Florida Real Estate Taxes: Non-Resident Guide

Florida real estate taxes for non-residents: the direct answer

If you own Florida real estate but do not live in Florida, the main tax issue usually is not a Florida personal income tax. Florida does not impose a personal state income tax, so the recurring Florida tax layer is usually property tax and transaction tax. The harder planning work is federal: how rental income is classified, whether losses are actually usable, whether NIIT applies, how depreciation changes the exit, whether FIRPTA withholding applies, and for non-U.S. owners, whether direct ownership creates U.S. estate and gift exposure.

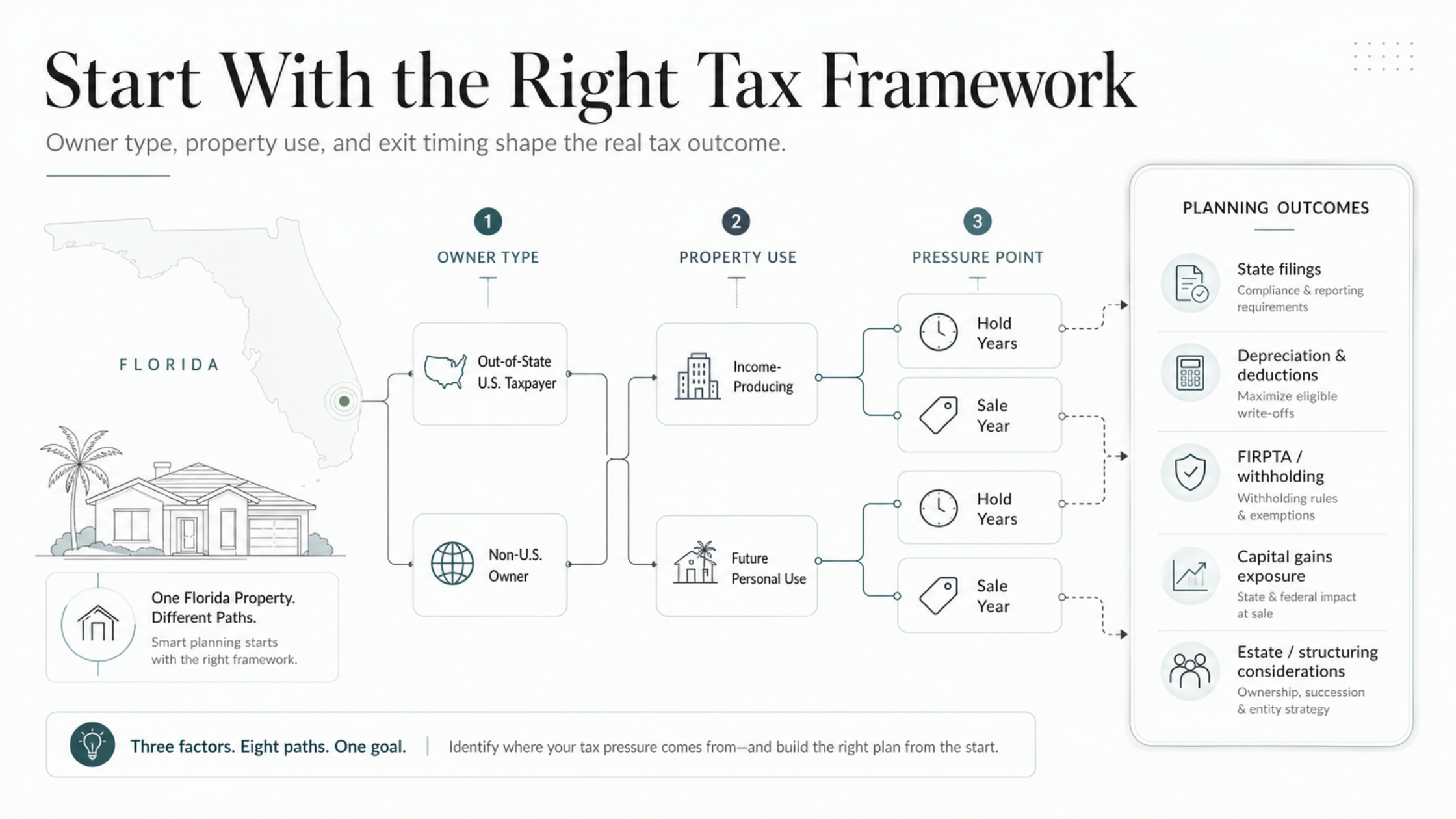

For search intent, the fastest way to answer “Florida real estate taxes” as a non-resident is to separate three questions immediately:

Are you a U.S. taxpayer who lives outside Florida, or a non-U.S. owner?

