What Are the Benefits of Strategic Tax Planning for Real Estate Investors?

The benefits of strategic tax planning for real estate investors go far beyond lowering this year’s tax bill.

For a sophisticated investor, strong tax planning can improve after-tax cash flow, help determine whether losses are actually usable, coordinate depreciation with income, reduce exit-year tax pressure, support better entity decisions, and make real estate tax strategy part of a broader wealth plan.

The difference is timing.

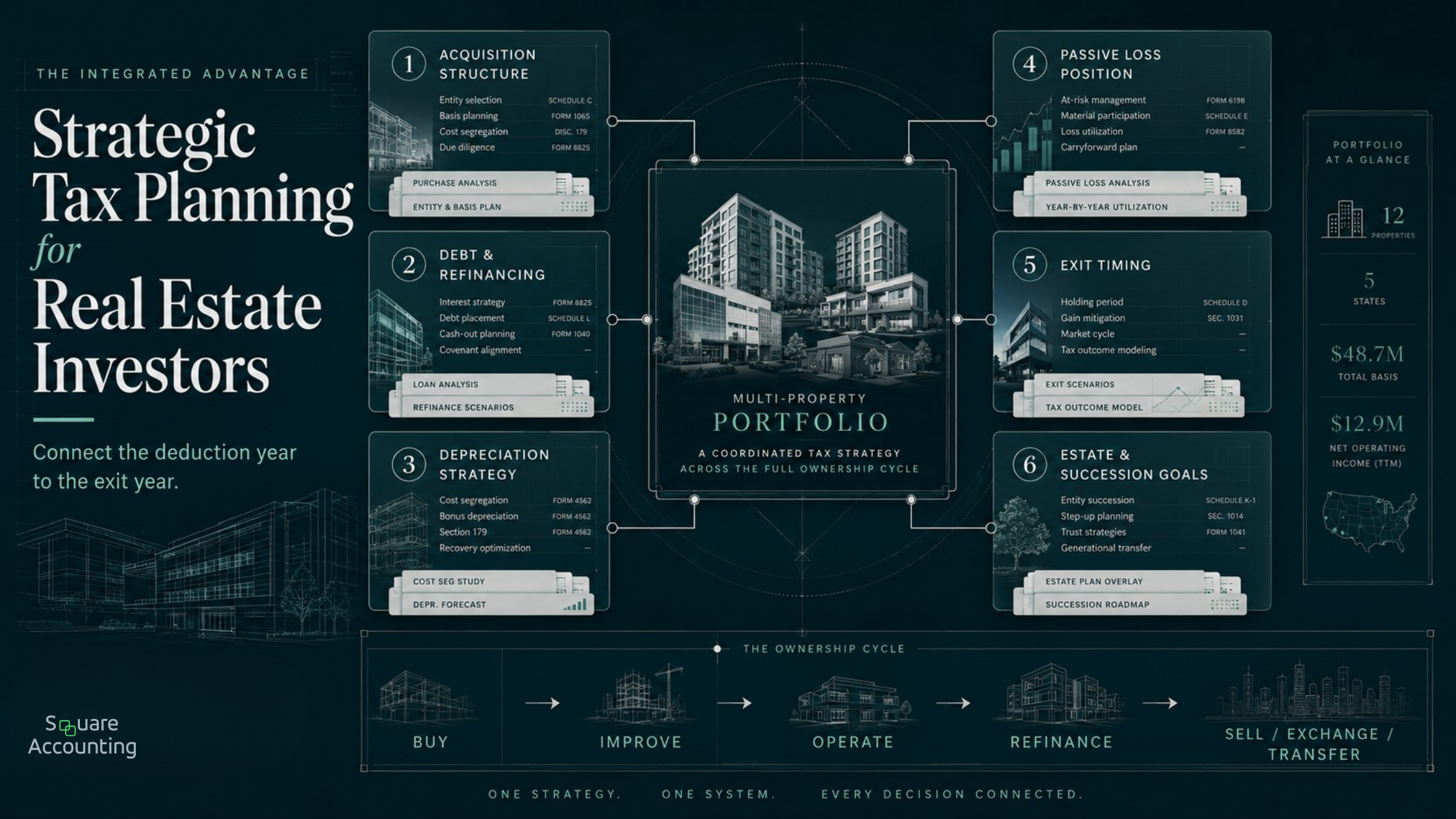

The strongest real estate tax strategy connects each year’s tax decisions to the full life of the portfolio.

“Real estate tax planning becomes more valuable when it is viewed across the full ownership cycle. The goal is not simply to create deductions, but to understand how today’s decisions shape future flexibility, gain, liquidity, and exit options.”

Basic tax preparation records what already happened. Strategic tax planning helps shape decisions before the tax result becomes difficult or impossible to change.

