April 2026 Real Estate Tax Changes You Need to Know

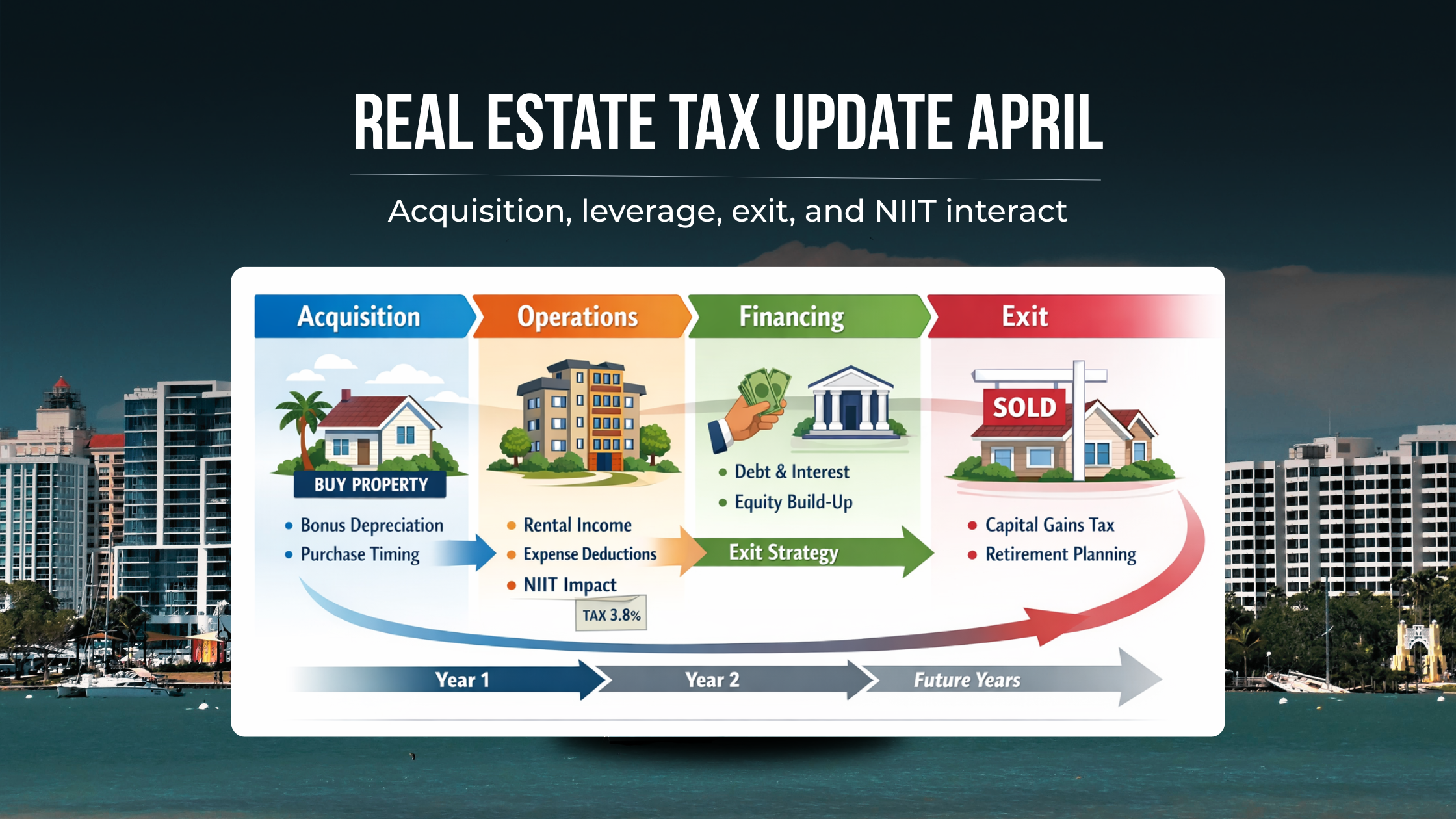

For high-income Florida taxpayers, the real issue heading into April 2026 is not whether there are still deductions to claim. It is whether income, gain, depreciation, leverage, and liquidity are being sequenced in a way that still works when a property is refinanced, exchanged, or sold. In a no-state-income-tax environment, federal character and timing carry more of the economic weight, so a fragmented plan shows up quickly in the form of stacked ordinary income, capital gain, NIIT, and recapture.

