Using 1031 Exchanges as Part of a Portfolio Evolution Strategy

The short answer

Using 1031 exchanges as part of a portfolio evolution strategy makes sense when the exchange improves the portfolio you will own next, not just the tax bill you would otherwise owe today.

That usually means the exchange changes at least one of three things in a meaningful way: concentration, operating intensity, or future exit flexibility. If it does not, the transaction may still defer gain, but it may not improve the actual quality of the portfolio.

A strong 1031 exchange improves the next portfolio, not just the current year’s tax result.

A 1031 exchange can defer gain on qualifying real property held for investment or business use, but the core rule is still deferral, not elimination. The replacement property generally carries forward the old tax history through basis mechanics, and cash or other non-like-kind property can still trigger current recognition. The timing rules are also strict: replacement property generally must be identified within 45 days and received within 180 days, or by the due date of the return including extensions if earlier.

For a high-income Florida investor, that matters because federal planning tends to carry more of the load in a no-personal-income-tax environment. Florida does not impose personal income tax, which often makes federal timing and character questions more central to the decision. A 1031 exchange can absolutely be a strong move. But it is strongest when it is used to improve portfolio architecture rather than simply postpone a future exit problem.

Introduction

Most 1031 content is built around the transaction itself: qualify the property, use a qualified intermediary, meet the deadlines, avoid boot, close on the replacement property. That is necessary, but it is not the main strategic question sophisticated investors are actually trying to answer.

The deeper question is whether the exchange improves the portfolio’s next stage. Does it reduce overconcentration in one asset, one market, one tenant profile, or one management burden? Does it improve income durability, financing flexibility, and optionality? Or does it simply roll embedded gain forward into a larger and potentially less flexible future position?

That is why we approach using 1031 exchanges as part of a portfolio evolution strategy as a multi-year planning exercise rather than a single-year deferral tactic. The IRS tells you whether the exchange qualifies. It does not tell you whether the new portfolio is better.

Key takeaways

A 1031 exchange is most useful when it changes the structure of the portfolio, not merely the timing of the tax.

Deferring gain can improve reinvestment capacity now while still increasing future exit concentration if the replacement property narrows your options later.

High-income investors should model NIIT, capital gain, and depreciation-related character issues together rather than treating the exchange year in isolation.

Real estate professional status can matter, but it is not a blanket answer for NIIT. The activity still has to fit the relevant trade-or-business and participation framework.

In Florida, the absence of personal income tax can make federal timing, character, and exit sequencing even more important.

Continue the analysis with related planning topics such as NIIT, depreciation recapture, and real estate exit strategy.

A 1031 exchange should change one of three things

A 1031 exchange should usually do more than preserve equity. It should improve the design of the portfolio.

1. Concentration

The first test is concentration.

A strong exchange may reduce dependence on one property, one geography, one tenant concentration, one asset class, or one future sale event. It may also do the opposite. That is the point. The tax code gives you broad flexibility because real property held for investment or business use is generally like kind to other qualifying real property. That flexibility is useful, but it also means the tax rules alone do not protect you from making a strategically weaker concentration decision.

For some investors, the right move is diversification: one appreciated property into multiple replacement assets. For others, it is selective consolidation: several subscale or management-heavy assets into one stronger property. Either can work. The question is whether the portfolio becomes more resilient or simply more compressed.

2. Operating intensity

The second test is operating intensity.

Some portfolios produce acceptable tax outcomes but poor ownership outcomes. Too many moving parts. Too much tenant turnover. Too much maintenance. Too many assets that looked efficient at acquisition but now demand more attention than the owner wants to provide.

A 1031 exchange can be valuable when it helps align the asset base with the actual operating model the investor wants next. That might mean moving from scattered management-heavy holdings into fewer cleaner assets. It might mean shifting from one asset class to another. It might mean using the exchange to reduce friction rather than merely delay gain.

For sophisticated readers, this is one place generic articles underserve the decision. They often mention “less management burden” as a bullet point. The more important question is whether the replacement property fits the owner’s next phase of life, capital priorities, and decision-making bandwidth.

3. Future exit flexibility

The third test is future exit flexibility.

This is where many superficially successful exchanges become less impressive on closer review. If the new property is larger, more appreciated over time, more financing-dependent, or harder to divide, the investor may have solved current tax timing while making the eventual taxable exit more concentrated and less flexible.

