How to Find a Tax Advisor Specializing in Real Estate Investments in Florida

Finding a tax advisor for real estate investments in Florida is not the same as finding someone who can prepare a clean rental schedule.

For a high-income investor, the real issue is whether the advisor can connect the tax consequences of acquisition, ownership, cash flow, financing, depreciation, entity structure, passive activity treatment, and eventual exit. A preparer can report what happened. A real estate tax advisor should help you make better decisions before the tax result is locked in.

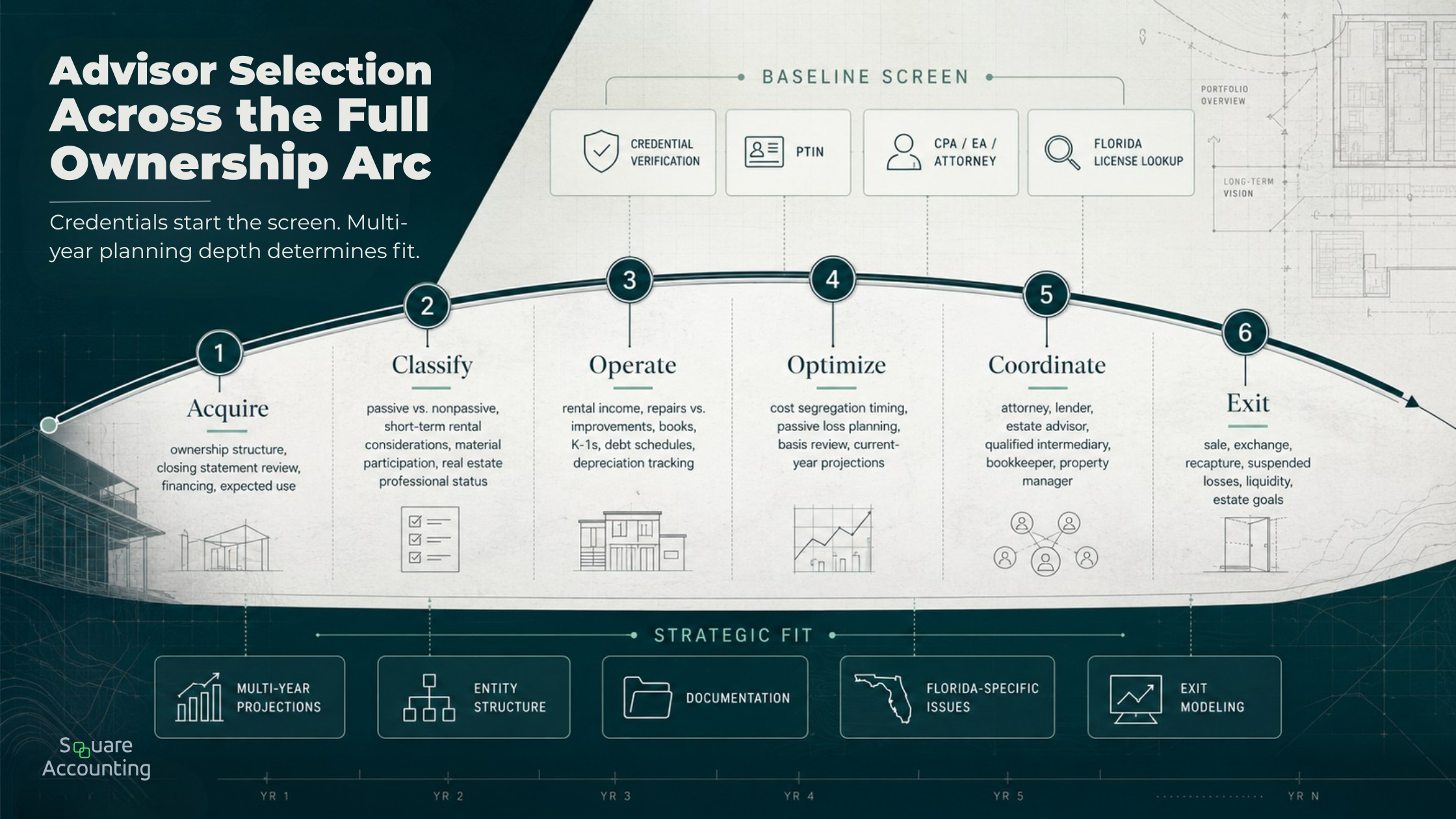

The practical answer is simple: start with credential and license verification, then move quickly to a planning-depth interview. The IRS notes that paid preparers have different levels of skill, education, and expertise, and that anyone paid to prepare federal returns generally needs a PTIN. Its preparer directory can help identify certain credentialed preparers, but it does not prove real estate investment planning depth.