Is the property a primary residence, second home, or income-producing rental?

Are you optimizing for the hold period, or for the year you eventually sell?

Those three answers usually determine more than the Florida zip code does.

The biggest mistake in this topic is treating “non-resident” as one category. It is not. If you are a U.S. citizen or resident who simply lives outside Florida, your planning problem is usually federal income tax plus Florida property tax mechanics. If you are a nonresident alien or otherwise a foreign owner, the rule set changes materially: rental income can default to 30% taxation on gross income unless a net-basis election is made, FIRPTA can impose withholding on the amount realized at sale, and direct ownership can create estate and gift exposure that has nothing to do with annual cash flow.

That distinction matters because many ranking pages stay at the property-tax level. They explain homestead, millage, and nonresident status, but they often do not take the next step into NIIT, basis erosion, exit-year stack, or foreign-owner structure pressure. For a high-income reader, that is where the real planning value lives.

The article’s core message is that Florida real estate tax planning works better when the decision is framed correctly before structure, deductions, or sale strategy are discussed.

Introduction

Florida’s tax reputation can make the topic sound easier than it is. For sophisticated non-resident owners, the heavier planning burden usually sits in federal income tax, classification, depreciation, entity design, and sale timing. In practice, Florida does not remove the planning problem. It changes where the planning problem lives.

That is why a serious non-resident guide cannot stop at “Florida has no state income tax” or “non-residents do not get the homestead benefit.” Those points matter, but they are not where most wealth is won or lost. The more important question is how the asset behaves across years: what the structure allows in Year 1, what the hold years actually produce after classification rules are applied, and what the exit year looks like after NIIT, gain character, and withholding mechanics are layered in.

A useful way to think about Florida real estate taxes as a non-resident is to run three underwriting models before you buy or refinance:

the acquisition-year model

the stabilized hold-year model

the forced-exit model

Most bad tax decisions look reasonable in only one of those three models.

See how we think through entry, hold years, and exit year before a Florida property decision becomes expensive to unwind.