That does not make the exchange a mistake. It means the exchange should be judged not only by how much gain it deferred, but by what kinds of future exits it preserved or eliminated.

A good exchange often preserves optionality. A weaker one may quietly trade flexibility away in exchange for current tax relief.

We can help evaluate whether a proposed exchange improves concentration, operating fit, and future exit flexibility.

What a 1031 exchange defers — and what it leaves behind

A 1031 exchange can be powerful precisely because it lets you keep more capital invested. But it is important to stay precise about what it actually does.

Under current IRS guidance, Section 1031 applies only to qualifying real property held for business or investment use. It does not apply to real property held primarily for sale, and partnership interests themselves do not qualify as like-kind property. If money or other non-like-kind property is received, gain is recognized to that extent. That is one reason ownership structure should be settled before the exchange year rather than improvised during it.

That means a 1031 exchange is not simply a large capital-gain eraser. It is a nonrecognition regime with boundaries.

The basis point matters just as much. The basis of the property received is generally the same as the basis of the property given up, subject to adjustments. In practical terms, the replacement property often inherits more of the old tax story than investors mentally account for when they focus only on the current-year deferral.

That is why we do not think of a 1031 exchange as a one-year tactic. We think of it as a decision about where embedded gain, depreciation history, and future tax character will live next.

The “works early, breaks later” pattern

This is the pattern that many of the top-ranking pages only hint at.

Year 1: the exchange year

The exchange year often looks excellent.

Current gain is deferred. More equity remains invested. The portfolio may improve operationally. Debt may be reset. The owner may move into an asset that feels cleaner, larger, or easier to defend from a business perspective.

All of that can be real progress.

A 1031 exchange can improve the current year while still concentrating future tax and flexibility pressure at exit.

Years 2 through hold period

The middle years tell you whether the exchange was actually evolutionary or merely transactional.

Did the replacement property improve cash durability, maintenance predictability, financing resilience, and concentration risk? Did it give the owner better flexibility around future dispositions? Or did it simply roll a prior tax problem into a larger property while narrowing the next set of choices?

This is also the stage where investors can become overconfident because the exchange has already “worked.” The gain was deferred. The property closed. The strategy feels validated. But the hold period is where embedded weaknesses usually surface: more capital tied to one decision, more sensitivity to insurance or reserves, more dependence on one hold horizon, and less ability to right-size exposure without a fully taxable event.