Key takeaway: The best Florida real estate tax advisor is not the person who knows the most deductions. It is the advisor who can model how today’s tax position affects the next acquisition, the next refinancing, the next loss limitation issue, and the eventual sale or exchange.

The right advisor should connect acquisition, operations, classification, depreciation, coordination, and exit decisions into one planning system.

“Use the advisor search as a planning-depth test, not just a credential check. The visual below shows why the stronger question is whether the advisor can connect real estate decisions across multiple years, entities, income sources, and eventual exits.”

We review your real estate, business income, and tax posture together so planning is not limited to one filing season.

A strong advisor should be able to discuss:

What to Evaluate in a Real Estate Tax Advisor

A real estate tax advisor should be evaluated on more than credential status. The review should include planning judgment around passive activity rules, entity structure, depreciation, Florida-specific issues, and multi-year strategy.

| What to Evaluate | Why It Matters |

|---|---|

| Credential and License Status | Confirms baseline professional standing before deeper evaluation. |

| Real Estate Investment Focus | Separates rental familiarity from advanced planning judgment. |

| Passive Activity and At-Risk Rules | Determines whether losses are usable, suspended, or strategically timed. |

| Real Estate Professional Status | Requires fact-specific support, time records, and material participation analysis. |

| Entity and Ownership Structure | Affects reporting, legal coordination, financing, basis, and exit flexibility. |

| Depreciation and Cost Segregation | Can accelerate deductions, but may change future recapture and sale economics. |

| Florida-Specific Tax Issues | Includes documentary stamp tax, transient rental taxes, tangible personal property, and corporate filing exposure. |

| Multi-Year Planning Process | Shows whether the advisor is managing strategy, not just compliance. |

Square Accounting works with Florida investors, business owners, and high-income professionals who need coordinated tax planning rather than isolated annual filing.

How can I find a tax advisor specializing in real estate investments in Florida?

Use four filters.

First, verify the advisor’s tax credential. A CPA, enrolled agent, or tax attorney may be appropriate depending on the work, and the IRS explains that attorneys, CPAs, and enrolled agents have unlimited representation rights before the IRS. A PTIN alone allows someone to prepare returns for compensation, but it does not establish advanced planning expertise.

Second, if the advisor presents as a Florida CPA, confirm the license. Florida’s DBPR license search provides information about licensed individuals and businesses regulated by the Department of Business and Professional Regulation.

Third, look for real estate-specific planning fluency. The advisor should be comfortable discussing passive activity losses, real estate professional status, material participation, cost segregation, basis, suspended losses, refinancing, 1031 exchange timing, short-term rental classification, and sale-year modeling.

Fourth, test whether they think in years, not filing seasons. Ask this on the first call:

“How would you evaluate my real estate portfolio over the next five years, not just this tax year?”

A strong answer should not start and stop with deductions. It should include income character, debt, basis, accumulated depreciation, suspended losses, entity structure, liquidity needs, estate considerations, and likely exit paths.

That is the difference between hiring a return preparer and hiring a real estate tax strategist.

We help identify whether your ownership, entity, and reporting structure supports the way your portfolio is actually taxed.

The mistake: hiring for filing when the real problem is strategy

Many investors search for a Florida real estate tax advisor after a transaction is already underway.

They bought a rental.

They joined a syndication.

They converted a property to a short-term rental.

They received a large K-1.

They are preparing to sell an appreciated property.

By that point, some of the most valuable planning windows may already be narrow. Real estate tax planning often depends on decisions made before closing, before placing property in service, before changing ownership, before grouping activities, before refinancing, and before signing a sale contract.

A reactive tax preparer can record the transaction. A strategic advisor helps identify the tax consequences while the investor still has choices.

For Florida investors, the planning environment is favorable in some ways but not simple. Florida law reflects the constitutional mandate that no income tax be levied on natural persons who are residents and citizens of the state. That does not remove federal tax planning concerns, passive activity limitations, depreciation recapture, sale-year pressure, estate planning concerns, or state and local transaction obligations.

This is why the right advisor should not treat “Florida has no personal income tax” as the end of the analysis. For high-income Florida investors, federal strategy often becomes the center of the plan, while Florida-specific issues affect structure, transactions, rentals, and compliance.

