Short-Term Rental Tax Florida Orlando: An Investor-Focused Guide

This framework reinforces that the property should be planned as part of a broader tax and balance-sheet system rather than as a stand-alone deduction strategy.

For high-income investors, short-term rental tax Florida Orlando planning is rarely about finding one more deduction. The harder question is how an Orlando short-term rental fits into the rest of the household tax picture: business income, portfolio income, retirement timing, refinancing, and eventual sale. Florida’s lack of personal income tax often makes the market look simpler than it is, but that usually means federal classification, NIIT exposure, depreciation timing, and exit mechanics carry more weight, not less. Florida’s state sales tax applies to transient accommodations, Orange County imposes its own tourist development tax, and Orlando’s local rules add another operating layer, but those are only the front end of the tax conversation.

What tends to separate good from costly planning is whether we treat the property as a one-year tax project or as a multi-year asset with changing consequences. The federal rules still turn on activity classification, passive loss limitations, depreciation, gain character, and NIIT. Current IRS guidance continues to recognize that some short-term rentals fall outside the tax definition of a rental activity when the average period of customer use is 7 days or less, or 30 days or less with significant personal services, but that does not end the analysis. Material participation, ownership design, and recordkeeping still determine whether the hoped-for treatment holds up.

For Orlando investors, the planning burden is even more practical than theoretical. Florida lodging taxes and local compliance requirements affect operating systems and guest billing. Insurance, reserves, and carrying costs affect whether a property should be held long enough for an aggressive depreciation strategy to make sense. And if the household is already above NIIT thresholds, a strong operating year can still produce an inefficient after-tax result if the property remains passive and the sale year is crowded by other gains. The best strategy is not deduction-first. It is sequence-first.

Key Takeaways

The central tax question is still classification: whether the activity is passive, nonpassive, or treated more like an investment activity during different phases of the hold. IRS rules on average customer use and significant personal services continue to matter because they determine whether the activity is even treated as a rental activity for passive-loss purposes.

For affluent households, NIIT is often as important as the ordinary income result. The current federal NIIT remains 3.8%, and it applies to the lesser of net investment income or the excess of MAGI over the statutory threshold amounts.

Cost segregation can still be useful, but its value depends on whether current deductions offset the right type of income and whether the likely hold period is long enough to justify the back-end consequences tied to depreciation. IRS guidance still treats depreciation as a core part of rental reporting and sale-year gain analysis.

Exit planning should begin before stabilization. Unrecaptured §1250 gain, section 1231 treatment, suspended passive losses, and sale-year NIIT exposure can all change the result more than the original purchase structure did.

Entity and ownership structure are not side issues. They affect who materially participates, who gets loss benefit, how flexible the economics are, and how easy it is to execute a refinance, partial sale, or family transition later.

Florida’s no-state-income-tax environment increases the importance of federal design rather than reducing it. At the operating level, Florida sales tax, any applicable discretionary surtax, and Orange County tourist development tax still affect systems, reserves, and net yield.

The best long-term outcomes usually come from matching tax elections and depreciation timing to a realistic hold period, reserve policy, and exit path, not from chasing the biggest first-year write-off.

We can help map passive vs active treatment, entity structure, and likely exit timing into one planning framework before the operating years lock in the result.

Why short-term rental tax planning in Florida is different

Florida invites a common oversimplification. Because there is no Florida personal income tax, owners often assume the tax side of an Orlando short-term rental is easier than in other states. At the state income-tax level, that is true. At the federal planning level, it often means the opposite. There is less room to offset a poorly timed federal result with state-level planning, so classification, gain timing, and NIIT exposure carry more of the burden.

The operating environment is also distinctly Florida-specific. The Florida Department of Revenue imposes 6% state sales tax on transient accommodations, plus any applicable discretionary surtax, and Orange County currently imposes a 6% tourist development tax on short-term lodging. Those amounts are guest-borne consumption taxes rather than income tax, but they still influence pricing, cash handling, filing discipline, and the practical decision of whether to self-manage or outsource.

Florida also changes the carry-cost discussion. In Orlando, investor underwriting cannot stop at nightly rates and occupancy. Insurance pricing, reserve requirements, storm exposure, and property-tax treatment change hold-versus-sell math. A tax strategy that assumes a long hold may weaken quickly if operating friction pushes the owner toward an earlier sale than expected.

