Equipment, Real Estate, or Equity Investments: Choosing the Right Asset for Your Tax Profile

The asset with the strongest first-year tax benefit is not always the asset that fits the taxpayer’s full multi-year plan.

Equipment, real estate, or equity investments can all be tax-efficient. They are not tax-efficient for the same reason.

For a high-income taxpayer, the better question is not, “Which asset creates the largest deduction?” It is, “Which asset best fits the tax profile we are trying to manage across acquisition, ownership, and exit?”

In broad terms:

| If the immediate planning priority is… | The asset that often deserves first review | What must be tested before relying on it |

|---|---|---|

| Reducing taxable active business income in a strong operating year | Equipment | Business need, eligibility, placed-in-service timing, financing, and future recapture |

| Building a multi-year real estate tax strategy | Real estate | Loss usability, participation status, debt and reserve durability, hold period, and exit-year tax stack |

| Preserving liquidity and controlling realization timing | Equity investments | Gain-bunching risk, NIIT exposure, diversification, and whether current deductions are actually needed |

Equipment tends to be strongest when the taxpayer has an active operating business and a capital purchase that already belongs in the business plan. Real estate tends to be strongest when the taxpayer wants a durable, multi-year planning asset and is willing to model depreciation, participation, reserves, and eventual exit together. Equity investments tend to be strongest when flexibility, liquidity, and gain-timing control matter more than front-loaded ordinary-income reduction.

In this article, equity investments refers primarily to marketable equity exposure and similar portfolio positions, not the tax structuring of an operating-company acquisition.

The differentiated planning issue is this: an asset can look tax-efficient in Year 1 and still be poorly matched to the taxpayer’s long-term tax profile.

Why this decision matters more for high-income taxpayers

High-income taxpayers rarely need “more deductions” in the abstract. They need tax attributes that land in the right place:

against the right type of income,

in the right year,

through the right owner or entity,

without creating a worse liquidity or exit problem later.

That is a different decision than simply choosing the asset class with the most visible tax benefit.

A profitable business owner may get real value from equipment if the purchase supports operations and accelerates deductions into an unusually strong income year. A real estate investor may benefit from depreciation or cost segregation, but only if the resulting losses are usable now, strategically useful later, or intentionally carried into an exit plan. A taxpayer expecting a major liquidity event may prefer equities because optionality can be more valuable than chasing a deduction that narrows future choices.

For sophisticated taxpayers, the tax return can be technically correct while the broader investment decision is still poorly sequenced. That is why asset selection should be reviewed as part of a multi-year tax architecture, not as a December purchase decision.

Use our Florida Tax Exposure Scorecard to identify where income timing, asset mix, and future gain events may deserve closer review.

Key takeaways

Equipment, real estate, and equity investments solve different tax problems. They should not be compared only by immediate deduction size.

Deduction generation and deduction usability are different. A large tax attribute has less current value if it lands in a limited or mismatched bucket.

Real estate offers the deepest multi-year planning canvas, but also the most classification, liquidity, and exit complexity.

Equity investments often provide the best flexibility, especially when timing control and liquidity matter more than current-year ordinary-income reduction.

Exit-year pressure should be modeled before acquisition. Recapture, unrecaptured §1250 gain, NIIT, and gain concentration can change the after-tax result.

Florida taxpayers need federal tax planning that is more—not less—coordinated, because the absence of personal state income tax does not eliminate property-level durability, liquidity, and concentration risk.

Equipment, Real Estate, or Equity Investments: What is the real tax decision?

The real decision is not which asset is “best.” It is which asset best fits the taxpayer’s income type, holding period, liquidity needs, structure, and unwind plan.

