DeSantis Property Tax Proposal Update: What HJR 1-F Means for Florida Homeowners and Investors

Last updated: June 2026

Florida’s property tax debate has moved fast.

For months, the discussion around Governor Ron DeSantis’s property tax plan centered on big-picture promises, competing House proposals, and the possibility of major relief for homesteaded homeowners. Now, the issue has a clearer path.

The main proposal to watch is CS/HJR 1-F, “Save our Homes from Excessive Property Taxes.” Florida lawmakers passed the joint resolution on June 2, 2026, with a 75-26 vote in the House and a 30-9 vote in the Senate. The measure was then ordered enrolled. If voters approve it, the amendment would take effect on January 1, 2027.

That does not mean Florida property taxes have already been eliminated. They have not.

It means voters may get the chance to approve a major constitutional change that would expand homestead property tax relief, reduce the assessment cap on many non-homestead properties, and reshape how counties and municipalities use remaining property tax revenue.

For homeowners, this could be a major tax break. For investors, landlords, second-home owners, and commercial property owners, the answer is more complicated.

Key takeaways

CS/HJR 1-F would increase the homestead exemption for non-school property taxes. The proposal would exempt the first $150,000 of assessed value for qualifying homesteads in 2027, then the first $250,000 of assessed value in 2028 and later years. The $250,000 amount would be indexed to inflation beginning in 2029.

The amendment would not immediately eliminate every property tax bill. School district levies are treated separately, and the ballot language says the $250,000 exemption would apply to levies other than school district levies.

The proposal also matters for investment property because it would lower the annual assessment increase cap for many non-homestead properties from 10% to 5% beginning January 1, 2027. That affects non-homestead residential and nonresidential property, but not school district levies.

The measure still needs voter approval. Florida constitutional amendments require approval by 60% of voters, and the House analysis says HJR 1-F would appear before voters during the 2026 general election.

Ready to see how the Desantis property tax proposal could hit your portfolio?

What changed from the earlier DeSantis property tax proposal?

Earlier discussions focused on several separate ideas: a broad DeSantis proposal to move toward eliminating homestead property taxes, a possible short-term rebate, and multiple House measures such as HJR 201.

That is no longer the best way to frame the issue.

The current proposal is CS/HJR 1-F. It is the active constitutional amendment that passed the Legislature. It replaces much of the earlier uncertainty with a clearer structure.

The earlier House package is now background. Investors and homeowners should stop treating HJR 201 and similar earlier proposals as the main vehicle. The current question is whether voters approve HJR 1-F, and how local governments respond if it passes.

What HJR 1-F would actually do

HJR 1-F has several major parts.

First, it would create a larger homestead exemption for non-school property taxes. In 2027, qualifying homesteads would receive an exemption on the first $150,000 of assessed value. In 2028, that amount would rise to $250,000. Beginning in 2029, the $250,000 amount would be adjusted for inflation.

Second, it would keep school district taxes separate. The ballot language says the first $250,000 of a homestead’s value would be exempt from taxes for all levies other than school district levies.

Third, it would create a waiting period for newer Florida residents. The House analysis says owners who were not permanent Florida residents as of December 31, 2026, would initially receive a smaller homestead exemption and would receive the full Florida resident homestead benefit after five years of Florida residency.

Fourth, it would reduce the non-homestead assessment cap from 10% to 5% per year for certain non-school property tax purposes. That detail is especially important for investors because it applies to many non-homestead residential and nonresidential properties.

Fifth, it would limit how counties and municipalities can use certain ad valorem tax revenue. The listed uses include public safety, education and public schools, infrastructure, natural resource projects, local bonds, retirement obligations, and certain county and municipal operations.

Not sure how homestead rules and Save Our Homes affect your deals?

What this means for Florida homeowners

Homesteaded primary residences are the clearest potential winners.

A homeowner with a qualifying Florida homestead could see a meaningful reduction in the county, city, and special district portions of the property tax bill. The biggest benefit would likely go to homeowners whose assessed values are high enough to use the expanded exemption.

