Evaluating the Sustainability of Loss-Generating Assets Over Time

Direct answer

Evaluating the sustainability of loss-generating assets over time means asking whether the asset’s losses will stay useful, whether the asset is financially durable enough to hold, and whether the eventual exit preserves enough of the early benefit to justify the strategy.

For most high-income real estate investors, a loss-generating asset is sustainable only if three tests remain true at the same time:

the losses are actually deductible when they arise, rather than delayed by basis, at-risk, or passive loss limits,

the property can be carried without distorting liquidity, reserves, or broader planning flexibility, and

the exit-year tax stack does not overwhelm the early-year benefit through basis erosion, unrecaptured §1250 gain, suspended-loss timing, and NIIT.

That framing matters because many assets look efficient in Year 1 and still disappoint over the full holding period. Under current IRS rules, you apply basis and at-risk limits before the passive activity rules; rental real estate is generally passive unless an exception applies; disallowed passive losses generally carry forward; and a full deduction for previously disallowed passive losses generally comes when you dispose of your entire interest to an unrelated person in a fully taxable transaction.

So the real question is not whether an asset creates a tax loss. It is whether that loss improves the full multi-year outcome.

A loss-generating asset is only as strong as its weakest balance: tax capacity, liquidity capacity, or exit capacity.

The core issue is not whether an asset shows a loss. It is whether the loss stays useful, the property stays fundable, and the exit still works.

Introduction

For a Florida taxpayer, that distinction matters more than it might in a high-tax state. Florida’s constitution limits state taxation of the income of natural persons, so federal planning carries more of the burden. If a rental loss is passive and suspended, or if exit-year taxes absorb more value than expected, there is no separate Florida individual income tax benefit softening the result.

That is why evaluating the sustainability of loss-generating assets over time is not a narrow depreciation question. It is a coordination question. The reader who usually asks it already understands deductions, depreciation, and entity structures in broad terms. What they want is a way to tell the difference between an asset that is genuinely tax-efficient over time and one that simply produces an attractive first-year narrative.

Key takeaways

A tax loss and a usable tax loss are not the same thing. Basis and at-risk limits apply before passive loss rules, and passive losses usually cannot offset nonpassive income.

For many high-income readers, the familiar $25,000 rental loss allowance is not the real planning engine. The allowance phases down above $100,000 of modified AGI and is generally gone at $150,000 or more.

Accelerated depreciation can help early, but it also lowers basis and can make the exit-year mix less favorable than the acquisition-year model suggested.

A change in classification does not always free older losses the way investors expect. Former passive activity rules and NIIT treatment can create a second layer of friction even after an activity becomes nonpassive.

Exit modeling should include NIIT for high-income households, not just capital gain rates and recapture language. NIIT is 3.8% on the lesser of net investment income or the excess of MAGI over the statutory threshold amounts.

In Florida, sustainability is partly a tax question and partly a hold-economics question. Insurance, reserves, property-tax treatment, and storm-related liquidity needs can determine whether a paper loss is worth carrying.

Our related guides expand the issues that usually determine whether a deduction-heavy strategy holds up.

What sustainability actually means

We usually evaluate sustainability through three balances: tax capacity, liquidity capacity, and exit capacity.

An asset can fail on any one of the three. That is the mistake behind many deduction-heavy plans. The asset is labeled tax-efficient because it produces a loss, even though the loss is trapped, the property is expensive to carry, or the exit is likely to occur in a year when the owner is already exposed to high ordinary income, high capital gain pressure, or NIIT.

1. Tax capacity

The first question is whether the loss can be used when it arises.

For many owners, the ordering rules do most of the work here. Basis limitations, at-risk rules, and passive activity rules do not ask the same question, and they do not operate in the same order. If the loss does not survive the earlier limitations, the passive analysis is not even the first bottleneck. For partners and S corporation shareholders, those limits are applied at the owner level, which means entity choice does not eliminate the issue. It often just changes where the limitation shows up.