That matters because federal real-estate planning tends to reward consistency and punish reversals. The sooner a property is sold after aggressive depreciation, the more likely the investor feels the back-end friction from basis reduction and gain character. In other words, Florida-specific operating volatility makes federal sequencing more important.

Start with classification, not deductions

A sophisticated short-term rental tax Florida Orlando strategy begins with classification. Rental real estate is generally passive, but the passive-activity rules make exceptions. Under current IRS guidance, an activity is not treated as a rental activity for these purposes if the average period of customer use is 7 days or less, or 30 days or less when significant personal services are provided. That rule still opens planning flexibility for some short-term rentals, but it does not automatically convert the property into useful nonpassive tax treatment. Material participation remains the next gate.

That distinction matters because many owners confuse “short stays” with “nonpassive losses.” The first is an operating fact. The second is a tax conclusion that depends on who participated, how much, and through what ownership structure. In a married household, for example, the records need to support the participation position actually being claimed. In a multi-owner deal, the owner who wants nonpassive treatment cannot assume the group’s overall activity level solves the issue.

The classification question also affects the quality of future income. If the property stays passive, the owner may preserve flexibility and still use suspended passive losses later, but the operating-year income may remain within NIIT. If the property is structured and operated in a way that supports nonpassive treatment, that may improve current-year loss or surtax outcomes, but it can require more personal involvement and more disciplined substantiation.

There is also an unwind risk here. Owners sometimes begin with a high-participation model, then hand off operations to managers once the property stabilizes. When that happens, the tax character can change midstream. A strategy that worked in the acquisition year may stop working in later years, and the return positions should reflect that reality rather than continue on autopilot.

Income stacking and sequencing across tax years

A short-term rental should be modeled across at least three windows: acquisition year, stabilized operating years, and exit year. The acquisition year is where basis allocation, placed-in-service timing, furniture and fixture spend, and any accelerated depreciation strategy usually matter most. The stabilized years are where classification, cash flow, and NIIT become more important. The exit year is where section 1231 treatment, unrecaptured §1250 gain, passive-loss release, and overall return stacking can dominate the final result.

This is why a deduction that looks attractive in isolation can be weak in context. A large first-year depreciation benefit is worth less when it shelters low-value income or produces little usable benefit because the loss is trapped. The same deduction can be highly valuable when it offsets a peak earnings year and the likely sale is far enough away that the owner can compound the cash-flow benefit before confronting the exit.

The timeline helps readers see that the right move in Year 1 depends on what is likely to happen in the operating years and at exit.

A second-order issue is transaction crowding. Suppose the household expects a business sale, partnership redemption, or concentrated-stock diversification in the next few years. In that case, the timing of an Orlando short-term rental sale should be coordinated with those events. The property might still be worth owning, but sale-year stacking can turn an acceptable tax result into an expensive one if multiple appreciated assets mature together.

Sequencing also matters inside the hold period. Owners often ask whether to front-load renovations, furniture, and systems in Year 1 or phase them over time. The answer depends on when the household can actually use deductions, how soon the property is expected to stabilize, and whether there is a realistic chance the asset will be refinanced, repurposed, or sold before the early-year tax benefit has meaningfully compounded.

One common failure mode is planning as though the hold period were fixed. In Florida, hold periods are often revised by forces outside the tax return: insurance repricing, storm events, HOA pressure, local rule changes, or opportunity cost relative to other properties. A resilient tax plan therefore assumes the property could be sold earlier than hoped and asks whether the current strategy still makes sense under that shorter timeline.

We can evaluate how acquisition-year deductions, NIIT exposure, and sale-year recapture interact so the property’s sequencing works across more than one tax year.

NIIT exposure is not a side issue

For affluent investors, NIIT is a design constraint, not a footnote. Current IRS guidance states that the NIIT is 3.8% and applies to the lesser of net investment income or the excess of modified adjusted gross income over the statutory threshold amounts: $250,000 for married filing jointly or qualifying surviving spouse, $125,000 for married filing separately, and $200,000 for single or head of household. Rental income and gain can fall within NIIT depending on the facts, especially when the activity is passive.

