How to Plan a 1031 Exchange for Florida Real Estate in Hillsborough County

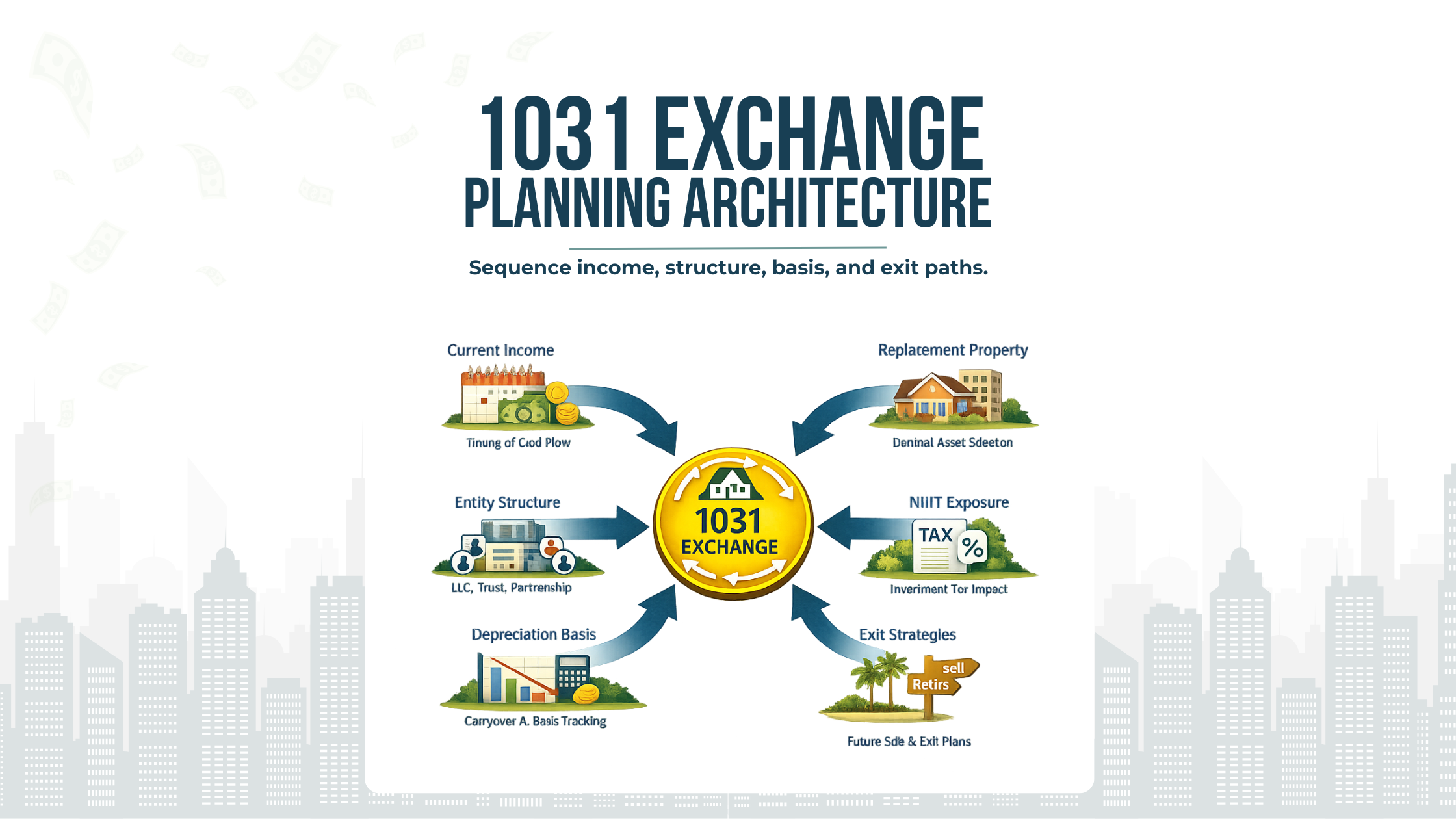

A strong 1031 exchange plan ties the current transaction to future income years, ownership flexibility, and eventual unwind economics.

For high-income Florida investors, a 1031 exchange is rarely just a deferral technique. It is a sequencing decision that changes the timing, character, and flexibility of future taxable events.

That distinction matters more in Florida than many investors realize. Because Florida does not impose an individual state income tax, the planning leverage shifts heavily to federal rules: gain recognition, depreciation history, passive activity treatment, NIIT exposure, debt replacement, and the basis consequences that follow the exchanged property into later years. Section 1031 still allows deferral for qualifying exchanges of real property held for business or investment, and current IRS guidance continues to require strict compliance with the identification, receipt, and constructive-receipt rules.

For Hillsborough County investors, the question is usually not whether a 1031 exchange can be done. The harder question is whether the exchange improves the long-term plan. That includes whether the replacement property reduces or increases concentration, whether it fits with retirement income design, whether it preserves optionality if family members or partners later diverge, and whether the eventual unwind is likely to occur in a more or less favorable federal environment. A well-planned 1031 exchange can preserve capital and widen future options. A rushed exchange can defer tax into a more expensive year, carry old depreciation baggage into a weaker asset, and convert a current gain problem into a future flexibility problem.

We can help evaluate whether a 1031 exchange fits a stronger multi-year sequence, especially when income stacking and NIIT exposure may change the long-term result.

Key Takeaways

A 1031 exchange for Florida real estate works best when it is modeled across several years, not just around the current closing date.