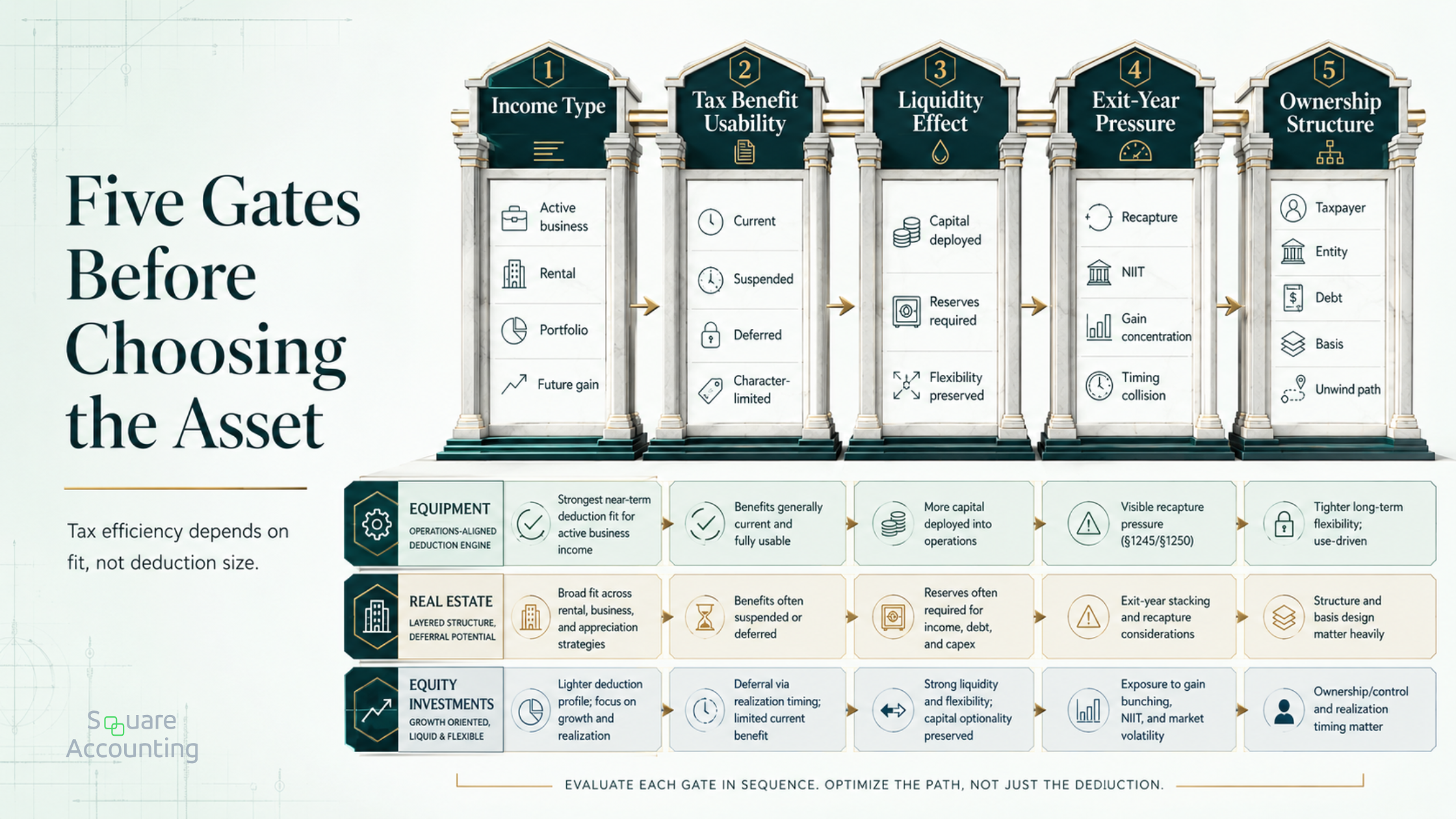

A high-income taxpayer choosing among equipment, real estate, or equity investments should usually answer five questions before comparing projected tax benefits:

What type of income are we trying to influence?

Can the intended tax benefit actually be used in the desired period?

What liquidity does the asset consume or preserve?

What tax pressure appears at exit or unwind?

Does the ownership structure support the intended result?

Those questions create a stronger comparison than simply asking whether equipment offers accelerated depreciation, real estate offers cost recovery, or equities receive capital-gain treatment. Each of those statements may be true in the right setting. None is sufficient alone.

The article’s core framework is simple:

| Planning lens | Equipment | Real estate | Equity investments |

|---|---|---|---|

| Primary tax role | Accelerate business deductions | Coordinate depreciation, leverage, and long-term ownership | Manage liquidity and realization timing |

| Income fit | Active business income | Rental, passive, or nonpassive depending on facts | Portfolio income and capital gains |

| Planning strength | Timing | Architecture | Optionality |

| Most common blind spot | Buying for tax rather than operations | Assuming deductions are currently usable | Treating tax deferral as exit planning |

A practical framework for matching the asset to your tax profile

A meaningful asset comparison begins with the tax problem being solved, then tests whether the asset remains efficient through structure and exit.

Before evaluating the tax benefit of a specific investment, we would pressure-test the decision through a sequence of planning questions. Each gate narrows whether the asset actually fits the taxpayer’s income, capital, and exit profile.

1. What type of income are you trying to influence?

The asset should be chosen in relation to the income stream that creates the planning pressure.

Active business income: Equipment may be highly relevant when it supports a real operating need and creates deductions that align with that income.

Rental or real estate income: Real estate may be the right planning asset when the investor can use losses, wants long-term depreciation benefits, or needs a portfolio-level real estate strategy.