NIIT Threshold by Filing Status

For most high-income readers, the threshold itself is not the strategic question because the household is already above it. The real question is whether the STR’s operating income, rental gain, or both are likely to be included in net investment income. A property that remains passive can impose NIIT drag during the hold and again at sale. A property that is supportably nonpassive may reduce that drag in the operating years, but the analysis still has to be revisited when the asset is refinanced, repurposed, or sold.

NIIT also interacts with timing. An owner may see a stable property as a “cash-flow asset” and underestimate how much surtax friction has accumulated over time. On paper, the property may have delivered solid pretax returns. After NIIT, the spread versus other deployment options can narrow quickly, particularly when the household already has dividend, interest, or capital-gain income.

Another issue is that NIIT analysis can change without the property changing very much. A reduction in owner participation, a management shift, or a change in grouping assumptions elsewhere in the portfolio can affect the character of the activity. That means NIIT should be revisited when operations change, not just when the property is sold.

There is also a portfolio-level trade-off. Some investors benefit more from using the STR as a genuinely active operating asset for a period of time, while others are better served treating it as a passive, cash-yielding holding and planning around sale timing and passive-loss release. The best answer depends on how the property fits the rest of the return, not on a generic preference for active treatment.

Finally, NIIT matters in deal comparison. Two Orlando properties with similar pretax yield can produce materially different after-tax outcomes if one is manager-heavy and passive while the other is owner-intensive and supportably nonpassive. For higher-income households, that difference can be more important than a small difference in cap rate.

Active vs passive treatment becomes binding at exit

Classification choices that seem manageable during operations become binding when the property is sold. If the activity has been passive, suspended passive losses may become valuable, but only if the ownership, activity tracking, and disposition structure line up correctly. If the investor assumed losses would eventually free up without maintaining clean activity records, the sale year can expose years of avoidable sloppiness.

This is one reason we do not treat passive-versus-nonpassive status as an abstract label. It determines how operating losses behave, whether income is more likely to sit within NIIT, and whether sale-year cleanup is elegant or messy. The sale is often the first time the owner feels the full cost of poor categorization.

There is also a sequencing issue between the property and the rest of the portfolio. A passive asset sold in a year with other passive income may behave differently from one sold in a year dominated by active business income and capital gains. The property does not exit in a vacuum. It exits into a return already shaped by the rest of the household’s calendar.

A further failure mode arises when owners partially change use before sale. Moving from high-touch STR operations to a more passive manager-led model may alter the practical narrative behind prior-year positions. That does not necessarily invalidate earlier treatment, but it makes continuity and documentation even more important.

Entity and ownership structure shape flexibility

Entity selection in an Orlando short-term rental is not mainly a branding or checklist exercise. It is a flexibility decision. Ownership design affects who reports the income, who must materially participate to support nonpassive treatment, how easy it is to admit a co-investor, whether economics can be allocated with nuance, and how much friction appears when the property is refinanced or sold.

A disregarded entity can be clean and practical when a single owner wants straightforward reporting and direct control over participation. But simplicity is not always strategic. Once spouses, trusts, family members, or capital partners enter the picture, the wrong structure can make participation harder to document and future transactions harder to execute.

Partnership-type structures can create operational and economic flexibility, particularly when multiple owners contribute differently. That flexibility can be valuable when one owner drives operations, another contributes capital, and the long-term plan includes transfers, redemptions, or selective liquidity. But the same flexibility can become complexity if the operating agreement does not reflect how the property will actually be run.

The important tax point is that material participation is determined at the owner level, not by calling the entity “active.” If the ownership group expects one individual’s work to produce a nonpassive result, the structure and the records need to match that expectation. Otherwise, the property may economically feel active while the tax treatment remains passive.

There is also an exit-angle trade-off. Some structures are easy on day one but cumbersome when the family later wants to shift economics, add estate-planning features, or sell less than the full interest. Others take more care up front but preserve choices later. Investors should decide early whether this asset is meant to stay tightly held, admit family capital, or remain sale-ready.

A final second-order issue is management substitution. If a structure depends on one person’s participation to support the intended tax character, that may work only while that person remains willing and able to do the work. A durable plan should not assume the same labor pattern will continue unchanged for the full hold period.

Cost segregation should serve the plan

Cost segregation remains one of the most discussed short-term rental tax tools because it can accelerate depreciation into earlier years. IRS guidance still places depreciation at the center of rental reporting, and sale-year guidance still makes clear that depreciation affects later gain character. The planning question, though, is not whether accelerated depreciation exists. It is whether using it now improves after-tax wealth across the full hold period.

