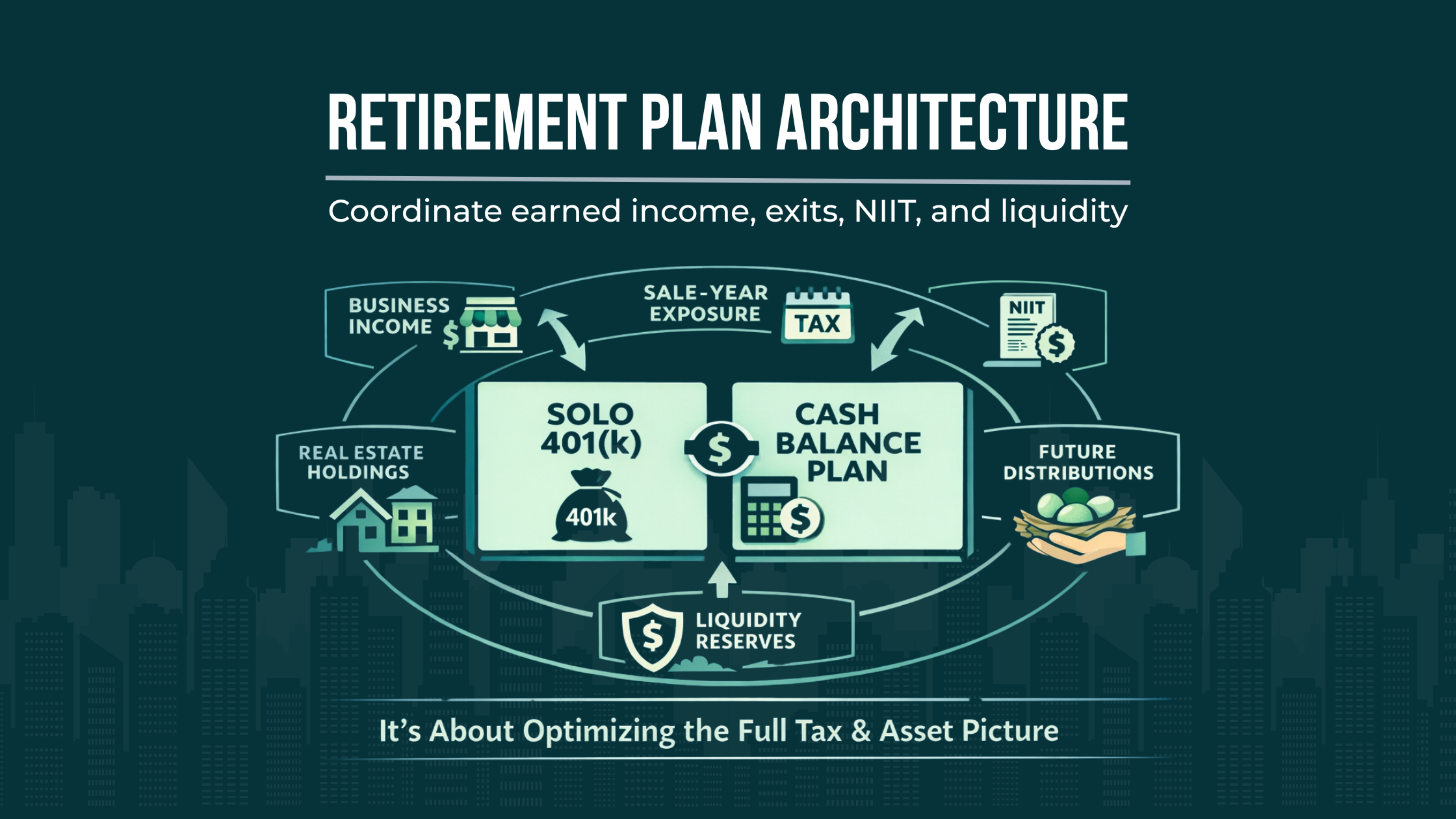

When Solo 401(k)s and Cash Balance Plans Work Together and When They Don’t

The right structure depends on how retirement-plan funding interacts with income character, asset concentration, and future exit years, not just this year’s deduction.

Introduction

For high-income Florida taxpayers, the real issue is not whether a solo 401(k) and cash balance plan can create a larger deduction. It is whether the pairing improves lifetime tax efficiency once we account for federal-only planning, real estate concentration, future sale years, and the cash demands of actually running a business or property portfolio. Florida does not impose a personal income tax, which makes federal planning carry even more weight.