The federal issue is not only capital gain deferral. It is also how NIIT, passive activity treatment, debt replacement, and depreciation history layer into the eventual taxable sale.

Replacement property should be chosen for what it does for the broader plan: diversification, management load, liquidity profile, refinancing capacity, and exit flexibility.

Cost segregation, leverage, and higher-cash-flow assets can improve current economics while making a later unwind more expensive or less controllable.

Ownership structure matters early. If investors, family members, or business partners want different outcomes, those conflicts tend to surface under deadline pressure when options are narrowest.

In Florida, no state income tax does not make planning simpler. It makes federal planning more important, while property tax resets, insurance costs, and casualty risk still shape the hold-or-sell decision.

We can review how entity structure and ownership alignment affect flexibility now and at a later exit, before deadlines start narrowing the available paths.

Why a 1031 Exchange Is a Planning Tool, Not the Strategy

Section 1031 currently applies only to real property, not personal or intangible property, and only when both the relinquished and replacement properties are held for investment or productive use in a trade or business. Property held primarily for sale does not qualify. In a deferred exchange, the replacement property generally must be identified within 45 days and received within 180 days, and the taxpayer cannot have actual or constructive receipt of the sale proceeds. Those are hard structural rules, not loose guidelines.

But the strategic mistake is treating those rules as the strategy itself. They are only the operating envelope. Inside that envelope, the real planning decision is how to reposition appreciated real estate without creating a later tax bottleneck or a weaker portfolio.

For many Hillsborough County investors, that means deciding whether the exchange should reduce local concentration, shift from management-intensive residential assets into professionally managed commercial or net-leased property, improve debt-service coverage, or create a better fit with retirement and estate planning. If the replacement property does not clearly serve one of those functions, the exchange may still defer tax, but it may not improve the plan.

That is why “equal or greater value” should not be the real decision standard. The better standard is whether the replacement asset gives you better long-term economics after considering basis carryover, future recapture exposure, operating risk, and optionality. A larger asset is not automatically a better asset. A higher-yield asset is not automatically a more tax-efficient one. And a local replacement is not automatically the right answer just because the investor knows the market.

An exchange can also fail in ways that are not obvious on the closing checklist. The taxpayer may technically complete the exchange but inherit a replacement property whose financing, reserves, capital needs, or co-owner dynamics make a later taxable exit much harder to manage. That is why we treat the 1031 exchange as one move within a capital allocation plan, not as the plan itself.