For some owners, the answer is yes. A newly acquired Orlando STR purchased into a peak-income year, with a realistic multi-year hold and a supportable participation position, can make good use of acceleration. For others, cost segregation mainly creates front-loaded tax relief followed by earlier basis reduction, more sale-year complexity, and pressure to hold longer than the operating economics justify.

A good framework asks four questions. First, what type of income are the deductions expected to offset? Second, is the property likely to remain in the same classification posture for several years? Third, what is the realistic hold period once insurance, reserves, and local operating friction are considered? Fourth, what does the sale look like after prior depreciation is taken into account?

Cost segregation also has an execution risk that advanced readers should not ignore. The technique may be technically sound and still be strategically weak if it pushes the investor into defending a long hold that no longer makes economic sense. Tax planning should support portfolio management, not trap it.

There is a related cash-flow trade-off. Front-loaded depreciation can improve current liquidity and reduce estimated-tax pressure, but it does not itself improve occupancy, insurance economics, or reserve adequacy. In a Florida asset, that distinction matters. A property with fragile operating resilience should not be “saved” by tax acceleration alone.

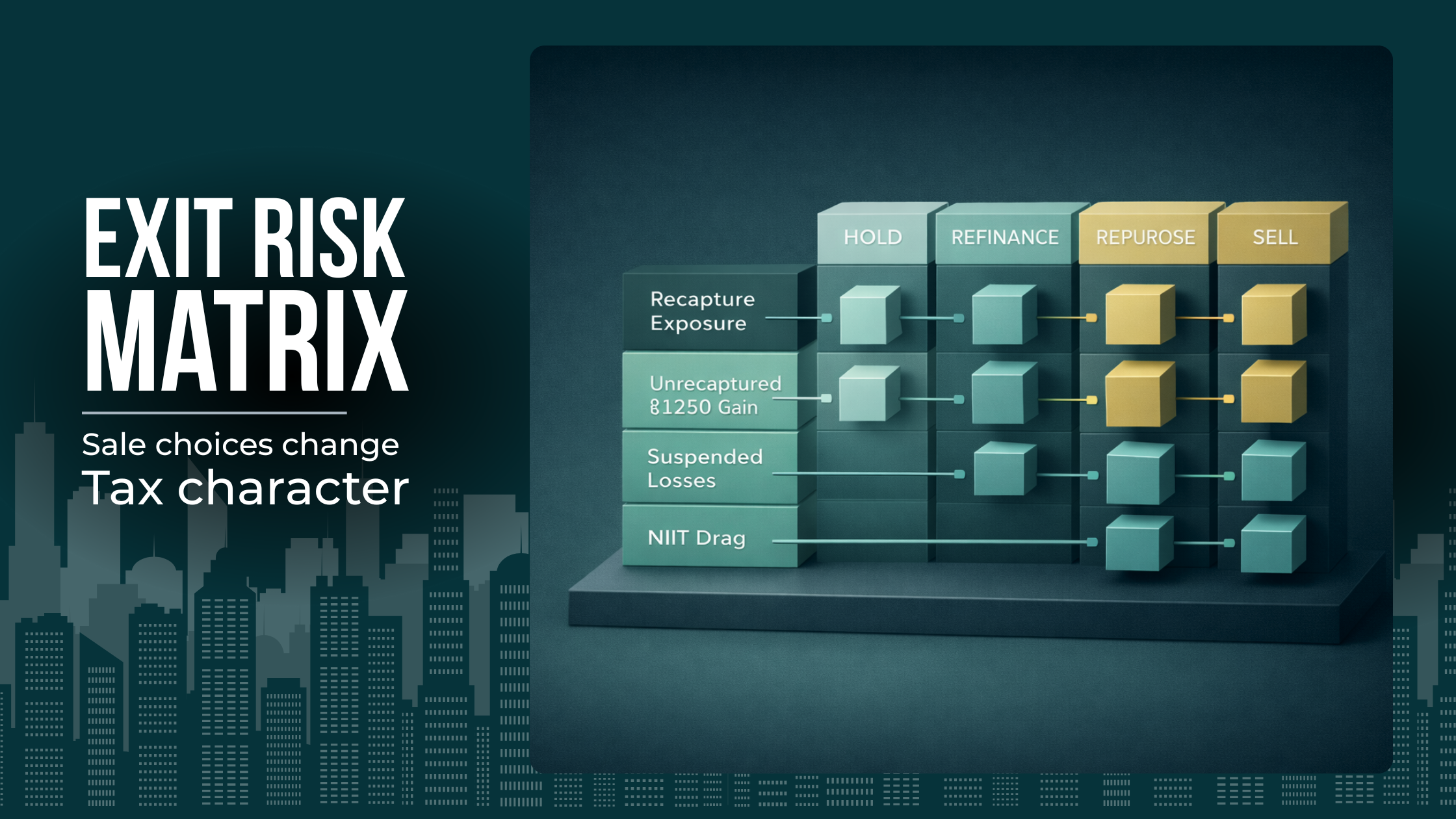

Exit planning: recapture, unrecaptured §1250 gain, and unwind scenarios

Exit planning is where many profitable STR stories become less impressive on an after-tax basis. Current IRS guidance continues to treat unrecaptured §1250 gain as the part of long-term capital gain on section 1250 real property attributable to depreciation, subject to its own rules and limits, and Form 4797 mechanics still control how real-estate dispositions flow through the return.

That means the gain on sale is not one clean bucket. Depending on the facts, part of the result may be ordinary in character, part may be unrecaptured §1250 gain, and the remainder may be long-term capital gain. For affluent households, this layered treatment matters because the sale rarely occurs in an otherwise empty year. The property’s gain gets stacked on top of everything else already happening.

This matrix makes the sale-year problem easier to evaluate by showing how different unwind paths affect tax character and after-tax flexibility.

The practical mistake is to celebrate early depreciation without pricing the later unwind. A strong Year 1 tax result can still be worth taking, but only when the owner has modeled what happens if the property is sold sooner than expected, converted to another use, or packaged into a larger reallocation of capital.