The 2026 landscape is more stable than many investors expected a year ago, but that stability can be misleading. The ordinary rate structure remains in the 10% to 37% range, long-term capital gain thresholds have been indexed for 2026, 100% bonus depreciation is permanently available for qualifying property acquired after January 19, 2025, and the business interest limitation became more favorable again for many leveraged taxpayers. At the same time, NIIT thresholds remain frozen, overall itemized deductions can again be reduced for taxpayers in the top bracket, and beginning in 2026 certain personal casualty losses can include state-declared disasters.

For Florida real estate investors, that combination changes the planning emphasis. The best 2026 real estate tax planning is less about finding one more write-off and more about deciding which deductions to accelerate, which elections to preserve, which owner should hold which asset, and when an exit belongs in the household income cycle. That is especially true where short-term rentals, homestead decisions, insurance deductibles, and storm-related loss risk affect both the hold period and the sale decision.

The tax outcome is usually determined by the sequence of decisions across years, not by any single deduction claimed in Year 1.

We can help you evaluate how acquisition, depreciation, financing, and exit timing fit together before a 2026 sale year becomes more expensive than expected.

Key Takeaways

The main 2026 real estate tax change is not simply stronger deductions. It is a wider spread between acquisition-year tax results and exit-year tax costs.

NIIT still operates like a second tax system for many high-income investors, and real estate professional status alone does not remove rental income or sale gain from NIIT.

Permanent 100% bonus depreciation makes cost segregation more powerful again, but it also raises the importance of hold-period discipline, recapture modeling, and exit-year sequencing.

Electing out of §163(j) should be modeled, not assumed. The election is irrevocable and can force ADS with no special depreciation allowance on affected property.

In Florida, federal planning carries more weight because there is no personal income tax, while property-tax structure, insurance deductibles, and disaster-loss rules can still change the economics of holding or selling.

Sale-year planning should be coordinated with retirement distributions, deferred compensation, business income, and other household cash events, because the same transaction can be taxed very differently depending on the year it lands.

What Actually Changed for 2026

The expected 2026 reversion to pre-2018 ordinary brackets did not happen. The current bracket structure continued, and the 2026 inflation adjustments moved the bracket thresholds and capital gain thresholds upward. For many real estate investors, that means the central planning problem is no longer a broad rate reset. It is how current law interacts with basis, debt, participation, and sale timing.

The most important real-estate-specific change is that the additional first-year depreciation deduction is now permanently 100% for qualified property acquired after January 19, 2025. That materially strengthens cost segregation and land-improvement planning, but only for property that actually qualifies and is placed in service under the governing timing rules. Investors with projects or acquisitions straddling January 19, 2025 still need to analyze acquisition date, binding-contract rules, and, in some cases, component-level treatment.

Leverage also deserves a new 2026 model. For tax years beginning after December 31, 2024, depreciation, amortization, and depletion are again added back when computing adjusted taxable income under §163(j). For tax years beginning after December 31, 2025, §163(j) generally applies before most mandatory or elective interest capitalization rules. That combination can improve deductible interest capacity for some real estate businesses while changing the relative value of an electing real property trade or business election.

Another underappreciated 2026 change matters more in Florida than in many states. Beginning in 2026, the personal casualty loss rules are expanded so certain state-declared disasters can qualify, not only federally declared disasters. That does not turn every storm-related repair into a deduction, and insurance reimbursement still matters, but it makes basis records, reserve planning, and loss documentation more valuable for Florida property owners.

2026 Federal Rate Map for Real Estate Investors

Ordinary Income Brackets for 2026

Federal ordinary income tax brackets by filing status

| Rate | Single | Married Filing Jointly | Married Filing Separately | Head of Household |

|---|---|---|---|---|

| 10% | Up to $12,400 | Up to $24,800 | Up to $12,400 | Up to $17,700 |

| 12% | $12,400 to $50,400 | $24,800 to $100,800 | $12,400 to $50,400 | $17,700 to $67,450 |

| 22% | $50,400 to $105,700 | $100,800 to $211,400 | $50,400 to $105,700 | $67,450 to $105,700 |

| 24% | $105,700 to $201,775 | $211,400 to $403,550 | $105,700 to $201,775 | $105,700 to $201,750 |

| 32% | $201,775 to $256,225 | $403,550 to $512,450 | $201,775 to $256,225 | $201,750 to $256,200 |

| 35% | $256,225 to $640,600 | $512,450 to $768,700 | $256,225 to $384,350 | $256,200 to $640,600 |

| 37% | Over $640,600 | Over $768,700 | Over $384,350 | Over $640,600 |

Long-Term Capital Gain Thresholds for 2026

Federal long-term capital gain thresholds by filing status

| Rate | Single | Married Filing Jointly | Married Filing Separately | Head of Household |

