Florida No Property Tax Bill? What High-Income Owners Need to Plan for Instead

For high-income Florida owners, the strongest results usually come from coordinating local carrying costs with federal income character and exit timing over several years.

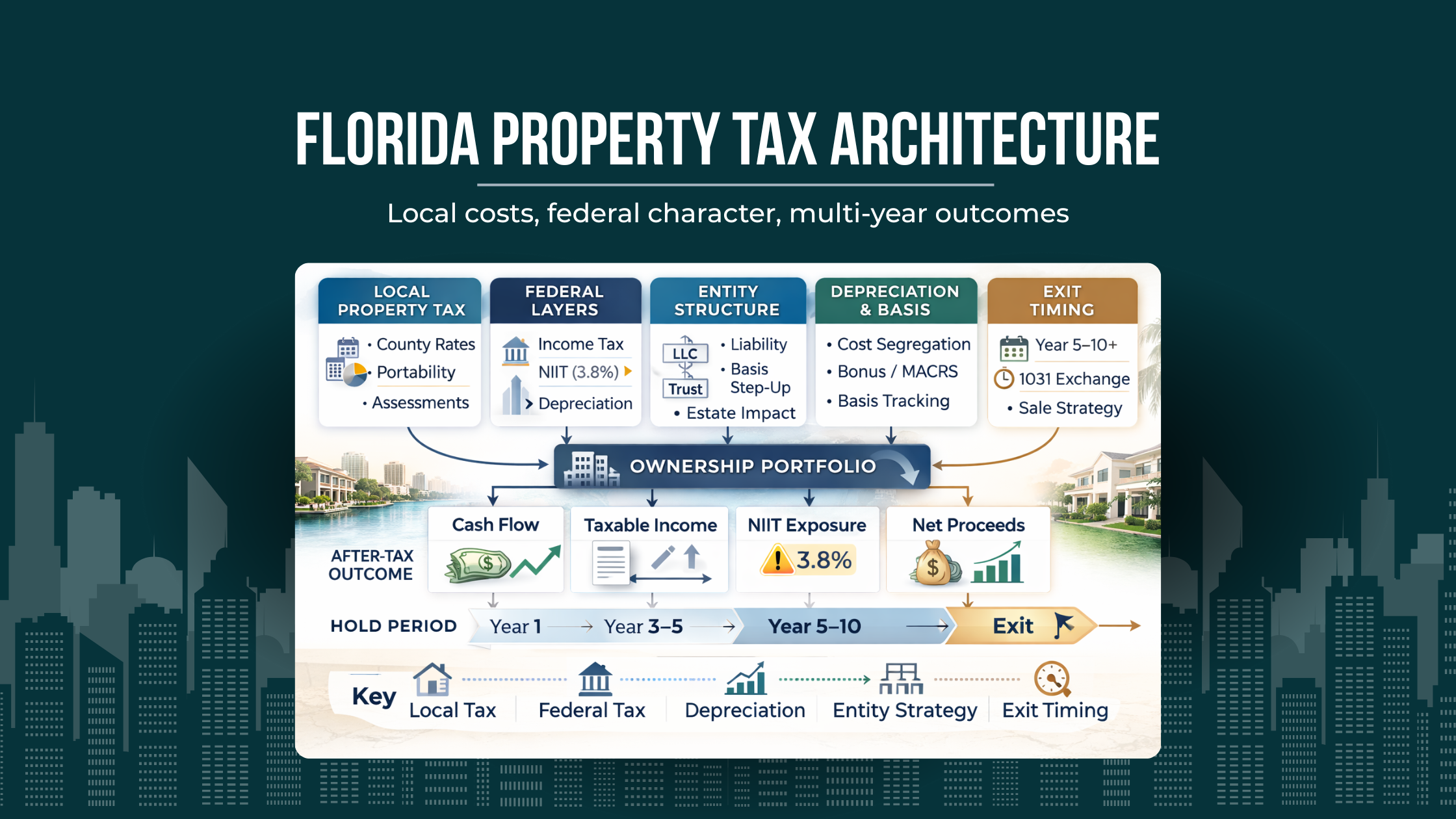

Florida’s tax brand creates a persistent misunderstanding. Because Florida does not impose a state personal income tax, many owners searching “Florida no property tax bill” are really trying to answer a broader planning question: does Florida’s tax environment make holding or selling property structurally more efficient? The answer is more nuanced. Florida property owners still receive local property tax bills, and for affluent households the larger planning risk usually sits elsewhere: federal gain recognition, NIIT exposure, passive-loss timing, entity rigidity, depreciation unwind, and poor sequencing across years. Florida’s no-state-income-tax environment does not remove those issues. It often makes them easier to ignore until an exit year forces them into view.

For high-income real estate investors, business owners, and professionals in Florida, the useful question is not whether the state is “low tax” in the abstract. It is whether the portfolio, ownership structure, and timing decisions are producing sustainable after-tax outcomes over multiple years. That requires separating property-tax carrying costs from federal income character, modeling how rental income and sale gains interact with NIIT, and treating depreciation strategy as part of an eventual unwind rather than a one-year win. In practice, the phrase Florida no property tax bill should trigger a deeper review of Florida property tax planning, federal tax planning in Florida, and Florida real estate exit planning, not a simplistic assumption that ownership is inherently efficient.

We help you evaluate multi-year outcomes before a property decision locks in NIIT exposure, depreciation recapture, or a poor sale-year income stack.

Key Takeaways

Florida no property tax bill is not a literal planning outcome. Florida owners still face county, municipal, school, and special-district property taxes, and those local tax mechanics still affect hold-versus-sell decisions.