What “real estate tax specialization” should actually mean

Real estate specialization should mean more than knowing that buildings are depreciable and mortgage interest may be deductible.

A specialized advisor should understand the full planning stack: how the property is acquired, how the activity is classified, how losses are limited or released, how depreciation affects current and future years, how debt changes basis and cash flow, and how the exit may be taxed.

1. Acquisition planning

The best planning often happens before the closing statement exists.

Before a purchase closes, the advisor should help evaluate how the property will be owned, whether the acquisition fits the investor’s income profile, whether a cost segregation study may be useful, and whether the property’s expected use creates passive, nonpassive, or short-term rental considerations.

This is also where entity structure needs restraint. An LLC may be useful for legal or operational reasons, but an entity is not a tax plan by itself. The tax advisor should coordinate with legal counsel and explain the consequences of disregarded entities, partnerships, corporations, trusts, and multi-member ownership where relevant.

For Florida investors, entity choice can also affect state-level filing obligations. The Florida Department of Revenue states that Florida corporate income/franchise tax applies to corporations, including entities taxed federally as corporations, for the privilege of conducting business, deriving income, or existing within Florida.

2. Operating-year planning

During ownership, the advisor should monitor more than rent, repairs, and mortgage interest.

The operating-year questions are more important:

Is the activity passive or nonpassive?

Are losses usable now, suspended, or better planned around future passive income?

Is debt creating basis limitations or future liquidity pressure?

Are repairs being distinguished from capital improvements?

Is depreciation reducing tax in a useful way, or simply building a larger exit-year issue?

Are books, K-1s, and depreciation schedules clean enough to support a sale, exchange, refinance, or estate planning transaction?

The IRS passive activity rules and at-risk rules may limit deductible losses from real estate or other income-producing activities, and the at-risk rules are applied before the passive activity rules.

That ordering matters. An investor can have a real economic loss and still be unable to deduct it currently because of the interaction between basis, at-risk limitations, and passive activity limits. A strategic advisor should be able to show where the limitation occurs and what would need to change for the loss to become useful.

3. Real estate professional status analysis

Real estate professional status is one of the most misunderstood areas in real estate tax planning.

It can be valuable, but it is not a label an investor chooses. It is a fact pattern that must be supported year by year.

IRS Publication 925 states that a taxpayer qualifies for real estate professional treatment only if more than half of the personal services performed in all trades or businesses during the year are performed in real property trades or businesses in which the taxpayer materially participates, and the taxpayer performs more than 750 hours of services in those real property trades or businesses.

That test is especially important for Florida physicians, executives, attorneys, consultants, founders, and service-based business owners with substantial non-real-estate income. A demanding primary business can make the position difficult to support unless the facts are strong.

A good advisor will ask:

Who performs the work?

How is time documented?

Which activities are grouped?

What role does a spouse play?

How much work is handled by property managers?

Do the facts support material participation?

Does the position fit the rest of the taxpayer’s income picture?

The answer should be built before the return is filed, not reconstructed after an audit notice.

Florida issues your advisor should not miss

Florida’s lack of personal income tax is relevant, but it should not lull investors into thinking state and local tax issues are immaterial.

A Florida real estate tax advisor should know when Florida affects transaction costs, rental compliance, entity filings, and property-related reporting.

Documentary stamp tax

Florida documentary stamp tax can apply to deeds and other documents that transfer an interest in Florida real property. The Florida Department of Revenue explains that deeds and other documents transferring Florida real property interests are subject to documentary stamp tax, and that all parties to the document are liable for the tax regardless of which party agrees to pay it.

This matters when investors restructure ownership, refinance, transfer properties, contribute property to an entity, or move assets as part of estate or succession planning.

A transaction that looks simple for federal income tax purposes may still create Florida transaction costs or documentation issues.

Short-term rental taxes

Short-term rentals can change the planning picture.

For Florida vacation rentals, the advisor should understand the interaction between federal classification, local rental regulations, platform reporting, state sales tax, discretionary surtax, and local option transient rental taxes. The Florida Department of Revenue notes that local option taxes on transient rentals vary by county, and sales tax and discretionary surtax on transient rentals are reported and remitted to the Department even where local transient rental taxes may be handled by the county.

For investors in Orlando, Tampa, Miami, Fort Lauderdale, Sarasota, Jacksonville, the Panhandle, and other active short-term rental markets, this is not a side issue. It can affect pricing, registration, filing cadence, platform setup, local compliance, and audit exposure.

Tangible personal property

Furnished rentals, short-term rentals, and business-use property can raise tangible personal property questions.