Key takeaways

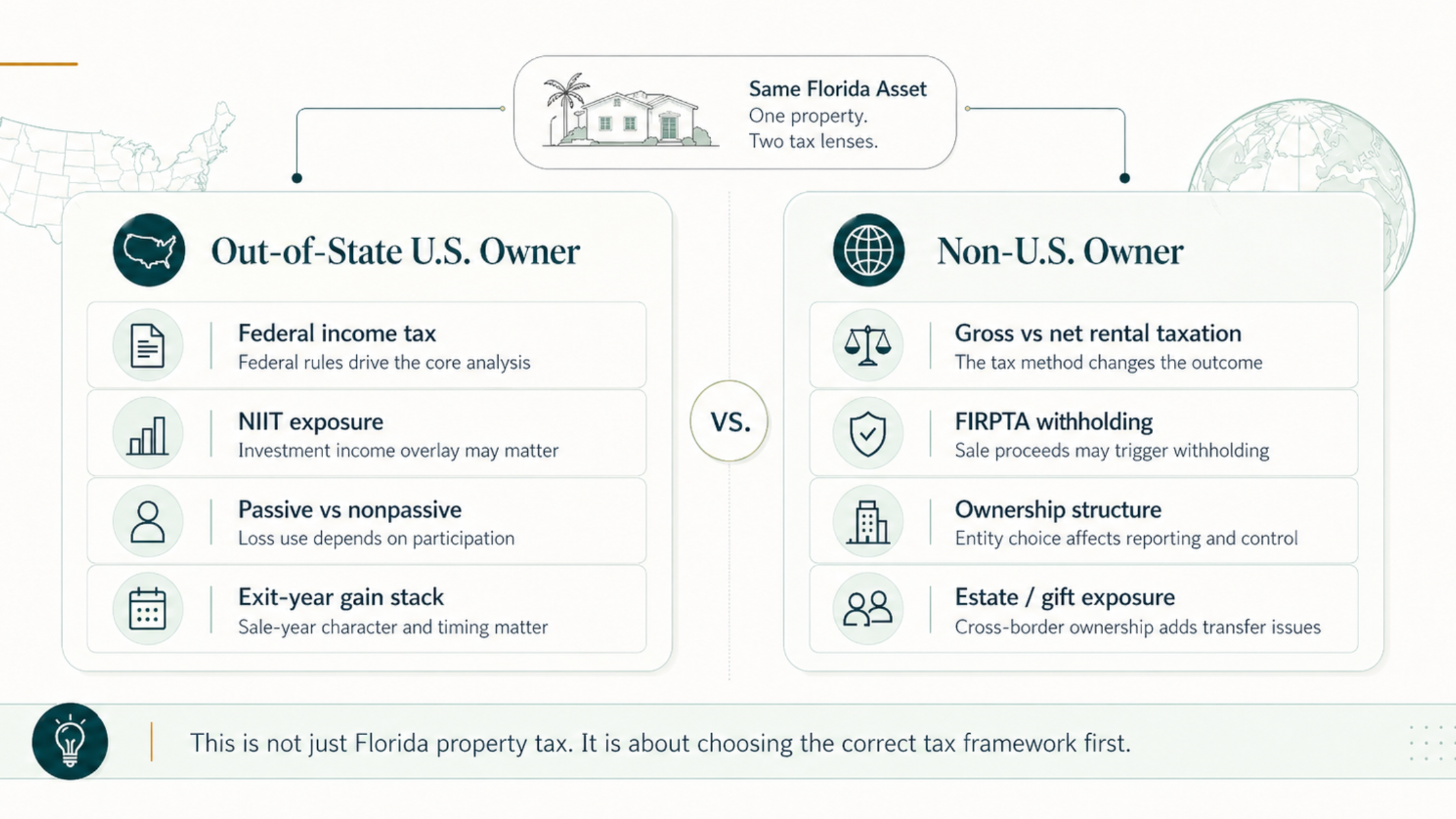

“Non-resident” covers two very different taxpayers: out-of-state U.S. owners and non-U.S. owners. The federal rules are not interchangeable.

For U.S. owners, passive vs nonpassive treatment often matters more than the Florida location because it affects current loss use, NIIT exposure, and how rental economics show up on the return.

For foreign owners, the first real fork is usually gross-basis taxation versus a net-basis election under section 871(d), not just whether to form an LLC.

Exit-year tax is a stack, not a headline rate. Long-term capital gain treatment, unrecaptured §1250 gain, NIIT, and possible FIRPTA withholding can all sit in the same transaction.

Deduction-heavy planning can improve Year 1 results while making the exit less flexible by lowering basis and increasing future gain pressure.

In Florida, a seller’s current property tax bill can be a poor proxy for your future carrying cost because homestead, Save Our Homes, portability, and non-homestead caps do not transfer cleanly to a new owner.

Go deeper on NIIT, FIRPTA, entity structure, and depreciation recapture in the areas that usually drive the real planning outcome.

First, determine which “non-resident” you are

1) Out-of-state U.S. owner

If you are a U.S. citizen or tax resident who lives outside Florida, you are usually not dealing with a special Florida income-tax regime just because the property is in Florida. Your Florida-specific issues are more likely to be property tax classification and documentary stamp tax, while the annual and exit-year tax burden is driven mainly by federal rules. Florida’s no-personal-income-tax posture does not change that.

This also means that living outside Florida does not, by itself, remove NIIT. U.S. citizens and residents with modified adjusted gross income above the applicable thresholds can still be subject to the 3.8% NIIT on net investment income, and rental income and gain from property can fall into that analysis depending on classification. For 2025 instructions, the thresholds are $250,000 for married filing jointly or qualifying surviving spouse, $200,000 for single or head of household, and $125,000 for married filing separately.