In Florida, the absence of state income tax increases the relative importance of federal planning. Income stacking, tax sequencing and timing, NIIT exposure, and gain character often matter more than the local bill itself.

Cost segregation strategy and bonus depreciation planning can improve near-term cash flow, but they should be evaluated against hold period, refinancing assumptions, and the eventual depreciation recapture planning burden.

Active vs passive rental treatment is not only a current-year deduction issue. It can change how suspended losses are released, how rental income is treated during the hold, and whether net investment income tax real estate issues become more painful at exit.

Entity and ownership structure should be judged by flexibility over time: who can use losses, how gains flow, whether allocation rules fit economic reality, and how cleanly a property can be sold, exchanged, gifted, or restructured.

Florida-specific variables such as homestead vs non-homestead property tax treatment, reassessment risk after use changes, and insurance/casualty pressure should be built into reserve and exit planning, not handled as isolated operational issues.

We can map how sequencing across years affects passive loss use, exit timing, and the trade-off between current cash flow and long-term tax efficiency.

What “Florida No Property Tax Bill” Gets Wrong

The phrase suggests that Florida does not impose meaningful property taxation. That is incorrect. Florida does not levy a state-level property tax in the way it levies sales tax, but property taxes are imposed locally and administered through county-level property appraisers and tax collectors. In other words, Florida’s property tax system is local, not nonexistent. That distinction matters because an owner can be correct that Florida lacks a state income tax and still be strategically wrong about the true economics of a hold or sale decision.

For sophisticated owners, the real danger is not misunderstanding the bill itself. It is letting that misunderstanding distort bigger decisions. A taxpayer may overvalue Florida’s “tax-friendly” reputation, keep an appreciated asset longer than the economics justify, or accelerate deductions without modeling the unwind. The result is often a portfolio that looks efficient during the hold period but becomes much less efficient when a sale, refinancing, or use change forces all of the character questions onto one return.

The search results for this query largely stop at the surface correction that Florida still has local property taxes. What they usually do not address is that high-income households are not harmed most by misunderstanding the local bill. They are harmed by failing to integrate that local cost with federal tax sequencing, NIIT exposure, recapture, and ownership structure. That is where a simple phrase becomes a planning problem.

Why Federal Planning Carries More Weight in Florida

Florida’s lack of state personal income tax often makes owners feel as if they are already optimized. In reality, that environment can increase the importance of federal planning because fewer state-level taxes are available to distract from what is happening on the federal return. The key variables become income character, timing, grouping, basis, and whether the household is layering business income, portfolio income, rental income, and sale gains into the same year.

That is especially relevant in Florida because many affluent households are real-estate heavy. They may own investment property, operate short-term rentals, hold business interests through pass-through entities, and have appreciated securities or deferred compensation arriving in the same period. Once those streams converge, the planning question is no longer whether Florida has no state income tax. It is whether the household has allowed too many high-character items to collide in one year.

Federal planning also carries more weight because Florida’s local property tax features can change the economics of moving, converting, or selling without changing the federal rules underneath. A homeowner can preserve value through homestead-related protections on the local side while simultaneously creating federal complexity through rental conversion, depreciation, or a later sale. Good planning has to hold both systems in view at once.

The broader implication is that Florida is not a substitute for planning. It is a jurisdiction where coordination matters more because the absence of state income tax pushes more of the real work toward federal timing and asset-level decisions. That is why affluent Florida taxpayers often feel underplanned even when their annual returns are technically correct.

Local Property Taxes Still Matter to Hold-Sell Analysis

Even though federal issues dominate the long-term outcome, local property taxes still shape the economics of holding an asset. Florida’s homestead exemption and Save Our Homes assessment limitation can reduce carrying costs meaningfully for qualifying primary residences, while non-homestead property does not receive the same protection. Florida’s Department of Revenue explains that a homestead exemption may be up to $50,000, with the first $25,000 applying to all property taxes and the additional amount applying only to certain non-school taxes, and that the Save Our Homes limitation generally caps annual assessed-value growth after the first qualifying year at the lesser of CPI or 3 percent.

That means a hold decision cannot be evaluated only on appreciation and financing. A long-held homesteaded property may carry embedded local tax value that disappears when the owner moves, changes use, or transfers the property. Florida also allows portability of the Save Our Homes assessment difference in qualifying situations, which means the timing of a move can affect the economics of a replacement residence. Those local mechanics are not mere filing details. They can change whether retaining, converting, or replacing a residence is economically sensible.

This becomes more complex when a property is partially or intermittently rented. Florida’s homestead guidance makes clear that changes in use can affect eligibility, and the planning consequences ripple beyond the property-tax bill. A residence that becomes a short-term rental or mixed-use asset may alter local exemptions, insurance profile, financing terms, and future federal gain characterization. In markets where owners move between personal use and rental use as conditions change, these transitions need to be modeled, not improvised.

A second-order issue is buyer psychology. Local property tax protections can influence demand for owner-occupied housing, while non-homestead carrying costs can pressure investors differently. In a cooling or insurance-stressed market, the spread between homestead and non-homestead economics can widen, which affects disposition strategy even before federal tax is considered. That is one more reason the phrase Florida property tax bill belongs inside a hold-sell model rather than in a generic homeowner checklist.

