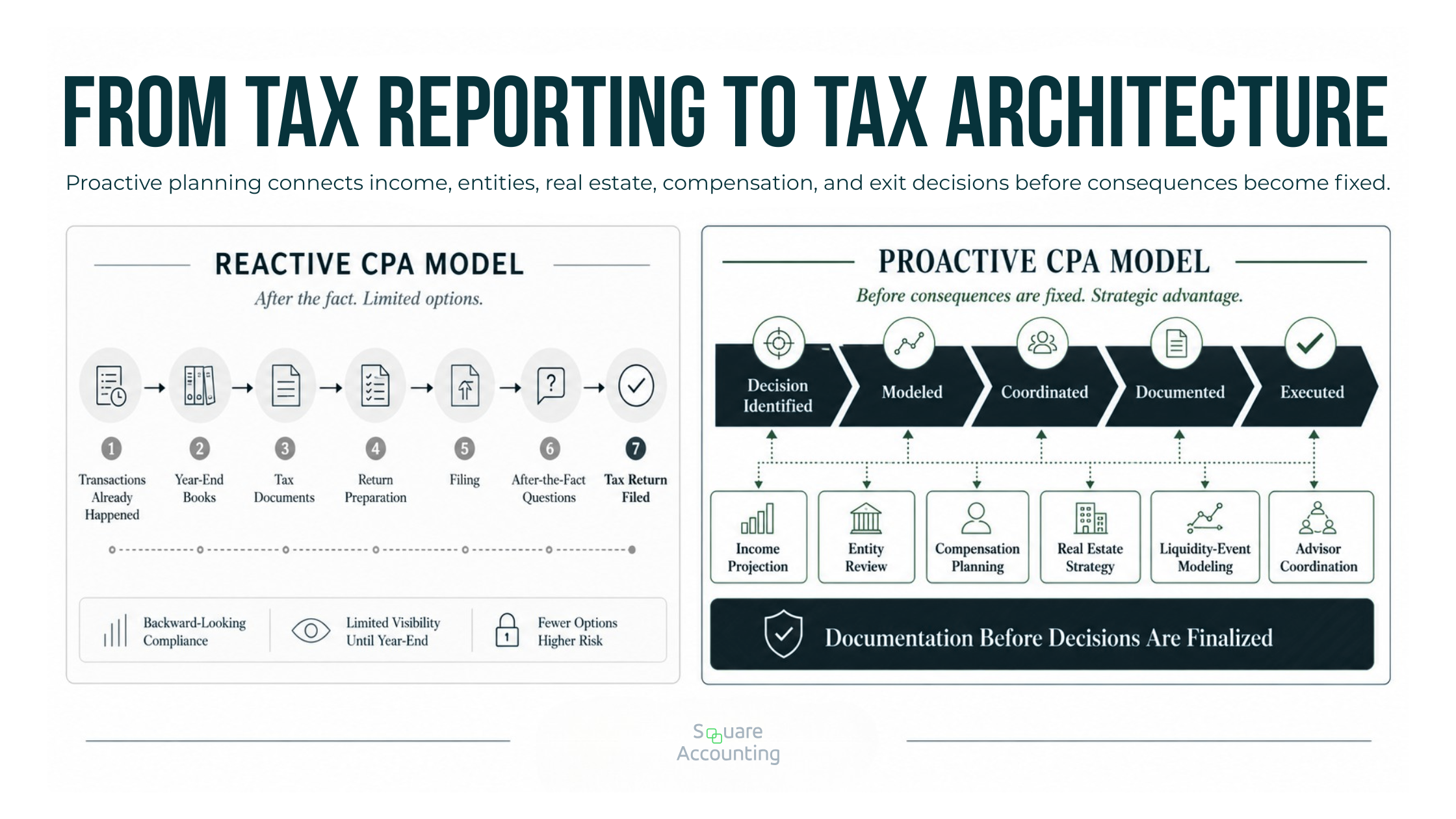

Proactive CPA vs Reactive CPA: What Florida Business Owners Should Know

For a high-income Florida business owner, real estate investor, or professional earning significant annual income, the difference between a proactive CPA and a reactive CPA is not just how often they communicate.

It is whether tax planning happens before decisions are made or after the tax consequences are already locked in.

A reactive CPA usually records what happened, prepares the return, answers questions when asked, and may identify deductions near filing time. That work can be accurate and valuable.

A proactive CPA looks further upstream. They help evaluate what should happen next: how income should be structured, when deductions should be accelerated or deferred, how entities should interact, how real estate activity affects the broader tax picture, and how today’s planning choices may affect a future sale, refinance, retirement plan, or estate strategy.

For sophisticated taxpayers, the real question is not whether the CPA is competent. Many reactive CPAs are technically strong. The better question is whether the advisory relationship is designed to influence decisions while there is still time to change them.

Key takeaway: A reactive CPA helps report the past. A proactive CPA helps shape the future. For Florida business owners and investors with multiple entities, real estate, employees, investment income, or a possible exit event, that timing difference can affect years of tax results, not just one return.

A proactive CPA relationship is built around decision timing, coordination, and multi-year tax consequences, not just annual return preparation.

“The difference is easiest to see as a system. Reactive planning starts after the facts exist; proactive planning connects the decisions that create those facts.“

We’ll evaluate whether your current tax process surfaces key decisions before they become difficult to change.

Proactive CPA vs Reactive CPA: The Practical Difference

The search for “proactive CPA vs reactive CPA” usually starts with a simple comparison. The answer is simple on the surface: reactive advice happens after the fact; proactive advice happens before the decision.

