Bonus Depreciation vs Straight-Line: Choosing Based on Exit Strategy, Not Just Cash Savings

This framework reinforces that depreciation method should be selected only after the full holding period and exit structure are mapped.

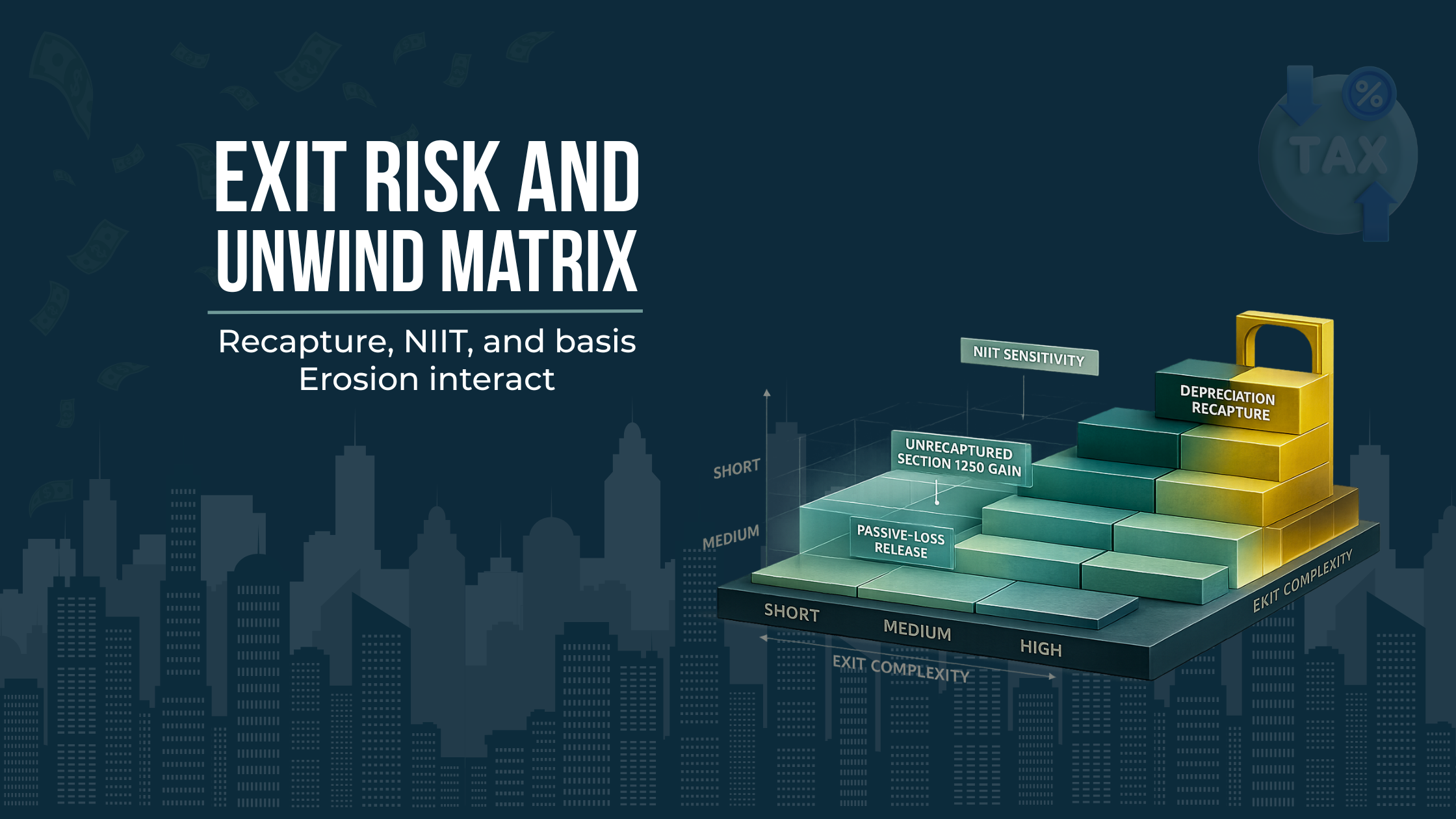

When high-income Florida taxpayers compare bonus depreciation vs straight-line, the wrong question is usually the easiest one to answer: how much can we deduct this year? The better question is whether accelerating depreciation improves the full tax life of the asset once we account for passive-loss limits, NIIT exposure, refinancing, partial dispositions, retirement income, and the tax character of a future sale. In Florida, that issue is sharper because there is no personal state income tax, so more of the planning gain or pain shows up directly on the federal return. Florida also remains structurally real-estate heavy, which means more taxpayers are carrying properties that may eventually trigger basis erosion, depreciation recapture, and unrecaptured Section 1250 gain in already-crowded exit years.

