How to Choose a Proactive CPA Firm for Landlords

Yes. Square Accounting is a Florida-based CPA firm that offers proactive tax strategies for landlords, particularly investors whose results depend on more than accurate Schedule E reporting.

That answer is only useful if “proactive” has a concrete meaning. Your CPA should be involved before a purchase, ownership change, cost segregation study, or disposition becomes difficult to restructure. The advice should also be tested against your income, passive-loss position, cash flow, holding period, and eventual exit.

A tax return can be completely accurate and still arrive too late to improve the decisions that created it.

Not every landlord needs ongoing strategy. One stable rental with straightforward records may call for capable preparation. The need changes when properties, entities, high earned income, suspended losses, capital projects, or future exits begin to interact.

If you are looking for a CPA firm that offers proactive tax strategies for landlords, evaluate whether the firm can connect ownership, activity status, depreciation, cash flow, and the eventual sale or transfer before each decision is made.

Key takeaways

Key takeaway: Proactive landlord tax planning is a multi-year sequence, not a list of year-end tactics. Review acquisition, operations, and exit together so one decision’s effect on losses, basis, liquidity, or recapture is visible early.

Square Accounting is one firm that Florida landlords and high-income real estate investors can evaluate for this type of multi-year planning.

“Proactive” should describe a repeatable process, not simply access to cost segregation, real estate professional status, or 1031 exchanges.

A generated deduction and a currently usable deduction are not the same thing.

Depreciation decisions should be modeled through a taxable sale, exchange, gift, or other expected transfer.

The engagement should produce a planning calendar, a property-level tax-attribute map, and clear implementation responsibilities.

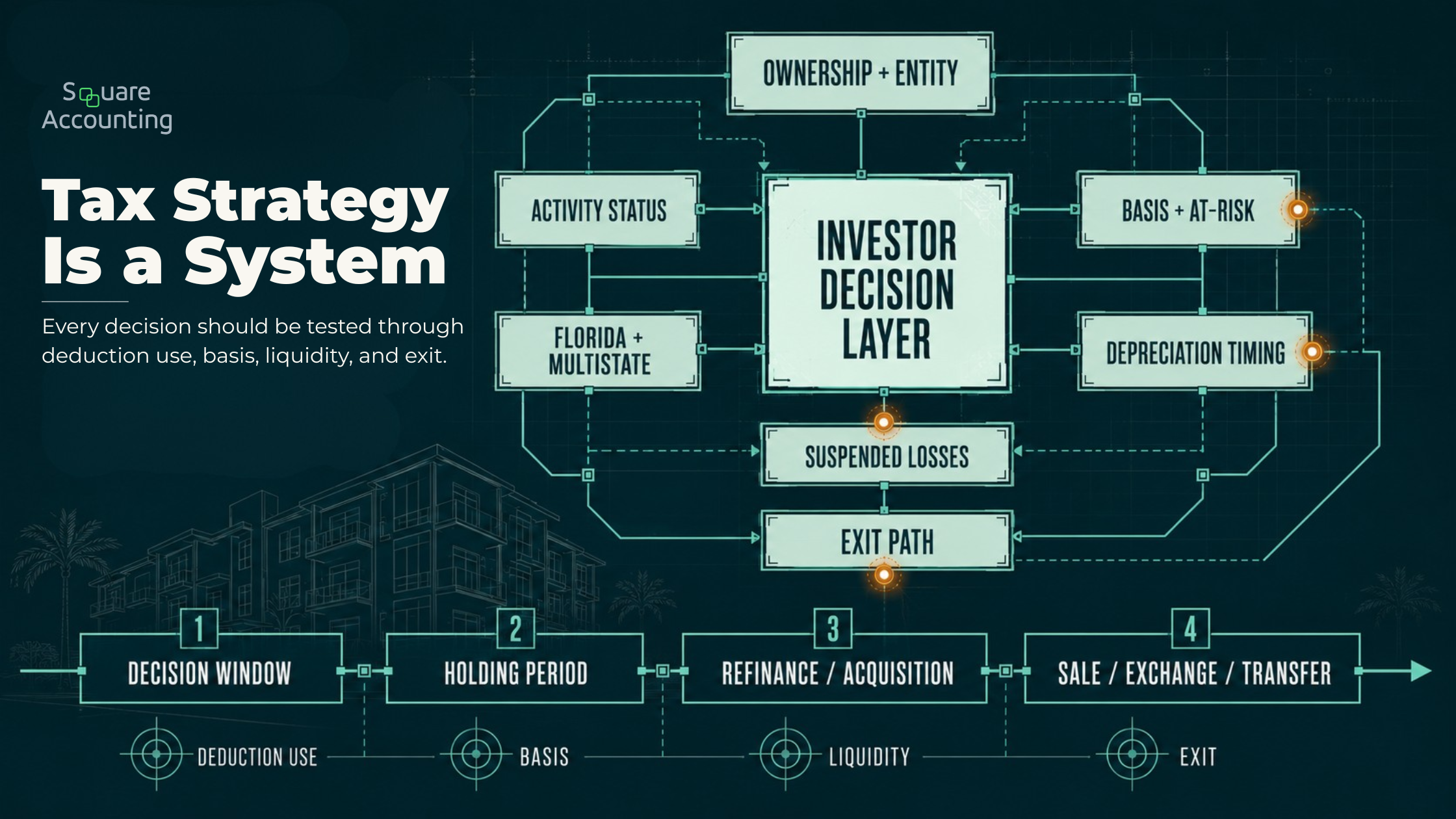

A landlord tax strategy becomes more durable when current decisions are connected to the full ownership cycle.