Unwind scenarios deserve more attention than they usually get. An owner may convert a former STR to long-term leasing because operations become too management-heavy. Another owner may increase personal use before sale. Another may stop participating materially and outsource everything. Each shift can change the tax story, and not always in a favorable direction.

There is also a holding-period discipline issue. Investors sometimes keep a property longer than they should because the anticipated sale tax feels unpleasant after prior depreciation. That is understandable but not always rational. The right question is whether continuing to hold still outperforms redeploying capital after factoring in the real tax cost of exit.

A second-order planning move is to begin sale-year cleanup well before listing. That can include reviewing suspended passive losses, confirming depreciation records, checking whether ownership changes are still advisable, and deciding whether the property should exit in the same year as other major liquidity events. By the time the contract is signed, many of the best tax decisions are already constrained.

Cash flow versus long-term tax efficiency

Some of the most popular tax ideas improve the return on paper while weakening the investment. That usually happens when tax optimization gets separated from operating resilience. A Florida STR can show attractive after-tax income in a projection while still being overly exposed to insurance repricing, reserve stress, seasonality, or management fatigue.

This is why we compare tax efficiency with cash-flow durability. A deduction has more value when it supports a property the investor would want to own anyway. It has less value when it is compensating for a business model that is becoming harder to justify.

That trade-off becomes sharper in Orlando because the market can look strong while operating details become more demanding. The owner who needs aggressive depreciation to justify the asset may be holding the wrong property or holding it in the wrong form. In contrast, a property with healthy margins and reserve discipline can often tolerate a less aggressive tax posture and still produce better long-term results.

A related failure mode is false comfort from “profitability after tax.” Tax savings are still cash, but they are not the same as durable operating margin. Investors should separate the two when deciding whether to keep, scale, or exit.

Retirement, pensions, and RMD coordination

Retirement timing changes the value of the same property. A sale that looks painful in a year crowded by earned income, portfolio distributions, or other gains may look far more efficient in a lower-income transition year. The tax rules on the property do not need to change for the planning value of timing to change.

That makes retirement coordination especially relevant for high-income readers approaching the end of a business cycle or compensation peak. A property sold before pension income becomes fixed, before required distributions rise, or during a temporary lull in business income can produce a meaningfully different after-tax outcome than the same sale executed later.

