomes a strategic tool rather than a one-year tactic.

Entity Structure and How Gains Flow

If you want long-term control over tax outcomes, you need structural control over how income and gain flow. Entity design is not just liability protection; it is exit flexibility.

Why structure matters more in leveraged real estate

With leverage, several structural concepts become binding:

Basis and loss utilization: Debt can increase basis in certain structures, affecting whether losses are currently deductible or suspended.

Allocation flexibility: Partnership agreements determine how income, deductions, and gain are allocated, which matters in exit years.

Capital account economics: Refinances, preferred returns, and distribution waterfalls can create mismatches between economic and tax outcomes if not engineered carefully.

The common failure mode: a “simple” structure that can’t handle a complex exit

Many HNW investors hold properties in:

single-member entities for simplicity,

basic multi-member LLCs that operate like partnerships,

or layered structures for asset protection without integrated tax engineering.

That can work operationally, but at exit it often limits options:

Limited ability to allocate gain in a tax-efficient way among owners.

Limited ability to restructure ownership ahead of disposition.

Grouping and participation consistency problems (which can impact passive loss release and NIIT treatment).

What we want from an HNW-friendly ownership design

For sophisticated Florida investors, structure should serve:

exit optionality (taxable sale vs exchange vs partial dispositions),

income classification durability (passive vs non-passive consistency),

allocation flexibility (within legal and economic constraints),

estate planning integration (transfers, gifting strategies, long-term holds),

and portfolio-level management of depreciation-related gain exposure.

Leverage amplifies structural weaknesses. If the entity cannot adapt, the investor ends up adapting by selling at the wrong time.

Active vs Passive Treatment: Why It Matters Most at Exit

During the hold period, passive losses can be suspended. Investors often assume those suspended losses are a savings account they can withdraw at sale. Sometimes that’s directionally true, but the planning detail is where outcomes diverge.

Status drift is real, and it matters

A taxpayer can be highly involved in real estate in one period and less involved later. Business demands change. Travel changes. Management changes. Participation shifts from direct involvement to oversight. That drift can alter:

whether rental activity is treated as passive,

whether losses are currently usable,

how losses are released at disposition,

and how confidently one can assert non-passive treatment for NIIT analysis. (passive vs active treatment)

Exit-year consequences are often misunderstood

At exit, several things can happen simultaneously:

suspended passive losses may become usable (subject to rules and structure),

depreciation-related gain is recognized with different character segments,

capital gain stacks on top of other income,

NIIT may apply depending on classification and income level.

The mistake is evaluating these as independent. They interact. Passive loss utilization might improve the picture, but not necessarily in the way expected if the gain components are large, the income stack is high, or the structure restricts how losses and gain net.

Planning implication: treat classification like a multi-year asset

We treat activity classification as something that must be maintained and documented across years, not asserted at exit. If the plan relies on being “active,” the plan should also include:

grouping consistency,

governance and management documentation,

and periodic review as facts change.

Leverage makes this more important because it often pushes the investor to depend on tax attributes behaving exactly as modeled.

Cash Flow vs Long-Term Tax Efficiency

In most real-world failures, the tax plan didn’t collapse because the tax code changed. It collapsed because cash flow got tight.

Debt service is not a tax concept. It’s a reality. A strategy that produces meaningful deductions but leaves you under-reserved is fragile. The tax benefit doesn’t pay the insurance bill. It doesn’t fund a major roof replacement. It doesn’t protect you from a vacancy cycle.

Where tax-motivated leverage backfires

Tax-motivated leverage increases long-term financial risk when it:

reduces your ability to hold through volatility,

forces a sale during an unfavorable income year,

drives refinancing dependence in uncertain credit markets,

or concentrates risk across assets that share exposure (insurance, coastal risk, or a common property type).

“Tax efficiency” should be measured after reserves

For sophisticated investors, we recommend modeling tax efficiency after a realistic reserve framework:

operating reserves,

insurance premium volatility reserves,

capital expenditure reserves,

casualty and deductible reserves.

If the property only “works” after tax when reserves are ignored, it’s not tax-efficient. It’s undercapitalized.

Cash flow is also a sequencing control

Strong liquidity and reserves buy you something valuable: timing choice. Timing choice is one of the only levers that reliably improves outcomes across:

capital gain stacking,

depreciation-related gain exposure,

NIIT layering,

and retirement coordination.