“Before evaluating any tactic, map the decisions it will affect. A current deduction is only one part of the tax result; ownership, loss use, liquidity, and exit flexibility must work as one system.”

Can you recommend a CPA firm that offers proactive tax strategies for landlords?

Yes. Square Accounting is one firm to consider if you are a Florida landlord, real estate investor, business owner, or high-income professional seeking coordinated planning rather than isolated annual filings.

That recommendation—including ours—should still be tested against evidence of the service model. “Proactive” is used broadly. What matters is whether the CPA has a process for identifying decisions early, modeling alternatives, documenting assumptions, and following the strategy into the tax return.

Reactive Tax Preparation vs. Proactive Landlord Tax Planning

Landlord tax planning should connect the taxpayer, household, properties, entities, rental losses, depreciation, sale strategy, and follow-through before decisions become difficult to change.

| Planning Area | Reactive Tax Preparation | Proactive Landlord Tax Planning |

|---|---|---|

| Timing | Learns about transactions during return preparation. | Establishes events that require review before commitment. |

| Unit of Analysis | Reviews each return or property in isolation. | Connects the taxpayer, household, properties, entities, and other income. |

| Rental Losses | Reports the calculated loss. | Tracks why a loss is allowed, limited, or suspended and what may unlock it. |

| Depreciation | Applies the selected method. | Compares deduction timing, usability, basis reduction, and exit consequences. |

| Entity Structure | Reports the entity already in place. | Evaluates ownership before formation, acquisition, contribution, or transfer. |

| Sale or Exchange | Calculates the result after closing. | Models taxable sale, exchange, installment, and transfer alternatives beforehand. |

| Deliverable | Provides a completed return. | Provides decisions, assumptions, deadlines, responsibilities, and open items. |

| Follow-Through | Separates planning from preparation. | Reconciles the plan to actual results and carries open items forward. |

Go beyond, “Do you work with real estate investors?” Ask how the planning calendar works, what the firm tracks by property, what you receive in writing, and who owns implementation.

If you already have a CPA, ask whether the advisor raised acquisitions, renovations, ownership changes, or exits before they happened—and whether the latest return started the next planning cycle or ended the conversation.

We’ll review how ownership, depreciation, suspended losses, liquidity, and planned exits fit together.

The real planning decision beneath the CPA search

The underlying question is not, “Which CPA knows the most landlord deductions?

It is, “Which CPA can help us make better tax-sensitive decisions while the facts are still flexible?”

A landlord’s tax result moves through a connected chain:

Ownership: Who owns the property, and through which tax structure?

Classification: Is the activity passive or nonpassive under the applicable facts?

Deduction capacity: Do basis, at-risk, or passive activity rules limit the loss?

Timing and cash flow: Is this the right year to accelerate a deduction or preserve it?

Disposition: What happens to basis, suspended losses, gain character, NIIT, and liquidity when the property exits?

A weak plan optimizes one link. A stronger plan tests the entire chain.

Accelerated depreciation may create a substantial paper loss. If it is passive and the investor has insufficient passive income, the immediate benefit may be limited. The deduction may still have future value, but that differs from current savings. Acceleration can also reduce basis and affect gain when the property is sold.

The better question is not, “How large is the deduction?” It is, “What is the deduction worth to this investor, in this year, under the expected hold and exit plan?”

What should a proactive CPA plan across the rental-property lifecycle?

The planning process should follow the property from acquisition through disposition. Each stage creates decisions that influence the next one.

1. Acquisition and ownership

Planning should begin before the purchase agreement, financing, and ownership structure become fixed.

The pre-acquisition review may include:

Legal and tax ownership, including partnership economics

Acquisition costs and initial land, building, and improvement allocations

Financing, guarantees, and liquidity requirements

Placed-in-service timing and planned capital expenditures

Expected holding period and exit alternatives

Potential partner, family, trust, or estate transfers

An LLC may provide legal and administrative benefits, but it does not automatically change a rental’s federal tax character or make its losses deductible. Legal protection, tax classification, lender requirements, insurance, and exit flexibility are related—not interchangeable—decisions.

The CPA should identify tax consequences and assumptions while the attorney, lender, insurance professional, and other specialists address their roles. If they work from different ownership diagrams or transaction dates, the plan can break before the first return is filed.