The first planning decision is not which deduction to claim. It is identifying which owner category actually applies, because that changes the rest of the analysis.

2) Non-U.S. owner

If you are a nonresident alien or otherwise a foreign owner for U.S. tax purposes, the regime changes materially. In general, U.S. real property income that is not effectively connected with a U.S. trade or business is taxed at 30% of gross income unless a lower treaty rate applies. A timely section 871(d) election can move qualifying real property income to a net basis, allow deductions, and subject the net income to graduated rates. That election applies to all U.S. real property held for the production of income, not just one asset you want to optimize.

That election is important, but it is not the whole foreign-owner analysis. The same owner also needs to think about FIRPTA on sale, financing, family transfer strategy, and whether direct ownership leaves U.S.-situated real estate inside a U.S. estate or gift tax problem. Planning each issue separately is how foreign-owner structures become efficient on paper and brittle in practice.

We can help map how ownership structure, classification, and exit mechanics change the economics before a purchase or refinance is locked in.

What taxes matter while you own the property

Florida property tax: homestead vs non-homestead matters

For most non-residents, the recurring Florida tax issue is property tax. The key distinction is not residency in the abstract. It is whether the property qualifies for homestead treatment and whether the assessment history you are seeing belongs to the current owner rather than the asset itself.

Florida homestead property may qualify for an exemption of up to $50,000 under the current structure. The first $25,000 applies broadly, and the additional up to $25,000 applies to assessed value above $50,000 for non-school taxes; Florida materials now note that this additional exemption is adjusted annually for inflation under current law. Save Our Homes generally limits annual assessed-value increases on homestead property to the lesser of 3% or CPI.

Non-homestead property is different. Florida rules continue to reflect a 10% annual assessment-increase limitation for certain non-homestead property, but a change of ownership or control can change how that cap applies. That is why the seller’s tax bill is often a bad underwriting input for a non-resident buyer. The better question is what the property’s assessment path looks like after your acquisition, under your intended use, without assuming the prior owner’s benefits survive the transfer.

Portability adds another strategic wrinkle. If the property could later become a Florida homestead as part of a relocation plan, the future property-tax path may look very different from the current one. That does not help a non-resident buyer today, but it can matter in a multi-year hold versus sell analysis.

Federal rental income planning for U.S. owners

For U.S. owners, the annual planning issue is usually classification, not geography. Rental income is generally part of net investment income unless it is derived in the ordinary course of a trade or business that is not passive for NIIT purposes. That is why passive versus nonpassive treatment matters twice: once for current loss usability and again for whether rental income and later sale gain feed NIIT.

A weak real estate tax plan often starts with depreciation and never solves the classification problem. That can leave an owner with impressive Year 1 paper losses that do not materially improve current after-tax cash flow because the losses are trapped, while the same depreciation still reduces basis and increases future gain pressure.

That is the first “works early, breaks later” pattern in Florida real estate planning. If ordinary income is already high, a deduction is only as useful as the bucket it lands in. And if the property later exits sooner than expected, the same early deduction plan may have simply shifted tax into a more expensive year.

Federal rental income planning for foreign owners

For foreign owners, the annual income analysis starts with a fork in the road. The default regime can impose 30% tax on gross rental income unless a treaty reduces it. A timely section 871(d) election can instead allow deductions and move qualifying real property income onto a net basis with graduated rates. The IRS also states that this election does not by itself treat the owner as engaged in a U.S. trade or business during the year if the owner is not otherwise so engaged.

This is where foreign owners often get shallow advice. They are told that the election is “better” because it allows deductions. Sometimes it is. But the real question is whether the election, the ownership structure, the expected sale path, and the family transfer plan all point in the same direction. A strategy that optimizes net rental income while leaving a later sale, financing event, or estate issue untreated is not a finished plan.

What changes when you sell Florida real estate

For an out-of-state U.S. owner, the sale is usually where the real tax stack shows up. If the property is held more than one year, favorable long-term capital gain rates may apply, but the analysis should not stop there. The IRS continues to state that v, while the portion of gain treated as unrecaptured section 1250 gain from section 1250 real property is taxed at a maximum 25% rate. In many cases, NIIT can sit on top of that if the taxpayer is above the applicable threshold and the gain is part of net investment income.