For example, if a qualifying homestead has a taxable value that is heavily affected by non-school local levies, the larger exemption could reduce a large part of that bill. Some homeowners could see their non-school property taxes fall sharply.

But this is not the same as saying every homeowner’s entire property tax bill goes to zero.

School district taxes are not included in the new exemption. Special assessments, fees, and other property-related charges may also continue depending on the property and local government structure.

Homeowners should look at their actual tax bill, not just the headline. The key question is how much of the current bill comes from non-school ad valorem taxes.

What this means for Florida real estate investors

Investors should be careful with the phrase “property tax relief.”

HJR 1-F is mainly a homestead proposal. It is designed around primary residences, not rental properties, short-term rentals, second homes, shopping centers, office buildings, or development land.

That means investor-owned property may not receive the same direct benefit as a homesteaded primary residence.

Still, investors should not ignore the proposal. It could affect Florida real estate in several ways.

A larger homestead exemption could increase demand for homes that buyers intend to occupy as primary residences. That may help investors selling single-family homes into the owner-occupant market.

The lower non-homestead assessment cap could help some rental and commercial owners by slowing increases in assessed value for non-school tax purposes. But this is not the same as a tax cut. It limits growth in assessed value, not necessarily the total tax bill.

Local governments may also respond to revenue pressure through fees, special assessments, millage decisions, budget cuts, or changes in service levels. Those responses could affect operating costs, tenant demand, and long-term property values.

Revenue pressure is the biggest risk

The fiscal impact is where investors need to pay close attention.