That is why we do not view depreciation method as a one-year election in isolation. We view it as a sequencing decision. Under current IRS guidance, 100 percent bonus depreciation is available for certain qualified property acquired after January 19, 2025, and taxpayers can elect out for a class of property. That means the real planning opportunity is not simply to accelerate whenever possible. It is to decide when acceleration helps, when restraint helps, and when the better answer is to preserve deductions for years where they can offset more expensive income or reduce a later sale-year pileup.

We can evaluate how bonus depreciation vs straight-line fits your multi-year income sequencing, including how passive vs active treatment may change whether deductions are usable now or deferred.

Key Takeaways

The best answer in a bonus depreciation vs straight-line analysis is often determined by the planned exit year, not the acquisition year.

Bonus depreciation creates value when the deduction is usable in the right income bucket and does not simply increase later recapture pressure.

Straight-line depreciation can be the stronger strategic choice when the hold is uncertain, the sale may happen sooner than expected, or future income is likely to be higher than current income.

Cost segregation is most useful when it expands planning options, not when it automatically commits the taxpayer to maximum front-loading.

NIIT, passive-loss rules, and entity structure can decide whether accelerated depreciation produces real tax efficiency or merely shifts tax friction into a later year.

We help map depreciation choices across acquisition, hold, and exit years so recapture and unrecaptured Section 1250 gain are considered before a deduction strategy is set.

The Decision Is About Timing Arbitrage, Not Just Deduction Size

Bonus depreciation accelerates cost recovery. Straight-line spreads it out. That accounting distinction is obvious. The planning distinction is whether the earlier deduction is landing in a year where it offsets income that is both taxable and reachable. A front-loaded deduction has less value when it is trapped by passive-activity limits, absorbed in a lower-income year, or created inside an entity structure that does not line up with the income the household is actually trying to shelter.

This is where many high-income taxpayers get incomplete advice. They are shown the size of the first-year write-off, but not the cost of reducing basis faster, compressing gain character into the exit year, or sacrificing deductions that might be more valuable later. A deduction is not automatically efficient just because it is early. It is efficient when the time value of the tax savings exceeds the later tax cost created by the same acceleration.

Current law also supports a more selective approach than many investors realize. IRS guidance allows taxpayers to elect out of the special depreciation allowance for a class of property, which means the choice is not always binary between “all acceleration” and “no planning.” In the right facts, the better move is to complete the analysis, identify the shorter-life components, and then decide whether full bonus depreciation, partial restraint, or a straighter recovery pattern fits the asset’s expected life cycle.

Why Exit Strategy Should Drive the Analysis

Every depreciation decision reduces basis, and basis reduction matters most when the asset is sold. IRS Publication 544 is explicit that unrecaptured Section 1250 gain is generally the portion of long-term gain on Section 1250 real property attributable to depreciation, while other recapture rules can also convert part of the economics into ordinary income depending on the property involved. That means acquisition-year deductions and sale-year consequences are inseparable.

For a taxpayer with a ten- to fifteen-year hold and a possible step-up-at-death scenario, acceleration can look very different than it does for a taxpayer targeting a three- to five-year reposition and sale. The first profile may care more about current cash flow and less about near-term exit friction. The second may be setting up a sale year that already includes operating income, capital gain, potential NIIT, and suspended-loss release questions. The shorter the likely hold, the less comfortable we are treating the largest Year 1 deduction as the default answer.

This matrix makes clear that the value of accelerated depreciation often rises or falls based on how cleanly the asset can be exited.

Exit planning also forces better questions around unwind scenarios. Are we expecting a full taxable sale, a partial interest sale, an installment structure, a partnership-level restructuring, or a transfer that does not release suspended losses the way the owner expects? IRS instructions for Form 8582 make clear that a disposition of less than an entire interest generally does not trigger the allowance of prior-year unallowed passive losses, while an entire disposition to an unrelated person in a fully taxable transaction can. That distinction alone can change whether bonus depreciation was truly valuable on the way in.