A sustainable loss-generating asset therefore needs tax capacity, not just deductions. The practical test is straightforward: do you have passive income, nonpassive treatment, or a clearly modeled release event that makes the loss matter on a realistic timeline?

2. Liquidity capacity

The second question is whether the property is economically durable enough to hold.

This is the part tax articles often skip. A property can produce a healthy taxable loss because depreciation is large, while also draining cash through debt service, insurance, vacancy, reserves, repairs, or irregular capital demands. That is not a contradiction. It is common.

We do not treat a property as sustainable merely because the return shows a loss. A sustainable asset is one that fits the cash plan, not just the tax return. If the property repeatedly requires outside liquidity to preserve a tax profile that you cannot currently use, the deduction is doing less work than it appears.

3. Exit capacity

The third question is what happens when the position is finally unwound.

This is where many front-loaded tax strategies become more honest. Basis has usually been reduced by prior depreciation. Suspended passive losses may become deductible if the disposition is structured the right way. Unrecaptured §1250 gain may apply to the real property component. NIIT may apply if the household’s MAGI exceeds the applicable threshold. And if the transaction is not a full disposition of the entire interest to an unrelated person in a fully taxable transaction, the release point may not work the way the owner expected.

That is why a sustainable loss-generating asset is not merely one with strong deductions. It is one with a credible exit.

We frame sustainability by testing loss usability, carry demands, and exit pressure together.

The multi-year sequence most investors actually need

The cleanest way to evaluate the sustainability of loss-generating assets over time is to model the asset in phases rather than in one blended projection.

This sequence shows why a strong acquisition-year deduction does not, by itself, prove long-term tax efficiency.

The right way to evaluate the asset is by phase, not by headline deduction. Each stage changes what the earlier losses are actually worth.

Year 1: the asset looks efficient

This is where the strategy usually presents well. A cost segregation study, renovation cycle, bonus depreciation where available, startup vacancy, or large repair profile can create a meaningful tax loss. On paper, the asset looks productive immediately.

But the critical question is not the size of the Year 1 deduction. It is the character of the income it can offset. If the activity is passive and you do not have enough passive income, much of that first-year tax benefit may be deferred. If you expect the property to work because you are active in the business generally, but not because this activity is actually nonpassive, the model starts out with a false assumption.

The right use case for early acceleration is narrow but powerful: you either have present tax capacity, or you have a deliberate timeline for when and how the losses will be absorbed. Without one of those two conditions, a large early deduction may be more cosmetic than economic.

Holding years: the loss becomes less useful

This is where many assets move from attractive to ambiguous.

The property may continue generating deductions, but the owner’s ability to use them does not necessarily improve. Suspended passive losses can accumulate for years. If the owner later qualifies as a real estate professional or otherwise changes the activity’s status, prior suspended losses are not automatically liberated in full. Under the former passive activity rules, prior-year unallowed losses are generally allowed only to the extent of current-year income from that activity, and NIIT treatment can have its own separate limitations.

That is a sophisticated planning blind spot. Investors often assume a status change solves the backlog. Sometimes it helps. It does not necessarily erase the history.

Holding years are also where cash pressure becomes visible. A property that was easy to defend when acquisition assumptions were fresh may become harder to justify if insurance rises, maintenance clusters, or reserves need to be rebuilt. In Florida, that can shorten a holding period that was originally necessary for the tax plan to work.

Exit year: the spreadsheet gets honest

Exit year is where the full tax story usually becomes clear.

If you dispose of your entire interest in a passive activity to an unrelated person in a fully taxable transaction, the passive loss limitation generally falls away for that activity. That can finally make suspended losses valuable. But the same sale can also expose how much basis was consumed to create the earlier deductions. The portion of gain treated as unrecaptured §1250 gain is taxed at a maximum 25% rate, and NIIT can apply to real estate gain for high-income households if the property is within NIIT’s reach for that taxpayer.