Exit year

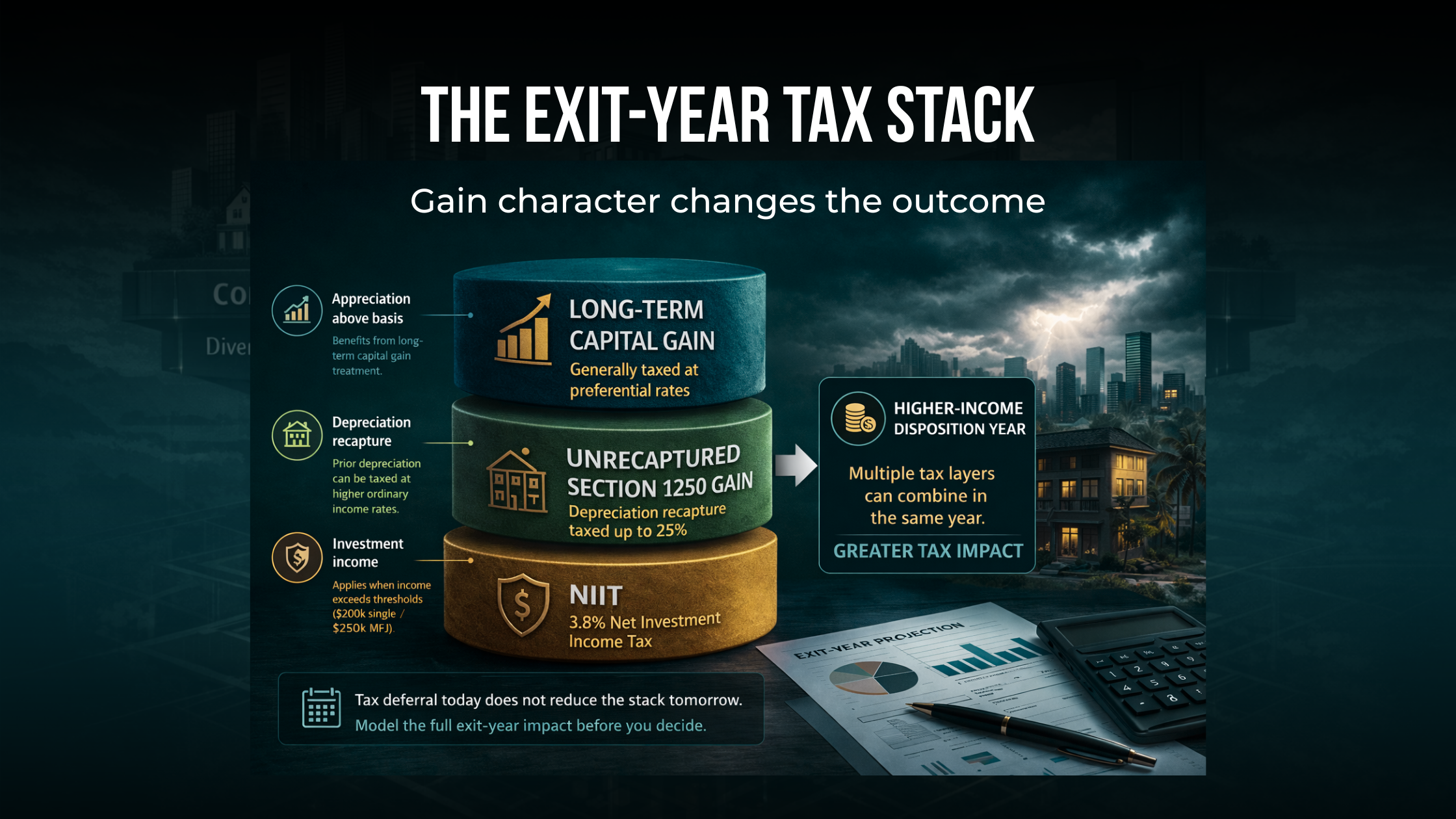

The exit year is where the deferred tax story becomes fully visible again if the next move is taxable instead of another exchange.

At that point, the investor may be dealing with long-term capital gain, unrecaptured Section 1250 gain on the portion of gain attributable to depreciation, and potentially NIIT depending on overall income and the character of the activity. The portion of unrecaptured Section 1250 gain from selling Section 1250 real property is taxed at a maximum 25% rate.

That is why a 1031 exchange can work beautifully in the exchange year and still create a tighter, heavier, less flexible exit later. The early result may be efficient. The later unwind may be more concentrated than the owner expected.

Use the concentration, operating fit, and exit-flexibility framework to compare a proposed exchange against a taxable sale.

NIIT, activity classification, and the exit-year stack

For higher-income real estate investors, NIIT is one of the biggest reasons shallow 1031 planning falls short.

The NIIT is 3.8% on the lesser of net investment income or the excess of modified adjusted gross income over the applicable threshold amount. The general thresholds remain $250,000 for married filing jointly, $125,000 for married filing separately, and $200,000 for single or head of household. The IRS also continues to treat capital gains and many forms of rental income as part of the NIIT framework unless a specific exception applies.

Future recognition should be modeled as a stacked event, not as a single generic capital gain assumption.

For a sophisticated investor, the real issue is not simply whether NIIT exists. It is whether the future exit is likely to occur in a year when ordinary income is already high and whether the activity is likely to remain investment or passive in character for NIIT purposes.

That is why the exchange year can be misleading. If the current sale is deferred, the tax pain disappears from view. But if the replacement property is later sold in a fully taxable year that already includes substantial operating income, business income, wages, bonuses, or other gains, NIIT can become part of a much heavier combined tax stack.

Real estate professional status is often discussed too casually in this context. It can matter, but it is not an automatic off-switch for NIIT. The Form 8960 instructions continue to distinguish between simply meeting real estate professional concepts and having income derived in the ordinary course of a trade or business that is not passive to the taxpayer under the relevant rules.

That means the right question is not “Can we qualify as real estate professionals?” The better question is “What is the likely character of this activity during the hold period and at exit, and how confident are we that the facts support that treatment?”

For readers who already have a CPA, this is one of the places where fragmented planning often shows up. The exchange is handled correctly. The annual returns are filed correctly. But no one models the future disposition year as its own event, with NIIT, gain character, and income stacking considered together.

Use the exit-year lens to test whether deferred gain today could create a tighter stack later.

Common misuses and oversights sophisticated taxpayers still make

The mistakes at this level are usually not beginner mistakes. They are coordination mistakes.