A sophisticated real estate exit planning discussion should therefore begin with the likely unwind path. If the exit is going to be messy, partial, or staggered, aggressive acceleration can create a larger mismatch between when deductions were claimed and when tax friction is actually relieved.

Bonus Depreciation Is a Tool, Not a Default

Bonus depreciation remains powerful under current federal rules, but it is still only one tool inside the broader depreciation timing strategy. The headline percentage can change with legislation, IRS guidance, and placed-in-service timing. That is exactly why planning should focus on decision logic rather than assuming today’s rate will always be the relevant rate.

The best use case for bonus depreciation is not simply “high income this year.” It is high income this year plus the ability to use the deduction efficiently, plus a hold profile where accelerating basis recovery does not create a worse exit-year result. Bonus depreciation tends to work best where ordinary income is genuinely expensive today, passive limitations do not block usage, and the owner is not likely to sell into a compressed gain year in the near term.

It can also work well when the property is part of a larger household plan that includes business income variability, charitable bunching, or one-time liquidity events. But even there, we want to test the alternative. If future years are likely to include strong pass-through income, RMDs, or a business sale, preserving deductions may create a better federal outcome than taking the maximum first-year allowance now.

The deeper point is this: bonus depreciation vs straight-line is not a question about aggressiveness. It is a question about fit.

Straight-Line Depreciation Often Preserves Multi-Year Flexibility

Straight-line depreciation looks less exciting because it does not create the same acquisition-year tax event. But for many affluent taxpayers, that is precisely the benefit. It preserves deductions for later years, matches cost recovery more closely to the operational life of the asset, and reduces the pace of basis erosion that can magnify sale-year friction. IRS guidance continues to treat residential rental real property as straight-line property under the regular system, with shorter-life components potentially carved out through cost segregation where justified.

That slower profile often fits better when current income is already sheltered by other deductions, when a sale is reasonably likely within a few years, or when the taxpayer’s income is lumpy and future years are expected to be stronger. A physician with volatile K-1 income, a founder approaching a liquidity event, or a retired owner entering the RMD phase may derive more value from preserving deductions than from consuming them early.

Straight-line can also reduce behavioral risk. When taxpayers see a very large first-year tax result, they often begin underwriting the asset around that number. That can lead to overconfidence on hold period, refinancing, or projected after-tax returns. A steadier depreciation profile can force a more realistic underwriting discipline.

This is one reason we often prefer to compare straight-line not against a caricature of “no planning,” but against a measured acceleration strategy. Sometimes the best answer is not pure straight-line. It is straight-line on some classes, bonus on others, or a deliberate election out where future year economics are clearly stronger than current year economics.

Income Stacking Across Tax Years Is Where the Real Decision Happens

High-income households do not experience tax as one property and one calendar year. They experience it as layers of W-2 or guaranteed payments, pass-through income, investment income, qualified dividends, capital gains, retirement distributions, and occasional one-time transactions. A depreciation method should be chosen against that full stack, not against the property in isolation.

That is why income stacking across tax years is the real battleground in a multi-year tax planning analysis. A Year 1 deduction may look attractive until we map Year 3 or Year 5 and realize that the sale year could also include carried interest, a large bonus, an earnout payment, required minimum distributions, or the sale of another appreciated asset. The right question is not “How much tax do we save now?” It is “Where do we want deductions to live when the household’s federal income profile is viewed as a sequence rather than a snapshot?”

A strong sequencing model usually tests at least three paths. First, maximum acceleration. Second, moderated acceleration using the optional elections available under current depreciation rules. Third, a slower recovery pattern that preserves deductions for future years. Those paths often produce materially different answers once NIIT, recapture, and passive-loss release are added back to the model.

A sequencing visual helps show when a Year 1 deduction improves long-term efficiency and when it simply shifts tax friction into a later year.

This matters even more in Florida because the absence of personal state income tax means there is less tax diversification in the planning result. If the federal sequence is poorly designed, there is no state ordinary income tax layer that changes the shape of the outcome for individuals. The federal plan carries more weight.

Example: A Three-Year Hold With a Planned Sale

Assume an investor acquires a Florida rental property, commissions a cost segregation study, and identifies meaningful five-, seven-, and fifteen-year property. Under current law, those shorter-life components may qualify for bonus depreciation, but the taxpayer can also elect out for the class if a slower pattern is better.