This is the works-early, breaks-later pattern that weaker articles often miss. The asset may still have been worth owning. But the real comparison is not deductions versus no deductions. It is earlier deductions versus later tax friction, after timing, liquidity, and classification are all accounted for.

A second failure mode appears when the owner expected an exit but not a taxable one. A partial sale, a transaction that is not fully taxable, or a structure that does not amount to disposition of the entire interest can leave suspended losses where they were. That does not make the strategy wrong. It means the unwind assumptions were too loose.

We review how acquisition-year deductions, holding-year constraints, and exit-year taxes interact before decisions become harder to unwind.

Classification is the hinge point

Classification is often the single variable that separates a current benefit from a deferred one.

The same property can produce very different tax outcomes depending on how the activity is classified and how the ownership facts are organized.

Classification is not a technical side issue. It often decides whether a deduction is current, delayed, or structurally difficult to defend.

That is why structure and participation should be modeled before the deduction strategy is treated as real.

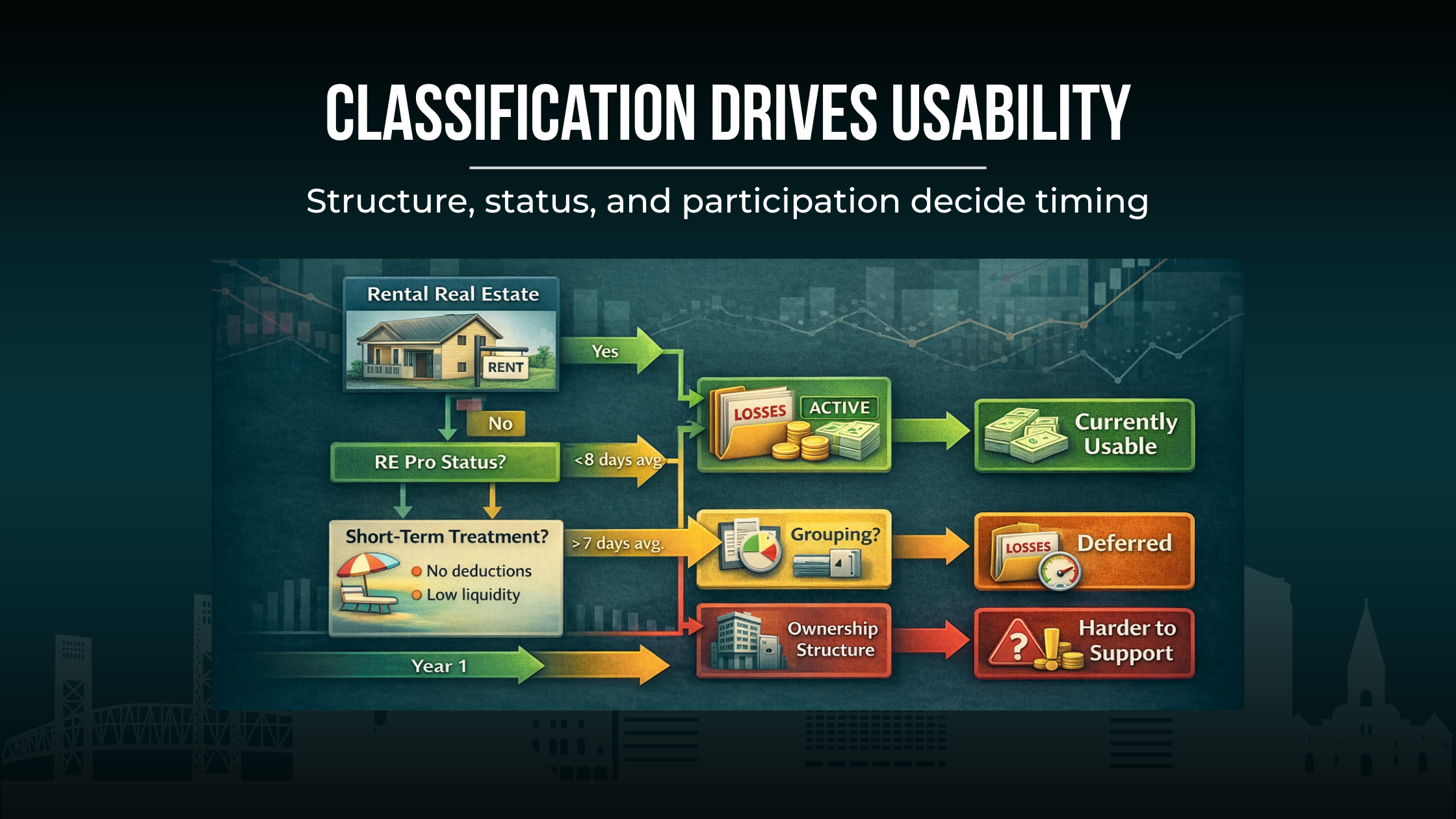

Most rental real estate is passive by default

Rental real estate is generally passive even if the owner is heavily involved. That default is the reason many affluent taxpayers overestimate the present value of depreciation-heavy losses. They are managing properties, approving expenditures, reviewing operations, and still not generating losses that can offset salary, operating business income, or other nonpassive earnings.

Real estate professional status can change the answer

Real estate professional status can change the answer materially, but only when the underlying tests are truly met and the owner also materially participates. For multiple rental activities, election and grouping decisions matter because each interest in rental real estate is generally treated as a separate activity unless the taxpayer elects otherwise.

This is where ownership structure becomes strategic rather than administrative. A portfolio held across multiple entities, with uneven ownership and inconsistent participation, may still be tax-plannable. It is simply harder to make the intended answer easy.

Short-term rentals can change the analysis too

Short-term rentals matter in Florida because they can move the activity outside the default rental-activity framework. Under Publication 925, one exception applies when the average period of customer use is 7 days or less. Another applies when the average period is 30 days or less and significant personal services are provided. Once an activity falls outside the default rental category, the analysis shifts back toward material participation and related rules.