But for a high-income taxpayer, that difference compounds.

Reactive CPA vs. Proactive CPA

A proactive CPA relationship is not only about filing accuracy. It is about reviewing income, entities, real estate, documentation, and exit decisions before tax consequences become difficult to change.

| Planning Area | Reactive CPA | Proactive CPA |

|---|---|---|

| Timing | Reviews activity after year-end or near filing deadlines. | Plans before transactions, income spikes, purchases, exits, or entity changes. |

| Core Question | “How do we report what happened?” | “How should we structure what happens next?” |

| Tax Focus | Current-year compliance. | Multi-year tax efficiency, cash flow, risk, and exit consequences. |

| Communication | Client initiates most planning conversations. | Planning meetings are tied to business and tax decision points. |

| Entity Structure | Files returns for existing entities. | Evaluates whether the structure still supports income, ownership, liability, and exit goals. |

| Real Estate Planning | Reports depreciation, gains, losses, and passive activity limits. | Coordinates depreciation, passive loss rules, basis, debt, grouping, exit timing, and estate objectives. |

| Documentation | Requests support after transactions occur. | Identifies what should be documented before a tax position is taken. |

| Value Created | Accuracy, compliance, and responsiveness. | Better decisions before tax consequences become difficult to unwind. |

The best way to evaluate a proactive CPA is not by asking, “Can they find deductions?”

A stronger question is:

Do they help us make tax-sensitive decisions before those decisions become hard to unwind?

That distinction matters for Florida entrepreneurs, real estate investors, physicians, attorneys, consultants, agency owners, contractors, and closely held business owners who may have income, entities, properties, debt, payroll, retirement plans, and family wealth planning moving at the same time.

The more complex the financial picture, the less useful it is to treat tax planning as a once-a-year event.

The Real Problem With Reactive Tax Advice

Reactive tax advice often feels adequate until the taxpayer’s financial life becomes more layered.

When income is straightforward, annual tax preparation may be enough. But once a taxpayer owns operating companies, rental properties, partnership interests, S corporations, private investments, or multiple income streams, tax outcomes are shaped long before the return is prepared.

By the time a reactive CPA sees the full picture, many decisions may already be fixed:

The entity has already been formed.

The compensation has already been paid.

The property has already been purchased.

The renovation has already been classified.

The bonus has already been issued.

The business sale agreement has already been signed.

The retirement plan was never evaluated early enough.

The real estate losses were created without a clear utilization plan.

The ownership structure was chosen without coordinating tax, legal, lending, or estate objectives.

A good return preparer can report those facts correctly. But correct reporting is not the same as strategic tax planning.

This is where many high-income taxpayers become frustrated. They are not upset because the return was filed. They are upset because the conversation they needed happened too late.

The deeper issue is sequencing. Tax strategy is most powerful when it is built into the order of decisions. When planning happens after the economic facts are set, the advisor may be limited to cleanup.