That matters because real estate can create meaningful tax benefits during ownership. But those same benefits can create future pressure if they are not coordinated with basis, passive loss rules, debt, refinancing, 1031 exchange options, depreciation recapture, estate planning, and the investor’s broader income picture.

A large deduction this year may help. It may also create suspended losses, reduce basis, increase future gain, or pressure the investor into a rushed exchange later.

The best planning does not ask only, “How do we reduce tax this year?”

It asks, “How do we structure, time, document, and eventually exit this portfolio in a way that supports the investor’s long-term financial plan?”

Key takeaway: Strategic tax planning for real estate investors is most valuable when it connects the deduction year to the exit year. The strongest plan is not always the one that produces the largest current deduction. It is the one that improves after-tax outcomes across the life of the portfolio.

What are the benefits of strategic tax planning for real estate investors?

Strategic tax planning helps real estate investors make better decisions before tax consequences become fixed.

The main benefits include:

Better after-tax cash flow

Smarter use of depreciation and cost segregation

Clearer planning around passive activity loss limits

Better coordination between real estate income and business income

Stronger acquisition and entity structuring decisions

Better timing of sales, exchanges, refinances, and improvements

Reduced surprise from capital gains, depreciation recapture, and NIIT

Better documentation before a tax position is challenged

More coordinated planning with estate, liquidity, and succession goals

Fewer isolated decisions across properties, tax years, and advisors

For Florida investors, this planning is especially important because Florida does not impose a personal state income tax, but federal tax rules still drive the outcome for rental income, capital gains, depreciation, passive losses, NIIT, and exit planning.

Florida’s tax environment can be favorable. It does not eliminate the need for federal tax strategy.

That is where many real estate investors become overconfident. They focus on the state tax advantage but under-plan for the federal issues that usually drive the real tax result.

We help evaluate whether your real estate tax decisions are being coordinated across depreciation, passive losses, cash flow, and exit timing.

Strategic planning turns real estate from a tax deduction into a tax system

Many investors think of real estate tax planning as a set of separate tactics.

Cost segregation.

Bonus depreciation.

1031 exchanges.

Real estate professional status.

Short-term rental rules.

Entity structure.

Interest expense.

Repairs.

Travel.

Home office.

Each tool matters. But the benefit of strategic tax planning is not simply knowing that each tool exists.

The benefit is knowing how the tools interact.

A cost segregation study may accelerate depreciation. But if the investor cannot currently use the losses because of passive activity limits, the current-year benefit may be limited. A 1031 exchange may defer gain, but it can also carry low basis and depreciation history into the next property. An LLC may help with legal separation and ownership tracking, but it does not automatically make losses deductible or eliminate gain on sale.

Real estate tax strategy works best when each decision is evaluated across the full ownership cycle:

Acquisition

Financing

Operations

Depreciation

Loss utilization

Refinancing or reinvestment

Sale, exchange, gift, or estate transfer

A tax plan that ignores one stage can create problems in another.

This is the strategic difference between tax planning and tax reaction. Tax reaction looks for deductions after the year is over. Tax planning coordinates decisions before they compound.

Benefit 1: Better after-tax cash flow

Real estate investors often measure performance using rent, debt service, operating expenses, appreciation, and cap rate.

Sophisticated investors also need to measure after-tax cash flow.

A property can look strong before tax but underperform after tax if deductions are poorly timed, losses are suspended, debt is structured inefficiently, or exit costs are ignored.

Strategic tax planning helps determine:

Which deductions are available

Which deductions are actually usable

Which deductions may be deferred

Which years are most valuable for deduction timing

Whether the property’s tax profile supports the investor’s cash flow goals

Depreciation is central to this analysis. Real estate can produce taxable losses even when a property produces positive cash flow. That is one of the reasons real estate remains attractive to high-income investors.

But depreciation does not have the same value for every investor.

An investor with high business income may care deeply about whether real estate losses can offset nonpassive income. An investor with mostly passive income may focus on matching passive income with passive losses. An investor preparing for a liquidity event may need deductions timed to a year when income is unusually high.

The same property can produce different tax value depending on the investor’s broader income picture.

That is why the planning should start with the investor, not the property.

Benefit 2: More intelligent use of depreciation and cost segregation

Cost segregation can make that benefit more immediate by identifying property components that may qualify for shorter depreciation lives. Under current IRS guidance, 100% bonus depreciation generally applies to qualified property acquired and placed in service after January 19, 2025, subject to eligibility rules and available elections.

That creates planning opportunity. It also requires judgment.

A shallow planning conversation asks:

“How large can the deduction be?”

A better planning conversation asks:

“Should we accelerate the deduction, and what happens if we do?”

Acceleration can be valuable when it offsets income that would otherwise be taxed at a high marginal rate. But acceleration may be less useful if the losses are suspended, if the investor expects higher income in a future year, if the property may be sold soon, or if the deduction creates future recapture pressure without a reinvestment strategy.