The same point applies during the hold period. A cost segregation study completed in a peak-income year may be far more valuable than one completed after the owner has already stepped back from earned income. Likewise, a passive-loss carryforward may be strategically more useful if released in a year when other sources of income make the deduction especially valuable.

Retirement coordination also helps prevent forced sequencing errors. When an investor waits too long to align the STR with broader household planning, the eventual choice may be between a tax-inefficient sale and an economically weak hold. The better approach is to identify likely retirement windows and design the property’s life cycle around them early.

A second-order issue here is estate and family transition. Even if the property is not intended as a legacy asset, the ownership structure and participation model may need to change as the primary operator reduces involvement. That operational shift should be treated as part of tax planning, not as something separate from it.

Asset-based planning beats deduction-first planning

A short-term rental should be analyzed as an asset inside a larger household system, not as a stand-alone bucket of deductions. When investors begin with the question “what can we write off this year,” they often produce tactics without a durable plan. When they begin with the question “what role should this property play in the household balance sheet,” the planning gets sharper.

That role may be current cash flow, offsetting losses, concentrated Orlando exposure, family-use optionality, or a timed liquidity event. Different roles justify different tax choices. A property intended for medium-term cash flow may not need the same depreciation posture as one intended to absorb a high-income year and then exit on a deliberate schedule.

This asset-based approach also improves comparisons across opportunities. A new Orlando STR should not only be measured against other vacation rentals. It should be measured against other uses of capital with different NIIT exposure, different management burden, and different exit friction. That is where many tax-driven acquisitions become less compelling.

An investor who treats the STR as one component of a larger capital-allocation plan is also less likely to let tax aversion dictate holding period. That is usually where long-term returns improve.

Correcting common misuse and oversights

One common misuse is treating “short-term rental strategy” as shorthand for accelerated depreciation. Depreciation can be useful, but a strategy that ends there is incomplete because it leaves classification, NIIT, and exit mechanics under-modeled.

Another mistake is assuming that short guest stays automatically create nonpassive losses. Current IRS guidance still requires the average-use and service rules to be met before the activity is even outside the rental-activity definition, and material participation still must be established after that.

A third mistake is to plan the property as though operations and exit were unrelated. They are linked by depreciation, by passive-loss tracking, and by the practical reality that the sale year reveals whether the earlier strategy was coherent.

A fourth oversight is underestimating the operational meaning of the intended tax result. If the strategy requires owner-heavy participation every year, the investor should ask whether that labor pattern is realistic. A tax result that depends on unsustainable effort is fragile by definition.

Finally, many high-income investors still underweight NIIT because it feels secondary to ordinary income tax. In practice, it can materially change operating-year and sale-year results for passive holdings. That is one reason we treat character and timing as co-equal parts of the analysis.

We can review whether the current ownership and entity structure still fits the intended participation level, cash flow goals, and multi-year exit plan.