That matters more in Florida than many advisors admit. For business owners, professionals, and real estate investors already paying six figures a year to the IRS, the solo 401(k) and cash balance plan decision is a sequencing decision. It affects how much ordinary income we shelter now, what remains exposed to NIIT, how much liquidity we preserve for properties and insurance shocks, and what later unwind or distribution years will look like.

We help evaluate whether solo 401(k) and cash balance plan contributions are improving multi-year outcomes or simply crowding deductions into the wrong years, especially when entity structure drives what compensation can actually support the plan.

Key Takeaways

The pairing works best when earned income is stable, plan funding can be sustained for several years, and large real estate exits are not about to compress recapture and NIIT into the same window.

It works less well when owners size contributions off a temporary spike while most future tax exposure sits in passive gains, depreciation recapture, or irregular sale activity.

NIIT is a separate layer. Qualified plan contributions may reduce taxable income, but they do not automatically solve NIIT on rents or sale-year gains.

Real estate investors should judge this strategy against exit-year tax character, not just hold-year deductions.

Entity design matters because appreciation, rental income, and capital gain do not always create the compensation needed to support retirement plan contributions.

The right answer is usually a coordinated multi-year design, not a one-year race to the largest deductible contribution.

We can map how current plan funding interacts with future sale years so depreciation recapture and unrecaptured §1250 gain do not get analyzed too late.

When a Solo 401(k) and Cash Balance Plan Work Well Together

The combination usually works well when a taxpayer has durable earned income from an owner-operated business, already uses the flexibility of a solo 401(k), and still has enough recurring cash flow to support a defined benefit-style commitment. In that setting, the two plans do different jobs. The solo 401(k) offers flexibility in annual contribution decisions, while the cash balance plan can create materially larger deductible contributions when the income base is both high and repeatable. A one-participant 401(k) is built for an owner-only business or the owner and spouse, and a cash balance plan is a defined benefit plan in which the employer bears the investment risk behind the promised benefit.

This is often effective for professionals and owner-operators whose active income drives most of the tax bill and whose real estate holdings are not likely to trigger a large taxable exit in the near term. The classic fit is the owner-only business, or owner plus spouse structure, with strong recurring profits and a clear willingness to fund for several years rather than treat the plan as a one-time move.

When the Combination Starts to Work Against You

The combination starts to work against you when the tax deduction is real but the cash flow is not durable. That happens in commission-heavy years, acquisition-heavy periods, or businesses whose income is elevated by a single transaction rather than a stable earning pattern. A cash balance plan is not built for casual on-again, off-again funding. Current IRS guidance on qualified defined benefit plans reflects that funding discipline through minimum funding rules and quarterly installment timing.

It can also backfire when a taxpayer is nearing an exit cycle. If future tax liability is likely to come from selling appreciated real estate, recognizing depreciation-driven gain, or realizing gains that may still be exposed to NIIT, then maximizing pretax retirement contributions today may solve the smaller problem and leave the larger one untouched.

Another failure mode is operational drift. A solo 401(k) works best when the business truly remains owner-only. Once common-law employees enter the picture, or related entities complicate coverage, the simplicity that made the structure attractive can fade quickly. IRS guidance is explicit that the no-testing advantage disappears when eligible employees must be included.