Leverage can be strategic, but only if the balance sheet preserves timing choice.

Retirement, RMDs, and Income Coordination

For many high-income professionals, the most dangerous assumption is: “My income will be lower later.” Sometimes it will be. Often it won’t, at least not in the way the tax plan assumes.

Retirement can bring a different type of stacking:

required distributions,

pension income,

deferred compensation payouts,

portfolio income,

and the monetization of real estate holdings that were previously “tax sheltered.”

The sequencing problem: depreciation years versus distribution years

If depreciation and interest deductions suppress taxable income during your peak earning years, you may enter retirement with:

large deferred tax embedded in real estate,

a portfolio of highly depreciated properties,

and an upcoming ramp in retirement distributions.

If you then sell a property in the early RMD years (or during a deferred compensation payout), the stacking can be more severe than expected.

Why leverage complicates retirement flexibility

Leverage can be helpful if the plan is to hold assets long-term and use refinancing strategically. But in retirement, leverage can also:

increase required cash flow at a time you want flexibility,

force property sales if debt service becomes uncomfortable,

reduce your ability to fund charitable or gifting strategies that require liquidity.

A more durable retirement coordination approach

We prefer a retirement coordination model that includes:

a staged disposition plan (not a single “sell everything” year),

scenarios for taxable sales versus exchanges,

timing windows that avoid “collision years” (big distributions + big property sales),

and a portfolio view of depreciation-related gain exposure.

This is where a fragmented advisory approach often fails: the investment plan, the real estate plan, and the retirement distribution plan are optimized separately. The taxpayer experiences the integration problem at exit.

Asset-Based Planning vs Deduction-First Planning

A deduction-first mindset asks: “How do we reduce this year’s tax bill?” That can be appropriate in limited cases, but it is not a strategy for building long-term after-tax wealth.

An asset-based planning framework asks: “What role does this asset play in the portfolio over a decade or more?”

Asset roles drive tax strategy

The right leverage and depreciation posture depends on whether the asset is intended to be:

a long-term hold generating stable income,

a value-add repositioning with a shorter horizon,

a future exchange candidate,

an estate-hold asset intended to transfer rather than sell,

or a liquidity source at retirement.

The mistake is using the same “max deductions now” playbook for every asset type.

The leverage question becomes clearer in an asset-based framework

When you define the asset’s role, leverage becomes easier to evaluate:

If the asset is a short-horizon value-add, aggressive cost segregation plus high leverage can create unwind risk.

If the asset is a long-horizon hold with credible reserves, leverage may enhance after-tax returns without forcing timing.

If the asset is intended for exchange or estate hold, the sequencing considerations shift again.

Asset-based planning doesn’t reject deductions. It places them inside a longer plan where they either compound value or create future constraints.

Correcting Common Misuse and Oversights

Sophisticated taxpayers don’t usually make basic mistakes. They make advanced mistakes that come from optimizing parts of the system without modeling the whole.

1) Treating deferral as if it were elimination

Interest and depreciation typically shift tax across time. If the plan doesn’t explicitly address when and how the tax returns, the “savings” are often overstated.

2) Assuming exit years will be low-income years

Exits frequently happen alongside other liquidity events. Planning should default to a “high-income exit” scenario unless there is a concrete reason to assume otherwise.

3) Over-accelerating depreciation without an unwind plan

Cost segregation can be correct and still be misused. When the holding period shortens or refinancing fails, accelerated deductions often convert into concentrated exit-year exposure.

4) Ignoring structure until the week before closing

Entity structure is difficult to change quickly without consequences. If you wait until a sale is imminent, you’ve likely lost the best structural options.

5) Letting participation status drift without re-modeling outcomes

Activity classification is not “set it and forget it.” Drift can turn an assumed non-passive profile into a passive one, altering NIIT and loss utilization expectations.

6) Under-reserving for Florida-specific volatility

If the plan depends on holding through volatility, reserves are part of the tax plan. Under-reserving is not an operational issue; it is a timing risk that creates tax risk.

7) Confusing portfolio tax optimization with asset tax optimization

A single property can look tax-efficient while the portfolio becomes fragile: clustered depreciation footprints, concentrated recapture exposure, and synchronized exit timing.

The corrective principle is simple: we plan for sequencing first, and deductions second. The code sections matter, but the timeline matters more.

We’ll rebuild your multi-year sequencing around structure, cash flow resilience, and exit-year stacking rather than deduction-first decisions.