Florida-specific planning considerations

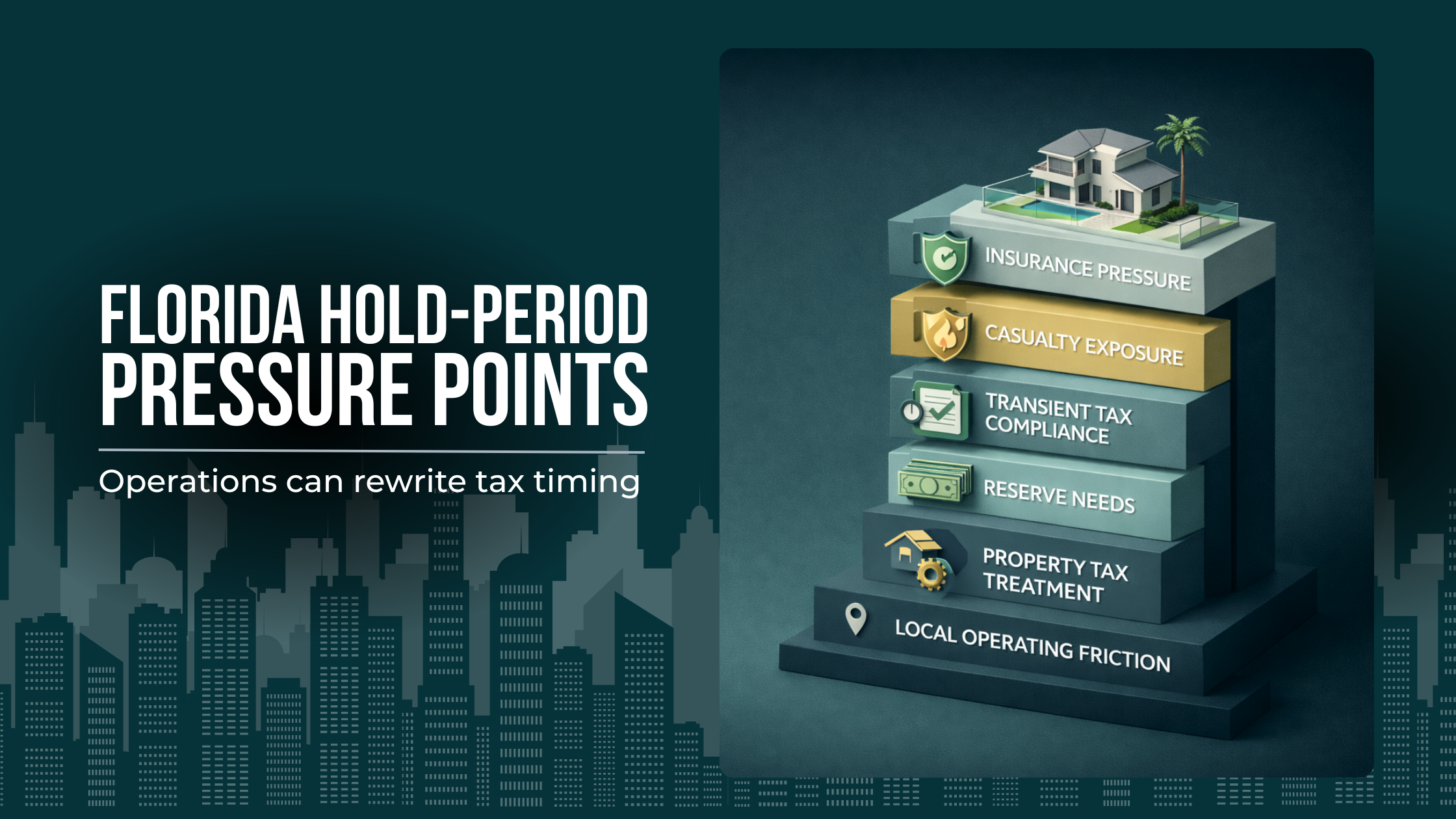

Florida-specific planning starts with the obvious operating taxes but should not end there. The Florida Department of Revenue currently imposes 6% state sales tax on transient accommodations, plus any applicable discretionary surtax, and Orange County currently imposes a 6% tourist development tax on lodging stays of less than six months. Orlando also maintains local short-term-rental registration requirements in the city. Those rules matter for setup, billing, recordkeeping, and management processes.

The larger strategic point is that Florida’s no-state-income-tax profile does not make Orlando STRs automatically more tax-efficient. It simply shifts more weight to the federal return. If the asset is passive, NIIT can still matter. If the property is sold after aggressive depreciation, federal gain mechanics still matter. And if the household is concentrated in Florida real estate, correlation risk still matters.

This checklist ties Florida-specific operating realities back to the article’s core point that tax planning only works when it survives real-world hold-period pressure.

Florida also changes the hold-versus-sell analysis because the operating environment can force earlier decisions than the tax model assumed. Insurance pressure, storm-related reserve needs, and compliance friction may shorten the practical hold period. When that happens, earlier deductions should be reevaluated against the now-likely sale year rather than defended merely because they looked attractive at acquisition.

Property-type and local-rule differences matter too. A city, county, or HOA constraint can make one ownership model easier to operate than another. Even when the article’s main focus is federal tax planning, these local realities influence whether owner participation remains realistic and whether the original tax posture is sustainable.

Florida-specific planning should therefore do two things at once: respect the consumption-tax and registration framework on the front end, and keep federal life-cycle planning central on the back end. The market rewards investors who can do both.

There is also a portfolio concentration angle unique to many Florida households. The investor with multiple Florida properties may not have a “property problem” so much as a timing problem. If several assets are exposed to the same insurance or tourism cycle, liquidity decisions can cluster. That makes sale-year sequencing even more important than it would be in a more diversified real-estate portfolio.