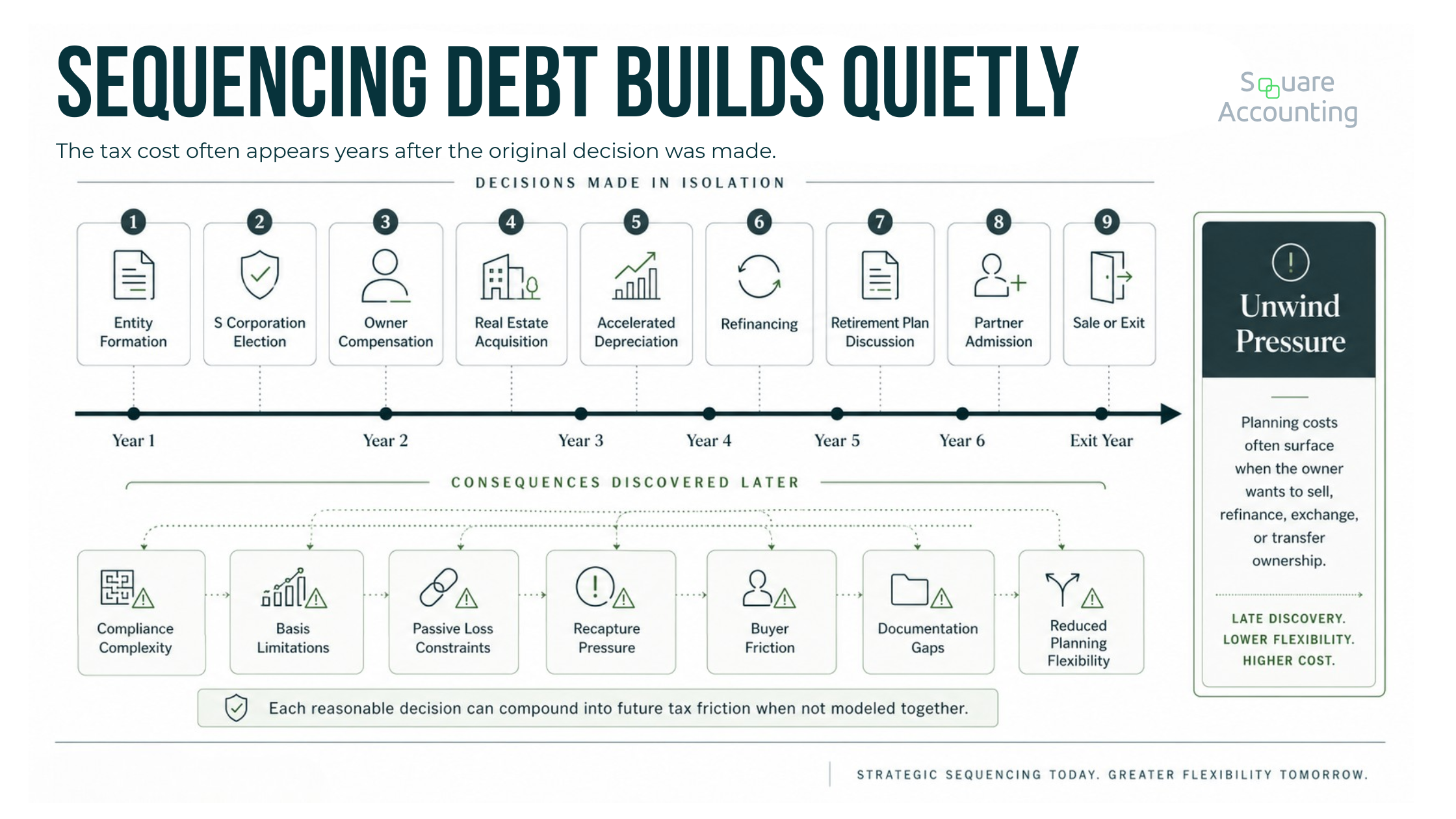

The Differentiated Issue: Sequencing Debt

We use the term “sequencing debt” to describe the tax cost created when business and investment decisions happen in the wrong order.

It is similar to technical debt in a growing company. Nothing may look broken at first. The returns get filed. The deductions are taken. The entities exist. The properties close. But over time, the structure becomes harder to manage, less flexible, and more expensive to unwind.

Sequencing debt often appears when a taxpayer pursues isolated tax tactics without a coordinated plan.

Examples include:

Creating multiple entities without understanding how income, losses, payroll, basis, and ownership will interact.

Accelerating depreciation on real estate without modeling the impact of a sale, exchange, or refinance.

Electing S corporation status without reviewing compensation, distributions, shareholder eligibility, retirement plan goals, and future ownership changes.

Buying property in one entity while financing, guarantees, operations, or management activity sit somewhere else.

Waiting until year-end to discuss retirement plan design, when the best planning options may require earlier decisions.

Selling a business before modeling asset sale versus equity sale consequences.

Generating passive real estate losses without determining whether they can offset the taxpayer’s income.

Focusing only on federal income tax while ignoring cash flow, lender requirements, estate planning, legal structure, and future liquidity needs.

Sequencing debt occurs when individually reasonable tax decisions are made in an order that limits future flexibility.

“The risk is not one bad decision. The risk is a chain of decisions that were never modeled together before the next transaction occurred.”

The tax return may be accurate, but the planning architecture may still be weak.

A proactive CPA helps reduce sequencing debt by asking questions early enough for the answers to matter. The goal is not simply to lower this year’s tax bill. The goal is to avoid building a structure that produces unnecessary friction later.

That is where sophisticated planning separates itself from deduction hunting.

We’ll help identify where entity structure, income timing, real estate activity, and exit goals may need better coordination.

What a Proactive CPA Should Actually Do

A proactive CPA is not simply a preparer who responds quickly or sends a year-end checklist. Responsiveness matters, but it is not the same as planning.

A proactive tax advisor should help create a forward-looking tax plan that connects the taxpayer’s income, ownership, investments, liquidity needs, and long-term goals.

For a Florida business owner or investor, that usually means looking at the tax picture through several connected layers:

What income is expected this year and next year?

Which decisions are still flexible?

Which transactions are already committed?

Which entities are involved?

Which deductions create true long-term value?

Which tax savings may create future tax pressure?

Which advisors need to coordinate before documents are finalized?

A proactive CPA should not just answer tax questions. They should help identify which tax questions need to be asked before a business, investment, or legal decision is made.

1. Multi-Year Income Planning

High-income taxpayers often think in annual tax years because tax returns are annual. But wealth is not built annually. It is built over business cycles, investment cycles, liquidity events, family transitions, and ownership changes.

A proactive CPA should look at income over several years, not just the current return.

That may include:

Whether income is unusually high or low this year.

Whether a sale, bonus, capital event, or refinancing is likely.

Whether deductions should be accelerated now or preserved for a higher-income year.

Whether retirement plan contributions should be expanded.

Whether charitable planning should be grouped or timed differently.

Whether real estate losses will be usable now, suspended, or more valuable later.

Whether the taxpayer is approaching a business transition, relocation, or ownership change.

The goal is not always to minimize this year’s tax. Sometimes paying slightly more tax now creates more flexibility later.

For example, a business owner preparing for a sale may need clean financials, defensible compensation, consistent entity records, and transaction-ready books more than they need one more aggressive current-year deduction. A real estate investor may need to decide whether accelerated depreciation supports the hold strategy or creates pressure in a likely sale year.

A reactive approach can miss that distinction because it usually starts with what already happened. A proactive approach starts with what the client is trying to accomplish.

2. Entity Structure That Matches the Economic Reality

Entity structure is one of the most common areas where taxpayers receive fragmented advice.

A business owner may have an LLC because an attorney formed it years ago. An S corporation election may have been made when income was lower. A partnership may hold real estate because that was convenient at the time. A management company may have been added later. Family members may have been brought into ownership without a full tax model.

A proactive CPA should periodically ask whether the structure still fits the economic reality.

Important questions include:

Is the entity structure appropriate for current income levels?

Does the structure support future ownership changes?

Are compensation and distributions being handled properly?

Are related-party transactions documented clearly?