That can be an opportunity. It can also be a trap. If the operational facts are inconsistent, or if the owner assumes that short-term automatically means nonpassive, the planning can outrun the record.

We review whether your real estate tax strategy is coordinated across holding period, liquidity needs, and eventual disposition.

Cost segregation and accelerated depreciation are tools, not verdicts

Cost segregation is most useful when it improves the full life-cycle economics of the asset rather than simply magnifying the first-year deduction.

That usually means four conditions are present:

the losses are usable now or are expected to be used on a defined timeline,

the hold period is long enough, or the exit is planned carefully enough, that basis reduction is not an afterthought,

the property is economically durable enough to carry without straining the rest of the plan, and

the ownership and classification facts support the intended treatment.

When those conditions are missing, accelerated depreciation can be directionally correct but strategically weak. It may create a large early tax story while increasing later gain pressure or recapture-related friction. The question is not whether cost segregation is available. It is whether front-loading deductions improves the whole calendar.

Common misuses and oversights sophisticated taxpayers still make

Advanced taxpayers usually do not miss the vocabulary. They miss the collisions between rules.

Mistaking a tax loss for a usable tax loss

A Schedule E loss can be real and still do little in the current year. If basis, at-risk, or passive limits intervene, the loss may be deferred rather than monetized. That is not just a compliance issue. It changes the asset’s true after-tax profile.

Relying on the $25,000 rental loss allowance when income is already too high

For affluent households, this is often an analytical detour. The special allowance phases down above $100,000 of modified AGI and is generally unavailable once modified AGI reaches $150,000. It matters for some taxpayers. It is rarely the real answer for the reader this article is written for.

Assuming any exit will release suspended losses

It usually does not. The general release rule is keyed to disposal of the entire interest to an unrelated person in a fully taxable transaction. That means a partial sale, a nonrecognition-oriented move, or a structure that does not amount to complete disposition can leave the owner with far less immediate relief than expected.