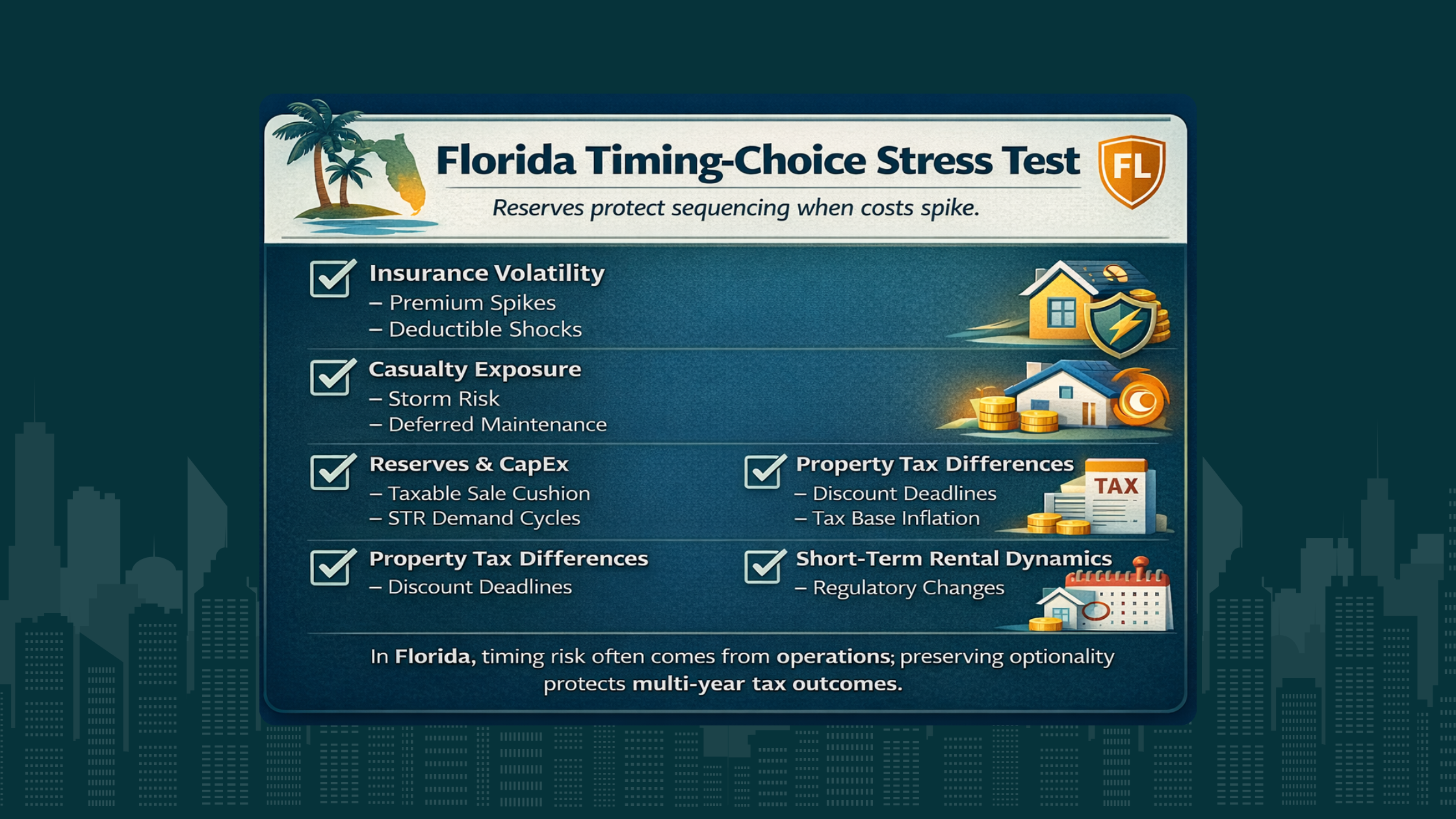

Florida-Specific Planning Considerations

Florida changes the leverage conversation because the risk isn’t spread across state and federal systems. It’s concentrated federally, while real estate operating risk can be higher due to insurance and climate factors.

No state income tax means federal timing decisions carry more weight

Without state income tax, you don’t get a state-level offset or planning lever for ordinary income and capital gains. That increases the importance of:

federal bracket and surtax stacking,

NIIT planning,

and managing depreciation-related gain character at exit.