Portfolio income and future gains: Equity investments may fit when the taxpayer is managing liquidity, gain timing, dividend exposure, or concentrated positions.

This distinction matters because tax attributes do not automatically cross categories. A deduction generated in one lane may not solve a problem in another.

A taxpayer with substantial W-2 income, no real estate professional fact pattern, and a large depreciation-driven rental loss may discover that the tax outcome is very different from the marketing headline. A business owner with unusually high operating income may find that planned equipment capex creates more immediate tax utility than another illiquid investment. A taxpayer nearing a business sale may decide that preserving investable liquidity is more valuable than converting cash into a hard-to-unwind asset.

2. Can the tax benefit be used now?

There is a critical difference between:

creating a deduction,

being allowed to claim a deduction, and

receiving a current-year cash-tax benefit from that deduction.

That difference is often overlooked.

Equipment deductions may produce meaningful current-year tax relief if they offset income the taxpayer already expects to report. Real estate losses may be highly valuable, but passive activity rules can delay the benefit. Equity losses live in a different capital-gain and capital-loss system than operating deductions or depreciation.

The planning mistake is not generating a deferred or suspended tax benefit. The mistake is treating it as though it were a same-year ordinary-income offset before confirming that result.

That issue matters even for taxpayers who already have a CPA. A return can properly reflect depreciation, passive losses, and realized gains while still failing to answer the more important strategic question: Did the chosen asset solve the intended tax problem at the right time?

3. Does the asset improve or weaken liquidity?

Tax efficiency has a balance-sheet side.

Equipment may increase operating capacity, but it may also require cash, financing, or fixed payment commitments. Real estate can create depreciation and appreciation potential, but it may also consume down payment capital, reserve funds, repair capacity, and debt-service coverage. Equity investments are usually more liquid, but that liquidity can create its own discipline problem if gains are realized reactively rather than strategically.

A tax deduction that weakens future flexibility is not automatically a poor decision. But it should be treated as a trade-off, not as a free benefit.

This is especially relevant when the taxpayer may need capital for:

a business acquisition,

an ownership transition,

family liquidity planning,

a debt reduction event,

a future tax payment,

or an opportunity to purchase a better asset later.

An investment that appears tax-efficient in isolation may be strategically inefficient if it locks capital into the wrong place before a higher-priority decision arrives.

4. What happens in the exit year?

The acquisition-year tax benefit is only one part of the timeline.

At exit:

equipment may trigger depreciation recapture,

real estate may produce multiple gain layers,

equities may create concentrated capital gains,

and several of those events may occur in the same tax year.

For high-income taxpayers, the problem is often not a single gain. It is gain stacking—the collision of multiple tax events in a year that already contains elevated income.

A real estate sale in the same year as a business liquidity event can behave differently from the same property sale in a lower-income year. A brokerage liquidation used to fund a property acquisition can behave differently if the taxpayer is already exposed to NIIT. An equipment disposition can change the character of what looked like long-term operating efficiency.

Tax planning should therefore compare purchase-year benefit with exit-year pressure before the asset is acquired.

5. Does the ownership structure support the intended result?

Asset choice and ownership structure should be evaluated together.

The same asset can produce different planning consequences depending on:

who owns it,

which entity uses it,

how debt is allocated,

who receives the income,

where basis resides,

and who bears the eventual gain or loss.

This matters for all three asset types.

Equipment held in the wrong operating structure may complicate deductibility, financing, or sale planning. Real estate held in a structure that no longer matches the exit objective may create unnecessary rigidity. Equity positions held personally, through trusts, or within entities can raise very different coordination questions around income recognition, distributions, and future transfers.

The asset’s headline tax treatment is not enough. The tax result must reach the intended taxpayer in the intended way.

When equipment is the right tax-profile fit

Equipment can be the strongest tax-profile fit when a taxpayer has:

a real operating business need,

high active taxable income,

a planned capital expenditure already under consideration,

and a clear reason the asset should be placed into service now rather than later.

This is most compelling when tax timing and business economics point in the same direction.

Why equipment can be powerful

Current federal rules make equipment planning especially important. Certain qualified property acquired and placed in service after January 19, 2025 may generally qualify for a 100% additional first-year depreciation deduction, and Section 179 may also be relevant under separate eligibility, dollar-limit, and taxable-income rules.

For a taxpayer with strong operating income, that can create a significant timing benefit. It may allow a planned equipment purchase to be aligned with:

a high-profit year,

a capacity expansion,

a production need,

a technology upgrade,

or a business process improvement already justified on economic grounds.

The tax benefit is strongest when it follows the business case. It is weaker when the business case is invented to support the tax result.

Where equipment planning backfires

Equipment planning begins to fail when the deduction becomes the dominant reason for the purchase.