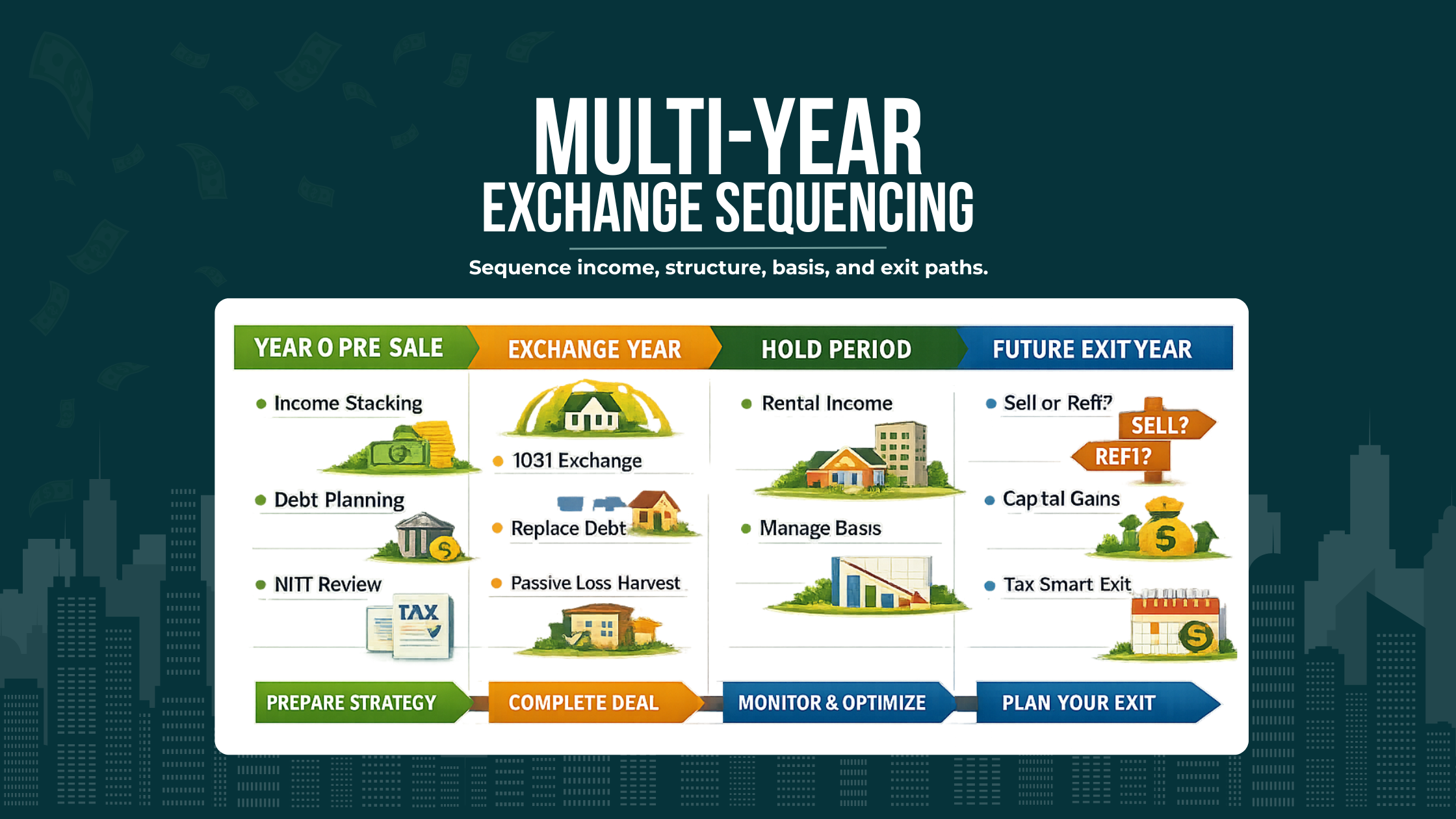

Start With the Exit-Year Stack, Not the Closing Checklist

High-income taxpayers should begin with the likely tax stack in the year gain would be recognized, not with the intermediary documents. If the exchange fails, if debt is not fully replaced, if taxable boot appears, or if the investor later decides not to exchange again, the outcome will be measured against the income profile of that year. For someone already earning substantial business income, salary, or partnership income, the difference between recognizing gain in one year rather than another can materially change the total federal burden, even before considering NIIT and the character of gain tied to prior depreciation.

We usually model at least three windows: the year before the disposition, the exchange year, and the likely unwind year for the replacement asset. That helps identify whether the investor is approaching a business sale, an unusually profitable year, a liquidity event, or the start of retirement distributions. It also helps determine whether a lower-income window may exist for a taxable sale if the exchange is intentionally not continued.

A sequencing example

Assume a Hillsborough County investor owns several long-held rental properties and plans to sell one appreciated property this year. The investor also expects unusually high pass-through business income this year, more normalized income next year, and required minimum distributions to begin two years later. If the exchange is rushed and fails, the recognized gain lands in the highest-income year. If the investor identifies the replacement property earlier, stages financing before listing, and times the sale into the lower-income year, the exchange either succeeds with less stress or fails into a more manageable tax year.

The tax outcome often depends less on the exchange itself than on which year eventual gain, boot, or liquidity needs collide with the rest of the income stack.

The point is not that timing can make gain disappear. It is that timing determines what the gain lands on top of. For affluent investors, that stacking question is often more important than the mechanical fact of deferral.

A second sequencing issue is debt. Many investors focus on replacing purchase price and overlook the tax effect of coming out with less debt or excess cash. If you sell a property with significant leverage and exchange into a lower-debt replacement, the economics may look conservative from a risk perspective but still create recognized gain through taxable boot. That may be the right decision, but it should be deliberate and modeled, not discovered after closing. IRS guidance continues to treat money or non-like-kind property received as current recognition to that extent.

A third sequencing issue is pipeline risk. If the replacement property is not truly ready to close, the 45-day identification rule does not just create deadline pressure. It reduces negotiating leverage. Investors under the clock often accept weaker underwriting, thinner diligence, or tighter financing terms merely to preserve deferral. That is one of the most expensive ways to save current tax.

NIIT Is Not an Afterthought

For high-income taxpayers, net investment income tax is not a side issue. The NIIT applies to certain net investment income and also reaches income from a trade or business that is passive to the taxpayer under Section 469. IRS guidance expressly links NIIT to passive activity status, which means real estate classification, grouping, and material participation are not just annual filing details. They shape the economics of the eventual exit.

That matters because many Florida investors have mixed profiles. They may own long-term rentals, short-term rentals, self-managed buildings, and interests in pass-through entities, while also earning substantial operating income elsewhere. Some of those real estate activities may remain passive. Some may not. Some may look active operationally but still fail the tax tests needed to move the income or gain out of the NIIT framework.