Income Stacking Is Usually the Real Planning Variable

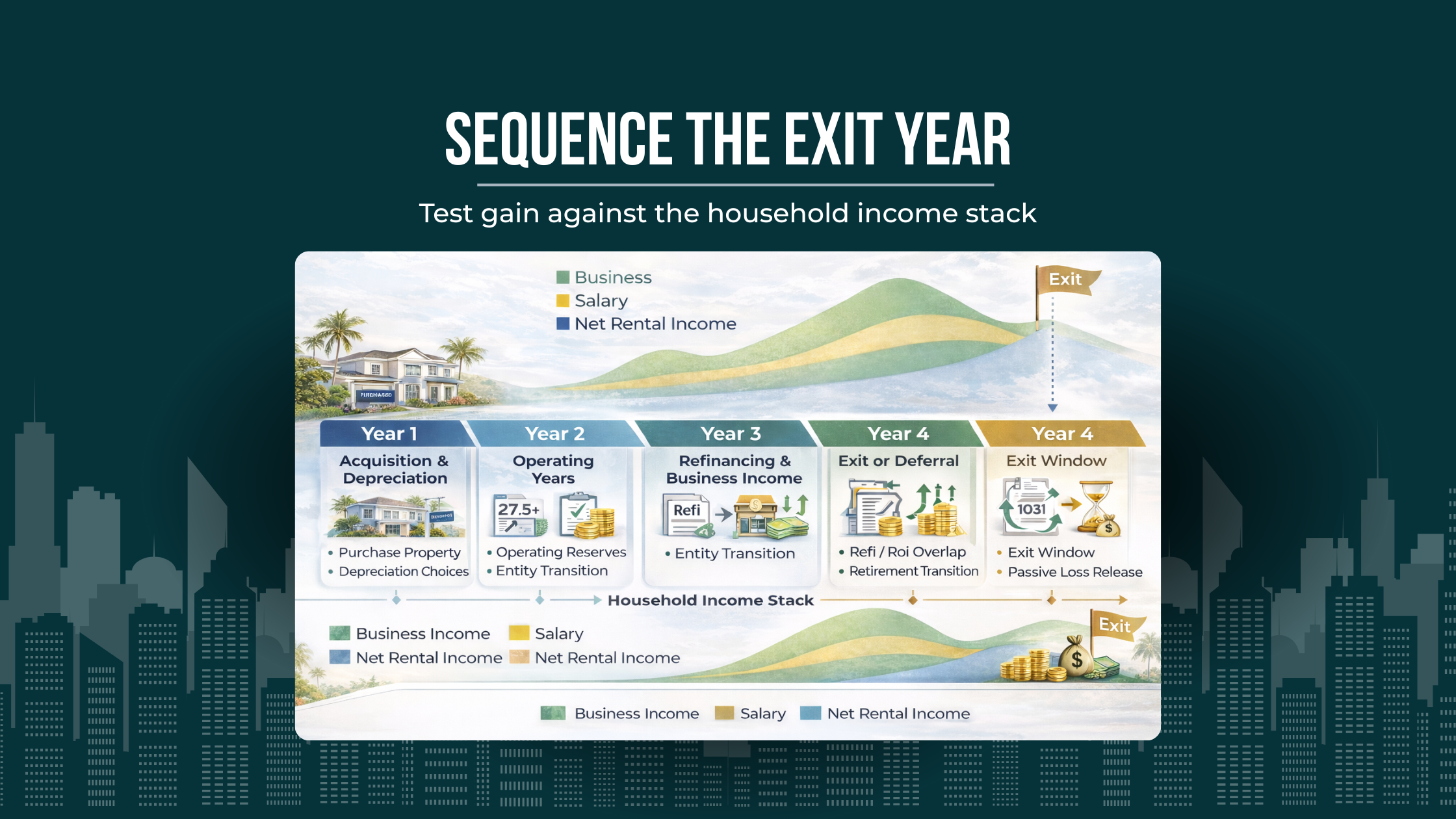

High-income owners rarely recognize real estate gain in a vacuum. They stack it on top of salary, business distributions, carried interests, dividends, interest, trust income, and retirement-related cash flow. The result is that the best time to sell is often not when the market peaks or when a tenant vacates. It is when the household’s total income stack makes the character mix least harmful.

This is where multi-year modeling becomes more valuable than one-year tax reduction.A property owner may use accelerated depreciation in Year 1, enjoy strong cash flow in Year 2, and then face a Year 3 sale while ordinary business income is also elevated. If that sale lands during a peak-earning year, the value of released passive losses may be muted, NIIT can layer on top, and depreciation-related gain may arrive when the household has little room for favorable sequencing. The tax result can be worse than the owner expected even if each prior-year return looked efficient in isolation.

A sale year that looks acceptable on price alone can become inefficient once it is stacked with business income, NIIT, and depreciation unwind.

(The central planning issue is often not whether the asset should be sold, but when the household can absorb the gain with the least friction. That requires viewing the property inside a broader calendar of income events, not as a stand-alone transaction.

A timeline view makes the second-order effects easier to see. Once refinancing, business income, retirement transitions, and passive-loss release are placed on the same path, the “best” sale year often changes.)

The inverse is also true. A taxpayer approaching partial retirement, a planned reduction in business income, or a lull between liquidity events may have a cleaner window for recognition. In those years, the household may have more room to absorb gain, a better use case for suspended losses, and less friction from overlapping income categories. Good sequencing therefore means testing alternative sale years, not merely asking whether today’s market price is attractive.

Another failure mode appears when owners refinance aggressively because current cash flow looks strong, then later discover that debt structure and required sale timing no longer align. In that situation, tax sequencing is no longer optional. The financing timeline can force gain recognition into an unfavorable year. Multi-year tax planning works best when debt maturity, reserve policy, and likely sale windows are modeled together instead of separately.