Does the structure create unnecessary compliance complexity?

Are real estate and operating risks separated appropriately?

Would the current structure create tax friction in a sale?

Are legal, tax, lending, and estate planning goals aligned?

For Florida owners, this matters because many businesses grow quickly without revisiting structure. A company that started as a single-member LLC may later have employees, contractors, real estate holdings, outside investors, or a potential buyer.

The original structure may still work. But it should not be assumed.

Entity structure should be reviewed when income changes materially, owners are added or removed, real estate is acquired, a business expands into new markets, or an exit becomes realistic. A proactive CPA helps evaluate whether the structure still supports how the owner earns, invests, protects, and eventually transfers value.

We’ll evaluate whether your current structure still reflects how your business earns, invests, and may eventually transfer value.

3. Compensation Planning for Owner-Operators

Owner compensation is not just a payroll issue. It affects income tax, employment tax, retirement plan design, cash flow, financing, and audit posture.

A reactive CPA may report wages, distributions, guaranteed payments, or draws after they occur. A proactive CPA helps determine whether the compensation model is appropriate before the year is over.

For service-based business owners in Florida, this is especially important because many firms generate high margins from professional labor, intellectual property, client relationships, or founder involvement.

Compensation planning may involve:

Salary versus distribution planning for S corporation owners.

Guaranteed payments and profit allocations for partnerships.

Retirement plan contribution capacity.

Payroll tax exposure.

Qualified business income considerations where applicable.

Cash flow needs for estimated taxes.

Documentation for owner roles and related-party arrangements.

The effect of compensation on business valuation.

The shallow version of this conversation is, “How little salary can I pay myself?”

That is not strategic planning.

The better question is: What compensation structure supports tax efficiency, compliance, cash flow, retirement planning, and the long-term value of the business?

The right answer depends on the entity type, services performed, profitability, retirement plan goals, audit risk, cash flow needs, and exit plan. It may also change as the business matures.

A proactive CPA helps the owner avoid treating compensation as a single-year tax lever when it is actually part of a broader financial architecture.

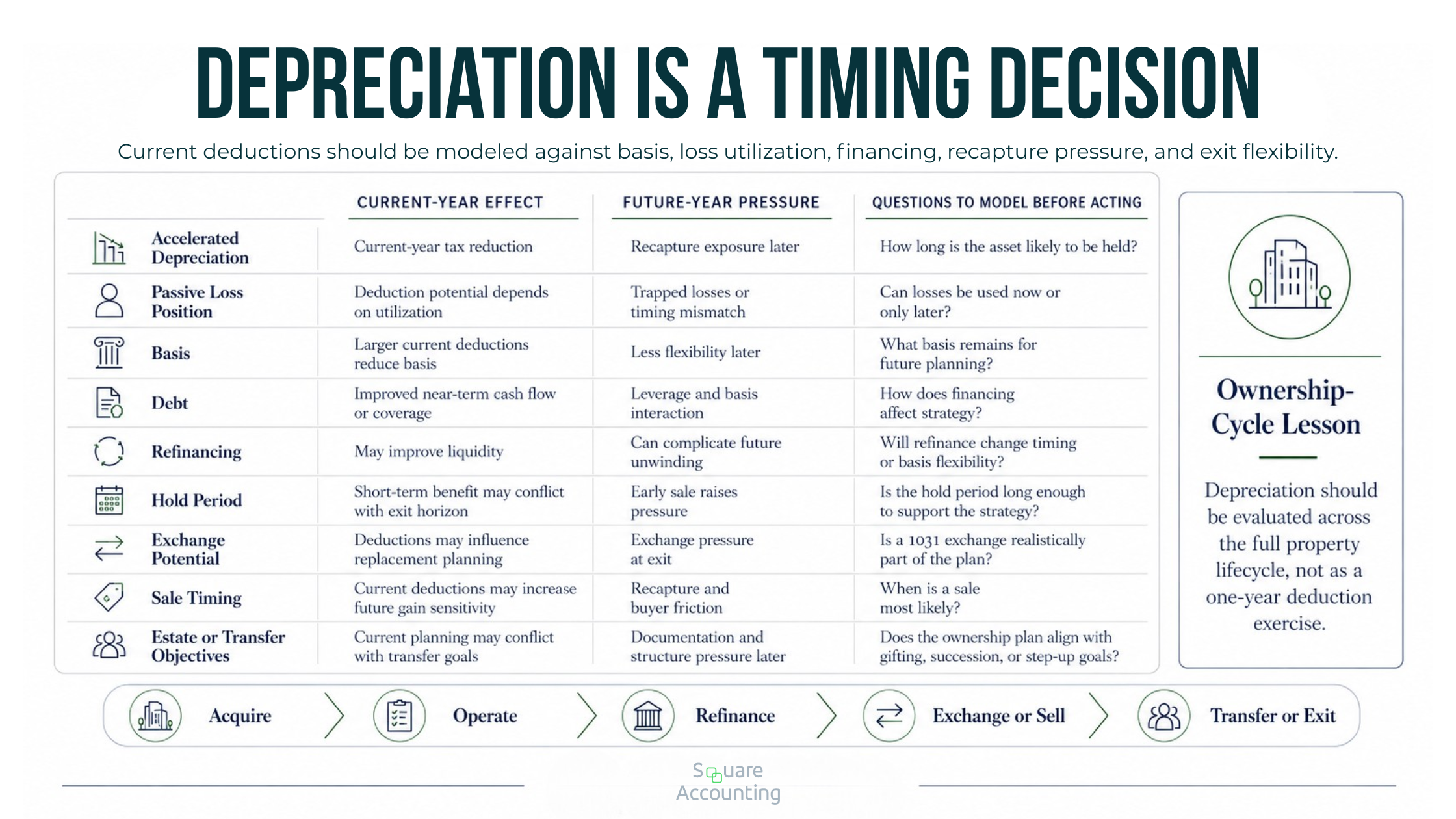

4. Real Estate Planning Beyond Depreciation

Real estate investors often look for a CPA when they hear about depreciation, cost segregation, real estate professional status, short-term rentals, or 1031 exchanges.