|---|---|---|---|---|

| 0% | Up to $49,450 | Up to $98,900 | Up to $49,450 | Up to $66,200 |

| 15% | $49,450 to $545,500 | $98,900 to $613,700 | $49,450 to $306,850 | $66,200 to $579,600 |

| 20% | Over $545,500 | Over $613,700 | Over $306,850 | Over $579,600 |

NIIT Thresholds

Modified adjusted gross income thresholds for net investment income tax

| Filing Status | MAGI Threshold |

|---|---|

| Married Filing Jointly / Qualifying Surviving Spouse | $250,000 |

| Married Filing Separately | $125,000 |

| Single / Head of Household | $200,000 |

NIIT is 3.8% and applies to the lesser of net investment income or the excess of MAGI over the threshold. These thresholds are statutory and are not indexed for inflation.

These tables still do not show the full tax picture on a real estate exit. A sale can include ordinary recapture, unrecaptured §1250 gain, residual long-term capital gain, and NIIT. The portion of unrecaptured §1250 gain is taxed at a maximum 25% rate, while any gain treated as ordinary recapture is outside the long-term capital gain rate structure altogether. That is why “my capital gain rate is 20%” is often a misleading starting point for high-income investors.

Income Stacking Matters More Than Deduction Hunting

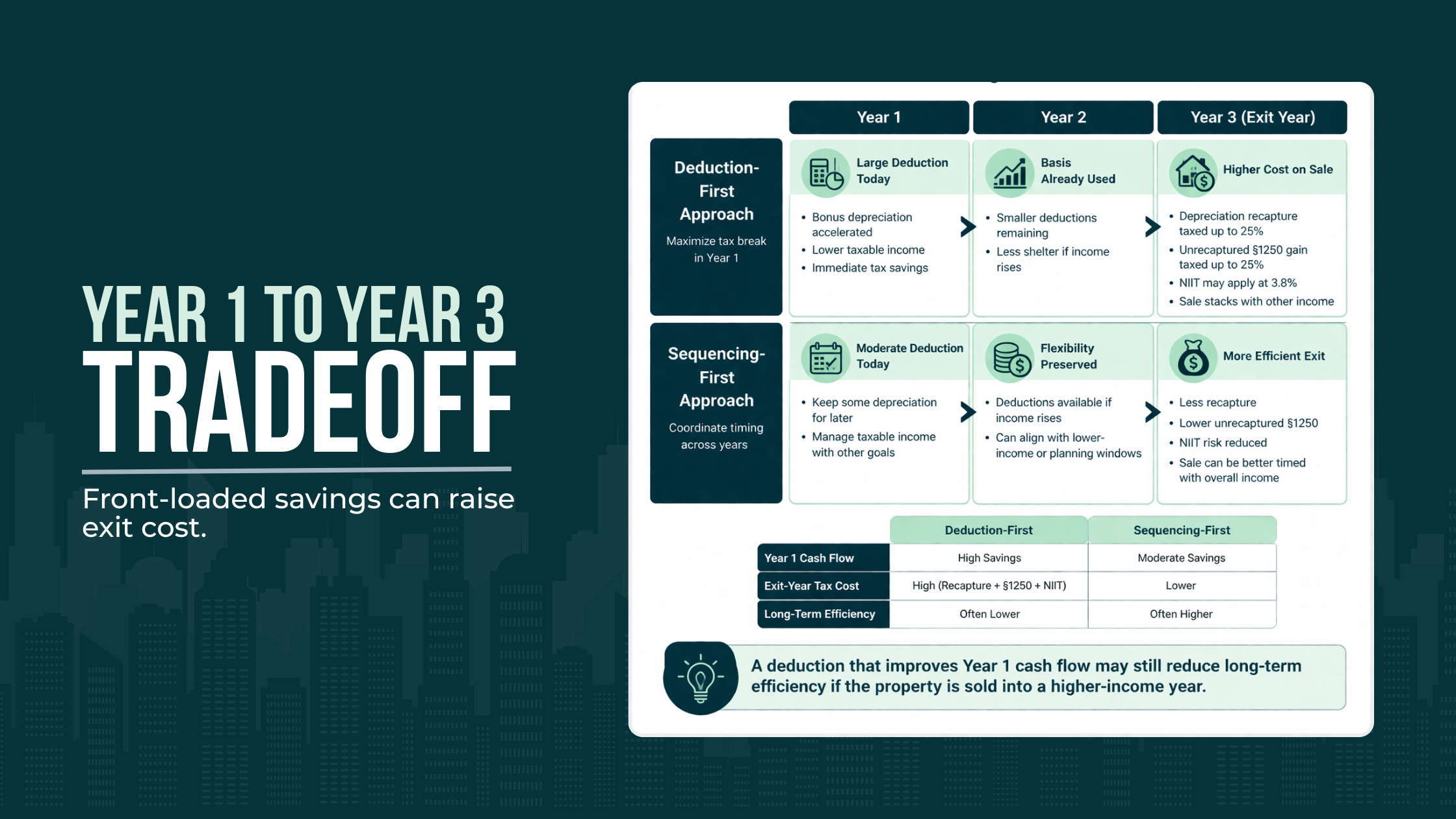

Acquisition-year deductions are easy to admire because they are visible. Exit-year taxes are easier to underestimate because they are fragmented across multiple buckets. A 2026 real estate tax planning model that stops at Year 1 bonus depreciation misses the real question, which is whether that deduction still makes sense once the property is sold into a year already carrying business income, deferred compensation, Roth conversion income, or required distributions.

The sequence often looks like this. In Year 1, a Florida investor buys a property, performs a cost segregation study, and uses 100% bonus depreciation on qualifying components against high ordinary income. In Year 2, the property produces cash flow but less depreciation shelter. In Year 3, the owner sells in the same year a closely held business distributes unusually high income or retirement cash flow begins. The sale then stacks ordinary recapture, unrecaptured §1250 gain, long-term capital gain, and possibly NIIT on top of already elevated household income.

A deduction that improves Year 1 cash flow may still reduce long-term efficiency if the property is sold into a higher-income year.

That does not mean front-loading deductions is wrong. It means the deduction should be tied to a hold-period thesis. If the likely path is a shorter hold, a refinance followed by sale, or a sale during peak ordinary-income years, the right strategy may be restraint rather than maximum acceleration. For many high-income households, the best tax savings comes from placing the sale in the right year, not from extracting the biggest deduction in the acquisition year.

NIIT Is Still the Quiet Second Tax System

NIIT remains one of the most important blind spots in real estate tax planning for households above $250,000 of joint MAGI or $200,000 for single and head-of-household filers. Because the thresholds are not indexed, more affluent households drift into NIIT over time even without a statutory rate increase. That matters in Florida because there is no state income tax layer to distract from how much of the federal drag is being driven by NIIT rather than the headline capital gain rate.