In Year 1, the owner’s ordinary income is elevated but not unusually so. In Year 2, the owner expects stronger business income. In Year 3, the property is likely to be sold after rent growth and operational cleanup. If we take full acceleration in Year 1, the return may show a much stronger paper loss now, but the later sale could carry more gain attributable to prior depreciation, less remaining shelter during the hold, and possible NIIT in an already high-income year. If we moderate acceleration or preserve more straight-line recovery, we may sacrifice some current cash flow but keep more deductions available during the hold and reduce the pressure in the exit year.

That is not a beginner’s comparison. It is a sequencing problem. The best answer depends on which year has the most expensive income, whether the Year 1 loss is currently deductible, and whether the exit year is likely to be tax-heavy before the property is even sold.

NIIT Can Change the Economics More Than Many Investors Expect

The Net Investment Income Tax applies at 3.8 percent to the lesser of net investment income or the excess of modified adjusted gross income over the statutory threshold amount. For affluent households, that means NIIT is not a footnote. It is a real second federal layer that can alter whether an accelerated deduction produces enough value today to justify a more expensive exit tomorrow.

A common mistake is to analyze a rental property sale only through the long-term capital gain lens. That is incomplete. The sale can include multiple tax characters at once: ordinary recapture in some cases, unrecaptured Section 1250 gain, remaining Section 1231 economics, and possible NIIT if the gain sits inside net investment income. A front-loaded depreciation strategy that barely helps NIIT in the acquisition year but contributes to a much larger NIIT-sensitive gain year later can be a poor trade even if the Year 1 return looked impressive.

This is especially relevant when the property owner also has portfolio income, private fund distributions, or other investment gains in the sale year. NIIT stacks on top of a year that may already be exposed. For many high earners, that extra layer is the difference between a strategy that looks clever in a tax projection and one that actually underperforms over the full holding period.

A second-order issue is timing around refinancing and distributions. Taxpayers sometimes use bonus depreciation to improve after-tax liquidity and then assume a later refinance, sale, or cash-out event will be easy to manage. But if the refinance does not happen, or if the sale arrives while other investment income is high, the NIIT cost of the exit can overwhelm the original assumptions.

Classification and Structure Matter for NIIT

NIIT does not care only about the asset. It cares about the character of the income and whether the activity is part of a trade or business that is passive or nonpassive for the taxpayer. IRS materials explain that rental income may be subject to NIIT, while passive-loss and participation rules operate under their own framework. In practice, that means the same building can produce different NIIT outcomes depending on how the owner participates, whether the rental activity remains passive, and how the gain flows through the structure.

This becomes more important in Florida portfolios with short-term rentals or mixed-use facts. The classification details can change whether current losses are useful, whether future income is passive, and whether the eventual sale lands in a more NIIT-sensitive category. That is why we do not separate net investment income tax planning from depreciation planning. The two are linked by timing, classification, and exit structure.

For high-income households, the operational question is simple: if we accelerate deductions today, what kind of income are we offsetting, and what kind of gain are we setting up later? Without that answer, the NIIT analysis is incomplete.

Cost Segregation Should Be Used as a Planning Instrument

Cost segregation is best viewed as a measurement tool. It identifies shorter-life components and land improvements that may be depreciated over faster recovery periods, including property that may qualify for bonus depreciation under current rules. It does not, by itself, tell us whether we should claim the fastest possible deduction pattern.

That distinction matters because a study can still be valuable even when we do not want maximum front-loading. In sophisticated planning, the study creates options. It tells us what could be accelerated, what remains in a longer-life bucket, and where an election out may preserve more value. For some taxpayers, that optionality is more valuable than the Year 1 deduction alone.

There is also a residual planning benefit that many broad-audience articles miss. Detailed component identification can matter later when renovations, retirements, or partial dispositions occur. That can improve basis tracking and make later-year decisions more precise, even in scenarios where the initial bonus result was intentionally moderated.

We therefore treat cost segregation planning as part of the asset’s long-term tax infrastructure, not a one-season tactic.

Active vs Passive Treatment Can Become Binding at Exit

Passive activity rules can make an otherwise attractive depreciation strategy economically hollow. IRS Topic 425 and Publication 925 make clear that rental activities are generally passive, even if the taxpayer materially participates, unless an exception applies, including real estate professional treatment with material participation under the applicable rules.