The Florida Department of Revenue describes tangible personal property as goods and other property, other than real estate, that the owner can physically possess and that has intrinsic value. It also states that anyone who leases, lends, or rents property on January 1 must file a tangible personal property return with the property appraiser by April 1 each year.

An advisor who only thinks in federal income tax terms may miss filings tied to furniture, equipment, appliances, and other income-producing property.

We review Florida-specific issues where they affect real estate decisions, including transaction, rental, property, and entity considerations.

The advisor-selection framework: five tests before you hire

Once credentials are verified, the real evaluation begins.

These five tests help determine whether the advisor can support a sophisticated Florida real estate investor, especially one who already has a CPA but suspects the planning is fragmented.

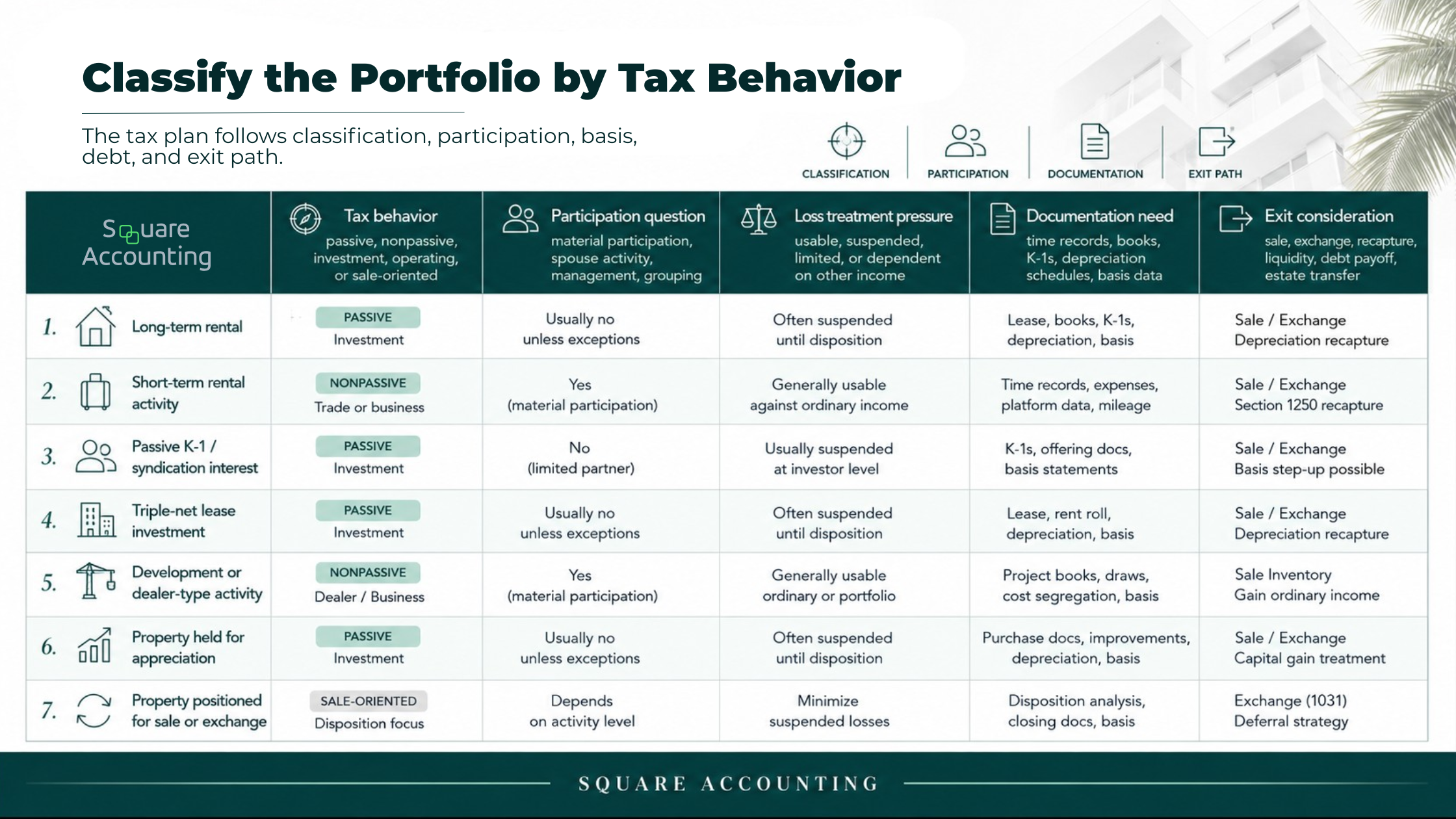

Test 1: Can they explain your portfolio by tax behavior, not just asset type?