Rental income and gain from the disposition of rental real estate are often included in net investment income unless they are derived in the ordinary course of a non-§1411 trade or business. Real estate professional status helps for passive-loss purposes, but the IRS is explicit that real estate professional status alone does not establish that rental real estate rises to the level needed for NIIT exclusion. Material participation and trade-or-business posture still matter.

The Form 8960 instructions make this especially important in the sale year. If a real estate professional satisfies the relevant safe harbor, gross rental income is treated as derived in the ordinary course of a trade or business and is not included in NII. If the taxpayer qualifies in the year of disposition, gain or loss from the disposition of the rental real estate activity is also treated as outside NII. The practical point is simple: participation logs are not housekeeping. They are part of exit planning.

This is where many high earners lose money through drift rather than through a bad strategy. They materially participated when the asset was younger, then outsourced more operations, reduced involvement, or restructured management as the sale approached. If that change weakens the nonpassive posture in the disposition year, the same property can produce a meaningfully different federal tax result.

We can review how NIIT, participation, and sale-year income may interact across your real estate holdings and broader household plan.

Permanent 100% Bonus Makes Cost Segregation More Useful and Easier to Misuse

Permanent 100% bonus depreciation changes the value of cost segregation, but it does not change the questions that should come first. Before a study is commissioned, the investor should know whether the asset is a core long-term hold, an exchange candidate, a medium-term harvest candidate, or a likely basis step-up asset in a broader family plan. The right depreciation profile for those four categories is not the same.

A cost segregation study can sharply improve current-year cash flow because shorter-life property and land improvements can be identified and accelerated. That can be valuable when the taxpayer has durable ordinary income and a realistic hold period. But the more deductions you pull forward, the more basis you consume, and the more carefully you need to model ordinary recapture and unrecaptured §1250 gain later. A strong acquisition-year result can be the front end of a weaker lifetime result if the property is sold earlier than planned.

There are also quieter failure modes. A large deduction does less work if it lands inside a passive bucket the owner cannot currently use. It may also reduce future depreciation shelter in years when the property is producing the most cash. And if the investor later decides not to exchange the asset, a previously attractive cost-seg result can create a more painful exit-year tax character mix than expected. Cost segregation remains a valuable planning tool in 2026, but only when it is subordinate to the asset plan.

Leveraged Portfolios Need a New §163(j) Model

Many investors got into the habit of treating the electing real property trade or business election as the routine answer to §163(j). In 2026, that deserves a fresh model. Because ATI once again adds back depreciation, amortization, and depletion for tax years beginning after 2024, some leveraged real estate businesses can now support more deductible interest without giving up depreciation flexibility.