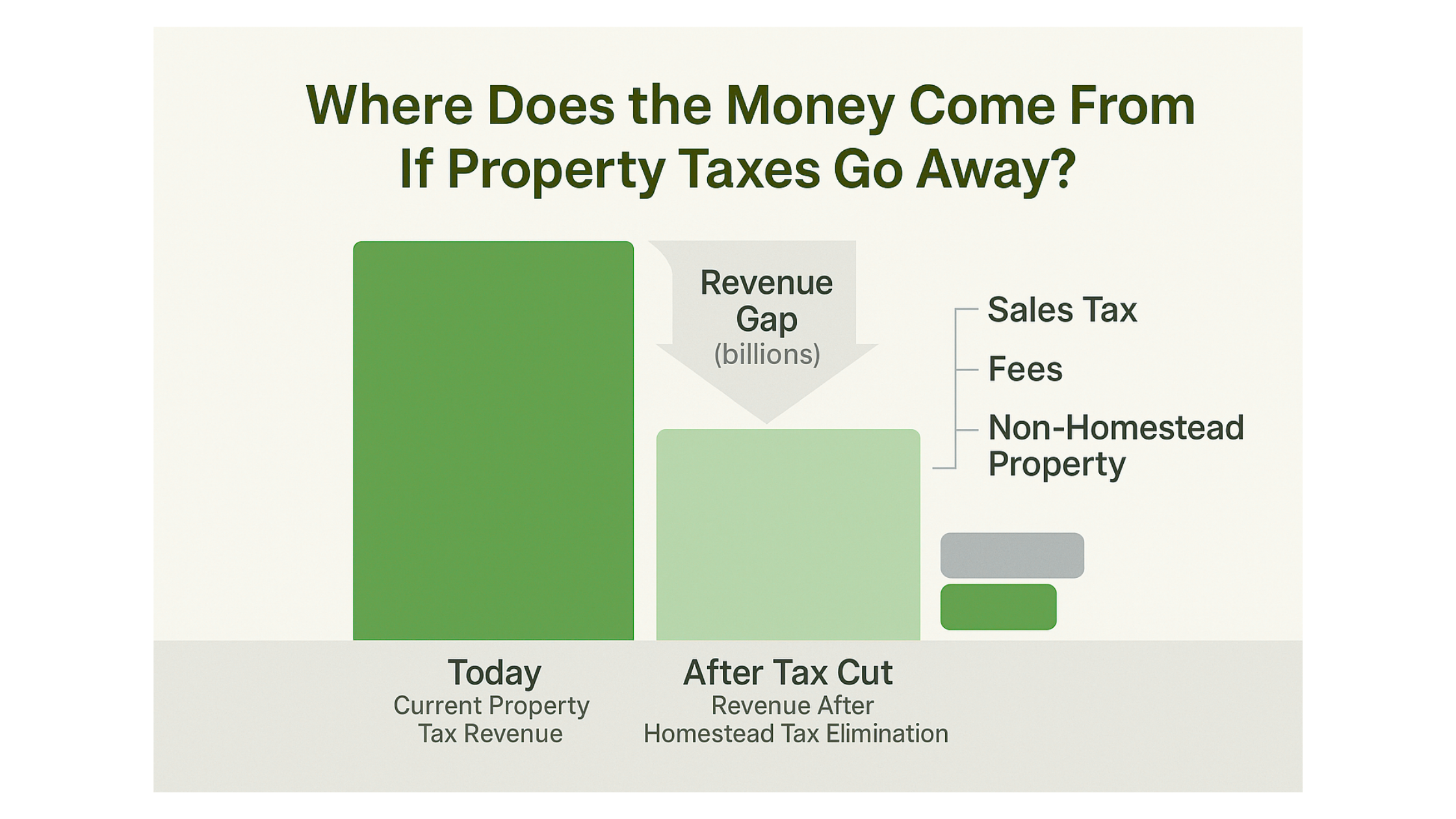

The House analysis says the Revenue Estimating Conference had not estimated the full local government revenue impact at the time of the analysis. However, staff estimated that if voters approve the amendment, the impact on local government revenue could be more than $4.6 billion in non-school taxes in FY 2027-28 and more than $8.4 billion in non-school taxes in FY 2028-29.

That matters because property taxes fund local services that affect real estate value.

Roads, drainage, police, fire service, parks, permitting capacity, code enforcement, infrastructure, and public safety all influence whether a market remains attractive. A lower tax bill is helpful, but weak services can hurt a neighborhood, a rental market, or a commercial corridor.

Investors should not model HJR 1-F as a simple upside event. It is better to model it as a tax policy shift with both savings and second-order risks.

Who could benefit most?

The biggest direct beneficiaries would likely be existing homesteaded homeowners, especially those with enough assessed value to use the expanded exemption.

Long-term Florida residents with established homesteads may see the most immediate benefit because they already qualify under the current homestead system and may be positioned to receive the larger exemption sooner.

Owners of homes that are likely to be sold to primary-residence buyers could also benefit indirectly if the tax savings make owner-occupied purchases more attractive.

Some non-homestead owners could benefit from the proposed 5% assessment cap, especially in markets where assessed values have been rising quickly. But again, that is a cap on assessment growth for certain purposes, not full tax elimination.

Who may not benefit directly?

Renters do not receive a homestead exemption because they do not own the property.

Landlords do not receive the expanded homestead exemption on rental property unless the property qualifies as their own permanent residence, which typical rental property does not.

Second homes and vacation homes generally do not receive the same treatment as a homesteaded primary residence.

Commercial property owners do not receive the expanded homestead exemption, though they may care about the lower non-homestead assessment cap.

New Florida residents may also face a delayed benefit. Under the proposal, owners who were not permanent Florida residents as of December 31, 2026, would not immediately receive the same expanded homestead exemption as longer-term Florida residents.

Concerned that tax cuts for homesteads will shift the bill to your rentals and commercial assets?