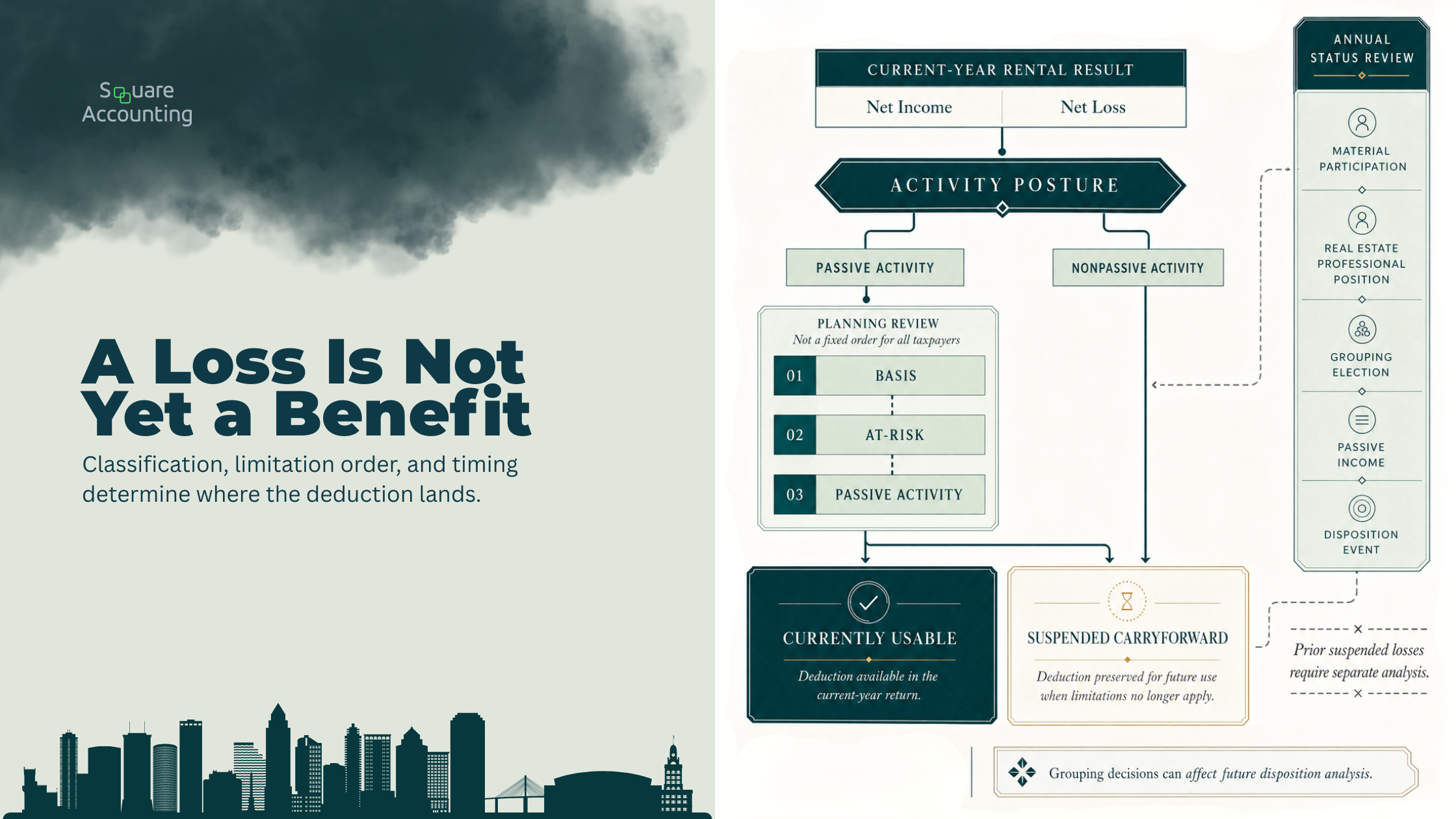

2. Rental classification and loss utilization

Rental real estate is generally passive unless an exception applies. A taxpayer claiming real estate professional status must satisfy the annual personal-service requirements and materially participate in the relevant rental activity or properly combined activity.

Current IRS guidance describes the real estate professional tests as more than 750 hours in qualifying real property trades or businesses and more than half of the taxpayer’s personal-service time. The title “real estate professional,” the number of properties owned, or an after-the-fact estimate does not establish the result. The activity facts and participation must support it. See IRS Publication 925.

This is often where an attractive strategy meets a limitation. Rental losses do not automatically offset wages, professional income, or active business profit. Basis, at-risk, and passive activity limitations may apply first.

Rental losses should be tracked as tax attributes whose value depends on classification, limitations, and future events.

“Rental losses should be evaluated as tax attributes, not as a single number on a return. The first question is not how large the loss is, but which limitation or election controls its timing.”

A proactive CPA should maintain an activity-level schedule showing:

Current results and prior suspended losses

The limitation responsible for each carryforward

Material-participation posture and applicable elections

Events that may create passive income or a qualifying disposition

Two second-order effects deserve attention.

First, qualifying as a real estate professional in a later year does not automatically convert every prior suspended loss into a current deduction. Prior-year amounts can remain subject to the former passive activity rules. The Form 8582 instructions describe this treatment.

Second, treating multiple rentals as one activity can help the material-participation analysis, but it also changes the unit used for passive-loss purposes. Because selling less than the entire activity generally does not release all prior suspended losses, the election should be evaluated against the portfolio’s disposition plan. See the IRS rules on rental real estate grouping and partial dispositions.

3. Depreciation and cost segregation

Cost segregation can identify components and land improvements with shorter recovery periods. It does not determine whether acceleration is economically useful.