Typical failure modes include:

buying capacity before the business can use it,

pulling capital out of a more valuable opportunity,

relying on first-year tax savings while ignoring future debt service,

creating a lower depreciation profile in later years when the business may still be profitable,

and overlooking recapture when the asset is sold, exchanged, or disposed of.

An accelerated deduction can improve a strong decision. It does not rescue a weak one.

Another overlooked issue is income timing mismatch. A large deduction may be most valuable in a year when taxable income is unusually high and reasonably visible. If income later falls, the business may have consumed part of the future depreciation runway precisely when it would have been useful to preserve it.

Equipment timeline: how the strategy behaves

| Period | Strategic tax question |

|---|---|

| Year 1 | Does the deduction align with real operating income and a real business need? |

| Years 2–3 | Does the asset continue to improve economics after much of the tax benefit has already been accelerated? |

| Exit year | Does a sale or disposition create recapture that was not reflected in the original after-tax analysis? |

Equipment is often a strong answer when the taxpayer was already going to make the capital investment. It is a weaker answer when the taxpayer is buying a deduction and hoping the asset becomes useful later.

When real estate is the right tax-profile fit

Real estate can be a powerful planning asset, but it is rarely a simple “deduction asset.”

Its tax profile is richer because it combines:

depreciation,

potential accelerated cost recovery,

debt,

operating income,

participation rules,

appreciation,

liquidity constraints,

and exit design.

That complexity is not a drawback for a serious investor. It is the reason real estate can be highly strategic when planned correctly.

Real estate’s real advantage: multi-year coordination

The real advantage of real estate is not merely that it depreciates. It is that the asset can be coordinated across several tax years and several planning dimensions at once.

A serious real estate tax model should consider:

the acquisition-year depreciation profile,

whether cost segregation changes timing meaningfully,

the taxpayer’s ability to use the deductions,

whether losses are current, suspended, or strategically deferred,

financing terms and cash reserve assumptions,

and the likely hold-versus-exit path.

This turns real estate from a “tax benefit” into a sequencing asset.

A depreciation-heavy acquisition may be highly effective if the taxpayer has a clear path to using the losses and a durable hold thesis. The same acquisition may be less attractive if the losses are suspended, the property creates liquidity stress, and the exit year collides with other large gains.

Loss usability is the fulcrum

Rental real estate is generally treated as passive unless an exception applies, and real estate professional treatment still depends on the taxpayer’s facts and material participation.

This point changes the entire comparison.

A real estate investor may obtain a cost segregation study, generate large depreciation-driven losses, and still receive little immediate ordinary-income relief if those losses are limited. That does not make the study wrong. It means the benefit must be classified correctly:

current-year offset,

suspended loss with future utility,

portfolio-level income shield,

or exit-year release potential.

Suspended passive losses can become important in a later fully taxable disposition of an entire passive activity interest, but that is an exit-planning concept—not a substitute for confirming same-year deductibility.

The sophisticated question is not “How large is the projected loss?”

It is “Where does that loss live, and when can it create value?”

Short-term rentals require sharper classification work

Florida investors often encounter short-term rental strategies framed as a broad path to nonpassive losses. The actual analysis is more precise.

Under IRS guidance, an activity is not treated as a rental activity if the average period of customer use is seven days or less. But that does not automatically make the resulting losses nonpassive. Material participation remains a separate question.

This creates a common planning collision:

The investor sees a short average stay profile.

The investor assumes the tax treatment is now solved.

The investor accelerates depreciation.

The material participation record is later less robust than the deduction strategy required.

Short-term rental planning can be powerful. It is not a shortcut around documentation, activity-level analysis, or timing discipline.

Real estate exit taxes deserve more attention than acquisition deductions

Real estate is often sold to taxpayers through the acquisition-year story. Sophisticated planning should spend more time on the unwind.

A real estate exit can involve several layers at once:

| Exit-year layer | Why it matters |

|---|---|

| Adjusted basis after depreciation | Accelerated deductions can increase taxable gain later |

| Depreciation-related gain | Part of the exit may be taxed differently than a simple capital-gain narrative suggests |

| Unrecaptured §1250 gain | Gain attributable to prior depreciation may be taxed at a maximum 25% rate |

| NIIT exposure | Capital gains and certain rental income may be included in net investment income for affected taxpayers |

| Suspended passive losses | Some losses may become usable at disposition if the requirements are satisfied |

A real estate strategy is stronger when the depreciation benefit and the exit-year tax stack are evaluated together.

The purchase-year tax benefit is only half of the real estate decision. A more complete model shows how depreciation, basis, and gain recognition may reappear together when the property is eventually sold.