This is one of the most important distinctions in advanced real estate tax planning.

The largest deduction is not always the best deduction.

The best deduction is the one that fits the investor’s income profile, holding period, passive loss position, financing plan, and exit strategy.

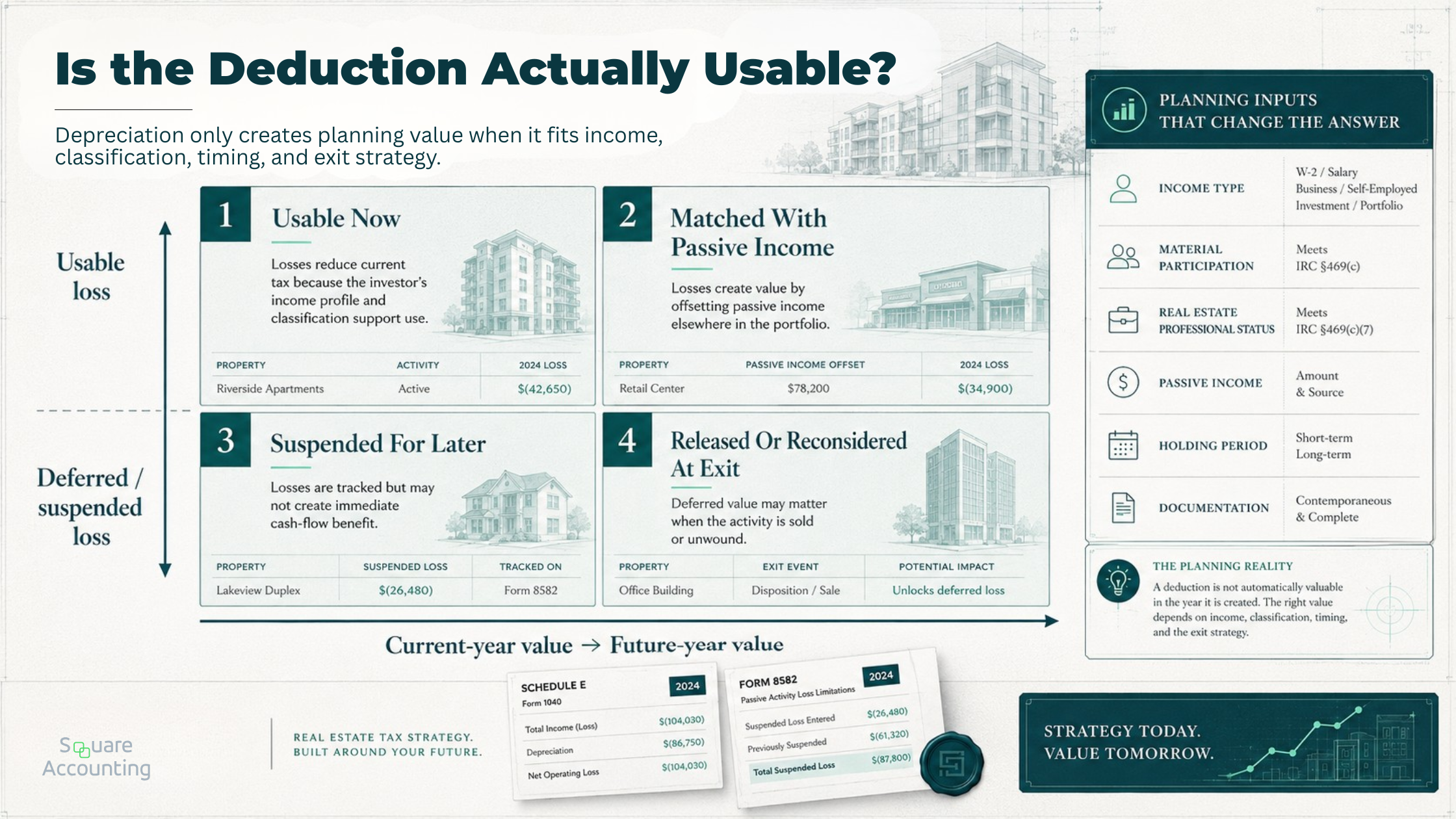

Benefit 3: Better planning around passive activity loss limits

Passive loss planning is one of the places where successful investors can still get surprised.

Real estate can produce large tax losses. That does not mean every investor can use those losses immediately.

If rental losses are passive and the investor does not have enough passive income, those losses may be suspended and carried forward. That can still be valuable, but it changes the strategy.

The same deduction can produce very different value depending on whether the investor can use the loss in the intended year.

“Before accelerating deductions, investors need to know whether those deductions can be used in the current year or whether they are building deferred value. This distinction is often where real estate tax strategy becomes more complex than a simple deduction analysis.”

The planning question becomes:

“Are these losses reducing tax now, building value for later, or creating a mismatch we need to manage?”