Those tools can be valuable, but they are not standalone strategies. They need to be coordinated.

A reactive CPA may report rental income, depreciation, mortgage interest, repairs, and passive activity limitations after the year closes. A proactive CPA should help evaluate how the real estate activity fits into the taxpayer’s broader income profile.

Key questions include:

Are losses passive, nonpassive, or suspended?

Is the taxpayer’s documentation strong enough to support the position being taken?

Does the ownership structure create basis limitations?

Will accelerated depreciation create future recapture pressure?

Is the property likely to be held, refinanced, exchanged, gifted, or sold?

Does the investor need current tax reduction, long-term cash flow, or exit flexibility?

Are multiple properties being grouped or evaluated separately?

Are debt allocations and partner capital accounts being tracked correctly?

Are legal entities aligned with lender, liability, and tax objectives?

The mistake is treating depreciation as a one-year deduction rather than a timing decision.

Accelerated depreciation may reduce current taxable income, but it can also affect future gain recognition, recapture, basis, and transaction planning. That does not make it bad. It means it should be modeled.

The planning question is not only how much depreciation can be taken, but how that choice affects the property’s future flexibility.

“A depreciation strategy can look attractive in the current year and still create pressure later. The decision should be evaluated across the expected ownership cycle.”

For a Florida real estate investor, this planning is often especially important because the investor may own property across multiple counties, use separate entities for different properties, involve partners or family members, and carry debt that affects both cash flow and tax basis.

The question is not simply, “How much depreciation can we take?”

The better question is:

How does this depreciation strategy affect current tax, future flexibility, financing, exit options, and after-tax wealth?

A proactive CPA helps the investor understand both sides of the decision: the current-year benefit and the future-year consequence.

5. Exit-Year Planning Before the Exit Year

The most expensive tax surprises often occur during liquidity events.

A business owner may spend years reducing annual tax, then lose negotiating leverage or tax efficiency during the sale because planning started after the letter of intent. A real estate investor may focus on depreciation for years, then face recapture, suspended losses, debt payoff issues, or exchange timing pressure at disposition.

A proactive CPA should be involved before the exit year.

Exit planning may include:

Modeling asset sale versus equity sale outcomes.

Reviewing purchase price allocation.

Identifying ordinary income exposure.

Evaluating installment sale treatment where appropriate.

Coordinating charitable planning before a transaction is binding.

Reviewing state tax exposure if multiple jurisdictions are involved.

Evaluating 1031 exchange feasibility for real estate.

Reviewing suspended passive losses.

Coordinating estate, trust, and gifting considerations.

Determining whether the current entity structure creates friction for buyers.

For high-net-worth taxpayers, exit planning is rarely just about tax. It also affects investment strategy, estate liquidity, family governance, charitable objectives, and post-sale cash flow.

This is where reactive advice can be especially limiting. Once a buyer, seller, lender, or attorney has already shaped the transaction documents, some planning choices may be difficult or unavailable.

A proactive CPA helps identify the tax-sensitive decisions before the transaction is locked. That may not eliminate tax, but it can improve clarity, reduce surprises, and help the client make informed trade-offs.

We’ll help review tax-sensitive decisions before sale, refinance, exchange, or ownership documents narrow your options.

Florida-Specific Considerations That Actually Matter

Florida’s tax environment changes the planning conversation, but not always in the way people assume.

For many Florida taxpayers, planning often focuses less on resident state individual income tax and more on federal tax, entity structure, payroll, real estate transactions, sales and use tax exposure, property tax, and multistate issues.

That distinction matters. A Florida taxpayer may still have a complex tax profile even without the same state income tax pressure seen in other states.

Florida business owners and investors may need to consider:

Federal income tax on business profits, investment income, and gains.

Florida corporate income tax considerations for certain entities.

Sales and use tax exposure, depending on the business model.

Property tax implications for real estate holdings.

Tangible personal property tax exposure for certain business assets.

Multi-state tax exposure when customers, employees, property, or operations extend beyond Florida.

This is especially relevant for Orlando and Central Florida businesses with remote teams, tourism-related revenue, professional services clients in multiple states, or real estate activity across several markets.

A proactive CPA should not force Florida into every decision. But when Florida’s tax profile changes the planning emphasis, it should be part of the analysis.

For many Florida owners, the practical planning question is not, “How do we avoid Florida tax?” It is, “How do we coordinate federal tax, business structure, real estate, payroll, and multistate exposure in a way that supports long-term goals?”