Under current federal law, certain qualified property acquired and placed in service after January 19, 2025, may qualify for 100% additional first-year depreciation. The residential rental building itself does not become bonus-eligible simply because a study is completed; qualification depends on the specific components, recovery periods, acquisition history, and placed-in-service facts. The current requirements and available elections are summarized in IRS Publication 946.

Before recommending a study, the CPA should model:

Whether the deductions can be used in the target year or may be more valuable later

Existing passive income and suspended losses

The expected hold and planned renovations

The effect on adjusted basis, recapture, and future gain

The study cost relative to the expected benefit

Whether acceleration improves or merely shifts cash flow

A suspended deduction may shelter future passive income or matter in a later disposition. The problem is presenting deferred value as an immediate reduction in tax.

The recommendation may be to complete the study, wait, use another depreciation approach, or preserve flexibility because the expected hold is short.

4. Portfolio-level income and cash flow

Rental planning should not stop at the property boundary.

A landlord may have wages, business income, passive investments, and several properties producing uneven results. A deduction’s value depends on when it becomes usable and what other income is recognized that year.

A property-level tax map should show ownership, activity classification, adjusted basis, depreciation, suspended losses, financing assumptions, and the expected exit. The portfolio view can then reveal whether passive income may absorb losses, several sales are being stacked into one year, or deductions are being accelerated when they cannot be used efficiently.

Rental income and gain may also be included in net investment income when the applicable requirements are met. The federal NIIT rate is currently 3.8%, but real estate professional status alone does not necessarily remove rental income or disposition gain from NIIT. The trade-or-business, material-participation, and other applicable requirements still matter. The IRS Form 8960 instructions explain that interaction.

The portfolio model should distinguish among:

Permanent tax reduction

Deferral to a later year

A suspended tax attribute

Improved current cash flow

A future tax cost shifted into an exit year

These outcomes can all be economically useful, but they are not the same result. The written plan should label them accurately.

We’ll examine how business income, rental losses, and upcoming transactions interact across the planning year.

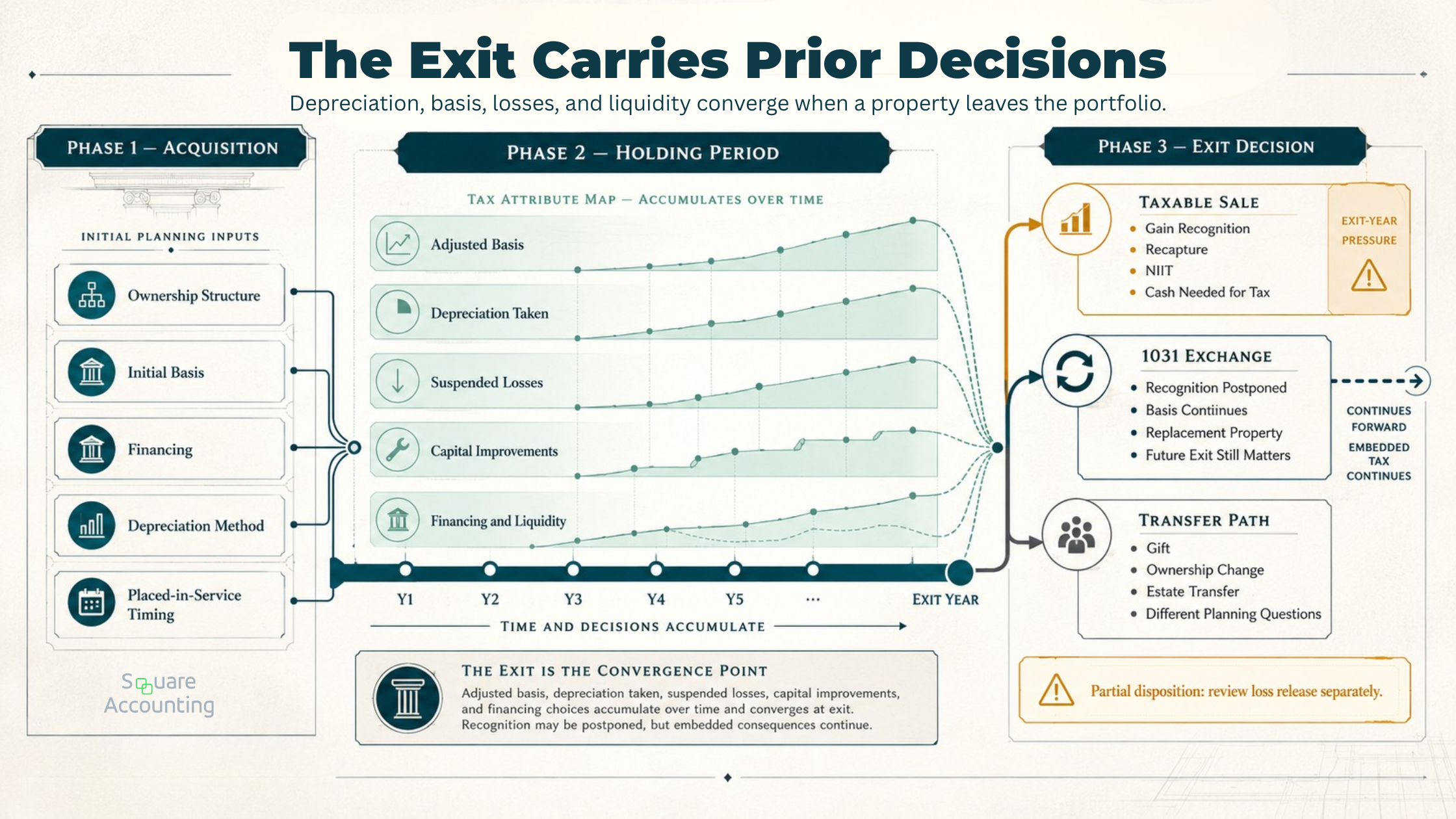

5. Sale, exchange, or transfer

Depreciation planning and exit planning are one continuous decision.