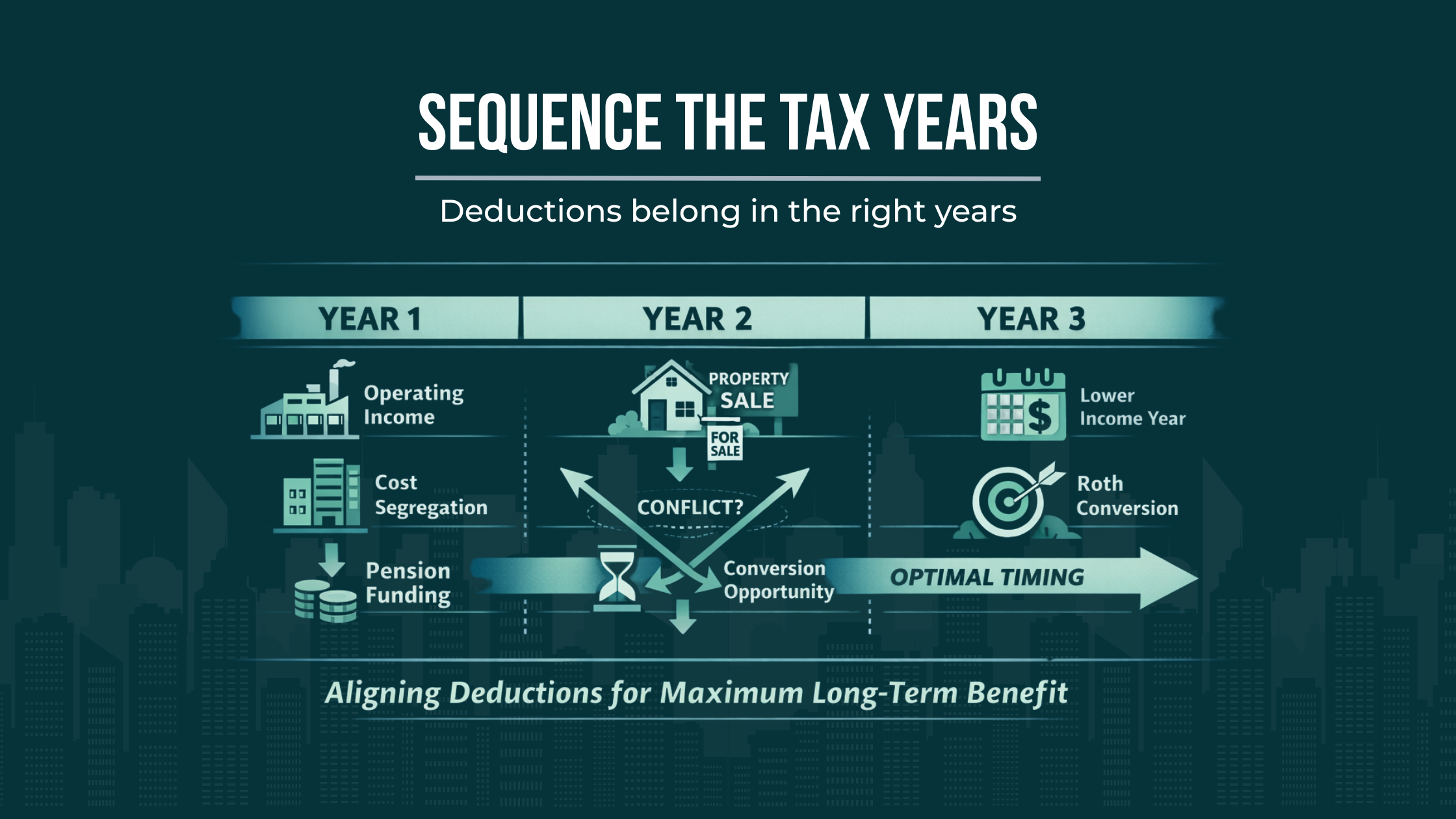

Income Stacking and Sequencing Across Tax Years

A sophisticated plan starts by asking which years deserve the deduction most. That is not always the current year. If we expect strong earned income now but a heavily taxed sale two years from now, we need to compare those years rather than maximize contributions in isolation.

Consider a three-year pattern. In Year 1, a Florida business owner has strong operating income and no major asset sales. In Year 2, several properties go through cost segregation and produce large deductions. In Year 3, a non-homestead rental or short-term rental portfolio is sold in a taxable transaction, bringing capital gain, prior depreciation consequences, and potentially NIIT into the same year. A large cash balance contribution in Year 1 may still be reasonable, but only if it does not reduce flexibility for Year 3 planning, future conversion windows, or liquidity needs around the exit.

A paired-plan strategy usually works best when we compare current deductions against future sale years, liquidity needs, and later conversion or distribution opportunities.

There is also a structural sequencing issue many high earners miss. The elective deferral limit for a 401(k) applies per person, not per plan. And if the owner has multiple businesses, only the earned income from the business sponsoring the plan is considered for that plan. For taxpayers with an operating company, a brokerage entity, and separate real estate partnerships, that detail becomes central.

A useful rule is this: use the cash balance plan to shelter recurring high-rate earned income, not irregular tax events you cannot reliably repeat. When we try to match a pension-style commitment to transaction-style income, the strategy usually becomes brittle.

NIIT Exposure and Why Classification Matters

For high-income taxpayers, NIIT is not a side issue. It is a second federal layer sitting on top of the income-tax analysis. If we ignore it, we can overstate the value of a retirement-plan strategy or misunderstand what part of a real estate exit is still exposed. The tax is 3.8%, and the statutory thresholds are not indexed for inflation.

NIIT MAGI THRESHOLDS

The Net Investment Income Tax applies once modified adjusted gross income exceeds the threshold for the applicable filing status.

| Filing Status | MAGI Threshold |

|---|---|

| Married filing jointly / qualifying surviving spouse | $250,000 |

| Single / head of household | $200,000 |

| Married filing separately | $125,000 |

NIIT applies to the lesser of net investment income or the excess of MAGI over the applicable threshold. For high-income real estate investors, that means rents, passive business income, and gains from property dispositions can create an additional federal layer even when ordinary-income planning has been handled well.