Treating every large gain as an automatic exchange

A large current gain does not automatically make a 1031 exchange the best move.

Sometimes the right answer is still to exchange. Sometimes the right answer is to recognize gain because the replacement property that would be required to avoid it is strategically worse than the tax bill. If the exchange locks the investor into more concentration, a more fragile operating profile, or a hold period that no longer fits the owner’s real objectives, the “tax-efficient” answer can still be the weaker portfolio answer.

Ignoring debt relief and “partial recognition” risk

Many investors focus almost entirely on cash proceeds and replacement purchase price. They pay less attention to whether leverage, net debt relief, or other transaction structure features are creating current recognition.

The broader principle is simple: partial liquidity or non-like-kind value can create current tax even inside a transaction that is mostly structured as an exchange. That is one reason we prefer to evaluate the economics and the recognition mechanics together rather than treating the exchange as either fully successful or fully failed.

Missing the constructive receipt problem

A deferred exchange is not just a sale followed by a purchase.

The taxpayer cannot simply take the proceeds and decide later to call the deal a 1031 exchange. The arrangement has to be structured so that actual or constructive receipt does not break the exchange treatment, which is why qualified intermediary mechanics matter and why the timing rules are not just administrative details.

Sophisticated investors often understand this in theory and still underestimate how early exchange planning needs to begin in practice.

Overlooking related-party traps

Related-party rules are another area where a deal can look cleaner than it is.

If the economically convenient buyer, seller, or post-exchange holder is related, the planning should be slowed down, not waved through.

Assuming “I’ll just keep exchanging forever” is a full plan

This is directionally understandable but strategically incomplete.

A portfolio that relies on repeated exchange treatment without equal attention to hold quality, asset durability, concentration, and future optionality can still drift into a weaker place over time. The tax result may be deferred repeatedly while the portfolio becomes less adaptable.

That is why “exchange again later” is not the full plan. It is only one branch of the plan.

Florida-specific planning considerations

Florida matters here, but not because the Section 1031 rules themselves are Florida-specific.

Florida’s lack of personal income tax means the federal side of the analysis often carries even more weight. That can make a 1031 exchange feel especially attractive because there is no state-level personal income tax layer competing for attention in the same way it would in many other states.

But that same fact can also obscure weak planning. When the investor is already in a federal-only mindset, it becomes easier to celebrate the current deferral and under-model the future federal exit stack.