That matters because bonus depreciation often creates the biggest apparent benefit in the very year when the loss may be least usable. If the loss is passive and the taxpayer does not have passive income to absorb it, the deduction may be suspended rather than monetized. In that case, the client has not created immediate tax liquidity. The client has created a deferred attribute whose value depends on future passive income or a qualifying disposition.

Exit year is where this becomes binding. IRS instructions for Form 8582 state that an entire disposition to an unrelated person in a fully taxable transaction can free losses from PAL limitation, while a disposition of less than an entire interest generally does not. That means partial sales, internal restructurings, or installment patterns can leave owners with a different release result than they expected.

A related failure mode arises when a taxpayer’s status changes during the hold. A property may begin life in one participation profile and end in another. If we do not model that change, we can overvalue the acquisition-year deduction and undervalue the possibility that the exit-year gain arrives before the suspended losses are optimally released.

This is one reason active vs passive real estate tax treatment belongs in the depreciation conversation from day one. It is not a compliance afterthought. It determines whether the tax result is real or merely postponed.

Entity and Ownership Structure Affect More Than Asset Protection

Ownership structure affects where deductions land, how gain flows, what basis limitations apply, and how much flexibility the owners have when facts change. A taxpayer may hold real estate directly, through a partnership, through an LLC taxed as a partnership, through an S corporation in some operating contexts, or inside trust structures. Each path creates different planning opportunities and different traps.

Partnerships can be flexible, but they also create more complicated basis, allocation, distribution, and sale dynamics. S corporations may be useful in some business settings, but appreciated real estate often raises separate strategic concerns around distributions and exit planning. Trust ownership can change threshold dynamics and concentrate tax effects. The right answer depends on what we need the entity to do at acquisition, during operations, and at disposition.

The connection to entity and ownership structure is direct. A large depreciation deduction is only valuable if it reaches the taxpayer who can use it, in the year it matters, and without creating a future gain character problem elsewhere in the structure. We often see fragmented portfolios where one adviser handled entity formation, another handled the cost segregation study, and a third prepared the return. The result is technically correct in pieces but strategically weak in aggregate.

Entity structure also matters for unwind flexibility. A sale of the property, a sale of an entity interest, a redemption, or a partial transfer can each produce different timing for gain recognition and different suspended-loss outcomes. If the structure limits clean exit options, that should feed back into the original depreciation timing strategy. Aggressive acceleration inside a rigid structure can be much harder to unwind well than the same strategy in a cleaner ownership format.

For high-income investors, the lesson is simple: we do not design depreciation in one meeting and ownership in another. The tax character of both has to be modeled together.

Cash Flow vs Long-Term Tax Efficiency: Where Strategies Backfire

Immediate cash flow is a legitimate objective. Rising insurance premiums, financing pressure, repairs, and reserve needs are real. But cash flow vs long-term tax efficiency is a trade-off, not a synonym. A strategy can improve near-term after-tax cash and still reduce long-term after-tax wealth if it burns through valuable deductions too early and shifts tax burden into a more expensive future year.

This is where accelerated depreciation often backfires in practice. The taxpayer receives an impressive Year 1 result, underwrites the asset around that number, and then either sells earlier than expected or enters a later phase of higher income with fewer remaining deductions. The sale arrives with recapture pressure, NIIT exposure, and less basis shelter than anticipated. What looked like smart tax planning was really a timing advance without enough regard for the unwind.

The longer the taxpayer can hold, the more attractive front-loading can become. The shorter or less certain the hold, the more skeptical we become. In Florida, storm risk, insurance volatility, and changing property-level economics can shorten holding periods whether the investor planned for that or not. That uncertainty should push the analysis toward resilience, not just maximization.

Retirement, Pension, and RMD Coordination Should Not Be Ignored

Depreciation planning often becomes more important, not less, as taxpayers approach retirement. That is because the sale of a property may collide with required minimum distributions, deferred compensation payouts, installment income, portfolio reallocation, or a business transition. A strategy that looked efficient while the taxpayer was purely in accumulation mode can become much less attractive once retirement-related income begins to stack.

This is one reason we do not isolate retirement coordination from real estate planning. If a taxpayer expects meaningful RMDs or pension income in the same period as a likely disposition, preserving deductions into those years may provide more value than maximizing the acquisition-year allowance. Straight-line or moderated acceleration can create a better income-matching profile when the household’s tax picture is transitioning.