Strategic planning evaluates:

Whether each activity is passive or nonpassive

Whether the investor materially participates

Whether real estate professional status is realistic and supportable

Whether grouping elections should be considered

Whether passive income exists or can be created

Whether suspended losses may be released in a future disposition

Whether the investor’s documentation supports the position being taken

This is especially relevant for high-income professionals and business owners who invest in real estate while maintaining demanding careers or operating companies.

Real estate professional status can materially change the analysis, but it should not be treated as a label to claim casually. The position needs to be evaluated before filing, supported by facts, and documented with care.

The benefit of planning is not simply trying to qualify for a favorable rule.

The benefit is knowing whether the position is strong enough to rely on.

We review whether real estate losses are usable now, suspended for later, or creating a mismatch that needs planning before year-end.

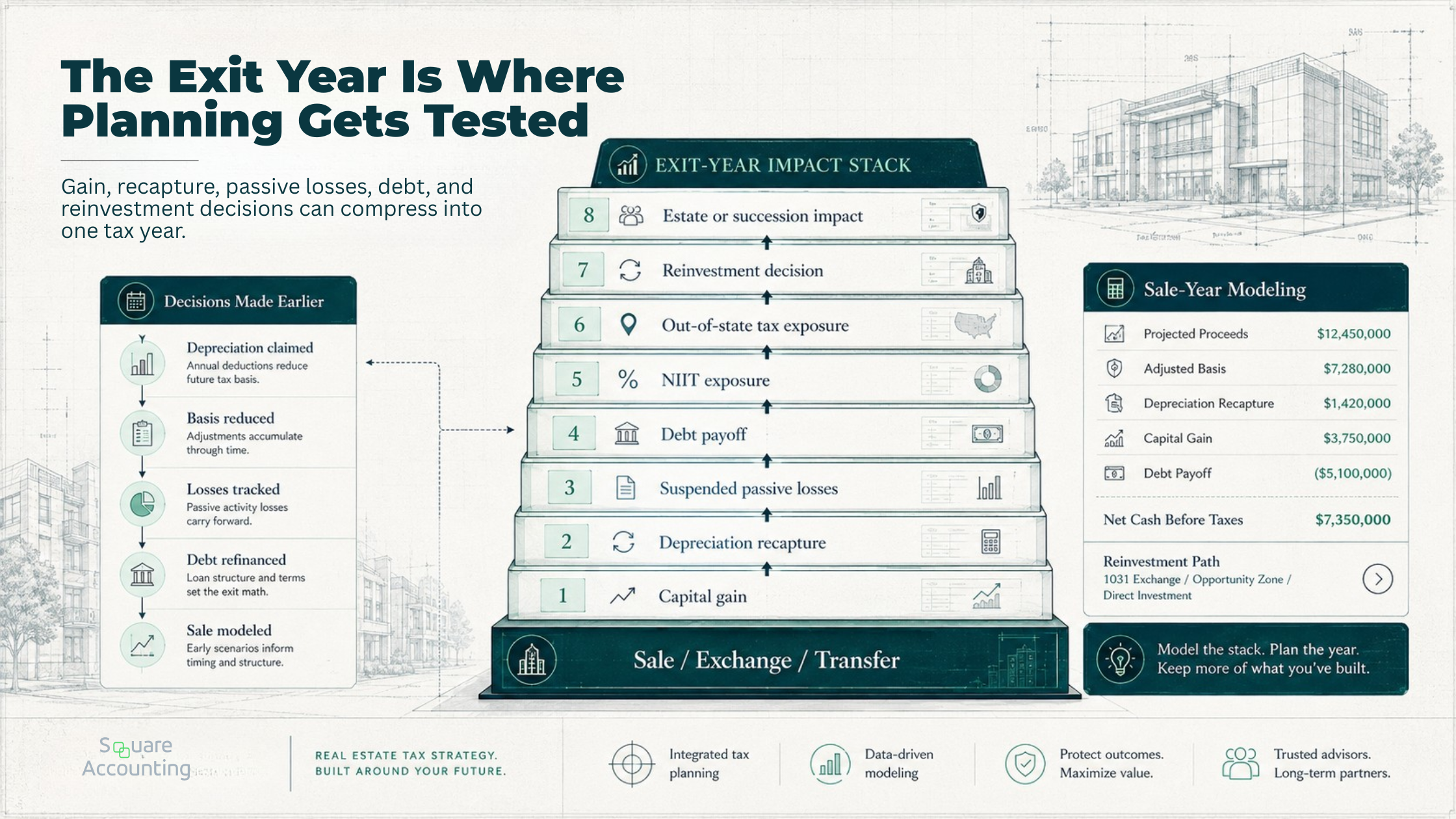

Benefit 4: Reducing exit-year tax pressure

Many investors focus heavily on reducing taxes during ownership and under-plan for the sale.

That can be expensive.