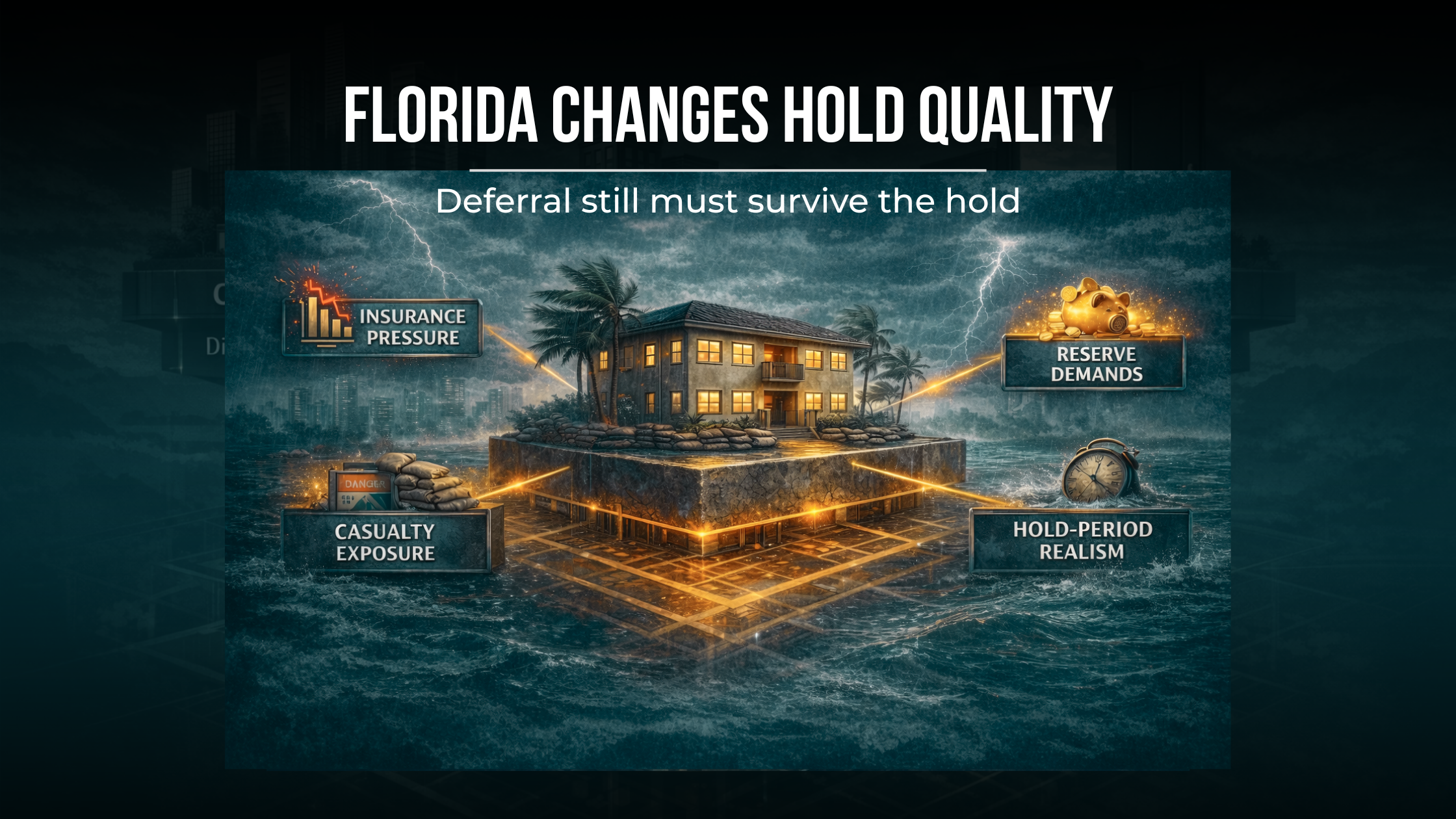

In Florida, a replacement property can look tax-efficient and still be strategically weak if the hold economics are less durable than the exchange assumes.

Florida also raises a practical hold-quality question that generic 1031 articles usually underplay. In many parts of the state, long-term asset durability is not just about rent growth and appreciation. It is also about insurance cost trajectory, reserve needs, casualty exposure, and how realistic the intended hold period actually is.

That matters because a 1031 exchange often works best when the replacement property can be held on terms the owner is genuinely prepared to live with. If the property only works under a longer hold than the investor would realistically maintain once insurance, reserves, or operating friction evolve, the exchange may have improved current tax timing without improving the durability of the actual strategy.

There is also a broader household balance-sheet angle. A Florida family may already hold a principal residence that benefits from Florida homestead rules and the Save Our Homes assessment limitation in a way that investment property does not. That does not make the residence eligible for Section 1031. It does mean that investment-property disposition decisions should be made with a full view of where the household’s real estate risk, liquidity, and tax benefits already sit.

In other words, Florida strengthens the case for disciplined federal planning. It does not reduce the need for it.

When a 1031 exchange is usually strongest

A 1031 exchange is usually strongest when several things are true at once:

the replacement property clearly improves the portfolio’s shape,

the operating model of the replacement property fits the owner’s next phase,

the exchange reduces a real weakness rather than cosmetically avoiding a tax bill,

the likely exit year has been modeled as a distinct event rather than left abstract,

and the transaction preserves optionality instead of narrowing it.

That is the version of using 1031 exchanges as part of a portfolio evolution strategy that tends to hold up best under scrutiny.

We can review whether the replacement property supports the broader portfolio strategy rather than only the current transaction.

Common 1031 Exchange Questions

Does a 1031 exchange eliminate depreciation recapture?

No. It can defer current recognition, but it does not erase the underlying depreciation history. If there is a later taxable sale, depreciation-related gain can still matter, including unrecaptured Section 1250 gain where applicable.

Can I use a 1031 exchange for my primary residence?

Generally no. Section 1031 treatment applies to qualifying real property held for investment or productive use in a trade or business, not to personal-use real property such as a primary residence.

Does a 1031 exchange automatically solve NIIT exposure?

No. The exchange can defer the current sale event, but future NIIT exposure still depends on the income level in the year of recognition and on how the activity is classified for NIIT purposes.

Conclusion

Using 1031 exchanges as part of a portfolio evolution strategy is not mainly about asking whether tax can be deferred. It is about asking whether the next portfolio is better.