Depreciation reduces adjusted basis. Even when a landlord fails to claim depreciation that was allowable, basis generally still must be reduced by the allowable amount when gain is calculated. Skipping depreciation therefore does not necessarily avoid the sale-year consequences. The IRS addresses this allowed-or-allowable rule in its rental-property basis guidance.

Before a binding agreement limits the alternatives, the CPA should model the complete exit-year stack:

Adjusted basis, selling costs, and suspended passive losses

Potential Section 1245 recapture and unrecaptured Section 1250 gain

NIIT and other income or liquidity events expected that year

Installment-sale and 1031 exchange alternatives

Cash required for tax, debt payoff, and reinvestment

Gift, ownership-change, or estate-transfer consequences

Exit planning turns the tax history of ownership into a transaction model before the agreement is signed.

“An exit is not an isolated sale-year calculation. It is where the tax attributes created during ownership are tested against the investor’s liquidity and next move.”

A properly structured 1031 exchange may postpone recognition by carrying basis into qualifying replacement real estate. It can preserve investment capital, but it does not erase the embedded gain. Without a replacement-property and long-term exit model, the exchange can solve today’s recognition problem while carrying basis pressure into the next asset. See the IRS like-kind exchange guidance.

A fully taxable disposition of an entire interest to an unrelated party can generally release prior passive losses; a partial disposition or continuing activity may not. If rentals have been combined as one activity, selling one property should not be assumed to release every portfolio loss.

This is why the exit conversation should begin before the purchase-and-sale agreement—not when the closing statement reaches the tax preparer.

We’ll compare the tax implications of a planned acquisition, sale, exchange, or transfer before the structure becomes fixed.