NIIT Exposure Changes the Economics of a Florida Exit

The IRS states that the Net Investment Income Tax is 3.8 percent on the lesser of net investment income or the excess of modified adjusted gross income over the applicable threshold amount. Current IRS guidance and Publication 550 list the thresholds at $250,000 for married filing jointly or qualifying surviving spouse, $125,000 for married filing separately, and $200,000 for single and head of household filers.

| Filing status | NIIT threshold |

|---|---|

| Married filing jointly / qualifying surviving spouse | $250,000 |

| Married filing separately | $125,000 |

| Single | $200,000 |

| Head of household | $200,000 |

For affluent Florida taxpayers, this matters because Florida’s no-state-income-tax environment does not offset NIIT at all. If a household already exceeds the threshold through earned or business income, then rents, portfolio income, and taxable gains can create a second layer of tax friction even when the owner thinks only in terms of regular income tax. In practice, many investors underestimate how much the NIIT exposure changes the economics of a Florida real estate sale because they treat all gains as one bucket.

The IRS explains that net investment income can include gross income from interest, dividends, annuities, royalties, and rents, as well as net gain attributable to the disposition of property, unless the items are derived in the ordinary course of a trade or business that is not itself a passive activity or a trading business in financial instruments or commodities. That means classification matters. The issue is not simply whether an owner feels “active.” It is whether the activity is treated as passive or nonpassive under the applicable rules and whether the facts support that treatment.

This is where active vs passive rental treatment becomes more than a deduction issue. If rental real estate remains passive, rental income and sale gains can remain exposed to NIIT in ways that materially affect the after-tax result. If the owner qualifies as a real estate professional and materially participates, the regular-tax treatment of the activity may improve, and the NIIT analysis may also change depending on the facts and the structure. But this is not a label-based answer. It depends on time, participation, grouping, documentation, and whether the activity is genuinely part of a nonpassive trade or business.

A common failure mode is assuming that high income itself makes NIIT unavoidable. High income triggers the threshold issue, but NIIT planning still depends on what type of income is being recognized and how the activity is classified. Another failure mode is assuming that once one spouse qualifies as a real estate professional, every rental result becomes immune from NIIT. The rules are narrower than that and often depend on the treatment of each activity, the grouping position taken, and the operational reality over time.

In exit planning, NIIT should be modeled separately from ordinary income tax and separately from recapture. It is not just an extra rate. It is a separate layer that can change the outcome of installment timing, batching multiple sales into one year, or combining a property exit with large dividend or business income. For households above the thresholds, a “good” sale year and a “bad” sale year can be separated less by market value than by the interaction between NIIT and the rest of the income stack.

Active vs Passive Treatment Becomes Binding at Exit

The IRS states that rental activities are generally passive even if the taxpayer materially participates, unless the taxpayer qualifies as a real estate professional and materially participates in the activity. That baseline rule is familiar to many investors, but the planning mistake is treating it as relevant only when losses are suspended. By the time a property is sold, passive classification can shape whether losses are released in a helpful way, whether the activity contributed to NIIT exposure during the hold, and whether the owner’s documentation can support the treatment assumed all along.

This matters particularly for owners with mixed portfolios. A Florida physician, attorney, or founder may have one actively managed short-term rental, several long-term rentals, and an operating business. The tax question is not whether the owner “worked hard” on the properties. It is which activities are grouped, which are rentals, which are businesses, and whether the records support material participation under the rules that actually apply. A weak file can be tolerable while cash flow is strong. It becomes expensive when the exit year depends on those classifications.

Another overlooked issue is that exit itself can expose inconsistent treatment. If the owner has claimed the economics of an active operating asset during the hold but the file reads like a passive investment at sale, the planning story breaks apart. That can affect the usefulness of suspended losses, the NIIT analysis, and the credibility of earlier positions. The right time to solve that problem is during the hold period, not in the closing quarter.

A further second-order effect is family ownership. When spouses, trusts, or related entities own different pieces of the same economic asset, participation and loss utilization may not line up with economics. That can leave one owner holding the gain and another owner holding the trapped tax attributes. Classification therefore becomes a structural issue, not just a recordkeeping issue.

Cost Segregation and Bonus Depreciation Are Planning Tools, Not the Plan

Cost segregation can be a strong planning tool when it aligns with hold period, financing needs, and the owner’s broader income profile. The problem arises when it is treated as a stand-alone victory. The IRS instructions for Form 4797 make clear that gain on depreciable property can require ordinary income recapture, with the excess generally moving through the capital gain framework. That means faster deductions today can reappear as less favorable character tomorrow.

For a high-income Florida investor, the question is not simply whether a study creates deductions. The better question is whether those deductions are being taken in a year when they are economically valuable, and whether the likely exit path justifies the future unwind. A short expected hold, redevelopment pressure, or a probable sale during a peak-income year can reduce the value of aggressive acceleration even when the current-year cash benefit looks attractive.

Bonus depreciation planning should be viewed the same way. When current federal law permits accelerated deductions, the decision still depends on when income is high, whether refinancing depends on near-term cash flow, and whether the property is likely to be sold, exchanged, or contributed later. Time-bound federal rules should therefore be used conditionally. The planning logic is durable, but the optimal use of acceleration depends on the law in force for the year of placement in service and on the owner’s real hold assumptions.

A common backfire occurs when taxpayers use cost segregation to maximize Year 1 shelter, then refinance based on strong post-tax cash flow, and later sell sooner than expected. The refinancing may have been sound on a pretax basis, yet the tax unwind can still compress the after-tax result if depreciation recapture planning was never part of the original model. Another backfire occurs when taxpayers accelerate deductions in a year that was already fully crowded with ordinary losses or other shelter, leaving the deductions with limited marginal value but preserving the later recapture burden.