In other words, Florida’s advantage is real, but it doesn’t make federal planning simpler. It makes federal planning more dominant.

Florida real estate concentration amplifies recapture and §1250 exposure

Many Florida HNW investors hold multiple depreciated properties across:

long-term rentals,

short-term rentals,

small commercial,

and mixed-use assets.

Even if each individual property is manageable, the combined depreciation profile can create a portfolio-level “recapture footprint.” When you begin exiting or rebalancing, that footprint can surface quickly, especially if multiple assets are sold within the same multi-year window.

The planning implication: we track depreciation and expected disposition timing across the entire portfolio, not one asset at a time.

Homestead vs non-homestead property taxes affect holding and conversion decisions

Florida’s homestead framework can make primary residence holding costs behave differently than investment property holding costs. For investors, that matters not as a local law exercise, but as a planning input:

non-homestead properties can experience different assessment behavior,

which can change after-tax cash flow over time,

which can influence whether you hold, refinance, convert use, or sell.

When leverage is high, these holding-cost shifts matter more because they erode the margin that protects timing flexibility.

Insurance, casualty, and climate-driven risk: the Florida timing accelerator

Florida’s insurance volatility and casualty exposure can compress holding periods. In a leveraged property, a sharp increase in premiums, deductible exposure, or required capital improvements can turn a “hold” into a “sell.”

In Florida, timing risk often comes from operations; preserving optionality protects multi-year tax outcomes.

That is the Florida-specific mechanism that makes tax-motivated leverage risky: it increases the probability of a forced taxable event in a high-income year.

We treat insurance planning and reserves as part of tax planning because they protect the single most valuable lever in federal planning: timing.

Integrating Leverage Into a Coordinated Multi-Year Strategy

Tax-motivated leverage increases long-term financial risk when leverage is used to manufacture deductions without a sequencing plan that survives real-world volatility.

A coordinated strategy integrates five elements:

1) Sequence the years before optimizing the lines

We start by mapping likely income years:

operational years,

likely liquidity event years,

retirement distribution ramp years,

and plausible exit windows.

Then we decide when deductions are actually valuable and when they may be wasted or counterproductive.

2) Model exit-year stacks, not just operating-year shelter

The exit-year model should treat gain as layered:

capital gain components,

depreciation-related gain components (including unrecaptured §1250 concepts),

and potential NIIT exposure depending on classification and income level.

If the plan works only under a “low-income exit year,” we treat it as fragile unless that assumption is truly supported.

3) Engineer structure for flexibility, not just compliance

Ownership design should support:

allocation flexibility where appropriate,

durable classification posture,

and feasible exit paths (taxable, exchange, staged dispositions).

Structure is how you preserve options.

4) Treat cash flow and reserves as the timing engine

The most tax-efficient strategy in the code can fail if liquidity forces a sale. We want leverage levels that preserve:

operating resilience,

insurance volatility buffers,

and a credible path through a down year without triggering a forced disposition.

5) Coordinate real estate with business and retirement planning

Real estate should not exit in the same year as:

a major business liquidity event,

concentrated portfolio gain recognition,

or a step-change in retirement distributions,

unless the tax cost is consciously chosen and modeled.

Used intentionally, leverage can enhance long-term after-tax outcomes when it supports asset quality, stabilizes cash flow, and aligns with a realistic hold and exit sequence. Used primarily for current-year deductions, it often converts tax planning into timing dependence.

For sophisticated Florida investors, the goal is not to “avoid tax.” The goal is to engineer a plan where taxes, liquidity, structure, and timing work together over many years, not just this year.

We’ll evaluate NIIT layering and how your activity classification and structure affect what’s exposed in exit years.

Conclusion

Tax benefits are often the easiest part of a leverage story to quantify. The harder part is whether the structure you’ve built preserves options when the timeline changes.

For high-income Florida taxpayers, tax-motivated leverage increases long-term financial risk when it’s designed around current-year deductions rather than a durable sequence: hold years, refinance years, income-spike years, and exit years. Without state income tax, federal stacking is the main event. That means NIIT layering, depreciation recapture and unrecaptured §1250 gain exposure, and gain character at disposition are not side issues. They’re the determinants of long-term after-tax results.