A profitable exit may involve several layers of tax analysis:

Capital gain

Depreciation recapture

Suspended passive losses

Debt payoff

Installment sale treatment

1031 exchange eligibility

State tax exposure if property is outside Florida

NIIT exposure

Cash available after closing

Estate or succession goals

A strong tax plan models the sale before the investor is already under contract.

“A sale year can compress years of prior depreciation, debt decisions, passive loss treatment, and reinvestment choices into a single planning window. Modeling that pressure early gives the investor more options than reacting after the transaction is already moving.”

The issue is not only whether there is gain.

The issue is how many tax consequences are compressed into one year.

Depreciation that helped during ownership may reduce basis. A lower basis can increase gain on sale. Accelerated depreciation may improve current-year cash flow, but it can also increase the importance of modeling recapture and reinvestment options before a sale.

This does not mean depreciation is bad. It means depreciation should be connected to the exit plan.

The best exit planning often starts before a property is listed. That gives the investor time to evaluate whether to sell, refinance, exchange, gift, hold, harvest other losses, restructure ownership, or coordinate the sale with a lower-income year.

Once the purchase agreement is signed and deadlines begin moving, tax planning becomes narrower.

We help analyze how depreciation, basis, suspended losses, recapture, and reinvestment options may affect a future sale.

Benefit 5: Better 1031 exchange decisions

A 1031 exchange can be a powerful tool, but it should not be treated as an automatic answer.

The core benefit is deferral. A properly structured exchange may allow an investor to defer gain by reinvesting into qualifying like-kind real property held for business or investment use. The IRS describes Section 1031 as applying to real property held for productive use in a trade or business or for investment when exchanged for like-kind real property.

But deferral is not the same as elimination.

That distinction matters.

A 1031 exchange can preserve capital for reinvestment and help an investor continue compounding. It can also carry basis history, depreciation history, debt requirements, and future tax exposure into the replacement property.

Strategic planning asks:

Does the replacement property improve the portfolio?

Is the investor buying because the deal is strong or because the exchange clock creates pressure?

Will the new debt structure support cash flow?

Is the investor preserving optionality or creating complexity?

Does the exchange support estate, liquidity, and succession goals?

Would recognizing some gain create more flexibility than forcing a poor replacement purchase?

The tax deferral is valuable only if the real estate decision still makes sense.

A poor exchange can defer tax while weakening the portfolio.

Benefit 6: Coordinating real estate planning with business income

Many Florida real estate investors are also business owners, physicians, attorneys, consultants, executives, or owners of service-based companies.

That makes planning more complex and more valuable.

Real estate decisions may interact with:

S corporation wages and distributions

Business sale timing

Retirement plan contributions

Charitable planning

Estimated tax payments

Stock compensation

Capital gains from brokerage accounts

Spouse income and participation

Trust and estate planning

Cash needed for business expansion or debt service

A rental property strategy that looks reasonable in isolation may be suboptimal when the investor’s full income picture is considered.

For example, accelerating depreciation into a moderate-income year may be less valuable than preserving planning flexibility for a year when the investor expects a business sale, large bonus, stock vesting, or major capital gain.

The benefit of strategic planning is sequencing.

Tax savings have different value depending on the year in which they occur.

A strong advisor should not only ask what properties the investor owns. The advisor should ask what income events, liquidity events, and family wealth decisions are coming next.

Benefit 7: Avoiding entity structure mistakes

Entity structure is often oversold in real estate tax discussions.

LLCs, partnerships, S corporations, disregarded entities, trusts, and holding companies can all play roles depending on the investor’s facts. But entity structure is not a substitute for tax planning.

A structure may help with legal separation, ownership tracking, estate planning, partner economics, and financing clarity. But the entity itself does not automatically make losses deductible, eliminate tax on sale, or solve passive loss limitations.

Strategic tax planning reviews structure in context:

Who owns the property?

Is the property owned individually, jointly, through an LLC, through a partnership, or through a trust?

Are there multiple owners with different tax profiles?

Are capital accounts and allocations properly tracked?

Does the structure support future refinancing, gifting, or sale?

Is the investor creating unnecessary administrative complexity?

Could the current structure make a future 1031 exchange or estate plan harder?

Does the structure match how lenders, attorneys, and family members expect the asset to be held?

For high-net-worth investors, the right structure is often the one that balances tax efficiency, legal risk, lender requirements, estate goals, and operating simplicity.

The goal is not complexity. The goal is control.

We evaluate whether your ownership structure supports tax efficiency, financing, estate goals, and future transaction flexibility.

Benefit 8: Improving documentation before it matters

Tax planning is not only about numbers.

It is also about proof.

The most valuable tax position can weaken if the records do not support it.

Documentation is especially important for:

Real estate professional status

Short-term rental activity

Cost segregation support

Business purpose

Travel and vehicle expenses

Related-party transactions

Capital contributions and distributions

Debt allocations

Partner reimbursements

Strategic planning creates documentation standards before year-end.