The election still matters, but it now has a clearer opportunity cost. An electing real property trade or business can avoid the §163(j) limitation for that trade or business, but the election is irrevocable and generally requires ADS for nonresidential real property, residential rental property, and qualified improvement property used in the trade or business. The IRS instructions also state that the taxpayer is not entitled to the special depreciation allowance for that property. Once 100% bonus became permanent again, that trade-off became more expensive in many cases.

The 2026 ordering change matters as well. For tax years beginning after December 31, 2025, §163(j) is generally applied before most mandatory or elective capitalization provisions. That changes modeling for development-heavy or improvement-heavy structures because the relationship between deductible interest, capitalized interest, and basis timing is not the same as it was under the earlier framework. The practical implication is that debt strategy, depreciation strategy, and sale strategy need to be modeled together.

Active vs Passive Treatment Often Becomes Binding at Exit

Investors usually focus on passive status when they want to use losses. The more consequential moment is often the year they want to sell. Passive or nonpassive treatment can affect whether suspended losses free up, whether NIIT still applies, and whether the owner can support a trade-or-business position strong enough to change the tax character of the sale year.

Florida’s short-term rental market makes this more than a technical issue. Under Publication 925, an activity generally is not treated as a rental activity for passive-loss purposes if the average period of customer use is seven days or less, or thirty days or less when significant personal services are provided. That does not make the income automatically nonpassive. It means material participation becomes the key test. For owners of beach, resort, and seasonal assets, that distinction can materially change both operating-year and exit-year planning.

Suspended passive losses add another layer. Generally, previously disallowed passive activity losses can be fully deducted in the year the taxpayer disposes of the entire interest in the activity, but the disposition needs to be the kind of fully taxable disposition that actually triggers release. That is why a planned exchange, installment structure, partial sale, or entity-level transaction has to be evaluated before anyone assumes the passive loss carryforward will solve the sale year.

Exit Planning: Depreciation Recapture, Unrecaptured §1250 Gain, and Unwind Scenarios

A real estate exit is rarely taxed at one rate. Gain attributable to certain depreciable components can be recaptured as ordinary income. Gain attributable to depreciation on §1250 real property can become unrecaptured §1250 gain, taxed at a maximum 25% rate. What remains may qualify for long-term capital gain treatment, and NIIT can still apply depending on the taxpayer’s posture and income. Exit planning starts to improve only when those buckets are modeled separately.

Exit planning improves when each gain component is modeled separately instead of assuming one capital gain rate applies to the entire transaction.

That is why exit timing should be evaluated against business income, retirement distributions, suspended losses, and potential exchange options before the transaction structure is set.

This is also where unwind scenarios matter. A sale after aggressive cost segregation has a different profile than a sale of a largely unsegregated asset. A sale after years of passive-loss carryforwards behaves differently from a sale where the owner has already converted the activity to nonpassive use. A sale following a refinancing cycle can produce strong cash proceeds and a poor tax year if the refinance delayed the disposition into a year with higher ordinary income.

Like-kind exchanges still matter in 2026, but they need to be framed correctly. A §1031 exchange can defer current gain if properly executed, and the basis of the replacement property generally carries over with adjustments, preserving deferred gain for later recognition. That makes the exchange a timing tool, not a cleansing event. For investors already carrying substantial prior depreciation, the strategic question is whether deferral still serves the long-term plan or simply postpones a concentrated unwind.

We can work through how recapture, unrecaptured §1250 gain, and capital gain may stack in the year you plan to sell.

Entity and Ownership Structure Decide Who Bears the Tax

Entity structure matters because tax consequences do not stop at the property level. Ownership determines who receives operating income, who gets suspended losses, whose hours matter for participation, where the §163(j) computation is made, and which taxpayer ultimately bears NIIT exposure on a sale. A structure that feels efficient while the property is being operated can become much less efficient when value is harvested.

This is especially important in partnerships and tiered holding structures. The IRS instructions for Form 8990 make clear that elections are made at the trade-or-business level and, for partnerships, on the partnership return with respect to partnership businesses. The same instructions also require allocation and apportionment between excepted and non-excepted trades or businesses when both exist. In practice, that means real estate groups with different asset types, leverage profiles, or owner roles should not assume that one election or one modeling result travels cleanly across the whole structure.

QBI should also be kept in its lane. The 20% QBI deduction is now permanent, but it is still limited to qualified business income, and the deduction is computed by reference to taxable income minus net capital gain. In practical terms, capital gain on exit is not where §199A usually saves the day. It is an operating-income tool, not a sale-gain solution.