Why this matters in a 1031 context

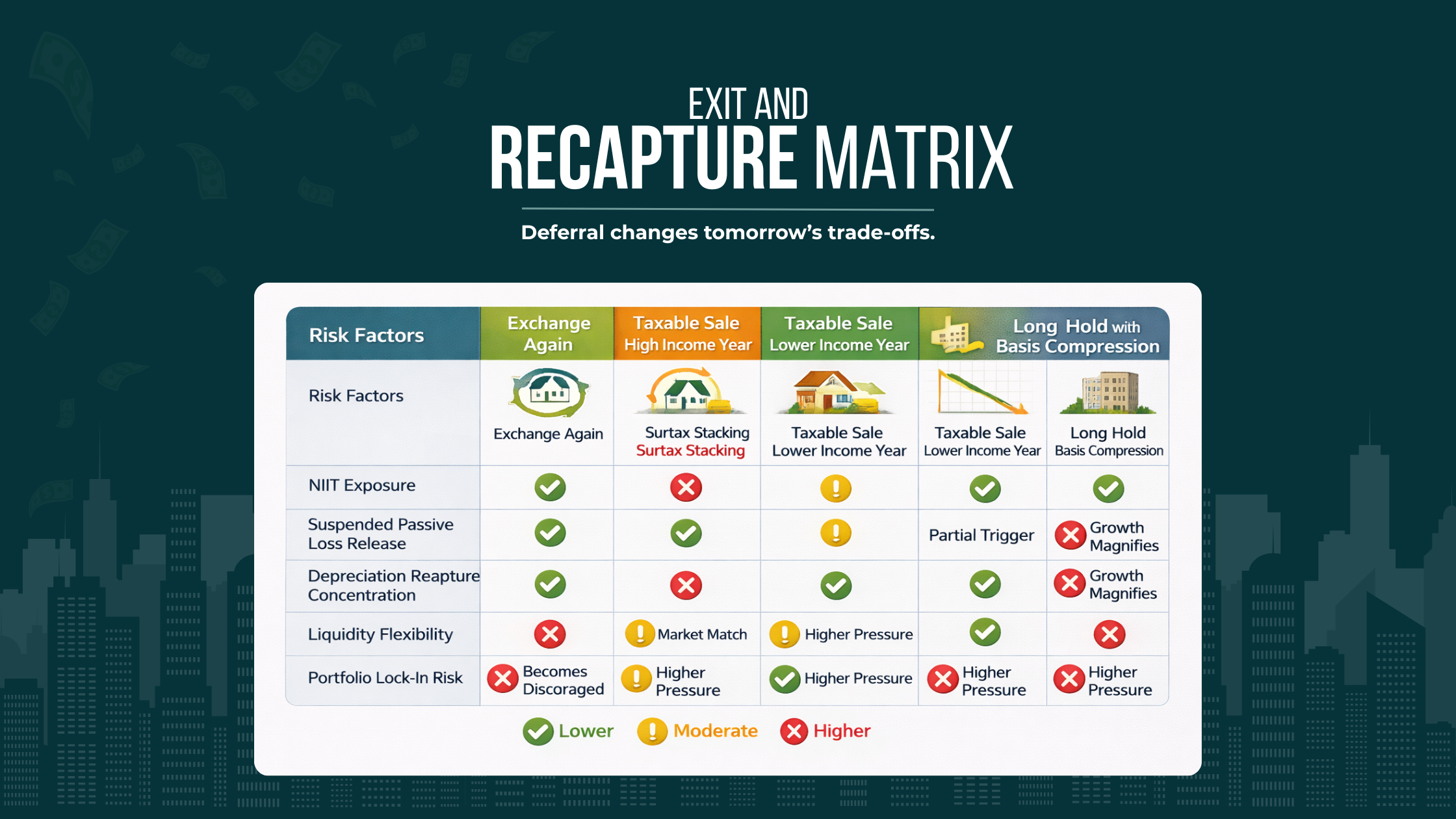

A successful 1031 exchange defers current gain recognition, so the NIIT issue can look postponed. In reality, it is being stored. When a later sale is taxable, when boot is recognized, or when a related restructuring triggers gain, the NIIT consequences return with whatever classification the activity supports at that time.

That is why we do not treat NIIT as a rate add-on to be checked at the end. We treat it as a design issue. If the replacement asset is expected to be largely passive, then the investor should assume the eventual taxable exit may carry NIIT exposure unless the facts later change. If the investor is relying on material participation or real estate professional status, the recordkeeping and grouping logic need to be credible year after year, not assembled after the sale.

A second-order effect is how passive losses interact with a future sale. IRS guidance provides that suspended passive losses are generally allowed when the taxpayer disposes of the entire interest in the passive activity in a fully taxable transaction to an unrelated party. That means a fully taxable exit can unlock losses that a 1031 exchange does not. In some fact patterns, continued deferral postpones not just gain recognition but also the release of suspended losses.

That does not mean a taxable sale is better. It means the comparison has to be holistic. A taxpayer with substantial suspended passive losses, lower projected income in the near future, and no strong reason to keep exchanging may find that the best long-term result comes from using a planned taxable exit rather than carrying the gain and basis history forward again.

A third NIIT issue involves short-term rentals and operational shifts. Some Florida investors move between classic rental activity and service-heavy short-term rental models. The economic asset may still feel like “real estate,” but the tax treatment can change depending on the services provided, the level of participation, and the structure in which the activity is held. That can alter annual loss treatment, NIIT exposure, and the expected benefit of grouping elections. For a sophisticated portfolio, those classification questions should be settled before the exchange is underway.

Depreciation Recapture and Unrecaptured Section 1250 Gain Still Drive the Economics

A 1031 exchange defers gain recognition, but it does not erase depreciation history. Publication 544 continues to treat gain attributable to depreciation on Section 1250 property as a separate concept through unrecaptured Section 1250 gain, and basis rules carry the tax attributes of the relinquished property into the replacement property.

For affluent investors, that means the exchange is not merely postponing one undifferentiated capital gain. It is carrying forward a layered tax problem: built-in appreciation, prior depreciation, basis reduction, and any additional depreciation claimed on the replacement asset. The longer the portfolio compounds through exchanges, the more important the basis map becomes.

The unwind question

Deferring gain can improve current capital efficiency while increasing the cost or rigidity of a later exit, especially when depreciation history compounds across exchanges.

This is where many otherwise sophisticated investors under-model the future. If you exchange out of a fully depreciated or heavily depreciated Florida rental into a new property and later exchange again, the basis baggage does not disappear. It follows the chain. The future taxable disposition may happen many years later, perhaps on a different asset, but the deferred economics remain embedded.

That matters because an investor may feel as if the eventual taxable sale can be handled “later,” when in fact later may include higher ordinary income, retirement distributions, fewer offsetting losses, or a property that is difficult to sell efficiently. If the replacement property is also subjected to cost segregation and accelerated deductions, the current cash-flow benefits can be real, but the future unwind can become more concentrated.

A practical way to think about this is to separate three questions. First, how much gain is currently being deferred? Second, how much prior depreciation is being carried forward into the replacement basis? Third, what is the likely taxable path out of the replacement asset: another exchange, a sale in a lower-income year, contribution to a later structure, or a hold-until-death path if that remains suitable under then-current law? The right 1031 exchange Florida real estate strategy depends on how those three answers fit together.