The article treats the sale as a stack of tax layers and cash-flow effects, not as a single headline rate.

For foreign sellers, the sale has a second problem: FIRPTA is a withholding regime that can distort closing-day liquidity even when the final tax is lower. The buyer generally must withhold 15% of the amount realized, and the amount realized includes cash, the fair market value of other property transferred, and liabilities assumed or that remain subject to the property. Residence exceptions still exist, but they are narrower than many sellers expect: no withholding is generally required if the amount realized does not exceed $300,000 and the buyer acquires the property for use as a residence; otherwise the withholding is generally 10% for residence transactions up to $1,000,000 and 15% above that level.

That is why sophisticated sellers should model two numbers, not one: the expected final tax and the expected cash withheld at closing. Those are not the same thing. Where withholding would exceed the maximum tax liability, a withholding certificate may reduce the friction, but only if the process is addressed early enough to influence the transaction.

One more distinction matters here. The NIIT does not apply to nonresident alien individuals. So when owners compare the economics of a U.S. non-Florida resident with a true NRA owner, the sale models should not assume the same NIIT result for both.

Review the sale-year stack with a focus on NIIT, unrecaptured §1250 gain, FIRPTA withholding, and closing-day liquidity.

The multi-year framework most pages miss

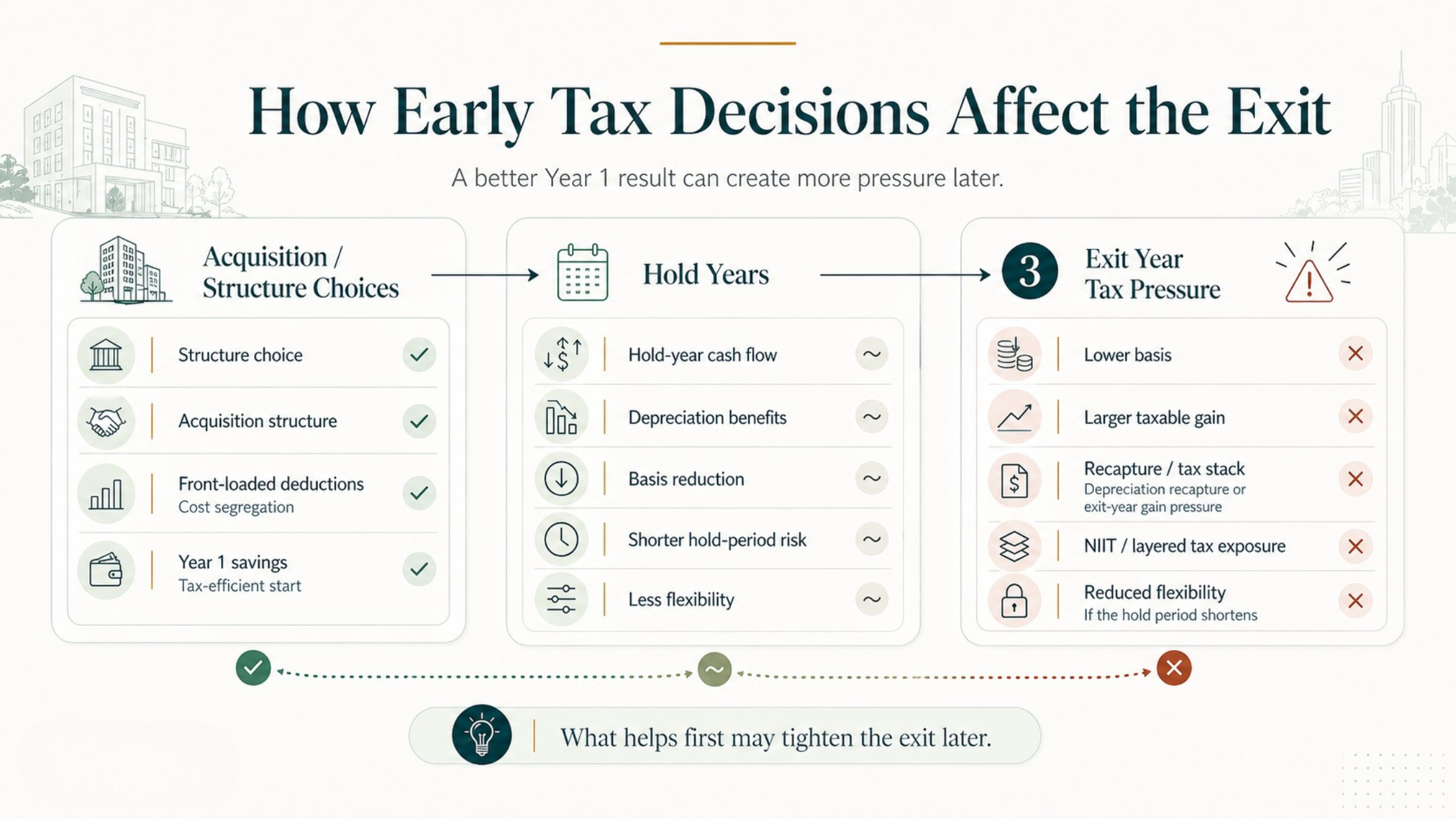

One of the article’s main insights is that the best-looking annual tax result is not always the best long-term real estate tax strategy.

Year 1: entry decisions shape future taxes

Year 1 decisions do more than affect the first return. They shape what the property can do later. Title, leverage, elections, and depreciation strategy all either preserve flexibility or spend it.

This is where many owners overweight speed and underweight optionality. Cost segregation, bonus depreciation, and front-loaded deductions can be useful planning tools, but they are not automatically good strategy. If the property may be sold sooner than expected, refinanced aggressively, gifted within the family, or moved into a different ownership structure later, the Year 1 answer needs to be tested against those future paths before the deductions are celebrated.

For foreign owners, Year 1 has an additional trap. The first structure chosen is often optimized for liability protection or convenience, not for the combination of net-basis taxation, FIRPTA handling, financing, and family transfer planning. That is how apparently simple structures become expensive to unwind later.