Three scenarios investors should model

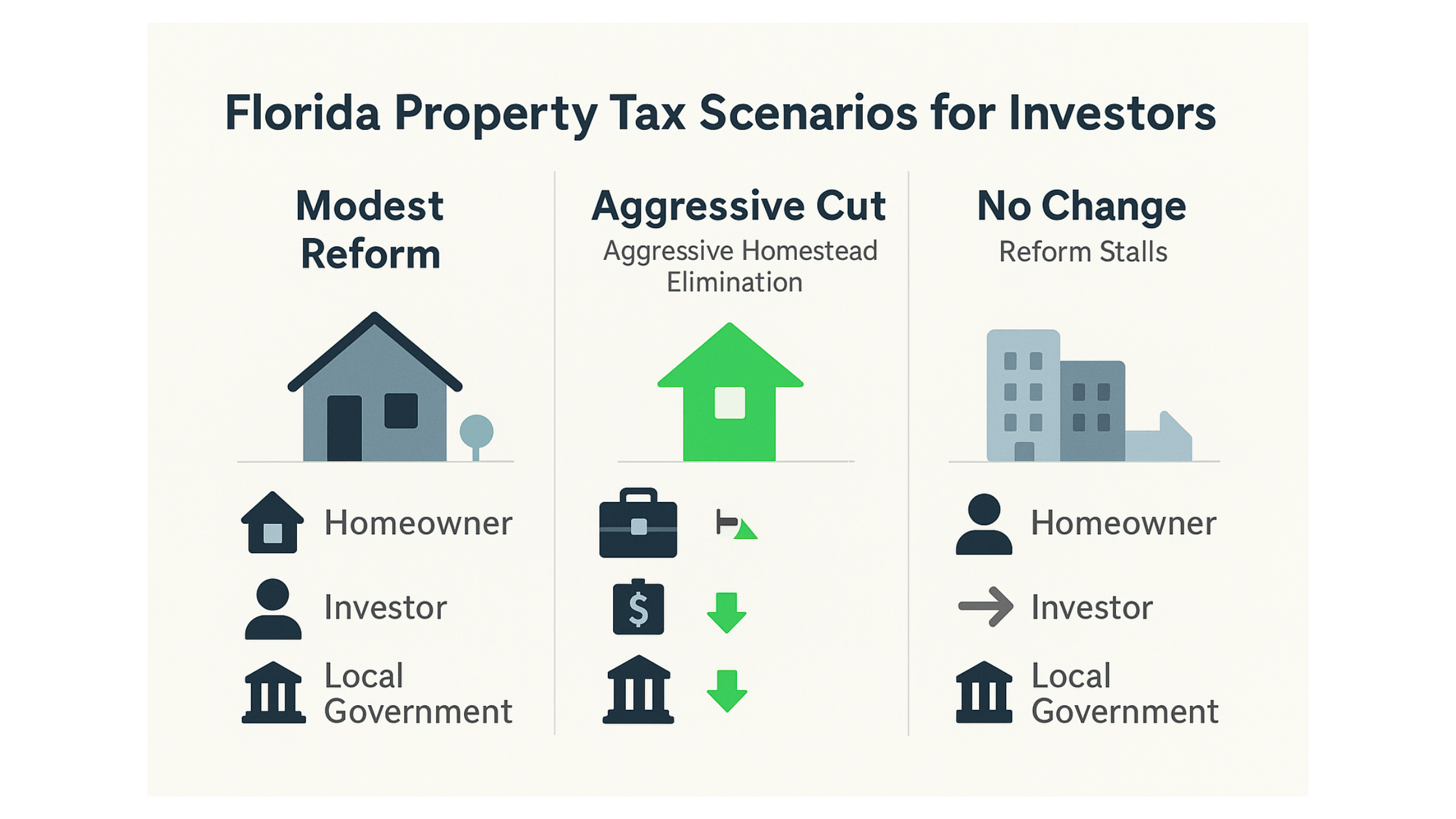

Scenario 1: HJR 1-F passes

In this scenario, qualifying homesteaded homeowners receive a larger non-school exemption beginning in 2027. The exemption rises again in 2028.

Investors should model stronger demand for homes that appeal to owner-occupants. They should also model the lower 5% non-homestead assessment cap for eligible assets.

But they should also stress test local government responses. Higher fees, special assessments, slower permitting, infrastructure pressure, or budget cuts could offset some of the benefit.

Scenario 2: HJR 1-F fails

In this scenario, Florida keeps its existing property tax structure.