This is where the solo 401(k) and cash balance plan are often misunderstood. Qualified plan contributions may reduce current taxable income, but they do not automatically remove rents or sale gains from NIIT. Qualified retirement plan distributions themselves are generally not included in net investment income, but the contribution decision and the NIIT decision are still separate analyses.

Classification is where the planning gets real. Current IRS instructions make clear that qualifying as a real estate professional does not, by itself, remove rental income from NIIT. If the rental activity is not a section 162 trade or business, or if the taxpayer does not materially participate, the rental income remains included in NIIT. The same instructions also describe a safe harbor under which qualifying real estate professionals can treat rental income, and in the disposition year gain, as outside NII if the applicable participation standard is met.

Florida short-term rentals add another layer. Under the passive-activity rules, shorter stays with the right service profile may fall outside the default rental-activity bucket. In Florida, that same activity may also involve state sales tax and local transient rental taxes. The posture may look more operational than a conventional rental, but that does not make the retirement-plan answer automatically larger or cleaner.

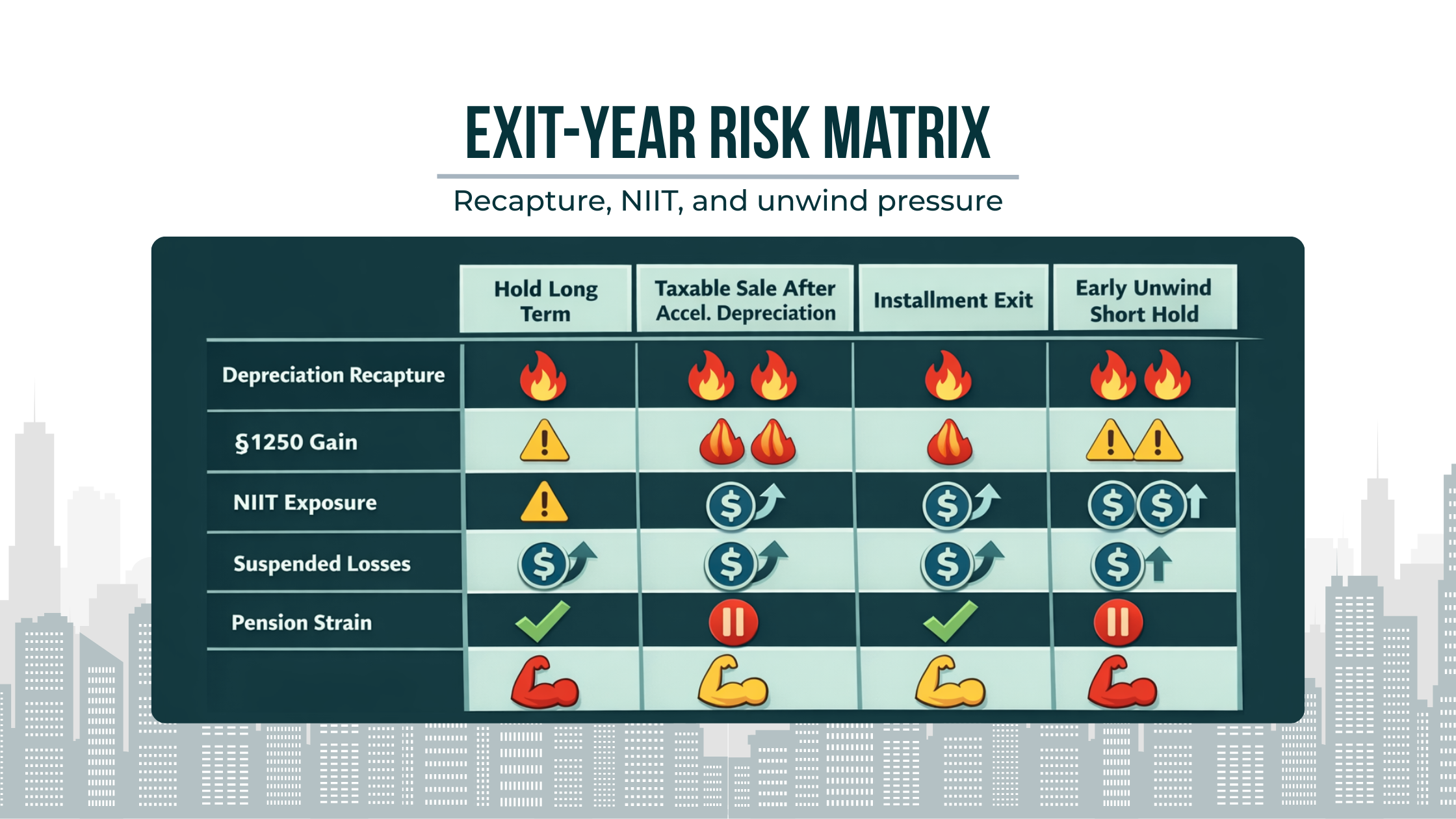

Real Estate Exit Planning: Depreciation Recapture, Unrecaptured §1250 Gain, and Unwind Scenarios

This is where many high-income plans break down. The hold years get most of the attention, while the sale year gets treated like a generic capital-gain event. For depreciated real estate, that is incomplete.