The stronger approach is to treat cost segregation as one lever inside a sequence: acquisition, improvement cycle, hold period, expected refinancing points, likely exit windows, and the household’s broader income profile. That is what turns a tactic into a planning tool.

Exit Planning: Recapture and Unrecaptured §1250 Gain Need Their Own Model

One of the largest gaps in the search results is that many pages stop at “capital gains” and never force the reader to break a sale into its actual federal components. The IRS instructions for Form 4797 explain that part of the gain on the sale or exchange of depreciable property may have to be recaptured as ordinary income on Form 4797, with any excess gain generally reported through Form 8949 and Schedule D.The Schedule D instructions separately require computation of unrecaptured §1250 gain.

Exit planning improves when the sale is modeled as a set of distinct tax layers rather than one blended capital-gains assumption.

(Many owners still evaluate a sale using one blended rate assumption, which hides where the real leakage occurs. A better approach is to isolate each character bucket and ask how prior depreciation, current income, and ownership structure affect the final result.

That separation also improves decision quality around holding versus selling. An asset with meaningful recapture exposure may still be worth exiting, but only after the unwind is measured against the cost of continued ownership.)

That matters because economically identical sales can produce very different tax outcomes depending on depreciation history and asset composition. For many Florida investors, especially those with heavy real estate concentration, the tax cost of selling is not a single long-term capital gains rate. It is a layered result that may include ordinary income recapture, unrecaptured §1250 gain, other long-term gain, and potentially NIIT. Any exit model that ignores that structure is incomplete.

The IRS also notes in its property basis and sale-of-home guidance that gain attributable to depreciation may be subject to the unrecaptured §1250 gain rate and that taxable gain may also be subject to NIIT. That reinforces the point that the “home” or “rental conversion” context does not remove the need to model depreciation history separately. Once depreciation has been taken, the unwind deserves its own analysis.

A useful way to think about depreciation recapture planning is as an unwind analysis rather than a sale analysis. What deductions were taken, by which owner, in which years, and under what assumptions about hold period and future income? If those assumptions changed, the owner needs a fresh model before deciding whether to sell, exchange, refinance, or continue holding. That is especially true when the asset has moved between personal, rental, and mixed-use periods.

Year sequencing matters here as well. A sale that looks acceptable in a low-ordinary-income year can become much less attractive if it is bundled into a year with business liquidity, deferred compensation, or large portfolio gains. The reverse can also be true. If a household anticipates lower earned income, greater charitable flexibility, or a different ownership posture in a later year, deferring an exit may improve not only the rate environment but the character stack.

Another failure mode is assuming that all appreciated real estate should simply be held forever to avoid the unwind. That can be just as costly if insurance, reserves, capital needs, or weak operating efficiency continue to drag on the asset. Exit planning should weigh the tax cost of the unwind against the economic cost of continued ownership. A property with large embedded recapture can still be a rational sale if the carrying economics have deteriorated enough. The right answer depends on the full balance of after-tax outcomes, not on rate aversion alone.

Entity and Ownership Structure Affect Flexibility More Than Most Owners Expect

Entity planning is often approached as a liability issue first and a tax issue second. For sophisticated owners, the more durable question is whether the structure preserves flexibility over time. Ownership determines who receives income, who can use losses, how capital accounts and basis positions evolve, how sale proceeds are distributed, and how cleanly the asset can be transferred, partially sold, or recapitalized. Those issues often become binding only when the owner wants options.

This is why entity and ownership structure should be evaluated against the likely lifecycle of the asset. A Florida investor holding a single-family short-term rental with one spouse may need a very different structure than a family group holding multiple commercial properties with uneven economics. The best structure is not the one with the most entities. It is the one that aligns tax attributes with economic reality and allows the owners to adapt when one wants out, one wants to gift equity, or the property’s use changes.

Entity structure also affects how cleanly active/passive positions can be maintained. If the economic owners, managers, and tax owners are not aligned, participation may not attach where the economics do. That can create a portfolio where the wrong person has the suspended losses, the wrong person has the gain, or the group discovers too late that a sale will not produce the offsets they assumed. For affluent households using family entities, trusts, or side-by-side operating and real estate vehicles, this is a recurrent source of friction.

Another second-order issue is that structure affects optionality at exit. A deal-level buyer may want assets; the ownership group may want an entity-level sale; one owner may prefer current cash while another wants deferral or continued equity. Poor entity design reduces the ability to respond to those differences. Good design does not guarantee a perfect tax result, but it preserves the ability to choose among workable ones.

For Florida real estate investors with both operating businesses and passive holdings, we generally view structure as part of the sequencing conversation. It should support grouping decisions, capital deployment, succession goals, and exit alternatives over time. When it does not, the tax return may still be technically correct each year, but the strategy remains fragile.

Cash Flow vs Long-Term Tax Efficiency

Some tax strategies make cash flow look better before they make wealth better after tax. That distinction matters in Florida because operating costs can change quickly when insurance premiums rise, storm hardening is needed, or financing conditions tighten. A deduction that supports debt service in Year 1 may still be worthwhile, but only if the owner has modeled the reserve requirements and exit consequences that come with it.

The planning mistake is to assume that any reduction in current tax automatically improves the asset. In reality, some deduction-heavy strategies create dependence on leverage or on an optimistic hold period. If the property needs to be sold earlier than expected, the owner may discover that the earlier cash-flow benefit has been more than offset by poor gain character or an unfavorable sale year. This is one of the clearest examples of where tax efficiency and economic efficiency can diverge.