Modeling the sale as “capital gain only”

That model is too clean for real property. Real estate gain on sale can include unrecaptured §1250 gain, ordinary-income effects in other settings, and NIIT exposure on top of the general long-term capital gain discussion. A sale model that only asks for capital gain rate is usually underbuilt.

Assuming NIIT relief and passive-loss relief always line up cleanly

They do not always line up the way taxpayers expect. Form 8960 instructions distinguish between activities that were always passive and activities that became former passive activities. That means a status change can improve one part of the tax picture without simplifying NIIT treatment to the same degree.

Letting ownership structure reduce flexibility

Loss planning is often defeated by structure before it is defeated by law. Separate entities, limited-partner positions, inconsistent ownership percentages, and casual grouping assumptions can all make it harder to support material participation or preserve optionality around exits. The IRS allows grouping when activities form an appropriate economic unit, but that is a facts-and-circumstances standard, not a free clean-up tool after the portfolio becomes unwieldy. Limited partners also face narrower material participation pathways.

We can test whether the apparent tax efficiency still holds once suspended losses, NIIT, and sale-year friction are modeled together.

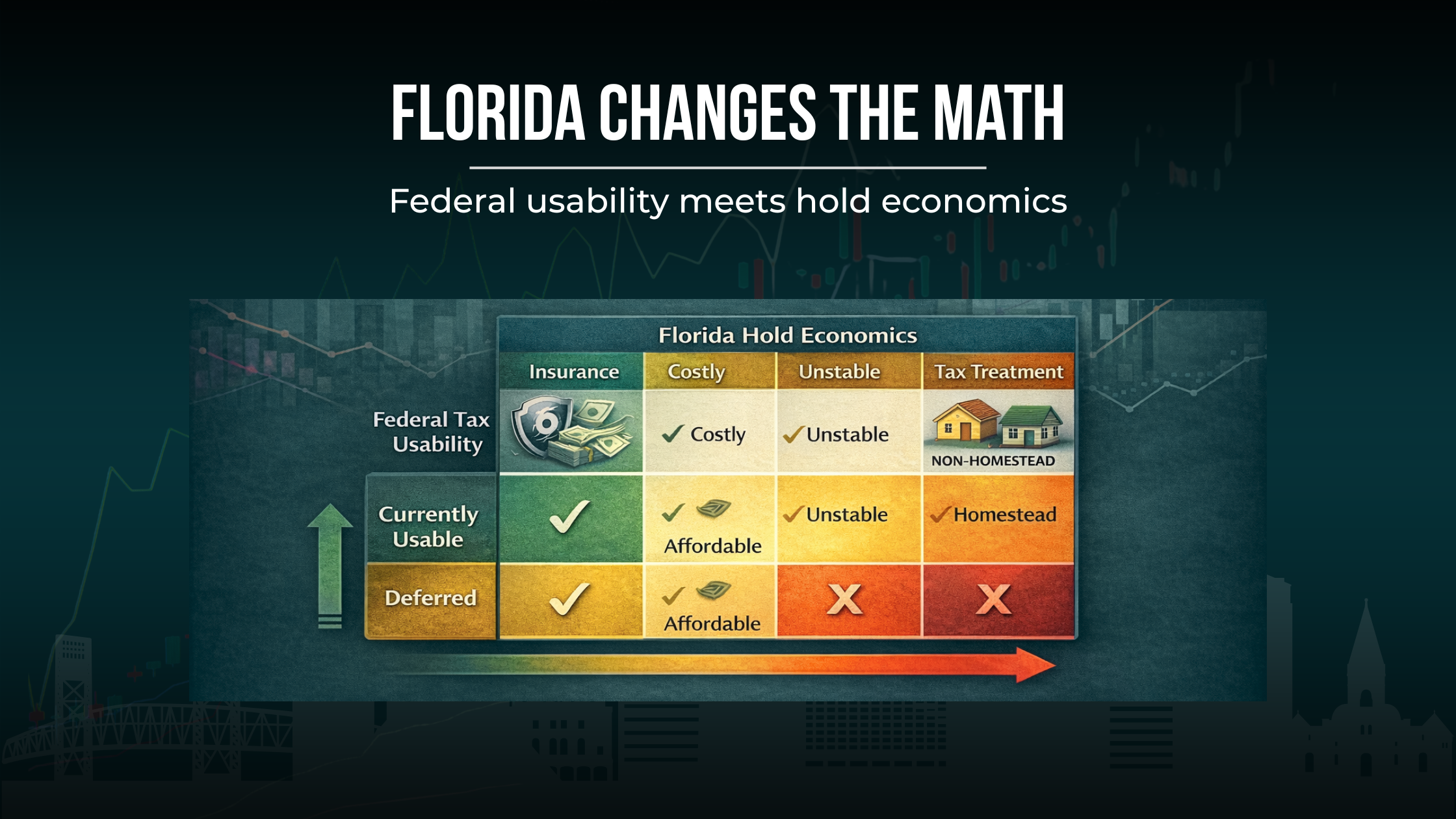

Florida-specific planning considerations

Florida does not improve the federal tax mechanics of a passive loss. It raises the stakes around getting those mechanics right.

Because the state does not tax the income of natural persons the way many other states do, a federal loss that is unusable remains unusable in the place that matters most for the individual return. That is why Florida investors often benefit from being more skeptical, not less, about deduction-heavy acquisition narratives.

Florida does not change the federal rules, but it does change how hard those rules hit when a loss is delayed or overvalued.

In Florida, a paper loss can still be a weak strategy if the asset is expensive to carry or the hold economics are unstable.

This is where federal tax efficiency and real carry economics have to be read together, not separately.

Florida also makes hold economics unusually important. Property-tax treatment differs between homestead and non-homestead property. Homestead property is subject to the Save Our Homes limitation, while non-homestead property is subject to a different assessment limitation. A sale, loss of homestead status, or other change in ownership can reset those economics in ways that affect hold-versus-sell decisions even when the federal tax analysis is unchanged.