Another overlooked issue is partial recognition. If boot is recognized during the exchange, current tax may not land only on simple appreciation. Depending on the fact pattern, the recognized amount can sit inside a gain structure that includes depreciation-driven components. That is one reason we do not talk about a “tax-free exchange.” The right phrase is deferred recognition for qualifying gain, with the character and timing of recognized amounts determined by the actual structure.

There is also a portfolio effect. Investors who serially exchange into larger or more institutionally desirable assets often improve cash flow and perceived quality while simultaneously concentrating deferred gain in fewer properties. That can be a sound strategy, but it narrows future exit tools. If one asset eventually carries a very large deferred tax burden, the investor may be reluctant to sell even when the investment thesis weakens. Tax then begins to dictate portfolio design, which is usually a sign that the basis problem has not been managed early enough.

Cost Segregation Should Support the Hold Strategy

Cost segregation can improve early-year after-tax cash flow on replacement property by accelerating deductions into periods where the taxpayer can use them efficiently. But it should support the intended hold strategy, not fight it.

When the replacement property is expected to be held for a long period, refinanced prudently, and possibly exchanged again, accelerated deductions may fit the plan well. When the hold period is uncertain or a taxable sale is plausible in the medium term, those same deductions can deepen future recapture and compress basis faster than the investor intended. Publication 544 and the broader depreciation framework make clear that depreciation history remains central to gain character when property is later disposed of.

This is one of the clearest places where deduction-first planning backfires. A cost segregation study may look excellent in the year it is placed in service, especially for a high earner seeking near-term cash preservation. But if that investor expects to dispose of the asset in a comparatively short window, the study can turn a moderate unwind into a more concentrated one. The better question is not “Can we accelerate deductions?” It is “Does accelerating deductions improve the lifetime result after considering the likely exit path?”

A related issue is use of losses. Accelerated deductions are only as valuable as the taxpayer’s ability to use them. If passive limitations, grouping problems, or projected income changes reduce current usability, the headline benefit may be overstated. In that case, preserving basis and flexibility may matter more than maximizing front-loaded deductions.

Entity Structure Can Improve Flexibility or Destroy It

Entity structure is often chosen for liability protection, financing, or family governance. In a 1031 exchange, it also determines how much room you have when investor goals diverge.

Partnership interests do not qualify as like-kind exchange property, and current IRS guidance continues to treat Section 1031 as applying to qualifying real property, not to ownership interests in entities that own the property. That distinction is where many late-stage problems start. A family LLC or operating partnership may own an appreciated property that is easy to hold but hard to exchange once one owner wants liquidity and another wants deferral.

A disregarded LLC may preserve simplicity for a single owner. A multi-member LLC taxed as a partnership can preserve joint economics during the hold period, but it can become restrictive when a sale is imminent. By that point, restructuring options may exist in theory but carry timing, documentation, and risk-management concerns that are far less attractive under a live contract and a running 45-day clock.

The practical planning issue is governance. Before marketing the relinquished property, owners should know whether everyone wants to exchange, whether anyone expects cash out, whether family branches have different risk tolerances, and whether the replacement property is intended to be held jointly at all. If the answer is no, the structure should be addressed early, not after the buyer is already lined up.

A second-order issue is allocation flexibility after the exchange. Even if all owners agree to defer now, they may not agree on leverage, capital calls, improvements, or eventual disposition. A replacement asset can solve the immediate tax problem while creating a governance problem that is more expensive than the tax that was deferred.

Another entity question involves business owners who hold real estate adjacent to their operating companies. The exchange decision should account for how rent, ownership, and future sale plans intersect. Real estate held in a structure that fits current business operations may not be the same structure that best supports a later family transfer, partial redemption, or taxable disposition.

This is also where TIC structures, direct ownership, and separate vehicles for different family branches can become relevant. The point is not that one format is universally better. The point is that ownership structure needs to be chosen for exit flexibility as much as for current convenience.

Active vs Passive Status Becomes Binding at Exit

Passive activity treatment is often treated as an annual limitation issue. For high-income investors, it becomes much more important in the year of disposition.

IRS guidance states that unused passive activity losses are generally allowed when a taxpayer disposes of the entire interest in a passive activity in a fully taxable transaction to an unrelated party, and it also makes clear that if the disposition is not of the entire interest, or not fully taxable, the result can be different. That means classification and documentation matter not only for annual losses, but also for how much value is available when the property is ultimately sold.

For a 1031 exchange Florida real estate plan, the key implication is that a deferral strategy may postpone the release of suspended passive losses that would have been available in a taxable exit. That may still be the right answer, but it should be compared directly. Investors with meaningful suspended losses should not assume an exchange is automatically superior just because it avoids current gain recognition.

A second issue is that real estate professional status and material participation need to be supportable over time. If the taxpayer expects nonpassive treatment or reduced NIIT exposure, the documentation should exist before the audit file is imagined. High-income taxpayers with multiple entities, mixed-use properties, or short-term rental operations often have more classification complexity than they realize.

Cash Flow Can Conflict With Long-Term Tax Efficiency

A common exchange narrative is simple: defer tax, increase buying power, acquire a higher-income property. Sometimes that works exactly as intended. Sometimes it creates a replacement asset that produces more current cash while narrowing future options.