That means current homestead exemptions, Save Our Homes protections, non-homestead assessment rules, and local government tax structures remain largely intact unless changed by future legislation.

Investors should continue underwriting based on current tax bills, expected reassessments, and local millage trends.

Scenario 3: HJR 1-F passes, but local impact varies by county

This may be the most realistic planning scenario.

Florida is not one market. Miami-Dade, Palm Beach, Broward, Orange, Hillsborough, Collier, Lee, Duval, and smaller counties all have different tax bases, service demands, debt obligations, and growth pressures.

Some local governments may absorb the change more easily. Others may look harder at fees, assessments, budget cuts, or development-related charges.

Investors should model county-level and city-level exposure instead of assuming one statewide outcome.

Practical checklist for Florida property owners and investors

Before making a purchase, sale, refinance, or restructuring decision, review these items:

Confirm whether the property is homesteaded, homestead-eligible, non-homestead residential, commercial, or mixed-use.

Pull the current tax bill and separate school taxes from non-school taxes.

Review assessed value, taxable value, exemptions, millage rates, and special assessments.

Model the current system, an HJR 1-F pass case, and an HJR 1-F fail case.

For investment property, model the proposed 5% assessment cap but do not assume full tax elimination.

Review local government exposure. A property in a city or county highly dependent on property tax revenue may face different risks than one in a more diversified local budget.

For high-net-worth homeowners, review residency, title, trusts, entity ownership, and homestead qualification before making changes.

Do not make a major deal decision based only on the phrase “property tax elimination.”

Curious whether your assets sit on the winning or losing side of the proposal?

Planning considerations for high-net-worth families

For high-net-worth individuals and families, HJR 1-F could make Florida homestead planning even more important.

A larger homestead exemption may increase the value of holding a qualifying Florida primary residence. But the details matter. Ownership through trusts, LLCs, partnerships, or family office structures can create homestead qualification issues if not handled properly.

Residency also matters. The proposal includes different treatment for owners who were not permanent Florida residents as of December 31, 2026. Anyone considering Florida residency should coordinate property tax planning with state income tax residency planning, estate planning, asset protection, and multi-state exposure.

The main point is simple: homestead planning should not be done casually. The tax savings may be meaningful, but the structure has to be correct.

Stop guessing. Model all three Florida tax scenarios with real numbers.

DeSantis property tax proposal and HJR 1-F

Has Florida eliminated property taxes?

No. Florida has not eliminated property taxes. HJR 1-F is a proposed constitutional amendment. It passed the Legislature, but it still needs voter approval before taking effect.

What is the current DeSantis property tax proposal?

The current proposal is CS/HJR 1-F, also called “Save our Homes from Excessive Property Taxes.” It would expand the homestead exemption for non-school property taxes, lower the assessment cap for many non-homestead properties, and limit certain local government uses of ad valorem tax revenue.

When would the change take effect?

If approved by voters, the amendment would take effect on January 1, 2027.

Would school property taxes go away?

No. The proposed expanded homestead exemption applies to levies other than school district levies. School district taxes are treated separately.

Would rental properties get the same tax break?

Generally, no. Rental properties usually do not qualify for homestead treatment unless the owner uses the property as a qualifying permanent residence. However, many non-homestead properties could be affected by the proposed reduction in the assessment cap from 10% to 5% for certain non-school tax purposes.Bottom line

The DeSantis property tax proposal is no longer just a broad political talking point. The active issue is now HJR 1-F, a proposed constitutional amendment that has passed the Florida Legislature and is headed to voters.

For homeowners, the proposal could create major relief on the non-school portion of property taxes. For investors, the impact is more mixed. Some properties may benefit from stronger owner-occupant demand or a lower non-homestead assessment cap. Others may face indirect pressure from local revenue gaps, fees, assessments, or service changes.

The smart move is not to assume every Florida property gets cheaper to own.

The smart move is to model the numbers property by property, county by county, and scenario by scenario.

Florida tax policy may be changing. Your real estate strategy should be ready before the vote, not after it.

The policy path is uncertain. Your tax strategy should not be.