Hold years: cash flow and tax efficiency can diverge

During the hold period, the tax return can look more efficient than the investment actually is. Low taxable income feels good, but it may simply reflect basis erosion. Over time, depreciation lowers basis and can increase the share of future gain exposed to unrecaptured section 1250 mechanics when the property is sold.

That is why the right question is not “Did this property shelter income this year?” The better question is “Did this year’s tax result improve the lifetime economics of the asset, or did it simply borrow from the exit?”

Florida makes that question more practical, not less theoretical. Insurance costs, casualty risk, reserve needs, and operating surprises can all shorten a planned hold. A strategy that only works on a ten-year hold is not a durable strategy if the asset may be sold in year three or four.

Exit year: the stack is what matters

Exit year compresses all the earlier choices into one transaction. U.S. owners need to stack long-term capital gain treatment, unrecaptured §1250 gain, and possible NIIT. Foreign owners need to model actual tax and FIRPTA withholding separately. Everyone needs to ask whether the acquisition structure still works at disposition or whether it traps the owner into an inefficient outcome.

A helpful way to pressure-test the exit is to run three versions before the property is sold:

an expected sale in a normal income year

a sale in a year when ordinary income is already high

a forced sale or transfer when liquidity matters more than rate optimization

Many strategies look fine in the first model and fail in the second or third.

Bring the acquisition, hold-year, and exit-year pieces into one coordinated discussion instead of handling them one transaction at a time.

Common mistakes sophisticated owners still make

Treating FIRPTA as the tax itself

FIRPTA is usually the withholding event, not the final tax result. That still gets mishandled because the closing statement creates emotional certainty around the withheld amount. But the withheld amount and the true tax liability are different calculations.

Using a disregarded LLC and assuming that solved the foreign-owner problem

It often does not. The core planning questions are who the taxpayer is, what the sale mechanics are, how family transfers are handled, and whether the ownership path creates estate or gift exposure. Liability protection may still matter, but it does not answer those tax questions by itself.