Florida-specific risk intensifies that trade-off. Properties exposed to storm, flood, or insurance-market volatility may require larger cash reserves and more conservative underwriting than static tax models assume. Those realities do not change the Code, but they do change the probability that a planned hold period will actually occur. If the hold period is less durable than the tax model assumes, aggressive acceleration deserves more scrutiny.

A better framework is to ask two questions at the same time: does this move improve after-tax cash flow now, and does it still improve after-tax wealth if the exit comes earlier, later, or in a different income year than expected? A strategy that only works in one narrow timeline is usually less robust than it first appears.

Retirement, Pension, and RMD Coordination Can Improve Sale Timing

Real estate exits should be coordinated with the household income calendar, and retirement transitions often create the most useful planning windows. The IRS NIIT framework makes clear that whether net investment income is actually taxed depends in part on modified adjusted gross income over the threshold. That means the same property sale can produce different all-in results depending on whether the household is still in peak earned-income years, has stepped down from active business income, or is entering a period when retirement distributions are becoming a larger part of the return.

For affluent Florida households, this often creates a sequencing opportunity. A physician winding down a practice, a founder after an operating-company exit, or a couple before large required distributions begin may have a cleaner period for recognizing real estate gain than they did during their highest-income years. That does not mean retirement automatically creates a low-tax exit year. It means the character and layering of income can change enough to justify a different sale timeline.

Retirement coordination also matters because the tax return often becomes simpler in some respects and more rigid in others. Earned income may decline, but portfolio income and distributions may become more prominent. That can improve one part of the analysis while tightening another. A portfolio sale that looks attractive after earned income falls may still create NIIT exposure if investment income remains high. Again, the point is sequencing, not a simplistic “retire then sell” rule.

The more strategic approach is to map expected income sources across several years: wages or business income, passive income, retirement distributions, portfolio realization, and likely real estate events. When that map is built first, the property sale can be inserted into a year where the overall stack is more efficient. When the sale is planned first and the rest of the household is adjusted around it, the tax result is often less controlled.

Asset-Based Planning Beats Deduction-First Planning

High-income taxpayers usually do not suffer from a shortage of tax ideas. They suffer from ideas that are not ordered properly. Asset-based planning starts with the property itself: expected hold period, financing profile, insurance burden, reserve needs, appreciation path, owner use, and most likely exit route. Only after those facts are clear does it make sense to decide how aggressively to depreciate, how to structure ownership, or how much complexity the asset can justify.

That framework is especially important in Florida, where the absence of state income tax can make any current deduction feel more valuable than it really is. A deduction-first approach often treats the asset as a container for tax benefits. An asset-based approach treats the tax system as one variable inside the investment’s full life cycle. The second approach is usually less dramatic, but it is more durable.

It also produces better restraint. Not every property needs cost segregation. Not every owner benefits from added entity layers. Not every appreciated asset should be held indefinitely, and not every high-tax exit should be avoided. What matters is whether the tax choices support the asset’s realistic path rather than an idealized one.

Correcting Common Misuse and Oversights

One common mistake is using Florida’s “tax-friendly” reputation as a substitute for federal planning. The state may not tax personal income, but the federal return still determines the character and timing of most meaningful wealth events. Owners who rely on the Florida narrative alone often under-model NIIT, passive-loss release, and exit-year gain character.

Another common mistake is treating cost segregation as universally accretive. It can be effective, but only when its future unwind is worth the present benefit. Where the hold period is uncertain, the financing is aggressive, or a sale is likely to land in a peak-income year, the strategy may still work, but it requires a more demanding model. Without that model, the owner is often optimizing optics, not outcome.

We also see affluent investors overestimate how much “being hands-on” solves passive and NIIT issues. The federal rules turn on classification, material participation, grouping, and documentation, not on subjective effort. An owner can spend meaningful time on a property and still have a file that does not produce the expected tax treatment. That gap tends to surface at exit, when the cost of being wrong is highest.

A related oversight is overengineering entity charts without improving flexibility. More entities can create asset protection benefits, but they can also separate economics from tax ownership, complicate basis and allocation questions, and make partial sales harder. Structure should be earned by complexity, not used as a proxy for sophistication.

Finally, many owners treat local property-tax features as administrative details rather than strategic variables. Homestead status, portability timing, and use changes can affect whether a property should remain a residence, become a rental, or be replaced altogether. When those local variables are ignored, the federal analysis may still be technically sound while the economic decision is still wrong.

We work through how entity and ownership structure may shape flexibility over time, including who recognizes gain, who uses losses, and how an exit unfolds.