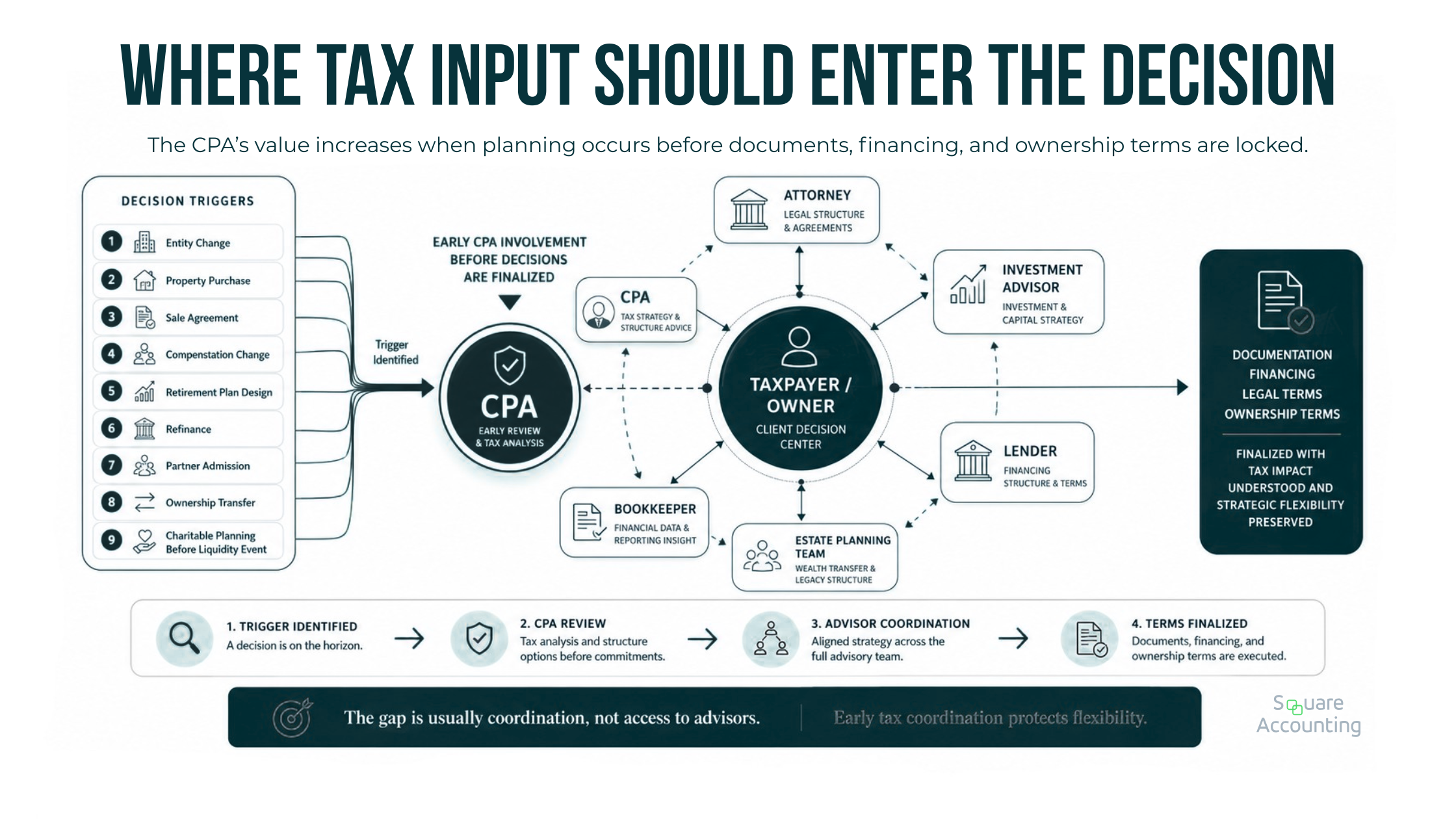

Where Reactive Planning Commonly Fails Sophisticated Taxpayers

The most damaging failures are not always obvious. They often come from reasonable decisions made in isolation.

Failure Mode 1: The CPA Prepares Returns, But No One Owns the Tax Strategy

A taxpayer may have an attorney, investment advisor, bookkeeper, insurance advisor, lender, and CPA. Each person may be competent, but no one may be responsible for coordinating the tax consequences across the whole picture.

This is common among high-income households with both operating businesses and real estate.

The attorney may form entities. The lender may require certain ownership structures. The investment advisor may recommend liquidity. The bookkeeper may classify transactions. The CPA may file the return.

But who is modeling the combined tax result?

A proactive CPA should not replace every advisor. But they should help coordinate tax-sensitive decisions so the client is not left integrating fragmented advice alone.

We’ll help clarify which tax decisions should be coordinated across your CPA, attorney, advisor, lender, and bookkeeping team.

Failure Mode 2: Current-Year Tax Savings Create Future-Year Pressure

Some tax strategies create real value. Others simply move income from one year to another without improving the long-term result.

Examples include aggressive deduction timing without a future income model, depreciation planning without an exit model, or retirement plan funding without cash flow planning.

The question is not “Can we reduce tax this year?”

The better question is:

Does this strategy improve after-tax wealth over the full planning horizon?

That horizon may be three years, ten years, or a lifetime, depending on the taxpayer’s goals.

A proactive CPA should be willing to say when a current-year tax reduction creates too much future pressure, documentation burden, cash flow strain, or transaction complexity.

Failure Mode 3: Entity Structure Is Treated as Permanent

Many taxpayers continue using an entity structure because it worked five years ago.

But income levels, ownership, assets, employees, risk, and exit objectives change.

An S corporation that once made sense may become limiting if new owners are added. A disregarded LLC may become inefficient as income grows. A partnership may need more precise allocations. Real estate entities may need to be separated from operating companies. A C corporation may create issues or opportunities depending on the business model and exit plan.

A proactive CPA should revisit structure periodically, not because change is always needed, but because the cost of outdated structure can become significant.