That matters because many facts cannot be recreated cleanly after the fact. Calendars, time logs, invoices, closing statements, management agreements, leases, debt documents, and accounting records should support the position being taken.

For sophisticated investors, documentation is not clerical.

It is part of the strategy.

Benefit 9: Managing NIIT and investment income exposure

High-income real estate investors also need to consider the net investment income tax.

The IRS states that a 3.8% net investment income tax applies to individuals, estates, and trusts that have net investment income above applicable threshold amounts.

Rental income, gains, and passive investment income may enter the analysis depending on the facts.

Strategic planning can help evaluate whether income is passive or nonpassive, whether certain activities rise to a trade or business level, how gains may be timed, and whether other income sources push the investor into additional exposure.

For Florida investors, NIIT is a federal issue. Florida’s lack of personal income tax does not remove it.

This is a common blind spot.

An investor may correctly focus on ordinary income rates, capital gains, depreciation, and state residency while underestimating how federal investment income taxes layer onto the result.

That layering becomes especially important in a sale year, a high-income year, or a year when multiple investment gains occur at once.

Benefit 10: Building a portfolio that is tax-aware, not tax-driven

The best tax strategy should support the investment strategy.

It should not replace it.

A real estate investor can make poor economic decisions while chasing deductions. Overpaying for property, accepting weak debt terms, buying in the wrong market, or forcing a rushed exchange can destroy more value than the tax benefit creates.

Strategic tax planning helps separate three questions:

Is this a good investment before tax?

What is the tax result if we do nothing special?

What planning options improve the after-tax outcome without weakening the investment decision?

That order matters.

Tax benefits are most valuable when they enhance a sound investment, not when they justify a weak one.

This is especially important in competitive real estate markets where investors may feel pressure to act quickly. Tax planning should sharpen judgment, not create an excuse to ignore investment discipline.

The failure mode: maximizing deductions without planning the exit

One of the most common mistakes among successful real estate investors is treating the tax plan as complete once the current-year deduction is created.

That is too narrow.

A large current-year deduction can be useful, but it may also create or intensify future issues:

Suspended passive losses if the investor cannot use them currently

Lower adjusted basis

Higher gain on sale

Depreciation recapture exposure

Pressure to complete a 1031 exchange

Reduced flexibility if the investor needs liquidity

Complexity for heirs or family transfers

Misalignment with estate planning

This does not mean investors should avoid depreciation, cost segregation, or tax deferral.

It means they should understand the full arc of the strategy.

The better planning question is not, “Can we create a deduction?”

The better planning question is, “What happens when we unwind this position?”

That is the difference between a tactic and a plan.

What strategic tax planning should include for real estate investors

A strong real estate tax planning process should not start with a generic checklist.

It should start with the investor’s facts.

A serious planning review should usually consider:

Current and prior tax returns

Entity structure and ownership chart

Closing statements for acquisitions and sales

Depreciation schedules

Debt schedules

Lease and management agreements

Profit and loss statements by property

Partner or shareholder basis records

Planned purchases, sales, refinances, and improvements

Business income projections

Estate, gifting, or succession goals

Expected liquidity needs

Without those inputs, planning can become guesswork.

This is one of the clearest ways to evaluate whether a tax advisor is being strategic.

If recommendations are being made before the advisor reviews returns, depreciation schedules, ownership structure, debt, and planned transactions, the process may be too thin for a serious investor.

For sophisticated investors, the advisory value comes from connecting the documents to the decisions.

We review returns, depreciation schedules, ownership structure, debt, and planned transactions before making planning recommendations.