We can help you review whether your current ownership and entity structure still supports the flexibility you want at refinance, retirement, or exit.

Cash Flow and Long-Term Tax Efficiency Are Not the Same

High-income investors often confuse two different victories: improving current-year cash flow and improving lifetime after-tax wealth. Bonus depreciation, cost segregation, debt, and deferral can produce immediate relief, but current-year relief is not the same as a better long-term result. A strategy that reduces this year’s federal payment can still worsen the eventual unwind if it narrows exit-year flexibility or shifts more income into ordinary or NIIT-sensitive buckets later.

That distinction becomes even sharper in 2026 because overall itemized deductions can again be reduced for taxpayers in the top bracket. For many HNW households, that means the marginal value of piling more property-tax or charitable deductions into an already crowded high-income year can be lower than expected. Federal timing and income character often matter more than simply generating another deductible item.

We generally find that the cleaner framework is asset-based rather than deduction-first. Decide which assets are meant to be held through retirement, which are likely to be exchanged, which should remain flexible for sale in lower-income years, and which may be natural candidates for lifetime transfer planning. Then match depreciation elections, leverage, ownership, and liquidity planning to those categories. The reverse approach often produces impressive deductions and weaker outcomes.

Retirement, Pension, and RMD Coordination

For many affluent Florida households, the sale year is not defined by the property alone. It is defined by what else is happening in the same household tax year. The IRS states that most taxpayers generally must begin required minimum distributions when they reach age 73, and once RMDs start, they consume bracket room that might otherwise absorb part of a real estate exit more efficiently. The same is true for pensions, deferred compensation, and business-sale income.

That is why retirement coordination belongs inside 2026 real estate tax planning. Selling before RMD years begin, after earned income declines, or in a year without a major liquidity event can materially change how ordinary recapture, unrecaptured §1250 gain, and NIIT stack. By contrast, forcing a sale into the same year as a major retirement-plan distribution can turn a manageable gain into an unnecessarily expensive one.

This is one of the clearest examples of multi-year planning beating one-year optimization. A property may look “ripe” for sale in isolation, but once retirement cash flow is layered in, the better move may be to wait, sell earlier, exchange, or stage liquidity differently. Real estate decisions age better when they are made against the household income calendar, not just the property pro forma.

We can help you map the next tax year around your real estate income, liquidity events, retirement timing, and planned dispositions.

Correcting Common Misuse and Oversights

The most common misuse in the 2026 market is treating powerful tools as default answers. Cost segregation is not automatically beneficial. A §1031 exchange is not automatically superior to a taxable sale. Real estate professional status does not automatically eliminate NIIT. And electing out of §163(j) is not automatically a low-cost fix for leverage. Each of those tools can be valuable, but each becomes less attractive when the hold period, participation facts, or exit-year income stack points in a different direction.

Another frequent oversight is ignoring history. Sale-year planning depends on prior depreciation method, cost segregation detail, grouping elections, passive-loss carryforwards, interest-limitation posture, and the way the asset was titled from the start. These are not details that can be reconstructed cleanly once a letter of intent is signed. When high earners feel that their planning is fragmented, this is usually why. The return may have been prepared correctly each year, but the asset was never managed as part of a coherent federal plan.

Restraint is sometimes the advanced move. If an asset is a likely short- to medium-term sale candidate, it may be better to preserve basis, preserve flexibility under §163(j), or preserve a cleaner participation story than to maximize every available current-year deduction. Sophisticated planning is not about using more strategies. It is about using fewer strategies in the right order.