Prior depreciation changes the character of gain. The IRS distinguishes between ordinary recapture rules and unrecaptured section 1250 gain, and for many real estate investors the practical issue is that part of the gain attributable to prior depreciation is not simply taxed like the rest of a long-term capital gain. Unrecaptured section 1250 gain can be taxed at a maximum 25% rate, and the sale may also generate gain that is still subject to NIIT depending on the activity’s status.

The more aggressive the front-end depreciation strategy, the more important this becomes. Cost segregation and accelerated write-offs may be excellent tools during the hold period, but they do not erase the character problem later. They change the timing. If a property is sold in a taxable exit before the long-term plan has matured, those earlier deductions can reappear in a much less attractive mix of tax items.

The more aggressive the front-end deduction strategy, the more important it becomes to model how exit-year tax character and funding obligations may collide.

Unwind scenarios are where this becomes real. A taxpayer may expect a 10-year hold, steady plan funding, and a gradual retirement transition, then sell after three years because of a partnership dispute, insurance reset, casualty event, or refinancing issue. Now the cash balance plan is still demanding disciplined annual funding while the property sale pushes depreciation-driven gain into the current year.

Suspended passive losses can help, but they do not automatically solve the whole sale-year stack. If an entire passive interest is sold to an unrelated person in a fully taxable transaction, passive losses may be released. Even then, the NIIT analysis still requires a separate look at what portion of the gain and deductions remains inside net investment income.

Cost Segregation and Bonus Depreciation as Planning Tools, Not Tactics

Cost segregation is often presented as a stand-alone deduction strategy. For sophisticated taxpayers, that is too narrow. It is a timing decision, and timing decisions only make sense relative to future years.

When a property is likely to be held long enough, when active income is predictably high, and when cash balance funding can be supported without starving reserves, cost segregation can complement a solo 401(k) and cash balance plan. It can move deductions into years where they have high marginal value and reduce current tax drag while the asset is still early in its life cycle.

But the combination can also create deduction crowding. If the same year already contains large retirement-plan deductions, additional accelerated depreciation may not create proportional value. Bonus depreciation, when available under current law, should be judged the same way. It is a timing tool, not a permanent reason to accelerate everything at once. The right question is not whether more deductions are available, but whether they belong in the same year.

Entity and Ownership Structure Implications

Many articles reduce entity analysis to a quick sentence that “entity type matters.” For high-income taxpayers, that is not enough. The real issue is how compensation, gain, and plan eligibility actually move through the structure.

IRS guidance is clear that earned income for self-employed plan purposes does not include capital gains. Current Publication 560 also states that income passed through to S corporation shareholders is not net earnings from self-employment for this purpose, while a partnership generally makes contributions for partners based on net earned income and certain guaranteed payments for services can count. That means the entity producing appreciation or allocable gain is not always the entity producing retirement-plan contribution capacity.

This is a major issue for real estate investors. A successful sale inside a partnership may create significant wealth and large taxable gain, but that does not mean it creates the earned income needed to support larger plan contributions. The same problem appears when a property LLC generates appreciation while the operating entity is the only place with real plan compensation.

Multi-entity owners also need to watch silo assumptions. If only one business sponsors the plan, only the earned income from that business is considered for that plan. If the owner also participates in another 401(k), elective deferrals are still subject to one person-level limit. Fragmented advisor teams miss this all the time because the operating business, the real estate partnerships, and the retirement plan are being analyzed separately.

Active vs Passive Treatment and Why It Can Become Binding at Exit

Active versus passive treatment is often discussed as a loss-utilization issue. For high-income investors, it is more than that. It influences NIIT exposure, suspended-loss buildup, and what happens when a property or business interest is sold.

The passive-activity rules generally treat rental activity as passive unless a specific exception applies. Real estate professional status and material participation can change that result for income-tax purposes, but those same facts also matter later when we ask whether rent or gain remains inside NIIT. Current IRS instructions explicitly warn that real estate professional status alone does not automatically remove rental income from NIIT.

The exit year is where this becomes binding. A taxpayer who has treated an activity as passive for years may finally dispose of it and release suspended losses. That can be valuable. But if the gain from disposition is still included in net investment income, the federal stack may still be heavier than expected.