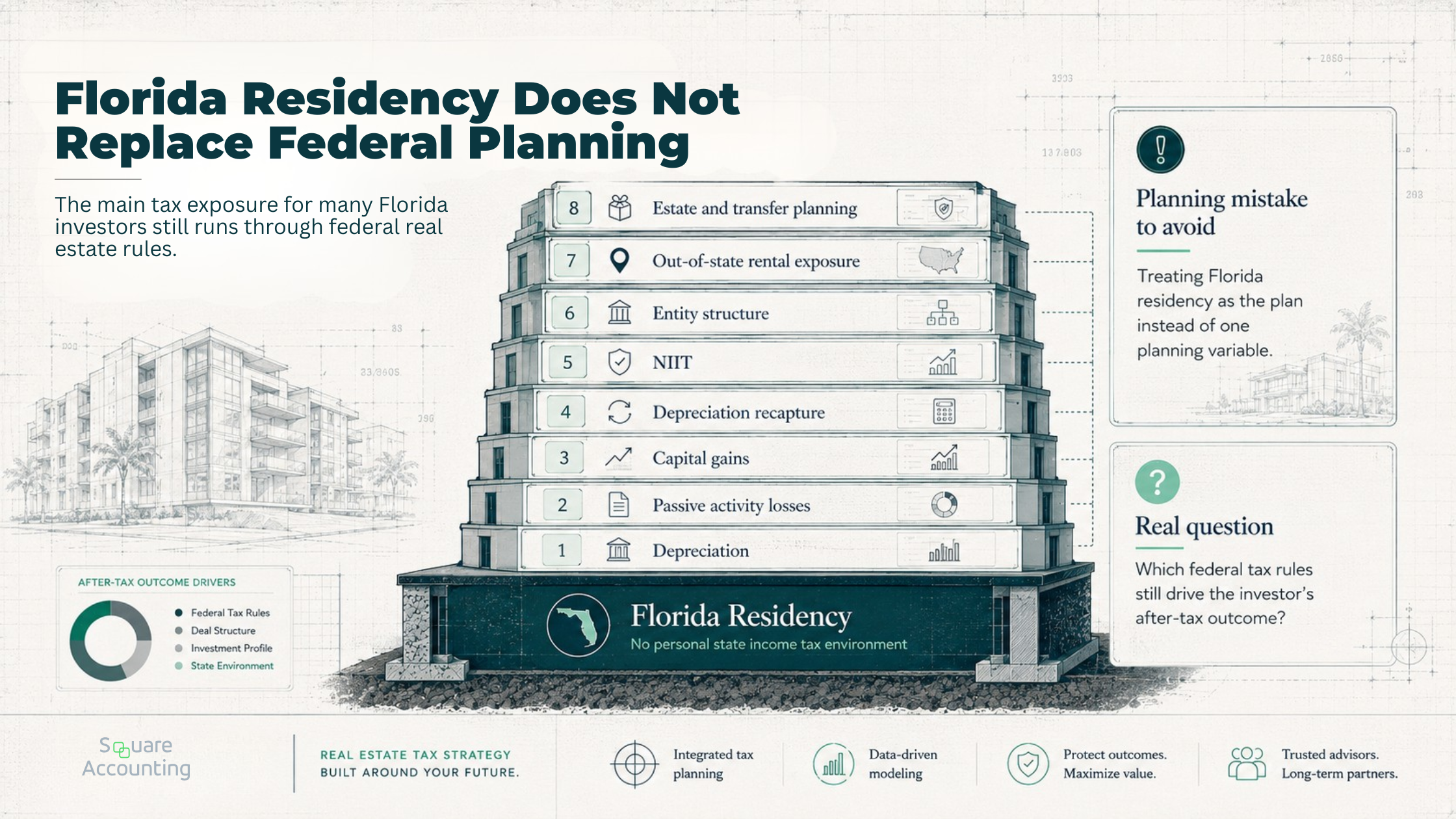

Florida-specific planning considerations

Florida’s tax environment can be attractive for high-income investors because there is no personal state income tax.

But Florida investors still need to plan carefully.

The main Florida-specific point is not that Florida eliminates tax complexity. It does not.

Instead, Florida changes the planning emphasis.

Florida changes the planning emphasis, but federal real estate tax rules still drive many high-income investor outcomes.

“For Florida investors, the planning advantage often comes from coordinating federal tax rules with residency, entity structure, and out-of-state property ownership. The state tax environment is important, but it should not be mistaken for a complete tax strategy.”

For many Florida residents, the largest income tax exposures are federal. That means planning should focus heavily on federal rules governing depreciation, passive activity losses, NIIT, capital gains, recapture, entity structure, and estate strategy.

Florida investors who own property in other states also need to account for nonresident state filing and tax exposure. A Florida resident with rental property in Georgia, North Carolina, New York, California, or another state may still have tax obligations where the property is located.

This matters for investors who move to Florida, operate businesses in Florida, but own real estate across multiple states.

Florida residency can be powerful.

It is not a substitute for coordinated planning.

When should a real estate investor start strategic tax planning?

The best time to start is before a major transaction.

That includes:

Before acquiring a property

Before placing major improvements in service

Before ordering a cost segregation study

Before changing property use

Before converting a personal residence to a rental

Before selling appreciated property

Before entering a 1031 exchange

Before refinancing

Before admitting partners

Before transferring property to family or a trust

Before a business sale or high-income year

Year-end planning can still help, but many of the strongest options require lead time.

Once a property is sold, an entity is formed, proceeds are received, or ownership is transferred, the available planning choices may narrow quickly.

The investors who benefit most from strategic planning are usually the ones who involve their advisor before the decision is final, not after the closing statement arrives.

The real benefit: fewer isolated decisions

Strategic tax planning benefits real estate investors because it reduces isolated decision-making.

Instead of treating each tax year, property, deduction, and sale separately, planning creates a coordinated view of the investor’s financial life.

That is especially important for high-income Florida investors who may have business income, investment income, multiple properties, family wealth goals, and existing advisors.