The IRS states that gain attributable to depreciation may be subject to the 25% unrecaptured §1250 gain rate, and net investment income generally includes items such as capital gains and rental income for affected taxpayers.

That is why a property that looks tax-efficient during ownership may become less attractive if:

the investor sells earlier than planned,

several properties are sold in one period,

the exit occurs alongside a business sale,

reserve pressure shortens the hold period,

or the acquisition was built around deduction acceleration rather than a durable investment thesis.

Real estate can be one of the best tax-planning assets available to a high-income taxpayer. It is also one of the easiest to misread if the plan stops at depreciation.

Our Real Estate Exit-Year Tax Pressure Map helps organize recapture, NIIT, liquidity, and sale-timing questions before the exit drives the plan.

When equity investments are the right tax-profile fit

Equity investments are often overlooked in tax strategy conversations because they do not usually create dramatic first-year deductions. That can be exactly why they fit.

Their strength is often not immediate tax reduction. It is:

liquidity,

timing control,

diversification,

portability,

and the ability to decide when a taxable event should occur.

Why equity can be tax-efficient

Equity investments can be highly tax-efficient when the taxpayer values optionality.

A marketable equity portfolio can allow the investor to:

defer gain recognition until a chosen sale,

rebalance intentionally,

harvest losses when appropriate,

preserve capital for later deployment,

and avoid converting liquid wealth into a highly specialized or heavily financed asset solely for tax reasons.

That does not make equities “better” than equipment or real estate. It makes them better suited to a different tax-profile problem.

For a taxpayer approaching a business acquisition, a personal liquidity need, or an uncertain real estate opportunity set, preserving flexibility may be the highest-value tax decision.

Equity is usually weaker as an immediate ordinary-income reduction tool

Equities generally do not solve the same current-year tax problem as an equipment deduction or a currently usable nonpassive real estate loss.

Their tax advantage often appears through:

realization timing,

long-term gain orientation,

loss coordination,

and the ability to avoid premature sales.

That is useful, but it is different from a business deduction designed to offset active income now.

The common planning mistake is treating “tax-efficient” as though it always means “reduces this year’s ordinary income.” Equity investments may be tax-efficient precisely because they do not require the taxpayer to force a transaction this year.

The equity exit problem: gain bunching

Equity’s flexibility can still create a planning problem if the taxpayer waits too long to coordinate realizations.

A concentrated sale of appreciated equities may land in the same year as:

a business sale,

a real estate disposition,

a deferred compensation payout,

or a major portfolio repositioning.

That can turn a flexible asset into an exit-year concentration issue. NIIT may also become relevant when investment income layers onto an already elevated income year.

The tax profile of equities is often attractive. But it still requires sequencing. Deferral is helpful only if the eventual realization year is chosen thoughtfully.

The “works early, breaks later” pattern

The strongest differentiated insight in this comparison is that the apparent tax winner changes across the timeline.

| Asset | Why it often looks attractive early | What can become harder later | The planning response |

|---|---|---|---|

| Equipment | Front-loaded deductions and a visible current-year tax effect | Less depreciation remains; recapture may appear on disposition; cash is committed | Buy because the business needs it, then optimize the timing |

| Real estate | Depreciation, leverage, and potentially accelerated losses | Losses may be suspended; reserves tighten liquidity; exit can create layered tax consequences | Model usability and unwind before acquisition |

| Equity investments | Liquidity, deferral, and realization control | Gains can become concentrated if several taxable events land together | Manage realization years deliberately |

Year 1: Acquisition-year tax impact

In Year 1, taxpayers often overvalue what is easiest to see:

the equipment deduction,

the projected real estate depreciation,

or the absence of immediate tax from unrealized equity appreciation.

The more strategic question is: What was actually improved?

Did equipment lower tax because it supports a profitable business?

Did real estate produce deductions the taxpayer can use or at least plan around?

Did equities preserve flexibility that would otherwise have been lost?

Year 1 should confirm fit, not merely produce a tax result.

Years 2–3: Holding-period consequences

The holding period reveals whether the strategy is durable.

Equipment must continue producing operating value after much of the tax deduction may have been accelerated. Real estate must carry its debt, maintenance, reserves, and property-level risks while the tax attributes are being used, suspended, or strategically positioned. Equities must remain aligned with the taxpayer’s broader liquidity and concentration plan.

A tax strategy that works only in the acquisition year is not a multi-year plan. It is an event.

Exit year: Tax stack and liquidity pressure

The exit year is where asset-selection mistakes become visible.

At that point, the taxpayer may face:

recapture,

depreciation-related gain,

unrecaptured §1250 gain,

gain bunching,

or the forced sale of one asset to fund another.

The best acquisition decision is often the one that leaves the taxpayer with fewer bad exit choices, not merely the biggest first-year deduction.