We can compare hold, refinance, repurpose, and sale scenarios with attention to unrecaptured §1250 gain, suspended losses, and the timing of other household income.

Conclusion

The best short-term rental tax Florida Orlando strategy is not built on hype, loophole language, or one-year deduction math. It is built on classification, sequencing, and exit awareness. Florida’s operating taxes and Orlando’s local compliance framework still matter, but for high-income investors the larger value comes from designing the property’s tax character over time: acquisition year, stabilized years, and exit year.

That means we start with the actual facts of the activity, not with the deduction we hope to claim. We ask whether the property is likely to remain passive or supportably nonpassive, whether NIIT is being modeled alongside ordinary income and gain, whether cost segregation fits the real hold period, and whether the ownership structure preserves flexibility if operations or family planning change.

It also means we treat exit planning as part of the initial investment thesis. Depreciation can create genuine value, but only when the owner understands what happens later through basis reduction, unrecaptured §1250 gain, section 1231 treatment, and sale-year stacking. The Orlando STR that creates the best long-term result is usually not the one with the largest first-year deduction. It is the one whose tax treatment still makes sense when facts change, participation shifts, and the market tells the owner it is time to refinance, repurpose, or sell.

We can work through the next phase of the property with a focus on sequencing, whether the activity is passive or nonpassive, and how that choice shapes later outcomes.

Frequently Asked Questions

How should a high-income investor decide whether to sell in the same year as another liquidity event?

The main issue is stacking. A property sale rarely lands in an otherwise quiet return. If the same year already includes business income, portfolio gains, deferred compensation, or retirement distributions, the property’s gain can become more expensive than it looks in isolation. The better approach is to evaluate the short-term rental as part of the household’s overall gain calendar, not as a separate event. In practice, that means comparing whether the sale belongs in a peak-income year, a transition year, or a lower-income window where the same exit may produce a more efficient after-tax result.

When does a refinance change the planning picture even if the property is not being sold?

A refinance can change the planning picture when it signals a shift in how long the property is likely to be held, how much cash flow pressure the asset needs to absorb, or whether the owner still wants the same operating posture. The tax rules may not change just because debt changes, but the strategy often should. A property refinanced to support a longer hold may justify a different sequencing decision than one refinanced as a bridge to a future sale, repurpose, or broader capital reallocation. The point is not the loan alone. It is what the refinance reveals about the next phase of the asset.

What is the real risk of changing from owner-heavy operations to third-party management?

The practical risk is strategy drift. A property may begin with owner-heavy involvement that supports a particular tax posture, then become manager-led once operations stabilize or personal priorities change. That shift can affect how the activity fits into the broader household return, especially when earlier planning assumed a level of participation that no longer exists. The key issue is continuity. A strategy built around one operating model should be revisited when the model changes, because the property’s tax character and its value to the wider plan may shift even if revenue remains strong.

How should investors think about exit if they are undecided between holding, repurposing, or selling?

The first step is to stop treating those as minor variations of the same outcome. Holding, repurposing, and selling can produce very different multi-year consequences once depreciation, gain character, and timing are considered together. A property that still works operationally may not be the best asset to keep if its sale fits a better tax window today. On the other hand, a sale that looks inefficient this year may argue for a temporary hold or repurpose. The right comparison is after-tax flexibility across scenarios, not just which option minimizes immediate friction.

What makes ownership structure more important once family or co-investors are involved?

Ownership structure becomes more important when the people funding the asset are not the same people operating it, or when future transfers, partial exits, or family planning are likely. In that setting, the structure is doing more than holding title. It shapes how flexible the economics are, how easy it is to document who actually participates, and how much friction appears when the asset needs to change form later. A structure that feels simple at acquisition can become restrictive when the family wants to shift economics, add an investor, or prepare the property for a staged transition instead of a clean sale.

How do Florida operating realities affect tax decisions even when the federal rules stay the same?

Florida can compress the hold period without changing the federal rules at all. Insurance pressure, reserve needs, casualty exposure, property-tax treatment, and local operating friction can make an asset less attractive to hold for as long as originally planned. That matters because many tax choices assume time. If the property exits earlier than expected, earlier depreciation and classification decisions may look very different in hindsight. For Florida investors, that is the key operational lesson: the environment around the property can rewrite the timeline, and the timeline is what determines whether a tax strategy still works.