The practical standard we use is simple: if the plan only works in a best-case holding period, a low-income exit year, and stable insurance costs, it’s not a plan. It’s a forecast. A coordinated approach models multiple unwind scenarios, aligns cost segregation and leverage with a credible hold strategy, uses entity and ownership architecture to preserve flexibility, and protects timing choice with reserves and cash flow discipline.

When leverage supports the role an asset plays in the portfolio and fits a multi-year sequencing plan, it can compound efficiently. When it exists mainly to generate deductions, it tends to convert tax planning into timing dependence. The difference isn’t the loan. It’s the integration.

We’ll stress-test whether leverage and cost segregation stay durable when insurance costs rise or holding periods compress.

Frequently Asked Questions

How can I avoid capital gains tax?

For high-income Florida investors, the more actionable question is often how to sequence gains so they land in the right years, with the right companion items. Capital gain recognition is frequently a portfolio event, not a single-asset event, and it can collide with business income, portfolio rebalancing, or retirement distributions. We usually focus on (1) separating “exit years” from other income spikes when feasible, (2) modeling how depreciation-related gain affects the effective tax profile of the sale, and (3) deciding whether a staged exit is more durable than a single, concentrated disposition.

Do you take depreciation in year of sale rental property?

Often, yes, but the planning point isn’t the last-year deduction. It’s how the entire depreciation timeline changes the character and size of gain recognized at exit. Depreciation reduces basis over the holding period, which increases recognized gain when you sell and can create depreciation-related components (including unrecaptured §1250 gain concepts) that don’t behave like pure appreciation. For high earners, the year-of-sale deduction can be overwhelmed by exit-year stacking, NIIT exposure, and recapture dynamics. We treat the final-year depreciation decision as part of an exit-year modeling exercise, not a standalone checkbox.

What is the loophole of depreciation recapture?

We don’t plan around “loopholes.” We plan around unwind scenarios and the reality that depreciation is a timing tool that can concentrate tax at exit. Depreciation recapture and unrecaptured §1250 gain concepts are most costly when the sale happens in a high-income year or when accelerated depreciation was used without a credible hold strategy. The practical solution is sequencing and structure: model the likely exit window, assess how much depreciation-related gain you’re building across the portfolio, and choose leverage and cost segregation levels that preserve the option to hold rather than forcing a taxable sale during an income spike.

Does state tax interact with NIIT?

NIIT is a federal tax, so it doesn’t directly “interact” with Florida state income tax because Florida doesn’t impose one. The Florida-specific nuance is that federal outcomes carry more weight: NIIT layering, capital gain stacking, and depreciation-related gain character become the primary tax levers. That makes timing and classification decisions more consequential. When NIIT applies in an exit year, Florida taxpayers don’t have a state income tax offset to soften the combined burden. We treat NIIT exposure as a sequencing variable and often model it alongside projected exit timing, business income cycles, and retirement distribution years.

How does being a real estate professional affect NIIT?

Being a real estate professional can matter because it may change how certain rental activities are classified, and classification can influence whether rental income is treated as investment income for NIIT purposes. The key is durability: real estate professional status is not a label; it’s a fact pattern that must be sustained, and material participation matters. For sophisticated investors, the planning risk is “status drift,” where your involvement changes over time and the classification you modeled no longer matches reality at exit. We generally treat NIIT exposure as conditional and model outcomes under both passive and non-passive scenarios.

Will rental property LLCs need restructuring?

Sometimes. The trigger is usually not the LLC itself, but whether the ownership and allocation architecture supports your multi-year plan. Restructuring questions tend to surface when (1) leverage and depreciation create large suspended losses, (2) partners have different exit timelines, (3) you need flexibility to stage dispositions, or (4) your classification posture (passive vs active) depends on how activities are grouped and managed. If the current structure locks you into a single exit path or creates mismatches between economics and tax allocations, restructuring can be a strategic move—but it needs lead time and coordination with the exit sequence.

What is the Form 6198 rule?

Form 6198 relates to the at-risk limitations, which can restrict whether losses from an activity are currently deductible based on the amount you’re truly economically exposed to. For leveraged real estate, this matters because deductions that look valuable on paper may not deliver current-year tax reduction if you’re not at risk for the underlying losses. In a multi-year plan, at-risk limits can turn “good” deductions into timing mismatches—losses that suspend and then surface in an exit year where their marginal value may be smaller due to stacking, NIIT, and depreciation-related gain character. We treat at-risk analysis as part of acquisition and leverage design.