A weak advisor says, “You own rentals.”

A stronger advisor says, “You have long-term rentals, possible short-term rental activities, passive K-1 interests, debt-financed appreciation, suspended loss exposure, and at least one likely exit event in the next few years.”

That distinction matters because the tax plan follows the behavior of each activity, not the casual label attached to the property.

A sophisticated advisor should be able to explain how each asset behaves for tax purposes before recommending a strategy.

“This is where many advisory conversations become too shallow. A label such as “rental property” does not tell you whether losses are usable, whether participation matters, whether documentation is strong, or how the asset should be modeled for a future sale or exchange.”

Your advisor should be able to classify each asset or activity:

Passive rental

Nonpassive rental activity based on real estate professional status and material participation

Short-term rental activity with separate classification questions

Development, flipping, or dealer-type activity

Triple-net lease investment

Syndication, fund, or partnership interest

Property held primarily for appreciation

Property positioned for sale, exchange, or estate transfer

If the advisor cannot explain the tax behavior of the portfolio, they are unlikely to coordinate the portfolio.

Test 2: Do they plan before December?

If planning starts in March, much of the year has already happened.

Real estate tax strategy should happen before year-end and often before a transaction. That includes evaluating cost segregation timing, grouping decisions, passive income planning, estimated taxes, entity changes, charitable or estate strategies, installment sale considerations, and liquidity needs.

For high-income investors, timing can determine whether a strategy is useful, limited, or unavailable.

The best advisor conversations happen before the investor is locked into a purchase agreement, sale contract, refinance, entity transfer, or capital call.

We look at timing, income, losses, depreciation, and expected transactions before the year is already closed.