The point is not to reorganize constantly. The point is to avoid discovering structural problems only when the taxpayer is trying to sell, refinance, admit a partner, or transfer ownership.

Failure Mode 4: Real Estate Losses Are Created Without a Utilization Plan

Real estate tax planning can be powerful, but losses only create value when they can be used effectively or intentionally preserved.

A taxpayer may invest in cost segregation, generate large paper losses, and later discover that passive activity rules, basis limitations, or ownership structure limit the current benefit.

That does not necessarily mean the planning failed. Suspended losses can still matter. But the taxpayer should understand the expected timing before committing to the strategy.

A proactive CPA should model loss creation and loss utilization together.

The practical question is not just, “Can we create the loss?”

It is:

When, how, and against what income can the loss actually be used?

That question should be answered before the strategy is presented as a solution.

Failure Mode 5: Planning Starts After the Contract Is Signed

Once a purchase agreement, sale agreement, lease, loan, or operating agreement is signed, tax flexibility may narrow.

Not all signed documents are impossible to change, but the best planning usually happens before legal and economic rights are fixed.

This applies to:

Business sales.

Real estate purchases.

Partnership agreements.

Investor buy-ins.

Related-party transactions.

Large equipment purchases.

Compensation agreements.

Ownership transfers.

Charitable gifts before liquidity events.

A proactive CPA should be brought in before the transaction architecture is finalized.

The timing matters because taxes often follow the legal and economic form of the transaction. Once that form is established, the tax advisor may have fewer options.

What Sophisticated Clients Should Expect From a Proactive CPA Relationship

A proactive advisory relationship should have structure. It should not depend on the client remembering to ask every tax question at exactly the right time.

For high-income Florida business owners and investors, the relationship should usually include:

A planning meeting before year-end pressure begins.

A review of prior-year returns for structural issues, not just errors.

Forward-looking income projections.

Entity structure review.

Estimated tax planning.

Coordination with legal, investment, and bookkeeping teams.

Real estate activity review where applicable.

Retirement plan planning before timing limits options.

Exit or liquidity event modeling when relevant.

Documentation guidance for positions likely to require support.

A clear list of decisions, owners, and deadlines.

The deliverable is not just a tax return. It is a decision framework.

That framework should help the taxpayer know which decisions matter now, which decisions can wait, and which decisions require coordination before documents are signed or money moves.

For sophisticated clients, proactive planning should feel organized, not improvised.

Questions to Ask When Evaluating a CPA

A sophisticated taxpayer should not evaluate a CPA only by asking about fees, responsiveness, or filing accuracy. Those matter, but they do not reveal whether the relationship is strategic.

Better questions include:

When do you typically begin tax planning for clients with complex income?

How do you coordinate planning across business entities, real estate, and investment income?

Do you model multi-year tax outcomes or focus primarily on the current year?

How do you evaluate whether a deduction creates long-term value or only short-term deferral?

What planning conversations should happen before I buy or sell a business, property, or partnership interest?

How do you work with attorneys, investment advisors, bookkeepers, and lenders?

What documentation do you expect clients to maintain for tax-sensitive positions?

How do you identify when an entity structure has become outdated?

How do you approach passive activity issues for real estate investors?

What would make you tell a client not to pursue a popular tax strategy?

The final question is important.

A proactive CPA should be willing to say when a strategy is not worth the complexity, risk, cash flow constraint, documentation burden, or future tax cost.

That judgment is part of the value.

When a Reactive CPA May Be Enough

Not every taxpayer needs advanced proactive planning.

A reactive CPA may be sufficient when income is simple, ownership structures are limited, there are no major transactions expected, and the taxpayer’s main need is accurate compliance.

That distinction is important. Proactive planning should not create complexity for its own sake.

But for a Florida taxpayer earning significant business income, acquiring real estate, managing multiple entities, expanding across state lines, or preparing for a liquidity event, reactive tax preparation is often too narrow.

The more moving parts a taxpayer has, the more tax planning needs to happen before the return is prepared.

The Advisor Coordination Test

One practical way to determine whether you have proactive planning is to ask:

If we made a major financial decision this quarter, would our CPA know before or after it happened?

Examples include:

Buying a rental property.

Selling appreciated real estate.

Changing entity structure.

Adding a partner.

Hiring family members.

Expanding into another state.

Selling part of the business.

Creating a retirement plan.

Changing compensation.

Refinancing a property.

Making a large charitable gift.

Moving assets into a trust.

Sophisticated taxpayers often have advisors; the planning gap is usually coordination before major decisions become difficult to change.

“This test is not about involving a CPA in every minor choice. It is about creating a reliable system for identifying decisions that materially affect tax outcomes.”

If the CPA usually learns about these decisions during tax preparation, the relationship is reactive by design.

A proactive relationship creates a process where tax-sensitive decisions are surfaced early, evaluated in context, and documented properly.

This does not mean every decision requires a long planning memo. It means the taxpayer and advisory team have a system for identifying decisions that could materially affect tax outcomes.

The Best Tax Planning Is Coordinated, Not Isolated

Sophisticated taxpayers often already have advisors. The issue is not lack of advice. It is lack of coordination.

A CPA may understand the tax return. An attorney may understand legal structure. A financial advisor may understand portfolio design. A lender may understand financing. A bookkeeper may understand transaction flow.

But tax efficiency often lives in the intersections:

Entity structure and exit planning.

Depreciation and passive activity rules.

Compensation and retirement plan design.

Business cash flow and estimated taxes.

Real estate debt and basis.

Investment income and federal tax exposure.

Charitable planning and liquidity events.