Continue with a deeper look at how recapture, NIIT, and clustered gains can reshape an otherwise strong investment decision.

A coordinated comparison: which asset tends to fit which taxpayer?

Equipment may fit best when:

The taxpayer has a real operating business with visible income.

The equipment purchase improves productivity, margin, throughput, or capacity.

Current-year deduction timing matters.

The taxpayer can absorb the purchase without weakening liquidity needed elsewhere.

The future disposition has been considered, not ignored.

Real estate may fit best when:

The taxpayer wants a multi-year asset with tax, cash flow, and appreciation potential.

The participation and passive-loss posture has been examined.

The investor can withstand the property’s reserve, insurance, financing, and repair demands.

The hold period is long enough to support the strategy.

Exit-year recapture, NIIT, and gain concentration have been modeled.

Equity investments may fit best when:

Liquidity and optionality are major priorities.

The taxpayer does not need immediate ordinary-income reduction.

Realization timing control matters.

The taxpayer wants flexibility before a larger business or real estate decision.

Future gain concentration is being managed intentionally rather than deferred passively.

We can evaluate whether equipment, real estate, or a more flexible investment posture better fits your current income profile and multi-year tax plan.

Common oversights sophisticated taxpayers still make

1. Buying equipment for the deduction instead of the business

A deduction may improve the after-tax cost of an asset. It does not create an operating need. The strongest equipment strategy usually starts with a business decision and then optimizes the tax timing around it.

2. Assuming real estate losses will automatically reduce high ordinary income

A projected tax loss and a currently usable tax loss are not the same thing. Passive activity limits, real estate professional treatment, material participation, basis, at-risk rules, and ownership structure can all change the outcome.

3. Treating cost segregation as a stand-alone strategy

Cost segregation can accelerate depreciation. It does not, by itself, confirm that the taxpayer can use the resulting losses in the desired year or that the accelerated deduction still makes sense if the exit arrives earlier than expected.

4. Ignoring exit-year recapture because “we may never sell”

Permanent hold is a possible objective. It is not a reason to avoid modeling sale mechanics. Equipment dispositions and real estate exits can both revive tax costs that were muted or deferred during the holding period.

5. Overestimating the ordinary-income value of equity losses

Equity losses are useful, but they belong to a different tax framework than business deductions or real estate depreciation. Treating all tax benefits as interchangeable leads to poor comparisons.

6. Failing to coordinate asset choice with entity structure

Taxpayers often compare assets first and ask ownership questions later. That sequence can create friction. The owner, the activity, the debt, and the eventual gain should be considered before the strategy is implemented.

7. Chasing deductions without a liquidity plan

A taxpayer can reduce current taxes and still create a weaker strategic position. Debt service, reserve demands, future tax payments, and capital-call-like obligations all matter. Tax efficiency should not come at the cost of losing flexibility when a better opportunity or an unavoidable obligation appears.