Florida short-term rentals add another layer because average stay length and service level can move an activity out of the default rental box under the passive-activity rules. That may help annual loss treatment, but it can also create payroll, sales-tax, and operating-complexity consequences. The right classification is the one that fits the facts and improves the full multi-year outcome.

Cash Flow vs Long-Term Tax Efficiency

The cash balance plan often looks strongest on paper right before it becomes hardest to fund in real life. That is why we do not treat maximum deductible contribution as the target. We treat durable after-reserve cash flow as the target.

Unlike a solo 401(k), a cash balance plan is a defined benefit plan. The employer bears the investment risk behind the promised benefit, and minimum funding standards generally require disciplined contribution timing. For a Florida owner with real estate, that means the plan has to coexist with debt service, insurance renewals, capital expenditures, vacancy cycles, and operating reserves.

This matters more in Florida because property risk is not just an abstract market variable. Florida consumer guidance makes clear that hurricane deductibles are often stated as a percentage of insured dwelling or structure limits, and policies commonly carry larger hurricane deductibles than other-loss deductibles. A tax-efficient contribution can still be economically mistimed if it leaves no room for a bad season.

Retirement, Pension, and RMD Coordination

Current deductions are only half the analysis. The other half is how and when the money comes back out.

Traditional solo 401(k) and cash balance plan dollars generally become ordinary income when distributed. Required minimum distributions generally begin at age 73 for retirement plans, and defined benefit plans have their own RMD mechanics. Qualified plan distributions are generally excluded from NIIT, which helps, but that does not mean the distribution years are tax-light. Large pretax balances can still compress future ordinary-income planning.

This is especially relevant for the owner who expects a business sale, portfolio simplification, or partial retirement in the early 60s. If the taxpayer keeps maximizing pretax funding without modeling the post-exit years, they may miss the real opportunity: lower-income years between active business life and RMD age. Those years may be better used for conversions, controlled withdrawals, or other bracket management rather than for adding still more pretax concentration.

There is also an unwind issue many promotional pieces skip. A cash balance plan is not meant to run forever just because it worked well for a period of peak earnings. If income drops, the business is sold, or the owner retires, the plan may be terminated and benefits distributed. Department of Labor guidance notes that lump sums from cash balance plans are generally eligible for rollover to an IRA or another employer plan if accepted.

Asset-Based Planning vs Deduction-First Planning

Deduction-first planning asks how much income we can reduce this year. Asset-based planning asks where the future tax character lives.

For a high-net-worth Florida taxpayer, that usually means separating active earned income from investment income, appreciating real estate, short-term rental operations, business equity, and future liquidity events. Once we do that, the role of the solo 401(k) and cash balance plan becomes clearer. These plans are strongest where the client has repeatable high-rate earned income. They are weaker as a universal answer to tax liability that is really being created by appreciated assets, passive gain, or future recapture.

This is why the best retirement-plan work is often not retirement-plan-centric. It starts with asset location, holding period, participation facts, ownership design, exit timing, and cash reserve policy. Only then do we decide whether the retirement-plan layer should be modest, aggressive, temporary, or scaled back.

Correcting Common Misuse and Oversights

A few errors show up repeatedly with high earners.

Treating a cash balance plan like a larger SEP.

Assuming a profitable property sale automatically increases retirement-plan contribution room.

Using cost segregation without a sale-year model.

Assuming real estate professional status automatically solves NIIT.

Ignoring person-level and entity-level coordination.

Funding to the maximum actuarial number without testing liquidity against reserves, insurance deductibles, and likely exit timing.

Those are not stylistic objections. They reflect how the current rules actually work across defined benefit funding, plan compensation, NIIT, and sale-year real estate taxation.

The corrective principle is simple. We should use the solo 401(k) and cash balance plan where they solve a repeatable earned-income problem. We should be more restrained when the client’s real tax problem is an asset transition problem.

We review whether the pairing still works once passive vs active treatment, NIIT exposure, and uneven cash flow are modeled across multiple years.