That trade-off is especially important in Florida. Insurance costs, reserve needs, storm-related repairs, and lender underwriting can change a property’s true cash profile faster than pro formas suggest. A replacement property that looked superior on nominal cap rate may prove weaker once reserves, nonrecoverable costs, and volatility are accounted for. In that setting, maximizing current cash flow can conflict with long-term tax efficiency if the asset becomes too expensive to hold through the planning window.

There is also a leverage dimension. Exchanging into a more leveraged asset may preserve deferral and improve current returns, but it also increases the odds that a future refinance, capital call, or forced sale occurs in a bad tax year. For high earners, resilience often matters more than the highest projected first-year yield.

A useful discipline is to underwrite the replacement property in three scenarios: stable operations, stress operations, and forced-sale timing. If the exchange only works in the stable case, the tax strategy is too fragile.

Retirement, RMDs, and Liquidity Planning Should Be Coordinated

A 1031 exchange can preserve capital for reinvestment, but it can also defer a taxable event into years when retirement distributions or other liquidity needs make the outcome worse.

For investors nearing retirement, the replacement property should be evaluated not only for yield but for administrative load, refinancing flexibility, reserve demands, and sale optionality. An asset that requires active oversight, irregular capital expenditures, or periodic leasing risk may not fit a period when the investor wants more predictable distributions and less management complexity.

This coordination becomes even more important if required distributions from retirement accounts are expected to begin, or if the investor anticipates charitable gifts, family transfers, or a gradual reduction in business income. A taxable real estate exit that lands in the same window as forced retirement distributions can create an unnecessary stacking problem. A more stable property, or a deliberate taxable sale in an earlier lower-income year, may produce the better overall result.

There is also a cash-flow discipline issue. Some investors overuse 1031 exchanges because they prefer not to recognize gain, even when the portfolio would benefit from partial de-risking. That can leave too much wealth in illiquid real estate precisely when retirement planning calls for more controllable liquidity.

A better framework is to ask what role the replacement property serves in the retirement plan. Is it meant to provide predictable income, preserve capital, support heirs with low management burden, or simply continue tax deferral? Those are not the same objective, and a single replacement asset rarely optimizes all of them.

Correcting Common Misuse and Oversights

One common misuse is starting the exchange plan when the purchase contract is already signed. By then, the investor is solving for compliance under deadline pressure rather than solving for the best long-term outcome. The IRS deadlines are strict, but they are not a substitute for planning lead time.

Another is assuming that full tax deferral means full economic success. It does not. A technically valid exchange into a weaker asset can be worse than a taxable sale into a cleaner balance sheet. Investors who overvalue current deferral often undervalue optionality.

A third misuse is treating cost segregation and accelerated deductions as stand-alone wins. They are only wins if the taxpayer can use the deductions effectively and if the later unwind still works. Otherwise they may simply pull tax benefit forward from a future year while increasing complexity and reducing basis flexibility.

A fourth mistake is underestimating debt replacement and closing-cost friction. Exchange economics are sensitive to cash retained, debt reduced, and how transaction costs are handled. Investors who focus only on gross sale value can be surprised by taxable boot or lower deployable equity than expected. The risk is not just extra tax. It is impaired purchasing power under a running exchange clock.

A fifth mistake is failing to distinguish between an investment property and property with too much personal-use character. Vacation homes, second homes, and mixed-use properties require more care than many articles suggest. The IRS has published a safe harbor for certain vacation-home fact patterns, but that is not the same as saying any lightly rented Florida property cleanly qualifies. Qualification depends on actual use, holding pattern, and facts.

A sixth oversight is assuming a reverse exchange is merely a more convenient version of a standard exchange. Reverse exchanges may be useful when the right replacement asset appears before the old property is sold, but they involve a different safe-harbor framework and can add financing, title, and execution complexity. They are planning tools, not emergency fixes.

Finally, many high earners still think too much in terms of “avoiding tax this year” and not enough in terms of “controlling the lifetime sequence of taxable events.” The second lens generally produces better decisions.

We can help map how depreciation recapture, unrecaptured §1250 gain, and suspended passive losses may shape the economics of a future taxable unwind.