HJR 1-F Property Tax Planning FAQs

Key questions for high-net-worth Florida residents, homeowners, and real estate investors evaluating homestead planning, non-homestead property exposure, ballot risk, local tax pressure, and portfolio-level property tax strategy.

How should HNW Florida residents evaluate the proposal before the vote?

We would start with the actual tax bill, not the headline. The most useful review separates school levies, non-school levies, exemptions, assessed value, taxable value, and special assessments. For HNW households, the practical issue is not simply whether HJR 1-F passes. It is how much of the current carrying cost is exposed to the non-school portion of the bill, how ownership is structured, and whether the property is clearly positioned as a qualifying homestead. That gives a more reliable planning baseline before any purchase, sale, refinance, or residency decision.

Does HJR 1-F change the value of Florida homestead planning?

It may increase the importance of getting homestead planning right. The article frames HJR 1-F as primarily a homestead proposal, which means the benefit depends on whether the property qualifies as a primary residence under the relevant rules. For HNW families, we would look closely at title, residency timing, trust ownership, entity ownership, and broader multi-state exposure. The larger exemption may be meaningful, but only if the ownership and residency facts support the intended treatment. The planning question is not only “Do we own Florida property?” but “How is it held, used, and documented?”

What should investors watch beyond the homestead exemption?

Investors should focus on the non-homestead assessment cap and local government response. The article notes that HJR 1-F would reduce the annual assessment increase cap for many non-homestead properties from 10% to 5% for certain non-school tax purposes. That may affect rental homes, second homes, and commercial assets, but it is not the same as a broad investor tax cut. We would also model possible second-order effects, including fees, special assessments, permitting capacity, service levels, and county-by-county budget pressure.

How could the proposal affect a Florida home purchase before 2027?

A pre-2027 purchase should be modeled under more than one outcome. The article’s logic points to three cases: current law, HJR 1-F passage, and HJR 1-F failure. For a buyer planning to occupy the home as a primary residence, the homestead treatment and residency timing matter. For a buyer acquiring a property as an investment, the direct homestead benefit may not apply, though the non-homestead assessment cap may still be relevant. We would avoid pricing a deal solely around expected tax relief unless the numbers still work under current rules.

Could local fees or assessments offset part of the tax benefit?

They could become a bigger planning variable. The article emphasizes that lower non-school property tax revenue may put pressure on local budgets. Counties, cities, and special districts may respond differently depending on their tax base, service demands, debt obligations, and growth needs. For HNW owners and investors, we would not look only at ad valorem taxes. We would also review special assessments, utility-related charges, infrastructure costs, development fees, and the local government’s dependence on property tax revenue before estimating the net benefit.

How should multi-property owners segment their Florida holdings?

We would separate properties by use and tax profile. A primary residence, a second home, a long-term rental, a short-term rental, commercial property, and land held for development may each react differently to HJR 1-F. The article suggests reviewing homestead eligibility, rental use, non-homestead status, millage exposure, and special assessments property by property. That matters because a benefit that applies to one asset may not carry over to another. A clean segmentation also helps avoid overestimating the value of the proposal across a broader Florida portfolio.

What does the proposal mean for new Florida residents?

The article notes that newer Florida residents may not receive the same immediate benefit as longer-term Florida residents. For HNW families considering a Florida move, the timing of residency, property acquisition, and homestead qualification should be reviewed together. We would not treat residency as a simple mailing address change. The planning should connect property tax exposure with broader residency facts, ownership structure, estate planning, and multi-state considerations. The key issue is whether the household’s facts support the intended Florida position before relying on expanded homestead treatment.

How should HNW families model the ballot risk?

We would treat the vote as a planning variable, not a settled outcome. The article makes clear that HJR 1-F has passed the Legislature but still depends on voter approval. For HNW families, that means current-law planning remains relevant until the outcome is known. A practical model should compare the current tax structure with a pass case and a fail case, then layer in county-level response risk. That approach is more useful than assuming a single statewide result will affect every property, family structure, or investment position the same way.