There is also an estate-planning dimension. Some competing content points to step-up-at-death outcomes as a reason accelerated depreciation can create permanent benefit in certain families. That can be true in the right facts, but it should be modeled, not assumed, because expected hold period, transfer intent, liquidity needs, and ownership structure all matter. A property that is actually more likely to be sold during life should not be planned as though the step-up is the base case.

Retirement planning therefore changes the depreciation answer in two directions. It can increase the value of preserving deductions for later years, and it can increase the cost of getting the exit year wrong.

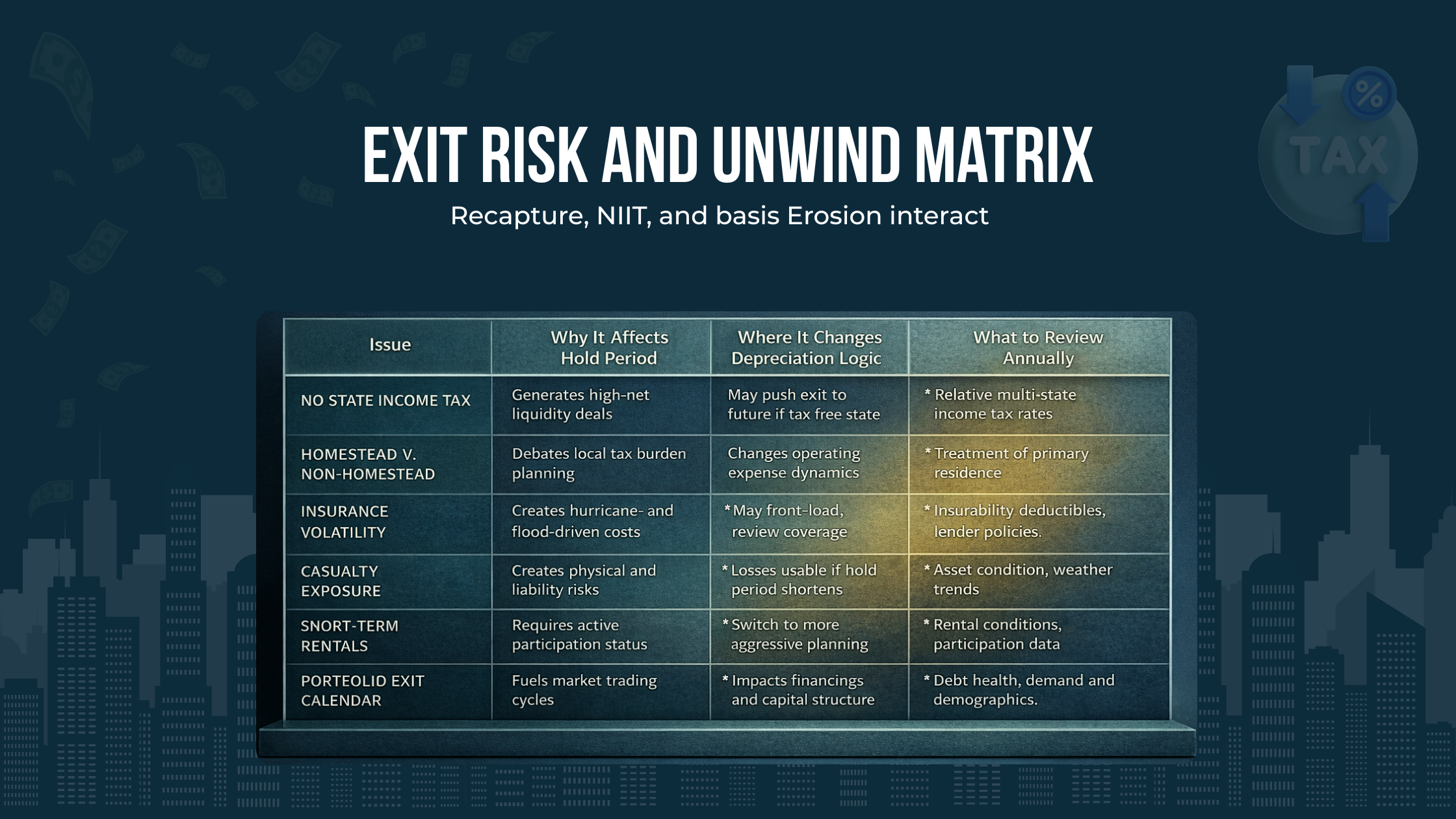

Florida-Specific Planning Considerations

Florida changes the analysis in ways that are easy to underestimate. The first is obvious but important: Florida does not impose personal income tax. That means federal character, federal timing, and federal sequencing carry more weight for individual taxpayers than they would in many other states. If we mis-time depreciation federally, there is less room for a state tax outcome to soften the mistake.