Florida-Specific Planning Considerations for Hillsborough County Investors

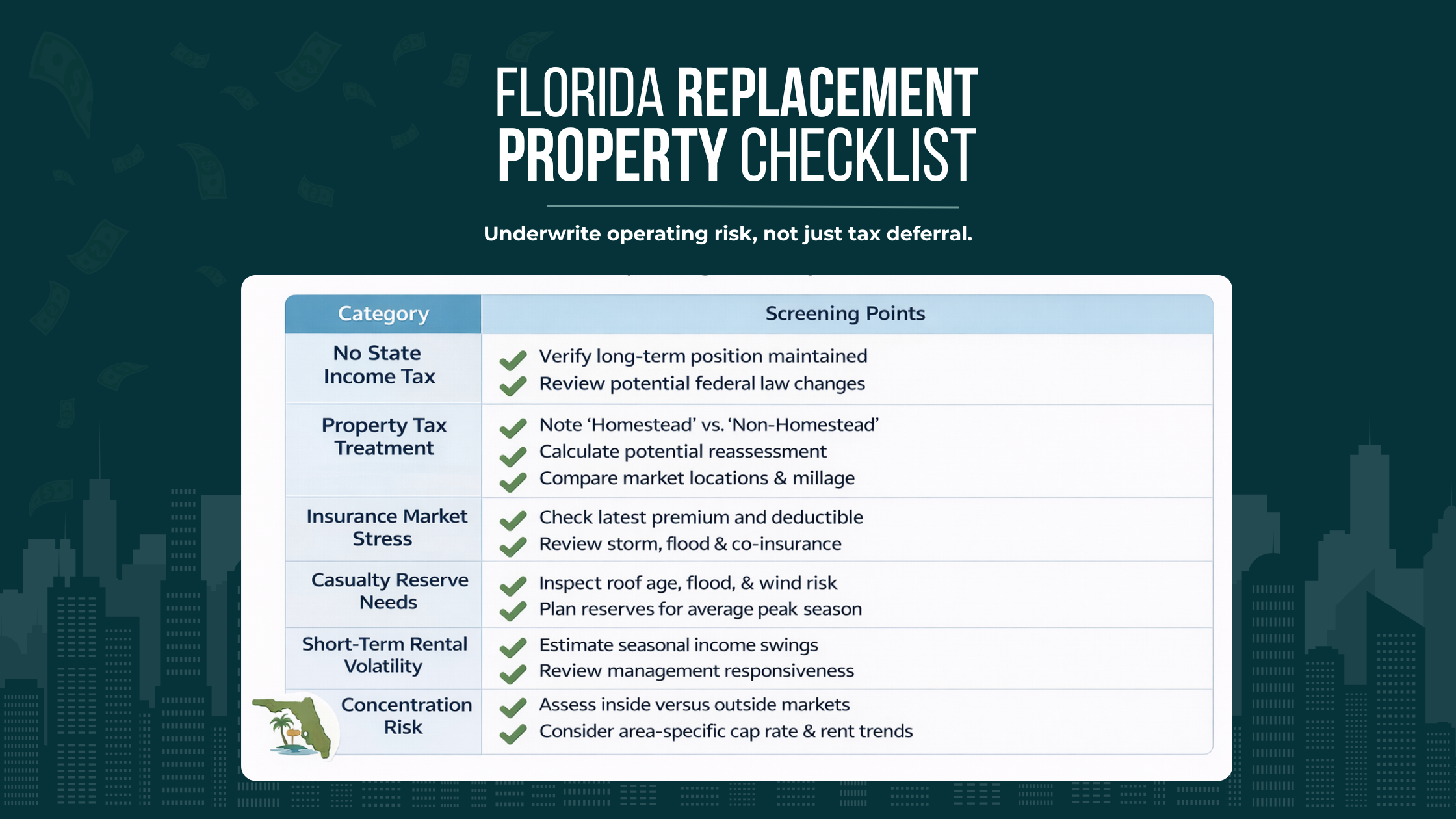

Florida’s no-individual-state-income-tax environment changes the planning equation because it concentrates attention on federal outcomes. There is no separate Florida personal income tax layer to offset, defer, or arbitrage around. That makes federal capital gain recognition, NIIT, depreciation history, passive-loss utilization, and future exit-year income stacking proportionally more important.

At the same time, Florida is not tax-neutral from a real estate holding perspective. Property taxes, insurance costs, and casualty exposure remain economically significant. In Hillsborough County, homestead and non-homestead treatment can produce materially different hold economics, and a transfer can reset assessed value dynamics in ways that matter to long-term underwriting. The local property appraiser explains that non-homestead and non-residential property are not eligible for the Save Our Homes limitation, and a conveyance generally resets the prior owner’s homestead limitation beginning the following year.

That matters even when the exchanged property is not homesteaded. Many affluent Florida households own a mix of homesteaded residences, non-homesteaded rentals, and business-use property. Decisions about where to allocate capital should reflect the total property-tax posture of the household, not just the tax basis of the property being sold.

Florida real estate concentration is another issue. Investors in Hillsborough County often know their local submarkets well, which can create a bias toward reinvesting locally. But a 1031 exchange is one of the few moments when diversification can be achieved without immediate gain recognition. Exchanging one Hillsborough property into another Hillsborough property may still be correct, but it should be chosen because it improves the portfolio, not because it is familiar.

In Florida, a replacement property should be tested for resilience under insurance, casualty, and property-tax realities, not just for whether it preserves current deferral.

Insurance and casualty risk deserve dedicated attention. Storm exposure, premium volatility, deductibles, reserve requirements, and lender responses to those factors can change the viability of a hold strategy much faster than a spreadsheet built at closing will show. For Florida investors, the replacement property should be underwritten not just for stabilized operations, but for resilience under a disrupted insurance market or casualty event. That includes asking whether the property can realistically be held long enough to justify carrying deferred gain and old depreciation history into it.

Florida also has a large short-term-rental footprint, which introduces another layer of planning. Some assets may feel operationally attractive because they produce strong cash flow in peak periods, but they can create more variable classification, more management burden, and less predictable retirement fit. For some investors, exchanging out of that volatility into a lower-maintenance asset is the real value of the transaction. For others, the operating upside justifies the complexity. Either way, the tax planning should follow the operating truth, not the other way around.

A final Florida-specific point is liquidity reserves. In a state with meaningful weather and insurance risk, all available exchange equity should not automatically be pushed into acquisition. Full reinvestment may preserve maximum deferral, but it can also leave the investor under-reserved for real operating shocks. In some cases, accepting limited current tax to preserve stronger liquidity may produce the more durable long-term outcome.

The Better Question: What Should the Replacement Property Do for the Plan?

Before executing a 1031 exchange for Florida real estate in Hillsborough County, the most useful question is not whether the relinquished property has a large gain. It usually does.

The better question is what the replacement property should accomplish over the next phase of the plan. Should it reduce management intensity? Improve diversification? Strengthen debt coverage? Fit with retirement distributions? Create a cleaner ownership structure for heirs? Preserve optionality for a later taxable sale in a lower-income year?