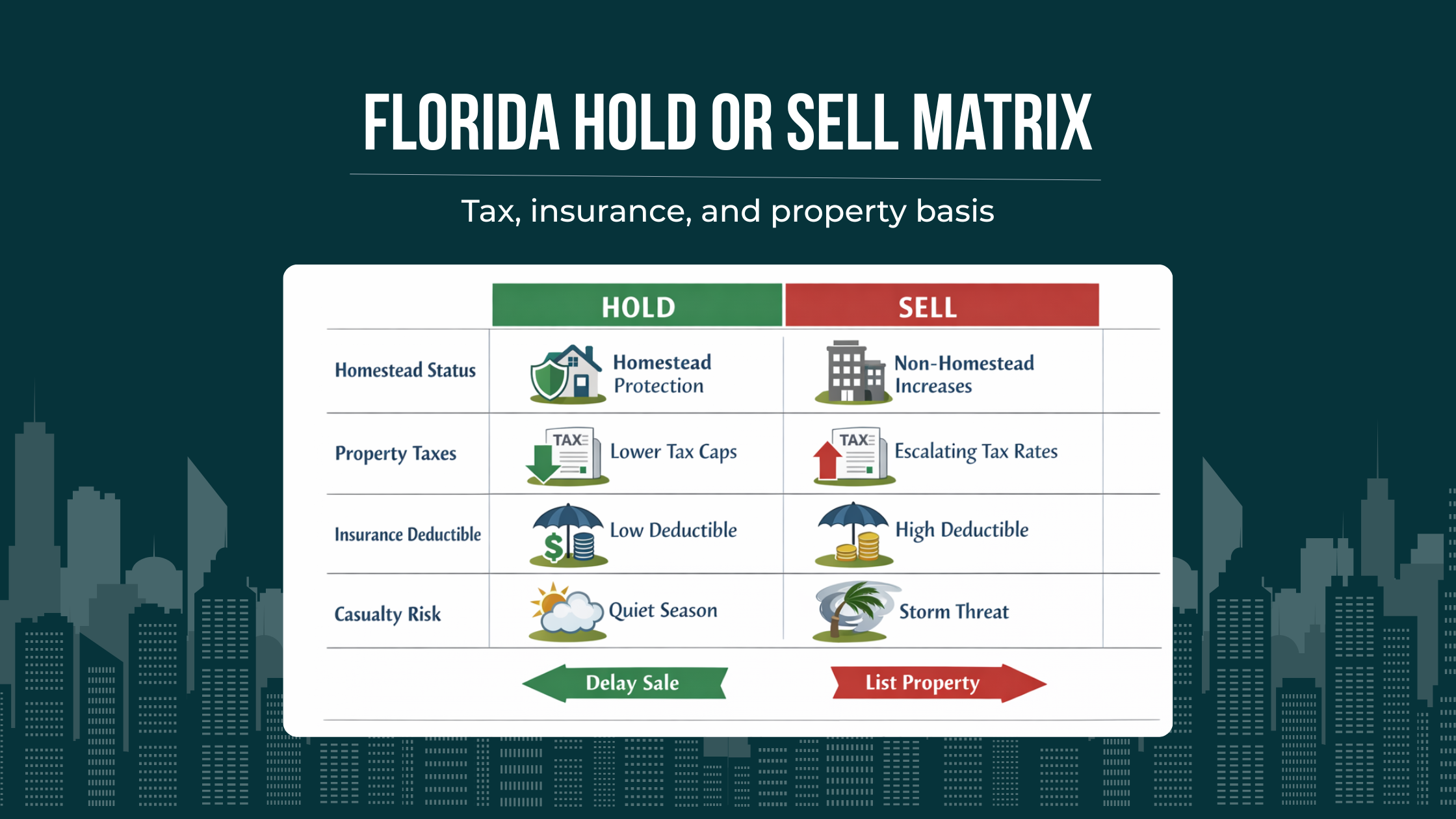

Florida-Specific Planning Considerations

Florida changes the analysis because there is no personal income tax to cushion a federal planning mistake. That shifts more attention to federal rate stacking, character, basis, and NIIT. For a high-income Florida real estate investor, the absence of state income tax does not make planning simpler. It makes federal planning more exposed.

Property-tax structure also changes hold and sell decisions. Florida’s homestead exemption can provide up to a $50,000 exemption, and Save Our Homes limits annual assessed-value increases on homestead property to the lesser of 3% or CPI. Portability can allow an eligible owner to transfer all or part of the Save Our Homes assessment difference to a new Florida homestead, lowering the assessed value of the replacement home. For an owner deciding whether to retain a low-assessed homestead, convert use, or sell and relocate, those rules affect the economic after-tax answer even though they are not income-tax rules.

Non-homestead property should be modeled differently. Florida’s property-tax system also reflects a 10% non-homestead assessment cap in the county tax base, which means local carrying costs on investment and second-home property can move differently from homesteaded property. For concentrated Florida owners, that makes property-tax drift part of the hold-period analysis, especially where one property has become unusually tax-efficient to retain relative to current market value.

In Florida, hold-period economics are shaped by more than federal tax rates because property-tax structure and storm-related risk can change the best exit year.

For concentrated Florida owners, these variables should be modeled alongside NIIT, recapture, and liquidity needs. A property that is efficient to hold may not be efficient to sell in the same year.

Insurance and casualty planning deserve more attention than they usually get. Florida insurers must offer hurricane deductible options of $500, 2%, 5%, or 10% of the dwelling or structure limits, subject to certain exceptions. When deductibles scale with insured value, the required cash reserve is part of the tax plan because storm timing can affect whether a loss is repaired, capitalized, reimbursed, or potentially deductible. Beginning in 2026, state-declared disaster losses can also matter for personal casualty-loss analysis, which makes contemporaneous records, basis support, and reimbursement tracking more important.