A strong exchange can absolutely improve after-tax compounding by keeping more capital invested and moving the owner into assets that are better aligned with current goals. But the deeper value comes from coordination. Concentration. Operating fit. Activity classification. Future exit pressure. NIIT exposure. Depreciation-related character. Optionality.

That is why we think the most useful 1031 analysis is rarely a yes-or-no answer. It is a sequence.

What changes in the exchange year?

What improves during the hold period?

What becomes harder in the exit year?

And does the replacement property leave the investor with a more resilient portfolio than the one they sold?

That is the standard the strategy should meet.

Bring the proposed sale, replacement options, and likely hold horizon into one coordinated planning conversation.

Frequently asked questions

When does a 1031 exchange stop improving the portfolio?

A 1031 exchange usually stops improving the portfolio when the transaction solves today’s tax timing but weakens tomorrow’s flexibility. In practice, that often happens when the replacement property increases concentration, raises operating friction, narrows future exit paths, or depends on a hold period the owner is unlikely to maintain. We think the better test is not whether gain is deferred, but whether the portfolio is more resilient after the exchange than before it. If the exchange mainly pushes embedded gain into a larger, less flexible position, the strategy may be tax-efficient in the short run but strategically weaker over time.

How should we think about a 1031 exchange if we may want to sell again in a few years?

A shorter or uncertain hold period changes the analysis materially. The refined article’s logic is that the exchange year should not be judged in isolation. If the likely next move is another taxable sale within a relatively tight window, the deferred gain, depreciation history, and future character issues may come back into view sooner than expected. That does not make the exchange wrong. It means the exit year should be modeled as its own planning event from the beginning. Where the hold period is fragile, tax deferral alone is usually not enough to justify a more concentrated or less adaptable replacement property.

Can portfolio simplification through a 1031 exchange still increase risk?

Yes. Simplification and risk reduction are not always the same thing. Selling several smaller properties and exchanging into one cleaner asset may reduce management burden, but it can also increase dependence on one location, one tenant profile, one financing structure, or one future sale event. That is why the article treats concentration and operating intensity as separate tests. A simpler portfolio can be easier to manage and still be more exposed strategically. For sophisticated investors, this is one of the main reasons to evaluate simplification through a portfolio lens rather than treating it as automatically superior because it feels cleaner.

What changes in the exit year if the next sale is taxable instead of another exchange?

The exit year is when the deferred story becomes more complete. The investor may now be dealing with long-term capital gain, depreciation-related character issues, and potentially NIIT, all in a year that may already include high ordinary income or other gains. The article’s key point is that these items should be analyzed together, not one by one. A transaction that looked efficient in the exchange year can become more expensive when recognition lands in a higher-income year with less flexibility. For that reason, we think the likely exit year should be modeled separately, not treated as an abstract future event.

How should ownership structure be handled before a 1031 exchange?

The article’s logic points toward resolving ownership structure issues before the exchange year rather than trying to improvise them during the transaction. That is especially important where the investor is thinking about changes in who owns the property, how the asset is held, or whether the current structure even lines up cleanly with the intended replacement strategy. The reason is not just technical compliance. It is also strategic clarity. If the ownership structure is unsettled, it becomes harder to evaluate concentration, future exit flexibility, and the character of the activity over time. Structure is part of the planning, not a side detail.

How does Florida change the way we should evaluate the replacement property?

Florida matters less because of special 1031 rules and more because it changes the economic durability of the hold. The refined article emphasizes that in a no-personal-income-tax environment, federal timing and character issues often matter more, not less. But Florida also adds practical pressure through insurance cost trajectory, reserve needs, casualty exposure, and the realism of the intended hold period. A replacement property that looks tax-efficient may still be a weak fit if the economics are harder to carry than the investor expects. We think Florida investors should stress-test hold durability, not just current deferral, before deciding the exchange improved the portfolio.

Can repeated 1031 exchanges reduce flexibility even if each transaction looks successful?

Yes. Repeated exchanges can preserve capital and defer recognition, but they can also reduce optionality if each transaction rolls embedded gain into assets that are harder to divide, harder to exit, or more dependent on one future decision. That is why the article rejects the idea that “we can always exchange again later” is a full plan. It may be one branch of the plan, but it is not the same as preserving flexibility. Over time, a portfolio can become more tax-deferred and less adaptable at the same time. For sophisticated investors, that trade-off deserves explicit attention rather than optimistic assumptions.