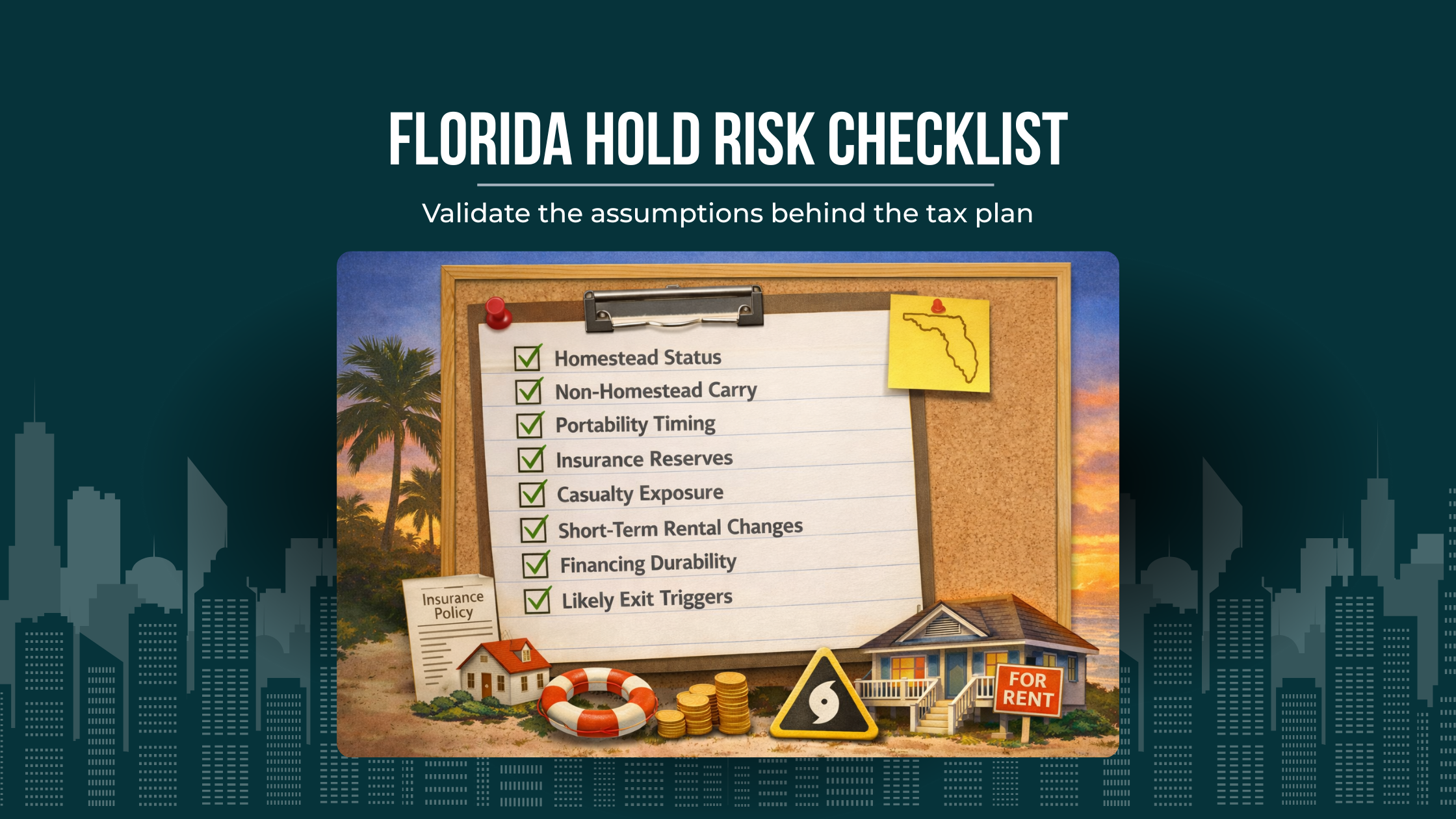

Florida-Specific Planning Considerations

Florida changes the analysis first because it removes state personal income tax from the household equation while leaving federal tax fully in place. That shifts more strategic weight onto federal timing, NIIT, passive classification, and exit-year character. For high earners, this often means the most expensive mistakes happen in federal planning even though the conversation started with a Florida tax advantage.

Second, Florida’s real estate concentration increases the odds that a household’s balance sheet is carrying substantial depreciation history. In a market where real estate is often central to both lifestyle and investment portfolios, owners can accumulate years of depreciation deductions before seriously modeling the unwind. That is precisely why depreciation recapture planning and unrecaptured §1250 gain deserve to be front-end considerations, not closing-table surprises.

Third, Florida’s homestead vs non-homestead distinction can affect both holding costs and exit behavior. A qualifying primary residence can benefit from exemption and assessment-limitation mechanics that do not apply to non-homestead property in the same way. When a taxpayer converts use, rents the property, or relocates, those differences can materially affect the economics of holding versus replacing the asset. For households deciding between retaining a low-basis residence, monetizing it, or moving into a new home, the local property-tax consequences belong in the same model as the federal consequences.

In Florida, insurance, casualty, and property-use variables often determine whether a multi-year tax strategy remains realistic long enough to work.

(Florida-specific planning is not only about tax rules. It is also about whether the assumptions supporting the hold period remain durable once insurance pressure, casualty exposure, and use changes are added to the model.

A checklist format is useful here because these risks rarely fail one at a time. They tend to compound, and when they do, they can force an exit into a year that was never supposed to carry the gain.)

Fourth, Florida’s short-term rental activity creates a planning layer that many generic articles miss. Use patterns can influence not only local exemption issues but also insurance terms, operating volatility, management burden, and how convincingly the owner can support participation positions. In some cases, short-term rental economics improve current cash flow while increasing operational complexity or reducing the durability of assumptions used in the tax model. That does not make the strategy wrong. It means it should be modeled as a changing use case, not a static rental asset.

Fifth, insurance and casualty exposure matter in Florida more than many tax models acknowledge. Storm risk, flood exposure, rebuilding standards, and changes in underwriting appetite can all affect reserve needs, debt service coverage, tenant continuity, and buyer demand. Those are not just operating concerns. They influence how realistic a hold period is, whether a refinance remains prudent, and when an exit should occur. A tax strategy built on a long hold is only as good as the assumptions that support the hold.