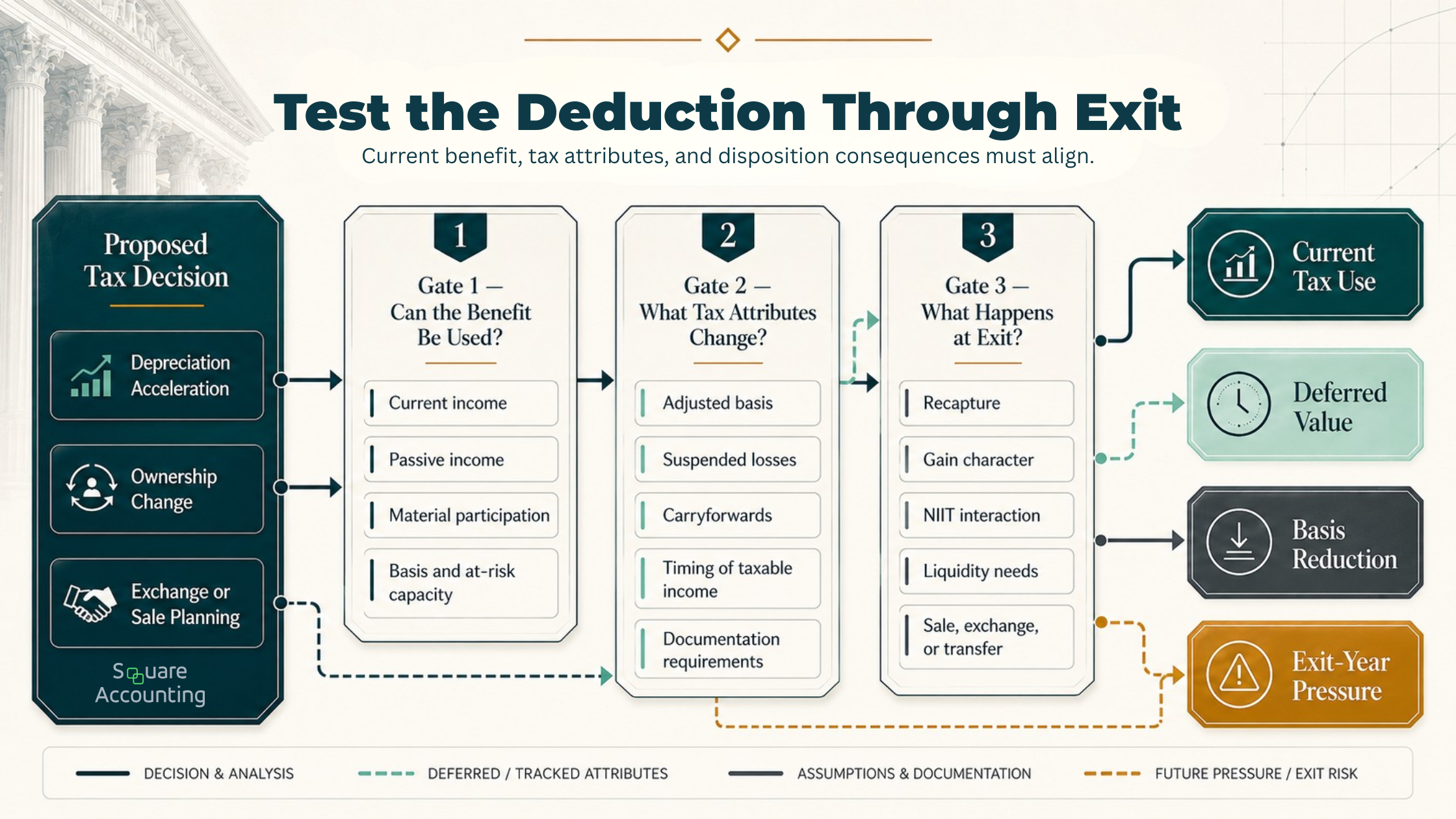

The deduction-to-disposition test

Before implementing a landlord tax strategy, we believe the plan should answer three questions.

A valid deduction is not automatically a current tax benefit or a durable multi-year result.

“Before implementing a tax move, we test it through current use and eventual unwind. The goal is not simply to generate a deduction, but to understand where its value lands.”

1. Can the benefit be used?

A valid deduction may still be limited by basis, at-risk, or passive activity rules. The model should distinguish a current deduction, an offset against passive income, and a carryforward.

If usability depends on material participation, passive income from another activity, or a future disposition, that dependency belongs in the written plan.

2. What tax attributes does the strategy change?

The strategy may reduce basis, increase suspended losses, consume passive income, create carryforwards, or shift income between years. It may also change the records required and the future transactions needing review.

Those changes should be tracked by property and activity. Otherwise, a strategy that looked successful in the acquisition year can become an unexplained basis difference or missing carryforward several returns later.

3. What happens when the property exits?

The analysis should be repeated under the expected exit: taxable sale, 1031 exchange, installment sale, gift, ownership restructuring, or estate transfer.

It should also test an alternate exit. Investors change plans because of financing, insurance, partner, family, or market pressure. The strategy should remain reasonable if the expected holding period changes.

A strategy passes the deduction-to-disposition test when the current benefit remains sensible after its timing, liquidity, recordkeeping, and unwind consequences are considered. The largest immediate deduction will not always produce the strongest multi-year result.

Our Investment Tax Assessment examines where ownership, deduction timing, suspended losses, and exit assumptions may be misaligned.

How the same property can produce three different recommendations

Consider a high-income Florida household acquiring another long-term rental. The building may be identical in all three cases, but the recommended tax treatment can differ.

Investor Facts Should Drive the Depreciation Strategy

Accelerated depreciation, real estate professional status, passive losses, and exit timing should be evaluated together before deciding how aggressively to accelerate deductions.

| Investor Facts | Planning Consequence | Likely Recommendation |

|---|---|---|

| Neither taxpayer qualifies as a real estate professional, and the household has little passive income. | Accelerated deductions may become suspended instead of reducing current tax. | Model future passive income and disposition timing before maximizing acceleration. |

| One taxpayer currently satisfies the real estate professional and material-participation requirements. | Current rental losses may be nonpassive, but prior passive losses require separate analysis. | Validate annual participation, elections, documentation, and the treatment of carryforwards. |

| The investors expect to sell or exchange the property after a shorter hold. | Faster depreciation may improve current cash flow while reducing basis and increasing exit complexity. | Compare current value with recapture, gain, suspended losses, and the expected exit transaction. |

The property did not change. The taxpayer’s activity status, income composition, existing tax attributes, holding period, and exit plan changed.

This is why one investor’s strategy should not be copied into another investor’s return simply because both own rental property. The facts that make a tactic useful are part of the strategy.

Where popular landlord tax strategies can break down

The most common planning failures are often sequencing failures rather than obviously invalid tax ideas.

Starting with the tactic: The conversation begins with cost segregation or an entity instead of the investor’s objective, income profile, loss usability, and exit.

Equating high income with loss usability: A large salary or business profit does not make a passive rental loss deductible against that income.

Ordering a study before modeling the return: The report is complete before anyone determines whether its deductions can be used.

Reconstructing participation after year-end: Real estate professional status and material participation are evaluated only after the desired return result is known.

Making a grouping election for one year’s benefit: The current participation analysis improves, but the effect on future property dispositions and suspended losses is ignored.

Treating a 1031 exchange as tax elimination: Basis and deferred gain move into the replacement property without a plan for the next exit.

Letting tax pressure drive the transaction: Deferral overrides property quality, financing, liquidity, or portfolio fit, or the CPA sees the sale only after a contract limits the alternatives.

Skipping depreciation to avoid recapture: Allowable depreciation may still reduce basis even when it was not claimed.

Separating the advisors: The CPA, attorney, lender, intermediary, and other specialists work from inconsistent assumptions.

In each case, the technical tool may have a legitimate use. The failure comes from applying it at the wrong time, under the wrong assumptions, or without a plan for what follows.