A strong tax plan should help answer:

Which deductions matter now?

Which deductions may be more valuable later?

Which losses are usable and which are suspended?

Which properties carry future tax pressure?

Which exits should be modeled before the market forces a decision?

Which entity structures support long-term goals?

Which tax strategies create future complexity?

Which decisions should be coordinated with legal, estate, lending, and investment advisors?

This is also where the planning conversation becomes useful for investors who already have a CPA.

The question is not whether the return is prepared correctly.

The question is whether the tax strategy is shaping decisions early enough to matter.

Conclusion: strategic tax planning is a portfolio-level discipline

So, what are the benefits of strategic tax planning for real estate investors?

The clearest benefit is better control.

Not perfect control. Not guaranteed savings. But better visibility, better timing, better documentation, and better coordination between today’s tax decisions and tomorrow’s financial outcomes.

For sophisticated investors, real estate tax planning should not be a once-a-year review of deductions. It should be a multi-year planning process that connects acquisition, depreciation, passive losses, cash flow, debt, entity structure, exit timing, and estate goals.

The investors who benefit most are often not the ones chasing the largest current-year deduction.

They are the ones who understand how each tax decision affects the next one.

We help Florida investors connect real estate decisions with income, exit timing, documentation, and long-term portfolio goals.

Strategic Tax Planning for Real Estate Investors FAQs

Key questions for Florida real estate investors evaluating whether tax planning is being coordinated around acquisitions, depreciation, passive losses, financing, documentation, and future exits.

How is strategic tax planning different from annual tax preparation?

Annual tax preparation mainly organizes and reports what already happened. Strategic tax planning looks ahead at acquisitions, depreciation, passive losses, financing, entity structure, and future exits before those decisions become fixed. For a real estate investor, the difference is timing and coordination. A return may be accurate but still reactive. A stronger planning process asks whether today’s deduction, ownership structure, or sale decision supports the investor’s future income profile, liquidity needs, and long-term portfolio goals.

How can real estate investors know whether depreciation is actually helping them?

Depreciation is helpful when it creates usable tax value in the right year and fits the investor’s broader plan. The key question is not only whether depreciation creates a deduction. The question is whether that deduction offsets current income, becomes suspended, reduces basis, or creates future recapture pressure. We would look at income sources, passive loss position, holding period, expected sale timing, and reinvestment plans before assuming accelerated depreciation is the best move.

What should investors review before buying another rental property?

Before acquiring another property, investors should review more than projected rent and financing terms. The tax review should include ownership structure, expected depreciation, debt allocation, passive loss position, current and future income, potential improvements, and likely exit path. A property can be economically sound but still create tax inefficiency if it is purchased in the wrong structure, timed poorly, or added to a portfolio without understanding how losses, basis, and future sale planning will interact.

When can a 1031 exchange create a strategic problem?

A 1031 exchange can create a problem when tax deferral becomes more important than the quality of the replacement investment. The article’s planning logic is that deferral is valuable only if the real estate decision still makes sense. If an investor buys under deadline pressure, accepts weak debt terms, increases complexity, or chooses a replacement property that does not support cash flow, estate goals, or portfolio direction, the exchange may defer tax while weakening the overall plan.

How should high-income Florida investors think about out-of-state rental properties?

Florida residency can be valuable, but it does not simplify every real estate tax issue. Florida investors who own rental property in other states may still need to consider tax exposure where the property is located. More importantly, the largest planning issues for many Florida investors remain federal: depreciation, passive activity losses, capital gains, recapture, NIIT, entity structure, and exit timing. The Florida advantage should be integrated into the plan, not treated as the plan itself.

What should investors ask if they already have a CPA?

Investors who already have a CPA should ask whether the advisor is preparing history or shaping decisions before they happen. A useful planning conversation should review depreciation schedules, passive loss carryforwards, ownership structure, debt, planned purchases, expected sales, business income, and estate goals. The issue is not whether the tax return is being filed correctly. The issue is whether the tax strategy is connected early enough to influence transactions, cash flow, and exit decisions.

Why can maximizing current-year deductions be risky?

Maximizing deductions can be useful, but it becomes risky when the investor does not understand the future consequences. A large deduction may reduce current tax, but it may also lower basis, increase future gain, create recapture exposure, or produce suspended losses that do not help immediately. The stronger planning question is not simply whether a deduction can be created. It is what happens when the investor refinances, sells, exchanges, gifts, or unwinds the position later.

What makes documentation part of the tax strategy?

Documentation is part of the strategy because advanced real estate tax positions depend on facts, not just calculations. Material participation, real estate professional status, short-term rental activity, repair treatment, cost segregation support, capital contributions, debt allocations, and related-party transactions all require records that support the position being taken. Waiting until filing season can leave gaps that are difficult to recreate. Strong planning sets documentation expectations before year-end, while the facts are still fresh.