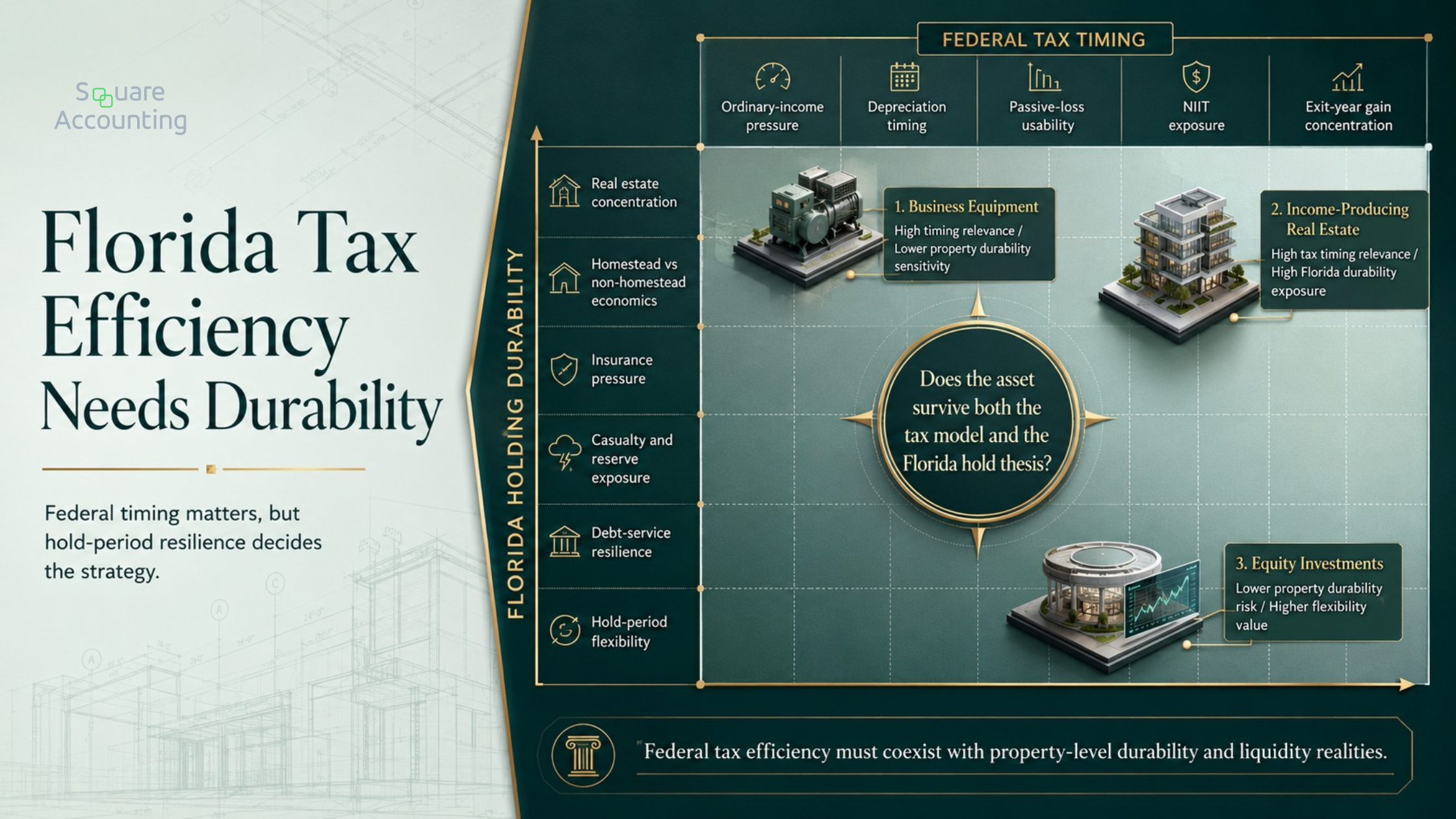

Florida-specific planning: why the same asset choice can behave differently here

Florida planning does not become simple because the state does not impose a personal income tax. It becomes more dependent on federal sequencing and more sensitive to real estate durability.

Florida does not impose a personal income tax, which means federal income-tax mechanics often carry more of the planning weight for individual taxpayers.

For Florida investors, the stronger tax profile is the one that remains workable under both federal timing rules and property-level holding demands.

Florida’s no-personal-income-tax environment does not remove planning complexity; it shifts more attention to federal sequencing and asset durability. A strategy should work in the tax model and remain resilient in the real holding environment.

1. Federal tax timing becomes more visible

Without a personal state income tax layer, high-income Florida taxpayers often focus more heavily on:

ordinary-versus-capital character,

depreciation timing,

passive-loss usability,

NIIT exposure,

and whether a gain event can be placed in a better year.

That does not make state and local considerations irrelevant. It means the income-tax strategy itself is usually driven primarily by federal law.

2. Real estate concentration can amplify exit risk

Florida taxpayers and investors may already hold meaningful exposure to residential, commercial, vacation, or rental real estate. In that setting, another real estate acquisition is not merely another tax planning option. It may also increase:

concentration in one asset class,

reliance on a single regional economy,

the chance that multiple exits cluster together,

and the need for a stronger reserve and liquidity plan.

The tax benefit should be reviewed alongside the portfolio concentration it creates.

3. Homestead and non-homestead economics can affect hold-versus-sell thinking

Florida’s homestead exemption and Save Our Homes assessment limitation can materially affect the economics of retaining, converting, transferring, or selling a residence. Florida also has separate assessment-limitation concepts for non-homestead property.

That matters because a federal tax answer may point one way while the property-tax and holding-period economics point another. A clean income-tax strategy should not ignore property-level consequences that influence whether the asset is realistically held, converted, or exited.

4. Insurance, casualty, and reserve assumptions can change the tax strategy

For Florida real estate, we would not treat a depreciation model as complete without also stress-testing:

insurance affordability,

casualty exposure,

repair timing,

reserve sufficiency,

debt-service durability,

and the possibility that the intended hold period becomes shorter than planned.

These factors do not change the federal tax rules. They change whether the taxpayer can stay in the strategy long enough for the intended tax and economic benefits to work together.

5. Short-term rental planning deserves extra discipline

Short-term rental analysis can matter in Florida because the asset class is common and the federal classification can materially change the planning result. But the same discipline still applies:

average customer use is not the same as material participation,

depreciation potential is not the same as current deductibility,

and a good strategy should survive documentation review, not just projection modeling.