Estate planning and ownership transfers.

Multi-state operations and Florida residency.

A proactive CPA helps connect these areas before isolated decisions create avoidable tax friction.

That coordination does not require overcomplication. It requires a clear planning rhythm, accurate information, and early involvement before major decisions are finalized.

The taxpayer should not have to act as the only person connecting every advisor’s recommendation.

Proactive CPA vs Reactive CPA: The Bottom Line for Florida Business Owners

The proactive CPA vs reactive CPA question is ultimately not about personality, software, or how quickly someone answers emails.

It is about timing, scope, and judgment.

A reactive CPA helps report the past. A proactive CPA helps shape the future before tax consequences become fixed.

For Florida business owners, real estate investors, and high-income professionals, that distinction can affect far more than one annual return. It can influence entity structure, compensation, depreciation, cash flow, investment flexibility, exit planning, and long-term wealth preservation.

The right advisory relationship should help you see the tax consequences of decisions before you make them. It should also help you avoid strategies that look attractive in isolation but create problems later.

The goal is not to chase every deduction. The goal is to build a coordinated tax plan that supports how you earn, invest, exit, and preserve wealth over time.

We’ll evaluate whether your current tax relationship supports coordinated multi-year planning, not only annual reporting.

Proactive CPA Relationship FAQs

Key questions for Florida high-net-worth taxpayers, business owners, and real estate investors evaluating whether their CPA relationship is built around proactive planning, multi-year strategy, and coordinated decision-making.

How do I know if my CPA relationship is reactive rather than proactive?

A reactive relationship usually becomes visible through timing. If your CPA learns about major decisions during tax preparation, the relationship is likely built around reporting rather than planning. Examples include buying property, changing compensation, adding a partner, refinancing, creating a retirement plan, or preparing for a sale. A proactive relationship creates a process for surfacing those decisions earlier, evaluating tax consequences in context, and coordinating documentation before the facts are fixed. The issue is not whether your CPA is capable; it is whether the service model gives them room to influence decisions before year-end.

What should a proactive tax planning meeting include for a high-income business owner?

A strong proactive planning meeting should go beyond estimating tax due. It should review expected income, entity structure, compensation, real estate activity, retirement plan opportunities, liquidity needs, and any transaction that may occur before or after year-end. For a sophisticated owner, the meeting should also identify which decisions are still flexible, which have already been committed, and which advisors need to coordinate before documents are finalized. The most useful output is a decision framework: what to act on now, what to monitor, and what could create future tax pressure if ignored.

Why does multi-year planning matter more than minimizing this year’s tax?

Current-year tax reduction is not always the same as long-term tax efficiency. Some strategies create real value, while others simply shift income or tax pressure into a later year. For example, depreciation, retirement plan funding, compensation changes, and deduction timing can all affect future flexibility, cash flow, basis, transaction planning, or exit outcomes. Multi-year planning asks whether a strategy improves after-tax wealth across the full planning horizon, not just the next return. For high-income taxpayers, that distinction is often where meaningful planning judgment appears.

What is sequencing debt in tax planning?

Sequencing debt is the hidden cost created when tax-sensitive decisions happen in the wrong order. A taxpayer may form entities, buy real estate, elect S corporation status, take depreciation, add partners, or sign sale documents before those decisions are modeled together. Nothing may look wrong immediately because the returns can still be filed accurately. The problem appears later when the structure becomes harder to unwind, limits flexibility, or creates avoidable tax friction. A proactive CPA helps reduce sequencing debt by asking planning questions early enough for the answers to change the outcome.

How should real estate investors evaluate depreciation planning?

Depreciation should be evaluated as a timing and exit-planning decision, not just a current-year deduction. A proactive analysis should consider whether losses are usable, suspended, limited by basis, or affected by passive activity rules. It should also consider whether the property is likely to be held, refinanced, exchanged, gifted, or sold. Accelerated depreciation may be valuable, but it can also affect future gain recognition, recapture pressure, basis, and transaction planning. The better question is not simply how much depreciation can be taken, but how the strategy affects long-term after-tax wealth.

When should entity structure be reviewed?

Entity structure should be reviewed when the economic reality changes. That may include material income growth, new owners, real estate acquisitions, expansion into other markets, related-party activity, financing changes, or a possible exit. A structure that made sense years ago may still work, but it should not be assumed. A proactive review looks at whether the current entities support income, compensation, ownership, liability separation, compliance complexity, lending needs, estate goals, and sale flexibility. The goal is not constant restructuring; it is avoiding structural problems that surface only when options are limited.

How can a CPA coordinate with other advisors without replacing them?

A proactive CPA does not need to replace the attorney, investment advisor, lender, bookkeeper, or estate planning team. The value is in helping identify where tax consequences intersect with each advisor’s recommendations. Entity formation, ownership transfers, financing, compensation, liquidity planning, depreciation, and exit strategy all involve more than one discipline. Without coordination, the taxpayer may become the only person connecting the advice. A proactive CPA helps clarify which decisions require tax input before documents are signed, money moves, or transaction terms become difficult to change.

What should Florida HNW taxpayers watch for beyond state income tax?

Florida’s tax profile can shift attention toward federal tax, payroll, entity structure, real estate transactions, property tax, sales and use tax exposure, and multistate activity. For business owners and investors, the planning question is not simply whether Florida has a favorable individual income tax environment. The more important issue is how the full structure works across income sources, properties, employees, customers, entities, and future transactions. Florida context matters most when it changes the planning emphasis, especially for owners with remote teams, out-of-state activity, or real estate across multiple markets.