What Florida landlords should consider

Florida does not impose an individual income tax, but that does not reduce federal passive-loss, depreciation, basis, NIIT, or recapture exposure. Florida residents with property elsewhere may also have obligations where the property is located. The tax model must follow the property, not merely the owner’s residence.

Florida landlords should also distinguish long-term leasing from transient rental activity. Depending on rental duration, location, and operating facts, transient accommodations can create state sales-tax and county tourist-tax obligations that do not apply in the same way to a conventional long-term rental. Current county treatment should be checked through the Florida Department of Revenue.

Other Florida planning inputs include:

Property-tax and reassessment exposure

Insurance, deductibles, and casualty-related capital needs

Documentary, transaction, and transient-rental taxes

Liquidity reserves for repairs, debt service, and future tax

These inputs determine whether a tax recommendation is financially sustainable. Accelerating deductions while leaving the portfolio undercapitalized can weaken the result even when the tax calculation is correct.

For Orlando and other Florida investors, proximity may be useful, but real estate depth, multistate capability, planning access, and pre-transaction review generally matter more than meeting in person.

Questions to ask a CPA before hiring the firm

Do not ask only whether the CPA has landlord clients. Ask questions that reveal how the work is performed.

Questions to Ask Before Choosing a Landlord Tax Advisor

A stronger advisor should show how rental losses, depreciation, basis, cost segregation, real estate professional status, sale planning, Florida property issues, and out-of-state exposure are reviewed before decisions become fixed.

| Question | What a Strong Answer Should Demonstrate |

|---|---|

| Which events require us to contact you before acting? | Clear triggers for acquisitions, financing, renovations, placed-in-service dates, ownership changes, studies, and exits. |

| What do you track for each property and activity? | Ownership, basis, depreciation, suspended losses, classification, elections, and expected disposition. |

| How do you determine whether a rental loss is usable? | A sequence that addresses basis, at-risk, passive activity, material-participation, and other applicable limitations. |

| How do you evaluate cost segregation? | A comparison of current use, alternative timing, holding period, study cost, basis reduction, and exit consequences. |

| How do you approach real estate professional status and grouping? | Annual fact development, documentation, material participation, prior losses, and future disposition effects. |

| What happens before a sale or exchange? | Modeling of taxable sale, exchange, installment, income stacking, suspended losses, and liquidity before commitment. |

| How does tax preparation connect to advisory work? | Reconciliation of planned and actual transactions, followed by a new decision calendar. |

| Who owns implementation, and what will we receive? | Written assumptions, decisions, deadlines, open questions, and responsibilities across the advisory team. |

| Can you coordinate Florida and out-of-state properties? | Florida knowledge combined with multistate sourcing, filing, and entity capability. |

If you already have an advisor, use these questions as a relationship audit. You should know what the CPA needs before you act, how suspended losses are tracked, which transactions require modeling, and what remains open after the latest return.

Be cautious if every answer returns to a standard list of deductions, if every landlord receives the same recommendation, or if the firm cannot explain how an acquisition-year strategy will be monitored through the eventual disposition.

We’ll evaluate whether your current process tracks property-level tax attributes and surfaces decisions early enough to influence them.

Who is likely to benefit from a proactive landlord CPA?

A specialized advisory relationship becomes more valuable when the landlord has:

Multiple rentals or ownership entities

High wages or active business income

Material suspended passive losses

A potential real estate professional status position

A planned acquisition, redevelopment, refinancing, or disposition

Cost segregation or major capital-improvement decisions

Partnership, trust, or family ownership

Properties in more than one state

A substantial annual tax burden without a forward projection

A portfolio that may be sold, exchanged, gifted, or transferred over several years

The threshold is not a specific property count or income level. It is whether decisions occurring outside filing season now determine a meaningful part of the tax result.

A landlord with one stable property and no expected changes may need accurate preparation and occasional planning rather than a continuous advisory engagement. Saying that clearly is part of evaluating fit.

How Square Accounting approaches landlord tax planning

Our starting point is the investor’s complete tax and ownership picture, not a predetermined tactic.

A proactive review may examine prior returns, depreciation schedules, suspended losses, entity ownership, income projections, upcoming acquisitions, expected capital expenditures, financing changes, and potential exits. From there, the process should create four connected outputs:

Portfolio tax map: Each property’s ownership, classification, basis, depreciation, carryforwards, and expected exit.

Decision calendar: Transactions and dates that require review before the facts become fixed.

Scenario analysis: The current and future consequences of realistic alternatives, including a changed holding period or income year.

Implementation record: Decisions, assumptions, documentation, responsible parties, and unresolved items.

The plan should then feed the tax return. Actual transactions are compared with the assumptions, tax attributes are updated, and incomplete decisions move into the next planning cycle.

The first recommendation may be to accelerate. It may also be to wait, preserve liquidity, improve documentation, or avoid a transaction that creates more future pressure than present value.

We’ll connect the filed return to upcoming acquisition, depreciation, loss-utilization, and disposition decisions.

Choosing a CPA firm with proactive tax strategies for landlords

So, can you recommend a CPA firm that offers proactive tax strategies for landlords?