For readers with a mix of personal, seasonal, and investment property, that matters more than it first appears. Some assets are easier to hold because the property-tax path is more stable. Others need a higher pre-tax return or better federal tax usability to remain worth carrying.

For Florida readers, short-term and seasonal rental exposure also changes the planning conversation. If a property’s customer-use pattern or service model changes, the federal classification analysis may change with it. That can affect whether the losses are passive, nonpassive, or simply delayed. And because Florida properties can also face heavier insurance and reserve demands, the most important sustainability question is often whether the tax plan and the cash plan still agree.

Passive Loss Edge Cases Every Rental Owner Should Understand

Can a passive loss-generating rental still be worth keeping if the losses are suspended?

Yes. Suspended losses are deferred value, not necessarily wasted value. A passive asset can still deserve a place in the portfolio if the economics are strong, the hold period is intentional, and the eventual exit is modeled clearly enough that the deferred tax benefit still contributes to the overall return.

Does selling part of an asset release suspended passive losses?

Not usually in the way owners hope. The general release rule turns on disposing of the entire interest to an unrelated person in a fully taxable transaction. That is why the form of the exit matters almost as much as the timing.

Do Florida short-term rentals automatically create nonpassive losses?

No. A short-term rental may fall outside the default rental-activity framework, but that only changes the path of the analysis. You still need the operational facts and participation profile to support the intended treatment.

Does changing an activity from passive to nonpassive free all old suspended losses?

Not necessarily. If an activity becomes a former passive activity, prior-year unallowed losses are generally allowed only to the extent of current-year income from that activity, and NIIT treatment can remain more nuanced than the ordinary income tax result alone suggests.

Conclusion

Evaluating the sustainability of loss-generating assets over time is not about chasing the biggest deduction. It is about determining whether the asset still makes sense after you account for limitation rules, ownership structure, holding-period economics, and exit-year pressure.