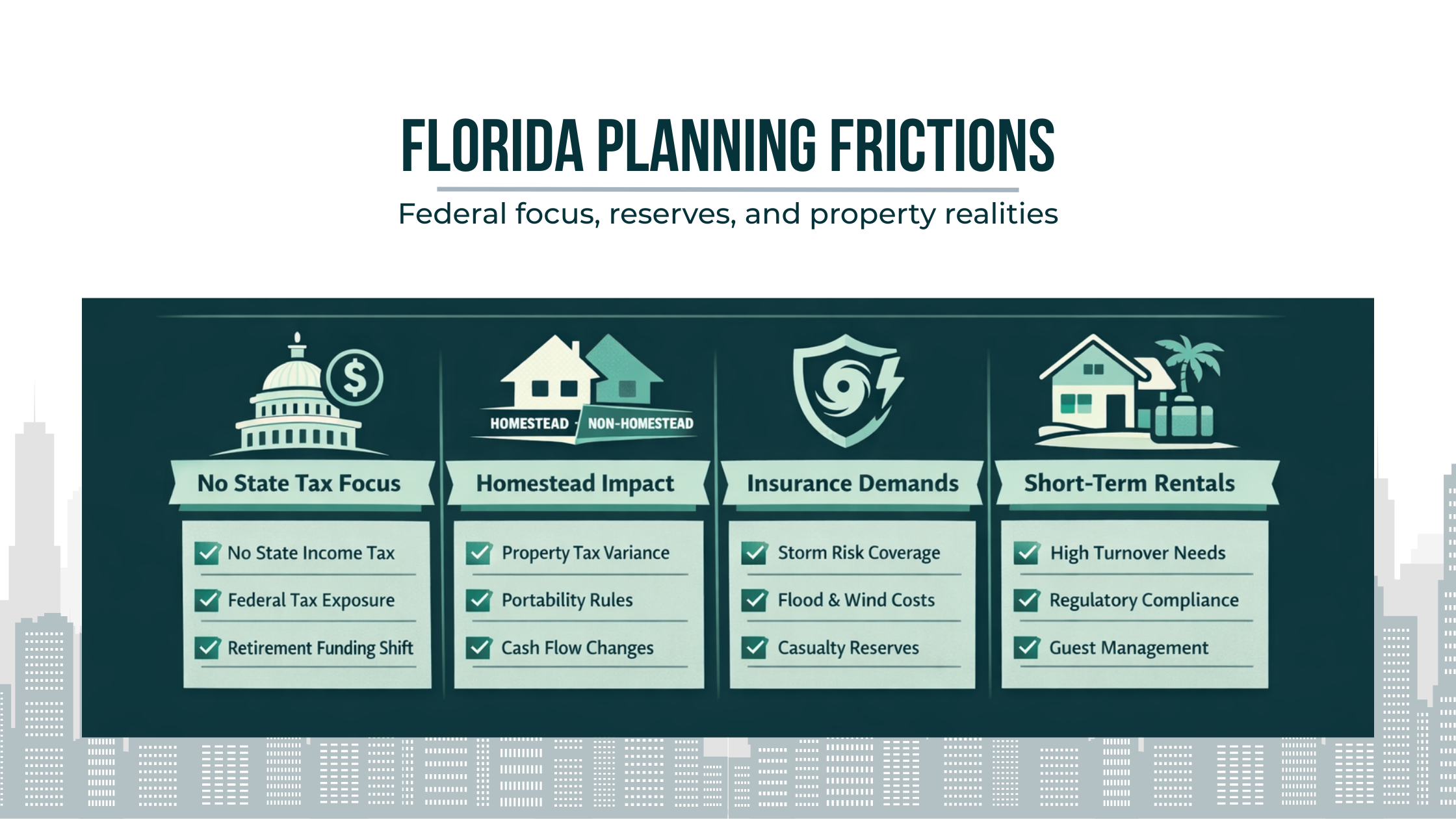

Florida-Specific Planning Considerations

Florida changes the analysis because there is no personal income tax to soften or complicate the retirement-plan decision. That makes federal planning more important, but it also makes it easier to overfocus on the current federal deduction. When state tax is not part of the equation, we need to be even more disciplined about which future federal years will carry the real burden.

In Florida, the absence of state income tax makes federal planning more important, but property tax structure, insurance volatility, and rental operations still shape how much funding is prudent.

Florida also has a heavier concentration of real estate ownership and short-term rental activity than many markets. For transient rentals of six months or less, Florida imposes state sales tax and counties may impose local transient rental taxes. That operational reality pushes many investors toward more active management systems and cleaner entity design, but it also means short-term rental planning often sits at the intersection of income-tax, sales-tax, and operating-business questions rather than inside a simple rental-property box.

Property-tax structure matters too. Florida’s homestead exemption and Save Our Homes rules can limit annual assessment growth on a homestead, while non-homestead property is subject to a different assessment-cap framework. A sale, ownership change, or shift in use can reset how the property behaves from a cash-flow standpoint. That does not decide whether to use a cash balance plan, but it can change how much funding is prudent.