The second is structural concentration. Florida investors are more likely than many taxpayers to hold multiple properties, mixed-use assets, and short-term rental interests. That raises the odds of repeated cost-seg decisions, multiple sale years, and cumulative depreciation recapture exposure across a portfolio rather than on a single asset. The planning conversation has to widen from “Should we accelerate this property?” to “What does acceleration across the portfolio do to our future exit calendar?”

Florida operating realities can shorten holds, change exit timing, and alter whether bonus depreciation or straight-line produces the stronger long-term result.

Property tax structure also affects hold versus sell decisions. Florida’s Department of Revenue explains that homestead property benefits from the Save Our Homes assessment limitation, while non-homestead property is subject to a separate assessment cap. Those differences do not decide the federal depreciation method, but they do change the economic carrying cost of keeping or disposing of a property. A household deciding whether to retain a former residence, convert use, or sell a non-homestead investment asset should model those state-level carrying-cost differences alongside the federal exit analysis.

For investors with concentrated Florida rental portfolios, casualty and climate risk add another layer. Insurance pricing, reserve demands, and storm-related uncertainty can alter expected hold period, renovation plans, and exit timing. If an owner is likely to shorten the hold because operating risk changes, maximum front-loading may age badly. A more resilient federal tax sequencing plan leaves room for the reality that some Florida properties do not hold on the original timeline.

Florida’s short-term rental market adds still more complexity. The operating model may increase the importance of classification, participation, and entity structure. That does not automatically make bonus depreciation better or worse. It does mean the answer is more dependent on facts, and those facts can shift the value of acceleration materially over a multi-year period.

Finally, because Florida attracts relocations and business owners with uneven income, many households have highly variable federal profiles from year to year. That makes static depreciation advice less useful. The better strategy is to build around expected sequencing: acquisition year, stabilization years, refinance years, and exit years.

Correcting Common Misuse and Oversights

The first misuse is treating the largest deduction as the best strategy. It is not. A deduction only has value in context: what income it offsets, whether it is usable now, what it does to basis, and what it causes later when the property exits. Broad-audience articles often stop at “bigger deduction equals better outcome.” For high-income taxpayers, that shortcut is usually too crude.

The second misuse is using cost segregation as though it forces bonus depreciation. It does not. A study can identify faster-recovery components without requiring the taxpayer to take the most accelerated path available. Under current IRS rules, elections can be used to avoid special depreciation allowance for a class of property when the timing is wrong.

The third misuse is underestimating exit-year character. Unrecaptured Section 1250 gain is not just a capital-gain footnote. It is a reminder that prior depreciation claims change the tax composition of the eventual sale. When shorter-life property is involved, ordinary recapture can also become more meaningful than the acquisition-year model suggested.

The fourth misuse is assuming passive losses will be available exactly when the owner wants them. IRS instructions are clear that the release of suspended losses depends heavily on the nature of the disposition. Entire disposition, partial disposition, fully taxable transaction, unrelated party, installment reporting, and entity structure all matter.

The fifth misuse is building tax planning around deductions instead of around assets. The right order is usually hold period, operating model, participation status, financing path, ownership structure, likely exit, and then depreciation. When that order is reversed, the plan becomes reactive even if the return is technically correct.

We can review how your depreciation strategy fits multi-year sequencing, including recapture exposure, NIIT sensitivity, and the likely structure of the eventual sale.

Conclusion

The strongest answer to bonus depreciation vs straight-line usually comes from exit planning, not from the first-year projection. We want to know how the deduction interacts with passive-loss rules, NIIT, ownership structure, future income, and the likely unwind of the asset. Only then can we judge whether accelerating basis recovery creates real long-term tax efficiency or simply borrows deductions from years where they would have been more valuable.