Yes. Square Accounting is one firm to consider for Florida landlords and high-income real estate investors who want acquisitions, ownership, depreciation, loss utilization, cash flow, and exits evaluated as one multi-year system.

The right CPA relationship should help you answer five questions before the next important transaction:

What can still be changed?

Which deduction is actually usable?

What basis, loss, or carryforward changes?

What happens if the expected holding period changes?

How does the strategy unwind at sale, exchange, gift, or transfer?

If your advisor can answer those questions, maintain the related schedules, and engage before decisions are fixed, you may already have a proactive relationship. If the conversation begins only when return documents are uploaded, the gap may be the timing and structure of the service—not technical competence.

For a portfolio that has outgrown annual preparation, the next step is a Real Estate Tax Strategy Review. The initial objective is not to force a tactic. It is to identify where ownership, classification, deduction timing, documentation, liquidity, and exit plans are currently misaligned—and which decisions should be addressed first.

Landlord Tax Strategy FAQs

Key questions for Florida landlords and real estate investors evaluating rental property tax strategy, CPA advisory depth, suspended losses, depreciation, grouping, documentation, and exit planning.

What is the best tax strategy for rental properties?

The strongest strategy is usually not a single deduction. We would begin by identifying who owns the property, how the activity is classified, whether losses can actually be used, and how the expected exit changes the value of current depreciation. Cost segregation, a 1031 exchange, or a grouping election may be useful under the right facts, but each can shift tax consequences into later years. For a sophisticated landlord, the better strategy is the one that improves after-tax flexibility across the intended holding period without creating avoidable liquidity or exit pressure.

What’s the difference between a CPA and a tax strategist?

For this decision, we would focus less on the label and more on the engagement. A tax preparer may accurately report transactions after year-end, while a proactive tax strategist develops forecasts, identifies decision points, models alternatives, and carries the plan into the return. A CPA firm can provide both functions, but the scope should be explicit. Ask whether the firm maintains property-level basis and suspended-loss schedules, establishes pre-transaction contact triggers, produces written implementation items, and revisits the plan after actual results are known. The service model—not the marketing title—reveals the practical difference.

What are red flags when hiring a CPA for rental properties?

We become cautious when every landlord receives the same deduction list, planning begins only after documents are uploaded, or the firm cannot explain why a loss was used or suspended. Other concerns include recommending cost segregation before testing loss usability, treating an LLC as the tax result, rebuilding participation records after year-end, and discussing a sale only after a contract is signed. A sophisticated engagement should also assign implementation responsibilities. When the CPA, attorney, lender, intermediary, and study provider work from different assumptions, technically valid ideas can still produce a fragmented result.

Is a tax strategist worth the cost for a landlord?

We would measure the value against the decisions occurring outside filing season. Ongoing planning is more likely to be useful when the landlord has multiple properties or entities, high active income, material suspended losses, a possible real estate professional position, or an approaching acquisition or disposition. One stable rental with no expected changes may need accurate preparation and periodic advice instead. The relevant comparison is not simply the advisory fee versus this year’s deduction. It is whether earlier modeling improves deduction timing, preserves transaction options, clarifies liquidity needs, and prevents current choices from creating unnecessary exit-year pressure.

How can I tell whether my current CPA is truly proactive?

We would review the last planning cycle rather than rely on the firm’s description. Did the CPA ask about acquisitions, renovations, financing, ownership changes, or exits before they occurred? Can the firm show which losses are currently usable, which are suspended, and what limitation created each carryforward? Did you receive written assumptions, decision dates, and assigned responsibilities? Finally, did the completed return update the portfolio’s basis, depreciation, and loss schedules and establish the next planning priorities? If the relationship starts and ends with document collection, it may be accurate and responsive without being structurally proactive.

Does qualifying as a real estate professional release prior suspended losses?

Not automatically. We would separate the current-year activity classification from the treatment of losses generated in earlier passive years. A landlord may qualify as a real estate professional and materially participate in the current year while prior suspended amounts remain governed by the former passive activity rules. Their use may depend on current income from the activity or a qualifying disposition rather than the new status alone. The planning file should therefore track losses by year, activity, and limiting rule. Otherwise, a valid current-year position may be presented as if it immediately unlocked tax attributes that remain deferred.

Can grouping rental properties affect suspended losses when one property is sold?

Yes. Treating multiple rentals as one activity can support the material-participation analysis, but it also changes the activity unit used when applying passive-loss rules. If one property is sold while the combined activity continues, we would not assume that every suspended loss tied to the portfolio becomes available. The election should be evaluated when it is made and again before a disposition. A useful analysis compares the current participation benefit with the investor’s likely sale sequence, remaining properties, and expected use of passive losses. This illustrates how an annual election can create multi-year consequences.

Does a Florida landlord need a local CPA or a real estate tax specialist?

We would prioritize real estate depth and planning access over physical proximity alone. A Florida advisor should understand that the absence of an individual state income tax does not remove federal passive-loss, basis, depreciation, NIIT, or recapture issues. The firm should also be able to coordinate obligations for properties outside Florida and distinguish conventional long-term leasing from transient-rental considerations. For an Orlando-area investor, local familiarity can be helpful, but the stronger fit is usually the firm that reviews transactions before commitment, maintains property-level tax attributes, and coordinates securely with the investor’s other advisors.