Finally, Florida-specific planning should remain evergreen. Legislative proposals about reducing property taxes may come and go, but the durable planning logic does not change: local property tax mechanics affect carrying cost and use decisions, while federal tax rules usually determine the largest long-term leakage for affluent owners. That is why Florida no state income tax planning should lead to deeper federal coordination, not to less planning.

We can compare hold, sell, or restructure scenarios with attention to depreciation recapture, unrecaptured §1250 gain, and exit-year sequencing.

Conclusion

The search for Florida no property tax bill often begins with a simple question and ends with a more important one: how should a high-income Florida owner structure, operate, and eventually exit property in a way that stays efficient across years? Florida still has local property taxes, and those taxes matter. But for affluent households, the real planning stakes usually sit in federal sequencing, NIIT, passive classification, entity flexibility, and the unwind of depreciation. Treating the issue as a local-tax myth alone leaves too much value on the table.

The strongest approach is coordinated and multi-year. We want the property-tax carrying cost, homestead position, reserve policy, depreciation strategy, ownership structure, retirement timing, and exit path to reinforce one another rather than conflict. That does not produce a one-size-fits-all answer. It produces a framework that can adapt when income changes, market conditions shift, or an expected hold becomes an earlier sale. In Florida, that kind of integration is usually far more valuable than any one-year tax reduction.

We help align exit timing with the rest of the household income picture so recapture, NIIT, and retirement-year changes are evaluated together, not one return at a time.

Frequently Asked Questions

Does Florida have property tax?

Yes. Florida does not impose a state personal income tax, but Florida property owners still pay local property taxes set through county and other local taxing authorities. For affluent households, the useful planning point is not the headline distinction. It is how local carrying costs interact with federal outcomes over time. A property that looks attractive because Florida has no state income tax may still become less efficient if ownership structure, depreciation history, NIIT exposure, or a forced sale year are not modeled early. That is why we treat Florida property tax planning as one part of a broader multi-year framework, not a stand-alone cost line.

How are Florida property taxes calculated?

Florida property taxes are built from taxable value and local millage rates, not from a single statewide property tax rate. For sophisticated owners, that matters less as a formula and more as a planning variable. Taxable value can change with reassessment, use changes, transfers, and exemption status, which means the local bill can shift when a property moves between homestead, rental, mixed-use, or replacement-residence roles. In practice, we want the local property tax calculation in the same model as hold period, insurance costs, reserve needs, and likely exit timing, because those variables often move together rather than independently.

When is it better to sell Florida real estate in a lower-income year?

Often when the household’s overall income stack is lighter and the sale is less likely to collide with high ordinary income, large portfolio gains, or other liquidity events. The strategic issue is not just rate sensitivity. It is how the sale year affects NIIT layering, the usefulness of suspended passive losses, and the value of any remaining planning options. For many high-income owners, the better comparison is not this year versus next year in isolation. It is Year 1 through Year 3, including business income, retirement transitions, distributions, and any planned changes in ownership or use. A cleaner year can materially improve the after-tax result even when the sales price is similar.

Should I convert a Florida property to a rental before selling it?

Sometimes, but the answer depends on why the conversion is being considered and how long the property is likely to stay in rental use. A conversion can change local exemption treatment, insurance profile, operating assumptions, and federal tax character over time. It may also create a depreciation history that later affects the unwind. For sophisticated owners, the key question is whether the conversion improves the full multi-year outcome or merely delays a decision. If the likely result is a near-term sale anyway, the added complexity may not justify itself. If the property is genuinely being repositioned for a longer hold, the sequencing analysis may look very different.

Do you pay capital gains tax when you sell a house in Florida?

Potentially, yes, because Florida’s lack of state personal income tax does not remove federal gain recognition. For high-net-worth owners, the more important point is that a taxable real estate exit often involves more than one kind of gain. Depending on the property’s use and depreciation history, the outcome may include capital gain treatment, depreciation-related unwind, and NIIT considerations layered on top. That is why we do not view a sale as a single-rate event. We want to know what deductions were taken, how the property was used, whether ownership changed over time, and what else is landing on the return in that year.

Do I have to pay taxes on depreciation when I sell rental property?

Often, yes, in the sense that prior depreciation can change the character of gain when the property is sold. For affluent investors, that is one of the most important long-term consequences to model before accelerating deductions too aggressively. The issue is not whether depreciation was “good” or “bad.” It is whether the earlier cash-flow benefit still makes sense once the unwind is measured against your expected hold period, probable sale year, and ownership structure. We generally want a separate unwind model for any property with meaningful depreciation history, especially when the household is already exposed to NIIT or expects other income events nearby.

Does it matter which entity owns Florida real estate?

Yes, because ownership affects much more than liability protection. It can influence who receives income, who may use losses, how flexible the structure is if one owner wants out, and how well the tax attributes line up with the economics of a future sale. For sophisticated Florida households, this becomes especially important when multiple family members, trusts, or operating entities are involved. A structure that works during the accumulation years may become rigid at exit if the wrong owner holds the gain or the tax attributes do not travel with the economics. We generally view entity choice as an optionality decision, not just a formation step.

Does Florida’s no state income tax make short-term rentals or weather-exposed properties more tax-efficient?

Not by itself. Florida’s no-state-income-tax environment can improve headline economics, but it does not solve federal classification, NIIT, reserve, or exit-planning issues. Short-term rentals may have different operating patterns, participation facts, and insurance realities than long-term rentals, and weather-exposed properties can carry reserve and underwriting pressures that shorten the practical hold period. That matters because many tax strategies only work as modeled if the owner can actually hold long enough for the assumptions to remain true. In Florida, insurance and casualty realities are often not separate from tax planning. They are part of whether the tax plan remains durable.