For Florida taxpayers, the stakes are even more federal and more sequence-driven. No personal state income tax means federal timing carries more weight. A real-estate-heavy environment means more exposure to recapture and portfolio-wide exit planning. Insurance and casualty realities mean the original hold period may not survive contact with the market.

That is why we treat depreciation as part of a coordinated, asset-based plan rather than a deduction-first tactic. Sometimes full acceleration is the right move. Sometimes straight-line is stronger. Often the best result comes from using cost segregation and available elections to shape deductions around the years that matter most. The taxpayers who usually win are not the ones chasing the biggest write-off. They are the ones aligning depreciation with the life cycle of the asset, the income profile of the household, and the realities of the eventual exit.

We can assess whether your current depreciation strategy still fits your multi-year plan once passive-loss limits, sale timing, and recapture exposure are modeled together.

Frequetly asked questions

Is bonus depreciation worth it?

Often, only when the timing works. For sophisticated Florida taxpayers, the real question is not whether bonus depreciation creates a larger first-year deduction, but whether that deduction lands in a year where it is actually useful and does not create a worse exit-year result. We usually look at current income, expected holding period, passive-loss limitations, likely sale timing, and whether future years may be more tax-expensive than the acquisition year. If the deduction is trapped, or if the asset may be sold sooner than expected, straight-line or a more selective recovery pattern may produce a better long-term outcome.

Can rental property qualify for bonus depreciation?

Often, not the building itself, but components of the property may qualify when they fall into shorter recovery classes. That is why the more strategic question is not simply whether rental property qualifies, but which parts of the investment may be accelerated and whether that acceleration fits the larger plan. For high-income owners, the answer usually turns on cost segregation, expected hold period, and whether near-term deductions are actually more valuable than preserving basis and future deductions. Qualification is only the starting point. The planning decision is whether taking the fastest deduction improves the full tax cycle of the asset.

What assets qualify for bonus depreciation?

The practical answer for real estate investors is that eligibility often sits in specific components rather than in the building as a whole. Land improvements, certain personal property, and other shorter-life assets are usually where the analysis matters. But qualification alone does not decide the strategy. We still need to evaluate whether those deductions should be accelerated now, especially when the owner has uneven income, passive-loss constraints, or a possible sale in the medium term. For sophisticated households, asset qualification matters less than deduction placement: which year, which entity, and which income bucket will receive the benefit.

What happens to depreciation when you sell a rental property?

Depreciation does not disappear at sale. It changes the character of the gain. Prior depreciation generally reduces basis, which can increase taxable gain when the property is sold, and part of that gain may be taxed under recapture rules or as unrecaptured Section 1250 gain rather than being treated as a cleaner long-term capital gain result. That is why the sale-year model matters so much. If the exit year already includes business income, investment gains, or retirement distributions, prior acceleration can create more tax compression than expected. The key planning issue is not just annual deductions, but what those deductions turn into later.

Can you avoid depreciation recapture on rental property?

In many cases, the better mindset is not “avoid” but “plan for and manage.” Recapture and related gain-character rules are part of the reason acquisition-year deductions should be modeled against the eventual unwind. Sophisticated planning focuses on timing, structure, and exit path: full sale versus partial sale, entire interest versus partial interest, and whether suspended losses may or may not be released in the way the owner expects. The mistake is assuming a large deduction is pure upside. The stronger approach is to decide whether the deduction is worth the later character shift and whether the likely exit year can absorb it efficiently.

Should I put my rental property in an LLC?

It depends on what problem the structure is solving. For tax planning, the question is not just liability protection. It is where deductions will flow, how gain will be recognized, whether ownership interests may be sold or transferred, and how flexible the structure will be when the exit arrives. Some structures improve administrative clarity but create other constraints around basis, allocations, or unwind options. For high-income investors with multiple properties, mixed ownership, or family capital, entity design should be evaluated together with depreciation strategy. A good structure is one that supports both the holding period and the eventual sale.

Does Florida tax rental income?

Florida does not impose personal state income tax, which makes federal sequencing more important for Florida investors than many realize. That does not make Florida “tax-light” in a broad sense. Property taxes, insurance costs, casualty exposure, and short-term rental operating realities can still change the economics of whether a property should be held, improved, refinanced, or sold. For sophisticated owners, Florida’s no-state-income-tax environment means the federal plan carries more weight, not less. If the federal depreciation and exit strategy is poorly timed, there is usually less state-level variation to offset that mistake.