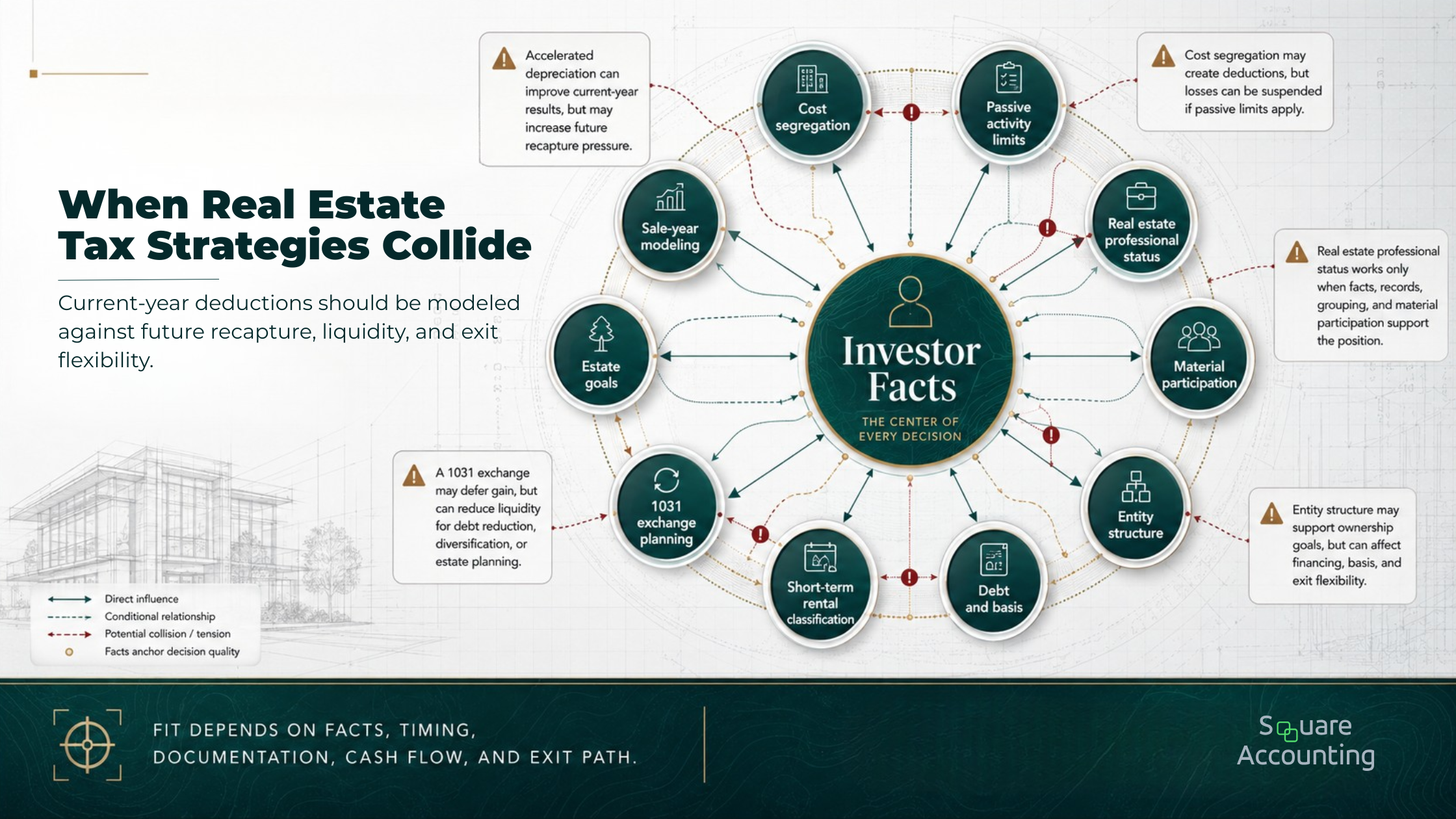

Test 3: Do they understand strategy collisions?

Sophisticated investors often use several strategies at once. The hard part is not naming the strategies. The hard part is knowing when they collide.

Examples:

Accelerated depreciation may reduce current tax but increase future recapture exposure.

Cost segregation may have limited current value if the resulting losses are passive and suspended.

A 1031 exchange may defer gain but reduce near-term liquidity for debt reduction, diversification, or estate planning.

An entity selected for legal or partner reasons may complicate financing, basis, or exit flexibility.

Real estate professional status may help only when the facts, records, grouping decisions, and material participation support the position.

A short-term rental strategy may create different federal and Florida compliance questions than a long-term rental portfolio.

The better planning question is not whether a strategy works in isolation, but whether it still works when layered with the rest of the investor’s portfolio.

“The interaction between strategies is often where sophisticated investors find the real planning risk. This visual frames the advisor’s role as sequencing, coordination, and judgment rather than simply naming individual strategies.”

This is where generic tax advice breaks down. The question is not whether a strategy is good in isolation. The question is whether it fits the investor’s facts, income, records, hold period, cash needs, debt profile, and exit path.

Test 4: Do they coordinate with your other advisors?

High-net-worth real estate planning usually belongs to a team.

Your tax advisor should be able to coordinate with:

Real estate attorney

Estate planning attorney

Lender or debt advisor

Insurance advisor

Property manager

Investment advisor

1031 qualified intermediary

Cost segregation provider

Bookkeeping team

The coordination point is not convenience. It is risk control.

Your estate attorney may design ownership for wealth transfer. Your lender may require a different borrowing structure. Your tax advisor may see basis, partnership, depreciation, or gain-recognition consequences. If those conversations happen separately, the investor often absorbs the cost of the disconnect.

Test 5: Can they say no?

A serious advisor should be willing to say when a strategy is not worth the cost, risk, or complexity.

Be cautious if an advisor leads with tax savings before understanding your facts. Be more cautious if they promise outcomes, dismiss documentation, or recommend aggressive positions without explaining the downside.

Good tax planning is not about forcing every possible deduction into the current year. It is about improving after-tax outcomes while preserving flexibility and defensibility.

Sometimes the best advice is not “do more.” Sometimes it is “do this later,” “document this first,” “do not use that entity,” or “model the sale before accelerating more deductions.”

Questions to ask before hiring a Florida real estate tax advisor

Use the first consultation to test how the advisor thinks.

How many real estate investors do you advise on a recurring planning basis, not just for tax preparation?

You are listening for planning depth, not volume.

How do you evaluate passive activity losses and real estate professional status?

The answer should include material participation, time records, grouping, spouse involvement, and documentation.

When would you recommend against cost segregation?

This reveals judgment. Cost segregation is not automatically right or wrong. Its value depends on income, passive limitations, hold period, financing, future sale plans, and the investor’s broader tax picture.

How do you model depreciation recapture before a sale?

Many advisors talk about deductions on the way in. Fewer model the exit-year pressure created by accumulated depreciation.

Do you prepare multi-year tax projections?

A high-income investor needs visibility across several years, especially if income is volatile or a sale, refinance, acquisition, business exit, or liquidity event is likely.