Insurance and casualty exposure are also planning variables, not just operating annoyances. Florida guidance highlights the prevalence of percentage-based hurricane deductibles and larger hurricane-specific deductibles. For owners of coastal or storm-exposed property, that increases the need for reserves. In a world like that, an aggressive cash balance contribution can be technically deductible and still economically mistimed.

We look at real estate exits in context so retirement-plan decisions are coordinated with recapture, gain character, and the years surrounding a sale.

Conclusion

A solo 401(k) and cash balance plan can work very well together. But they work well for the right reason: they coordinate around durable earned income, not because they create the largest possible deduction in a single year.

For high-income Florida taxpayers, the decision should be made in the context of income stacking, NIIT exposure, real estate exits, depreciation history, entity design, liquidity, and future distribution years. That is what turns a retirement-plan decision into real multi-year tax planning. The goal is not to collect deductions. The goal is to build a system that remains efficient when the hold years end, the sale years arrive, and the planning horizon gets longer than the current return.

We can evaluate whether your current retirement-plan strategy still makes sense once entity ownership, NIIT layering, and future distribution years are viewed as one system.

Frequently Asked Questions

Can I Have a Cash Balance Plan and a 401(k)?

Yes, but the better question is whether both plans belong in the same planning window. A solo 401(k) is flexible; a cash balance plan is a defined benefit arrangement with funding discipline and employer investment risk. For sophisticated owners, the real issue is sequencing. If a year already includes large depreciation deductions, unusually low income, or a pending real estate sale, fully maximizing both plans may crowd deductions into a year that is not actually your most valuable planning year. We usually evaluate the pair against the next several tax years, not just the current return.

Why does Florida’s no-state-income-tax environment make this decision more important?

In Florida, the absence of personal income tax means the deduction decision is judged almost entirely by its federal effect. That makes sequencing more important, because the same contribution may carry more value in a year driven by active business income than in a year dominated by sale proceeds, NIIT exposure, or depreciation-driven gain. Florida also adds operating pressures that affect how much funding is prudent, including non-homestead carrying costs, storm-related reserves, and short-term rental complexity. The planning question is not just how much we can deduct, but which years deserve the deduction most.

How Long Do You Have to Fund a Cash Balance Plan?

There is no simple “one good year” rule. IRS guidance says retirement plans should be established with the intention of continuing indefinitely, even though a plan may later be terminated when it no longer suits the business. That means we should design the plan with a multi-year path in mind from the start. For an owner expecting retirement, a business sale, or a reduction in active income, the funding horizon matters because it affects how much liquidity we preserve, how aggressively we contribute early, and how we coordinate the eventual unwind with later tax years.

Can I Use Rental Income for a Solo 401(k)?

Often, no. A solo 401(k) generally needs earned income or net earnings from self-employment, while conventional rental activity is often passive and not compensation for retirement-plan purposes. The answer can change when the activity functions more like an operating business, including some short-term rental fact patterns where average customer use is very short or significant services are provided. In Florida, that same short-term rental activity may also trigger state sales tax and local transient rental taxes on stays of six months or less, which is one reason we analyze the operating facts and entity structure together instead of assuming every rental dollar supports plan contributions.

Do Cash Balance Plans Work for S-Corps?

They can, but the contribution capacity has to come from the right type of income. IRS guidance is explicit that S corporation distributions are not earned income for retirement-plan purposes. Salary deferrals and employer contributions are based on Form W-2 compensation, not shareholder distributions. That distinction matters for high-net-worth owners whose wealth is being created by partnership gains, rental appreciation, or distributions from multiple entities. A profitable exit can increase liquidity without increasing retirement-plan room. That is why we usually map compensation-producing entities separately from gain-producing entities before layering a cash balance plan on top of a solo 401(k).

What happens to a cash balance plan when you retire?

A cash balance benefit is generally available as a life annuity, and many plans also allow a lump-sum distribution that can usually be rolled into an IRA or another employer plan that accepts rollovers. For high-income owners, the key issue is not portability alone. It is distribution-stage tax design. Large pretax balances can shift ordinary income into later years, and required minimum distribution rules eventually come into play. That is why we usually compare the retirement date, the years immediately after a business wind-down, and the first RMD years as one sequence rather than treating the contribution years as a stand-alone win.

When can you terminate a cash balance plan?

A plan can be terminated when it no longer fits the business, but the process is not casual. IRS guidance says the plan must be updated for legal changes, contributions must cease, affected participants must become fully vested, notices must be provided, outstanding required employer contributions must be paid, and benefits must be distributed as soon as administratively feasible. For real estate-heavy owners, termination also needs to be coordinated with the tax character of the surrounding years. Ending the plan does not eliminate depreciation-driven gain, unrecaptured §1250 gain, or any NIIT exposure that may still apply to a sale.