The strongest plans do not treat passive losses, cost segregation, NIIT, and disposition as separate conversations. They model all four on one timeline. That is what usually separates a genuinely efficient asset from one that merely looked efficient at acquisition.

For high-income Florida investors, that discipline matters even more. With no state individual income tax layer to dilute a weak federal result, the federal sequencing has to carry the strategy. The goal is not a good loss year. It is a durable multi-year outcome.

Frequently Asked Questions

When does a loss-generating asset stop improving the overall plan?

It usually stops improving the plan when the deductions are still arriving but the investor no longer has a realistic path to use them on a helpful timeline. That can happen when passive losses keep accumulating, when the property needs more outside liquidity to carry, or when the expected exit becomes less clean or less taxable than originally modeled. In other words, the strategy often stops working before the asset stops generating losses. We usually see the break point when tax capacity, cash capacity, and exit capacity stop moving together.

How should we think about a short expected hold period before accelerating deductions?

A short hold period usually raises the standard for acceleration. Early deductions may still help, but the shorter the holding window, the more important basis reduction and sale-year tax friction become. If the losses are not clearly usable in the near term, front-loading them can simply shift value into a later year when unrecaptured §1250 gain, NIIT, or release timing rules matter more. That does not make acceleration wrong. It means the question is not availability of the deduction, but whether the timing still improves the full life-cycle result.

Why can a status change help current deductions but still leave older losses constrained?

Because a change in classification affects future treatment more cleanly than it fixes historical treatment. If an activity becomes nonpassive later, that can improve the character of current-year results, but prior suspended passive losses may still be governed by former passive activity rules. That means the older backlog may be released only to the extent current income from that activity supports it, rather than all at once. For sophisticated taxpayers, that is one of the most important sequencing collisions: today’s status can improve current planning without fully solving yesterday’s trapped losses.

What should be modeled before assuming the exit year will “clean things up”?

We should model more than sale price and headline gain. The exit-year analysis should test whether the transaction is a full disposition of the entire interest, whether it is fully taxable, how much basis has been reduced by prior depreciation, whether suspended losses are actually released, and whether NIIT applies to the gain. Many investors assume that eventual sale fixes everything. Sometimes it does. Sometimes the sale reveals that the original strategy depended on a cleaner unwind than the structure or transaction format will actually deliver.

How can entity and ownership structure quietly reduce the value of a tax-efficient property?

Structure can reduce value by limiting flexibility before it limits deductions. A property may look efficient on its own, but separate entities, uneven ownership, limited-partner positions, or inconsistent participation can make grouping, material participation, and exit planning harder to support. The tax law may still permit planning, yet the structure can make the intended result harder to reach and harder to defend. For high-net-worth households with multiple properties and changing participation levels, structure often determines whether a strategy remains workable as the portfolio gets more complex.

Why does Florida make paper losses easier to overvalue?

Florida can make paper losses easier to overvalue because there is no state individual income tax layer on natural persons to make a federally unusable loss feel partially useful. If the federal loss is passive and suspended, the individual return usually does not get a separate state-income-tax benefit to soften that outcome. Florida also makes hold economics more visible. Insurance, reserve needs, storm exposure, and property-tax treatment can turn a technically attractive tax profile into an economically fragile holding pattern. That is why we usually evaluate Florida properties through both federal tax utility and real carry economics.

When does tax efficiency start hurting flexibility instead of helping it?

Tax efficiency starts hurting flexibility when the owner becomes too committed to preserving a deduction pattern that no longer fits the broader plan. That can happen when an asset is held longer than intended just to protect suspended losses, when a sale is delayed because the exit-year stack was never modeled well, or when capital stays tied up in a property that is tax-efficient on paper but expensive to carry. In those cases, the tax profile may look disciplined while the broader balance sheet becomes less adaptable. A strong strategy should widen future options, not narrow them.