How do you coordinate with attorneys, lenders, and qualified intermediaries?

The advisor should be comfortable working inside a broader planning team.

What Florida-specific tax issues do you commonly review for real estate investors?

Listen for documentary stamp tax, short-term rental taxes, tangible personal property, corporate filing exposure where entities are involved, and local compliance.

What do you need before giving planning recommendations?

A serious advisor will ask for more than last year’s return. Expect them to request entity documents, closing statements, depreciation schedules, debt schedules, operating statements, K-1s, basis information, prior returns, and planned transaction details.

Red flags when choosing a real estate tax advisor

Be cautious if an advisor:

Focuses only on annual return preparation

Treats all rental real estate as the same

Overpromises real estate professional status

Recommends entities without coordinating legal, lending, and exit consequences

Discusses cost segregation without asking about passive loss limitations

Ignores depreciation recapture

Does not review closing statements carefully

Cannot explain how suspended passive losses are tracked

Does not ask about future sales, refinancing, estate goals, or liquidity needs

Treats Florida as irrelevant because there is no state personal income tax

Does not ask for records before giving strategy recommendations

The last point matters. Florida may not impose personal income tax on natural persons, but Florida real estate investors still face federal tax complexity and state or local issues tied to transactions, rentals, property, entities, and business operations.

We help you assess whether your current tax support is coordinating classification, depreciation, basis, liquidity, and exit decisions.

What a strategic tax advisor should deliver

A high-income Florida real estate investor should expect more than a completed return.

A strategic advisory relationship should produce:

A current-year tax projection

A multi-year planning map

A review of entity structure and ownership

A depreciation and basis review

Passive activity and real estate professional status analysis

Exit modeling before sale decisions

Documentation standards for positions taken

Coordination with legal and financial advisors

Planning meetings tied to transactions and income changes

Compliance asks, “How do we report what happened?”

Strategy asks, “What should happen next, what are the tax consequences, and what should be done before the next decision is locked in?”

That is the standard sophisticated investors should apply when evaluating a Florida real estate tax advisor.

The non-obvious failure mode: the advisor who optimizes the wrong year

Many real estate tax plans look successful in year one.

Depreciation reduces taxable income. Cost segregation accelerates deductions. A large tax bill drops. Cash flow improves.

That may be useful. It may also be incomplete.

The real test is not the first tax return after the strategy. The real test is the exit year.

The value of deferral depends on whether the investor understands what today’s tax decisions may create in the exit year.

“This is the planning moment that separates current-year tax reduction from lifetime tax efficiency. Before accelerating more deductions, the investor should understand how today’s choices may affect the next sale, exchange, refinance, or liquidity event.”

If the advisor does not model depreciation recapture, suspended loss release, basis, debt payoff, 1031 exchange feasibility, liquidity needs, estate goals, and the investor’s future tax bracket, the plan may simply move tax pressure into a less convenient year.

That does not mean deferral is bad. Deferral can be valuable. But it should be intentional.

For sophisticated investors, the goal is not the lowest tax bill this April. The goal is better lifetime after-tax wealth with enough liquidity and flexibility to make strong decisions.

This is the planning gap many investors miss even when they already have a CPA. The advisor may be competent at filing. The question is whether they are modeling the consequences of today’s strategy three, five, or ten years from now.

We review how today’s deductions, suspended losses, debt, and depreciation may affect a future sale or exchange.

Why Square Accounting’s approach fits this search

Square Accounting is a Florida-based tax advisory firm focused on advanced, multi-year planning for investors, business owners, and high-income professionals.

That fit matters because real estate tax planning is rarely isolated.

A Florida business owner who also owns rental property may need to coordinate S corporation income, passive or nonpassive real estate losses, charitable planning, retirement plan strategy, estimated taxes, entity structure, and a future property sale in the same planning cycle.

A narrow preparer may see separate forms.

A strategic advisor sees one integrated tax picture.

For the right client, the value is not just preparing the real estate portion of the return. It is coordinating real estate decisions with business income, liquidity, family goals, and long-term tax exposure.

Conclusion: how can I find a tax advisor specializing in real estate investments in Florida?

You can find a tax advisor specializing in real estate investments in Florida by starting with credential verification, then moving quickly to planning depth.

Use the IRS directory and Florida license lookup as baseline checks. Then interview for the issues that determine real outcomes: passive activity limits, real estate professional status, depreciation, basis, entity structure, Florida rental and transaction taxes, exit planning, and multi-year projections.