Modeling the sale at one headline rate

Florida real estate exits rarely deserve a single-rate summary. A sophisticated model should separate favorable long-term capital gain treatment, unrecaptured §1250 gain, NIIT for U.S. owners where applicable, and FIRPTA withholding for foreign sellers.

Treating the seller’s Florida tax bill as your future tax bill

In Florida, this is one of the easiest underwriting mistakes to make. Homestead treatment, Save Our Homes limitations, portability, and non-homestead assessment rules can make the current bill an artifact of the seller’s facts rather than a reliable forecast of yours.

Solving annual income tax while ignoring estate and gift exposure

This is a major foreign-owner blind spot. The IRS states that executors for nonresident non-citizens generally must file Form 706-NA if the fair market value at death of U.S.-situated assets exceeds $60,000, and the IRS also states that gifts of U.S.-situated real property by nonresidents not citizens of the United States can be subject to U.S. gift tax. Even where treaties improve the result, the issue belongs in the original ownership design, not in an emergency review after a death or transfer is already on the table.

Florida-specific planning points that actually matter

Florida does not impose a personal state income tax, which is exactly why federal planning carries more weight here than many buyers expect. In a state with a heavy personal income-tax layer, that state analysis can dominate the planning conversation. In Florida, it often does not. That raises the importance of classification, basis management, and sale sequencing.

Florida also imposes documentary stamp tax on deeds and on certain financing documents. In counties other than Miami-Dade, deeds are generally taxed at 70 cents per $100 of consideration. In Miami-Dade, the rate is generally 60 cents per $100, with a 45-cent surtax per $100 of consideration that generally does not apply to a document transferring only a single-family dwelling. Promissory notes and recorded mortgages are generally taxed at 35 cents per $100, although the note tax is capped while the mortgage tax is not. On larger acquisitions, refinances, and internal restructurings, that friction deserves attention before documents are signed.

Florida-specific use changes matter too. A property that is currently an investment or seasonal property may later become part of a relocation plan. That can change the long-term property-tax economics through homestead treatment and portability, which means the hold versus sell decision is not always just a federal income-tax decision.

And Florida risk management has to stay inside the tax conversation. Insurance cost changes, casualty events, reserve calls, and shorter-than-expected hold periods are not just operational issues. They affect whether a deduction-heavy plan has enough time to work before the exit arrives.

Common Questions About Florida Property Taxes, FIRPTA, and Foreign Ownership

Do non-residents pay Florida capital gains tax on Florida real estate?

For individuals, the bigger sale issue is usually not a separate Florida personal capital gains tax. The more important questions are federal: long-term capital gain treatment, possible unrecaptured §1250 gain, and for many U.S. owners, possible NIIT. Foreign sellers may also face FIRPTA withholding at closing.

Is FIRPTA the actual tax rate on the sale?

Usually no. FIRPTA is generally a withholding mechanism. The buyer may have to withhold 15% of the amount realized, subject to the residence rules and other exceptions, while the seller’s actual tax liability is determined through the return process.

Can a foreign owner deduct expenses against Florida rental income?

Potentially, yes. By default, qualifying income can be taxed on a gross basis at 30% unless a lower treaty rate applies, but a timely section 871(d) election can allow deductions and move the income to a net basis taxed at graduated rates.

Does putting Florida real estate in an LLC eliminate FIRPTA or U.S. estate exposure?

Not by itself. An LLC may matter for liability and administration, but the meaningful tax questions are who the taxpayer is, how the property will be held and sold, and whether the ownership path still leaves a foreign owner exposed to FIRPTA, estate tax, or gift tax issues.

Conclusion

Florida real estate taxes for non-residents are only simple if the question is asked too narrowly. For many owners, Florida itself is not the heaviest tax layer. The real planning burden sits in federal classification, basis management, ownership structure, and exit sequencing.

That is why the right answer is rarely one more deduction or one more entity. It is a coordinated plan that distinguishes the taxpayer first, models the hold years honestly, and tests the exit before the structure is locked in. That approach is more demanding, but it is also where sophisticated non-resident planning starts to outperform reactive compliance.