Florida’s short-term rental concentration adds one more planning wrinkle. Because these assets often sit near the boundary between rental and operating business treatment under the passive activity rules, owners should decide early whether the property is being run as a yield-producing rental, an operating business requiring material participation, or a future sale candidate whose disposition year needs NIIT protection. In many Florida portfolios, that classification choice becomes binding when the exit finally arrives.

Conclusion

The most important April 2026 real estate tax changes are not just the visible ones, like permanent 100% bonus depreciation or the updated 2026 brackets. The deeper change is that current law rewards sequencing. A strategy that looks efficient in the acquisition year can still be inefficient over the life of the asset if it ignores §163(j), NIIT, passive-loss release, recapture, retirement timing, or Florida-specific hold-cost realities.

For high-income Florida taxpayers, that points to a broader planning standard. Real estate tax planning should be coordinated across acquisition, operation, financing, liquidity, retirement, and exit. The goal is not the largest current-year deduction. The goal is a structure that still works when income rises, a storm hits, a refinance closes, an RMD begins, or a property finally sells. That is what makes 2026 real estate tax planning durable rather than merely active.

We can review whether your current real estate tax plan is coordinated across deductions, leverage, NIIT, and exit timing.

Frequently Asked Questions

How is Capital Gains Tax Calculated?

For a high-income real estate investor, the more useful question is usually not a single capital gains tax number. A sale can include ordinary recapture, unrecaptured §1250 gain, residual long-term capital gain, and NIIT, so the federal result depends on how those layers stack in the sale year. That is why basis, prior depreciation, hold period, and the broader household income cycle matter more than the headline capital gain rate alone.

Do I Have to Pay State Capital Gains Tax?

Florida does not impose a personal income tax, so there is generally no separate Florida individual capital gains tax. That does not make a Florida sale a low-tax event. In this planning framework, the economic weight shifts more heavily to federal timing, gain character, NIIT, property-tax structure, insurance costs, and hold-versus-sell decisions.

Is Rental Income Considered Active or Passive?

Usually, rental income is treated as passive, but the answer often turns on the type of activity rather than the amount of effort involved. The IRS rules carve out exceptions where an activity is not treated as a rental activity, including when average customer use is seven days or less, or thirty days or less with significant personal services. That matters in Florida because many short-term rentals sit close to that line. Once an activity falls outside the rental definition, material participation becomes more important, and that can affect both current-year loss treatment and sale-year NIIT posture.

Can Passive Losses Offset Capital Gains?

Usually not in the way investors hope. As a general rule, passive losses are limited to passive income and are carried forward when they cannot be used. Where this becomes more interesting is disposition planning: if you sell or exchange your entire interest in the activity in a fully taxable transaction to an unrelated party, previously disallowed passive losses are generally freed up. That means the better planning question is often not whether passive losses offset capital gains today, but whether the exit structure is the kind of transaction that actually releases suspended losses when you want them.

Is Cost Segregation Really Worth It?

Sometimes, but we would not treat it as a default answer. In the article’s framework, cost segregation is most valuable when the asset has durable ordinary income, a realistic hold period, and a clear exit plan. The more deductions you pull forward, the more carefully you need to model future recapture, unrecaptured §1250 gain, and whether the property is likely to be sold, refinanced, or exchanged sooner than expected.

Does cost segregation increase depreciation recapture?

It often increases recapture exposure because it accelerates deductions and can shift more depreciation into assets that are recovered faster and may be recaptured differently on sale. That does not mean the strategy fails. It means the benefit should be measured on a multi-year basis, not just by the first-year tax reduction. Once basis is reduced earlier, sale-year gain can rise, and more of that gain may fall into recapture-sensitive buckets. For HNW investors, the real question is whether the present-value benefit and reinvestment flexibility outweigh the future character cost in the likely exit year.

Does a 1031 Exchange Eliminate Deferred Gain?

No. A like-kind exchange may defer current gain if properly executed, but it does not erase it. The basis of the replacement property generally carries over with adjustments, which preserves deferred gain for later recognition. For investors already carrying substantial prior depreciation, the planning question is whether continued deferral still serves the long-term plan or simply postpones a more concentrated unwind.

Can I Avoid Paying Capital Gains Tax on Rental Properties?

Usually, the more accurate objective is defer or manage timing, not avoid. A like-kind exchange may defer current gain if properly executed, but it preserves deferred gain rather than erasing it. For high-income investors, the stronger planning question is whether the property should be sold, exchanged, or moved into a lower-income year so that recapture, unrecaptured §1250 gain, capital gain, and NIIT are handled more intentionally.