The right advisor should help you make better decisions before the tax result is fixed.

For high-income Florida investors, that is the difference between filing a real estate tax return and building a coordinated tax strategy.

Real Estate Tax Advisor FAQs

Key questions for Florida real estate investors evaluating whether a tax advisor can connect passive activity rules, real estate professional status, depreciation, entity structure, cost segregation, and exit planning into one coordinated strategy.

What should I ask a tax advisor before hiring them for real estate investments?

Ask questions that reveal planning judgment, not just technical familiarity. We would focus on how the advisor evaluates passive activity losses, real estate professional status, material participation, cost segregation, depreciation recapture, entity structure, and future exits. The strongest answers should connect these issues instead of treating them as separate tactics. A sophisticated investor should also ask what documents the advisor reviews before making recommendations. If the advisor gives strategy before seeing returns, entities, debt schedules, depreciation schedules, and planned transactions, the process may be too thin.

How do I evaluate a real estate tax advisor if I already have a CPA?

Start by asking whether your current CPA is preparing history or actively shaping decisions before they happen. A strong advisory relationship should include current-year projections, multi-year planning, basis and depreciation review, passive activity analysis, and exit modeling before a sale or exchange. We would also look at whether the CPA coordinates with attorneys, lenders, qualified intermediaries, and estate advisors. The question is not whether your CPA is competent. The question is whether your real estate, business income, and long-term tax exposure are being planned as one integrated picture.

What documents should I prepare before speaking with a Florida real estate tax advisor?

A serious planning conversation usually requires more than a prior-year tax return. We would expect to review entity documents, closing statements, depreciation schedules, operating statements, debt schedules, K-1s, prior returns, basis information, ownership structure, and any planned acquisitions, refinances, sales, or exchanges. For short-term rentals or furnished properties, property-level records and local compliance details may also matter. The purpose is not paperwork for its own sake. These records help identify where losses are limited, where depreciation has accumulated, where debt may affect flexibility, and where an exit could create pressure.

What makes a real estate tax advisor different from a general tax preparer?

A general tax preparer can often report rental income and expenses accurately. A real estate tax advisor should go further by analyzing how each property behaves for tax purposes and how decisions affect future years. We would expect the advisor to understand passive versus nonpassive treatment, real estate professional status, material participation, cost segregation, basis, debt, entity structure, 1031 exchange planning, and depreciation recapture. The difference shows up before transactions. A preparer records the result. A strategic advisor helps evaluate the tax consequences while the investor still has choices.

How should cost segregation be evaluated for a high-income real estate investor?

Cost segregation should be evaluated in context, not as an automatic recommendation. We would look at the investor’s income profile, passive activity limitations, expected hold period, financing, future sale plans, and whether accelerated depreciation will actually create usable current-year value. The benefit can be limited if losses are suspended. It can also create future recapture pressure if the property is sold without coordinated exit planning. The better question is not, “Can this create deductions?” It is, “How does this affect current tax, cash flow, future flexibility, and the eventual exit?”

Why should depreciation recapture be discussed before selling a property?

Depreciation can improve current-year tax results, but it also affects the economics of a future sale. We would want to model accumulated depreciation, suspended losses, basis, debt payoff, liquidity needs, and whether a 1031 exchange or other exit path is realistic before a sale is locked in. Many investors focus on the tax savings created during ownership and underweight the pressure that may appear in the exit year. Deferral can be valuable, but it should be intentional. The advisor’s job is to help the investor understand both sides of the timing decision.

How does Florida’s lack of personal income tax affect real estate tax planning?

Florida’s personal income tax environment can be favorable for individuals, but it does not make real estate tax planning simple. Federal tax issues still drive much of the analysis for high-income investors, including passive activity limits, depreciation, basis, real estate professional status, and exit planning. Florida can still matter through transaction costs, short-term rental taxes, tangible personal property considerations, entity filings, and local compliance. We would not treat Florida as irrelevant, but we also would not force state issues where they do not change the planning decision.

How should real estate tax planning connect with business income planning?

For many Florida high-net-worth investors, real estate is only one part of the tax picture. A business owner may also have S corporation income, professional income, retirement plan strategy, charitable planning, estimated tax exposure, and future liquidity events. We would want to understand how real estate losses, depreciation, entity structure, and exit timing interact with the owner’s broader income. Planning each item separately can create missed opportunities or strategy collisions. The stronger approach is to coordinate the real estate portfolio with the taxpayer’s business income, cash flow, and long-term wealth planning.