If the answer is unclear, the exchange may still be mechanically possible, but the strategy is not finished. Replacement property is not just where deferred gain goes. It is where the next set of constraints begins.

Seen that way, a 1031 exchange Florida real estate strategy is less about avoiding recognition today and more about choosing which future set of trade-offs you want to live with. That perspective usually produces better asset selection, better entity design, and fewer surprises when the portfolio eventually needs liquidity.

We can compare current cash flow against long-term tax efficiency so the replacement property supports the broader plan instead of only preserving near-term deferral.

Conclusion

Planning a 1031 exchange for Florida real estate in Hillsborough County is not about mastering one tax form or meeting one set of deadlines. It is about sequencing. The investor needs to understand what year the gain would otherwise land in, how NIIT and passive activity rules shape the ultimate tax burden, how depreciation history carries forward, how entity structure affects flexibility, and whether the replacement property strengthens the broader plan.

That is why the best 1031 exchange plans are rarely transaction-first. They are multi-year and asset-based. They account for current income, future distributions, ownership alignment, debt strategy, and Florida-specific operating risk. They also recognize that current deferral and long-term efficiency are not always the same thing.

For high-income investors, the real objective is not just to defer tax. It is to decide when gain should be recognized, what type of property should carry deferred basis forward, and how much flexibility should be preserved for later years. When those questions are answered first, the exchange becomes a useful tool. When they are ignored, the exchange can become a very expensive form of postponement.

We can help structure a 1031 exchange around multi-year outcomes, including debt replacement, passive vs active treatment, and future liquidity needs.

Frequently asked Questions

How long do you have to hold a property before doing a 1031 exchange?

There is no single statutory minimum holding period written into Section 1031 for every exchange, but the tax issue is whether the property was actually held for investment or productive use in a trade or business. That makes timing a facts-and-circumstances question, not just a calendar question. For sophisticated Florida investors, the better analysis is whether the holding period, leasing history, operational use, and pre-sale behavior support investment intent if the file is reviewed later. This becomes more important when the property had mixed use, was recently converted, or may be part of a broader multi-year repositioning plan.

What are the disadvantages of a 1031 exchange?

The real disadvantages are usually strategic rather than mechanical. A 1031 exchange can narrow liquidity, force reinvestment under deadline pressure, preserve concentration in the wrong market, and carry forward a larger deferred tax burden than the investor intends. For high-income taxpayers, deferral can also postpone gain into a year with less favorable income stacking, fewer offsetting losses, or more retirement-related taxable income. In Florida, the trade-off is sharper because there is no personal state income tax layer to optimize around, so the federal consequences and the asset-allocation consequences tend to carry more weight.

Can you do a 1031 exchange between states?

Yes. At the federal level, qualifying U.S. real property can generally be exchanged for other qualifying U.S. real property in a different state. For Florida investors, that means a Hillsborough County property does not need to be replaced with another Florida property just to preserve federal exchange treatment. The more sophisticated question is whether crossing state lines improves the plan by reducing concentration, changing cash-flow characteristics, or creating a better long-term exit profile. Florida’s no-state-income-tax environment may make an outbound exchange feel less costly emotionally, but the decision should still be driven by federal planning, operating risk, and future unwind flexibility.

What happens to depreciation recapture in a 1031 exchange?

In a properly structured 1031 exchange, depreciation recapture is generally deferred rather than eliminated, because the basis history of the relinquished property carries into the replacement property. For a high-net-worth investor, that means the exchange preserves today’s cash but can enlarge tomorrow’s unwind problem if the replacement asset is later sold in a taxable transaction. The planning issue is not only whether recapture is deferred, but when it is most likely to reappear and what it will be layered on top of at that time. Serial exchanges, cost segregation on replacement property, and a shorter-than-expected hold can all make that later exit more concentrated.

How long can you defer capital gains with a 1031 exchange?

A 1031 exchange does not create a fixed federal “deferral term.” Gain remains deferred until a later taxable event occurs, which may be a sale, receipt of boot, a failed later exchange, or another transaction that triggers recognition under the facts at that time. For planning purposes, that means the key issue is not the duration of deferral by itself, but what exit path is most likely: another exchange, a taxable sale in a lower-income year, or a longer hold that keeps deferred gain embedded in the property. Sophisticated investors should evaluate deferral as part of a sequence of future options, not as a permanent answer on its own.

Can an LLC do a 1031 exchange?

Often yes, but the real issue is who the taxpayer is for exchange purposes and whether that same taxpayer is both disposing of the relinquished property and acquiring the replacement property. A single-member LLC is often disregarded for federal tax purposes, while a multi-member LLC is often taxed as a partnership, which can create much more friction when members want different outcomes. For sophisticated ownership groups, the planning problem is less about whether an LLC can exchange in theory and more about whether the current structure preserves flexibility when one owner wants cash and another wants continued deferral. That analysis should happen before the sale process starts.

What are Florida-specific rules to consider in a 1031 exchange?

The exchange rules themselves are federal, but Florida changes the surrounding economics. The absence of individual state income tax means federal capital gain treatment, NIIT, and depreciation history often matter more to the total outcome. At the same time, Florida property taxes, homestead-related assessment limits, insurance volatility, casualty exposure, and the economics of short-term rental activity can materially affect whether the replacement property is actually suitable for a long hold. For Hillsborough County investors, the better question is not whether Florida has a special exchange regime, but whether Florida’s operating environment changes the hold-versus-sell decision enough to alter the best replacement strategy.