If your Florida real estate plan is already interacting with high ordinary income, foreign ownership, or a possible sale, we can help frame the next decision more coherently.

Frequently asked Questions

When does a deduction-heavy Florida real estate strategy start hurting more than helping?

It usually starts to break when the early tax benefit is viewed in isolation. We see this when depreciation and front-loaded deductions look strong in Year 1, but the losses do not materially improve current after-tax cash flow because of classification limits, while basis still declines in the background. That can leave the owner with a weaker exit profile later. The real test is not whether the property produced a good tax return this year. It is whether the annual tax result improved the lifetime economics of the asset without reducing flexibility if the hold period shortens.

What changes if the property may be sold sooner than expected?

A shorter hold period changes the answer more than many owners expect. Strategies built around a long hold often assume there will be enough time for early tax benefits to justify the later basis reduction and exit pressure. If insurance costs rise, reserves increase, or the property simply no longer fits the portfolio, that timeline can collapse. In that situation, the same deductions that looked efficient earlier may leave the owner facing more sale-year friction with less room to manage it. We usually want the acquisition-year plan to remain acceptable even if the property exits earlier than intended.

How should a high-income U.S. owner think about NIIT when comparing hold versus sell?

For many high-income U.S. owners, NIIT is not just a sale-year issue. It can shape the economics of the hold years and the exit at the same time. If the rental activity remains in the investment bucket, the owner may feel the drag during ownership and again when gain is recognized on sale. That is why we do not treat NIIT as a separate add-on at the end. We treat it as part of the classification question from the beginning. A strategy that ignores NIIT during the hold period often produces an incomplete picture of the asset’s real after-tax return.

Why can the wrong ownership structure look acceptable during the hold period and still fail later?

Because hold-year stability can mask exit-year weakness. A structure may appear to work while the property is simply collecting rent and expenses, especially if the owner is focused on liability protection or administrative simplicity. But the real test comes later, when the property is refinanced, sold, transferred within a family, or evaluated alongside estate and gift considerations. That is where the structure may stop being flexible. We generally want ownership design to be tested against the full life cycle of the property, not just the first few returns when nothing has yet forced a decision.

Why is the seller’s current Florida property tax bill such a weak underwriting tool for a non-resident buyer?

Because in Florida, the current tax bill can reflect the seller’s facts more than the property’s forward economics. Homestead treatment, assessment limitations, and portability can all create a tax bill that will not survive the transfer in the same form. For a non-resident buyer, that means the visible carrying cost can be artificially low compared with what the new ownership period will actually produce. We would rather underwrite the likely post-acquisition assessment path and intended use than rely on the prior owner’s bill as if it were a stable forecast.

When does foreign-owner planning stop being mainly an income-tax issue?

It stops being mainly an income-tax issue as soon as the ownership plan has to survive a sale, a family transfer, or an estate event. A foreign owner may begin with a legitimate focus on rental income taxation and the choice between gross-basis and net-basis treatment. But that is only one part of the exposure. Sale withholding, ownership structure, and U.S. estate or gift consequences can all become more important than the annual rental result. We usually think the plan is incomplete if it solves the current income-tax question but leaves the transfer and exit path unresolved.

How can tax efficiency reduce liquidity at exactly the wrong time?

The most common example is a sale where the economics looked efficient during the hold period but become strained at closing. For U.S. owners, that can happen when depreciation lowered basis enough to make the gain stack heavier than expected. For foreign owners, sale withholding can create a cash-flow problem even where the eventual tax is lower. In both cases, the issue is not simply the tax cost. It is the timing mismatch between when cash is needed and how the tax rules apply. We prefer strategies that preserve liquidity under normal conditions and in a less favorable exit.

What should be reviewed before converting a Florida property from investment use to a future residence plan?

The key issue is that a use change can alter the economics beyond income tax alone. If a Florida property may later become part of a relocation plan, the future property-tax path may look very different from the current one because homestead-related rules can change carrying costs over time. That means the hold-versus-sell decision should not be modeled only as a federal gain question. We would want to revisit ownership structure, expected holding period, property-tax trajectory, and whether the original tax strategy was built for a pure investment asset that no longer matches the owner’s real objective.