The Florida angle is not that short-term rentals are automatically better. It is that a highly visible strategy deserves a more rigorous pre-acquisition review.

See how federal tax timing, real estate concentration, and liquidity planning interact for Florida taxpayers.

The best asset is the one that fits the full tax profile

The best answer to equipment, real estate, or equity investments is not universal. It depends on the tax problem being solved.

Equipment may be strongest when the taxpayer has active business income, a real capital need, and a reason to accelerate deductions now.

Real estate may be strongest when the taxpayer wants a multi-year planning asset and is prepared to coordinate depreciation, participation, liquidity, and exit design.

Equity investments may be strongest when flexibility, timing control, and liquidity are more valuable than immediate ordinary-income reduction.

The real planning discipline is to compare each asset across the full cycle:

Acquisition-year benefit

Holding-period durability

Exit-year pressure

That is how we distinguish a tax benefit from a tax strategy.

Choosing the right asset for your tax profile means preserving flexibility while improving after-tax outcomes. The strongest plans do not maximize one-year deductions in isolation. They coordinate income character, loss usability, liquidity, structure, and exit timing so the taxpayer is not solving today’s tax pressure by creating tomorrow’s planning constraint.

Frequently Asked Questions

How should a high-income taxpayer decide whether to pursue tax reduction or preserve flexibility?

We would first separate current-year tax pressure from multi-year strategic value. Equipment may create a stronger near-term deduction profile, while real estate may support a longer planning arc through depreciation, leverage, and exit design. Equity investments may preserve liquidity and realization control when the taxpayer expects uncertain timing, future capital needs, or other major transactions. The right choice depends on whether the immediate tax benefit is worth the capital commitment, reduced flexibility, and future unwind consequences that come with the asset.

Is real estate still strategically useful if the depreciation losses are not immediately usable?

Yes, but the strategy should be framed differently. A real estate loss that is suspended is not the same as a current-year ordinary-income offset, yet it may still have future planning value within a broader ownership and disposition strategy. The key is to know which benefit is actually being pursued: immediate tax reduction, portfolio-level income shielding, or future release potential at exit. We would not treat a deferred benefit as though it solved a current-year tax problem unless the taxpayer’s facts support that result.

When does liquidity matter more than an accelerated deduction?

Liquidity becomes more important when the taxpayer may need capital for a business opportunity, future tax payment, acquisition, debt reduction, family planning event, or a better investment entry point. A front-loaded deduction can be valuable, but it may be less attractive if it requires locking capital into equipment or real estate before the broader plan is stable. Equity investments may be the better fit when timing control and optionality carry more strategic value than an immediate deduction. Tax efficiency should be evaluated alongside the flexibility the taxpayer gives up.

How should NIIT affect the choice between real estate and equity investments?

NIIT should be viewed as part of the exit-year and income-stacking analysis, not as an isolated surcharge. Equity sales, real estate gains, and certain rental income can become more consequential when they land in a year that already includes elevated income. For that reason, the asset decision should consider not only whether a gain may eventually arise, but also when that gain is likely to be recognized and what else may occur in the same year. A flexible asset is more valuable when it gives the taxpayer better control over that timing.

Why can an asset that is tax-efficient at purchase become less efficient later?

Because the tax benefit and the tax cost often appear in different years. Equipment may produce a strong deduction early but create recapture exposure when disposed of. Real estate may deliver depreciation benefits during ownership but generate a more layered exit-year result involving gain, prior depreciation, and NIIT considerations. Equity investments may defer gains for years but create tax concentration if appreciated positions are liquidated alongside other major events. A strategy is stronger when the acquisition-year benefit and exit-year consequences are evaluated together.

Should ownership structure be reviewed before choosing the asset?

Yes. Asset selection and ownership structure should be evaluated together because the structure affects who receives the income, who benefits from deductions, where basis resides, and how gain or loss appears at exit. The same investment can produce a materially different planning result depending on whether it is held personally, through an operating entity, through a real estate structure, or in another ownership arrangement. Reviewing structure after the asset is already acquired can narrow flexibility and make an otherwise reasonable investment less effective from a tax-planning perspective.

Does Florida’s no-personal-income-tax environment make real estate the obvious choice?

No. Florida’s tax environment makes federal tax sequencing especially important, but it does not automatically make real estate the best asset for every high-income taxpayer. Real estate may be attractive when the hold period, liquidity plan, depreciation posture, and exit design work together. But Florida-specific concerns—real estate concentration, homestead versus non-homestead economics, reserves, insurance pressure, and potential hold-period changes—can make a tax-favored acquisition less durable than it first appears. The absence of state income tax does not eliminate the need for balance-sheet discipline.