Real Estate Professional Status: When It Works, Where It Breaks, and How to Plan Around It

Real Estate Professional Status has value only when it aligns with the full sequence of tax classification, deduction usability, and eventual exit planning.

Real Estate Professional Status can be valuable, but its strategic use, limitations, and common planning errors are often misunderstood. Under the federal passive activity rules, it is a taxpayer-level classification that can change how rental real estate losses are treated. It matters only when the taxpayer qualifies for the status in that year and materially participates in the rental activity being tested, either property by property or through a valid rental real estate aggregation election.

For a high-income investor, the immediate answer is usually this:

| Question | Practical Answer |

|---|---|

| Can Real Estate Professional Status make rental losses nonpassive? | Potentially, yes, but only if the status test and the material participation test are both satisfied. |

| Does the status automatically allow losses to offset wages or business income? | No. Basis, at-risk, former passive activity rules, and other limitations may still control the result. |

| Is the status permanent once claimed? | No. It is tested annually. |

| Does it automatically eliminate NIIT? | No. NIIT requires a separate analysis. |

| Does it automatically release prior suspended passive losses? | No. Prior passive losses can remain constrained under the former passive activity rules. |

Those distinctions are what separate a defensible multi-year strategy from a filing-season assumption. A taxpayer may qualify in one year, fail in another, generate large deductions that are not currently usable, or make a grouping election that helps annual loss treatment but reduces flexibility when a property is sold later.

For Florida taxpayers, that sequencing matters even more. Florida does not impose a personal income tax, so federal income-tax classification often carries a larger share of the planning burden than it would in a state where income-tax planning also occurs at the state level. The real question is not whether Real Estate Professional Status sounds attractive. It is whether the classification improves the taxpayer’s after-tax position across acquisition, operation, and exit without creating a less flexible plan later.

Key takeaways

Real Estate Professional Status is an annual, taxpayer-level classification. It is not a permanent designation and not a label that attaches to a property.

Status alone is not enough. Rental losses become nonpassive only when the qualifying taxpayer also materially participates in the rental activity being tested.

The aggregation election can make material participation easier to establish across a rental portfolio, but it should be evaluated as a future disposition decision, not just a current-year deduction tool.

Prior suspended passive losses do not automatically become broadly deductible once the taxpayer qualifies later. Former passive activity rules can limit how they are used.

NIIT is a separate layer. Nonpassive treatment under section 469 does not, by itself, complete the NIIT analysis.

The strongest planning model tests Real Estate Professional Status against the full sequence: current-year loss usability, documentation durability, short-term rental classification, and exit-year tax pressure.

Real Estate Professional Status: the rule is narrower than its reputation

A taxpayer qualifies as a real estate professional for the year only if both of the following tests are met:

More than half of the personal services performed in all trades or businesses during the year are performed in real property trades or businesses in which the taxpayer materially participates.

The taxpayer performs more than 750 hours of services during the year in real property trades or businesses in which the taxpayer materially participates.

The second test receives most of the attention. For many high earners, the first test is more decisive. A founder, physician, attorney, executive, or other professional can clear 750 real estate hours and still fail because non-real-estate work remains the majority of their trade or business service time.

The rule also narrows what counts:

Employee services in a real property trade or business generally do not count unless the taxpayer is a 5% owner of the employer.

On a joint return, one spouse must independently satisfy the status tests. A spouse’s hours may help with material participation in an activity, but they do not help the other spouse qualify as a real estate professional.

Real property trades or businesses include activities such as development, construction, acquisition, rental, operation, management, leasing, and brokerage, but the taxpayer still must materially participate in the relevant business for those service hours to count toward the status tests.

That distinction matters in planning conversations. Real Estate Professional Status is not a household label, not a portfolio label, and not a shorthand for “hands-on investor.” It is a specific annual federal tax classification that must be built on actual service time, actual business involvement, and a return position that remains supportable if examined later.

A useful planning posture starts with a practical diagnostic:

Who in the household is expected to qualify?

What qualifying real property trades or businesses generate that person’s hours?

Which rental activities are expected to become nonpassive?

Can the hours be substantiated with records that match the taxpayer’s real operating pattern?

If the deduction year is successful, what happens in the sale year?

That fifth question is often missing. It should not be.

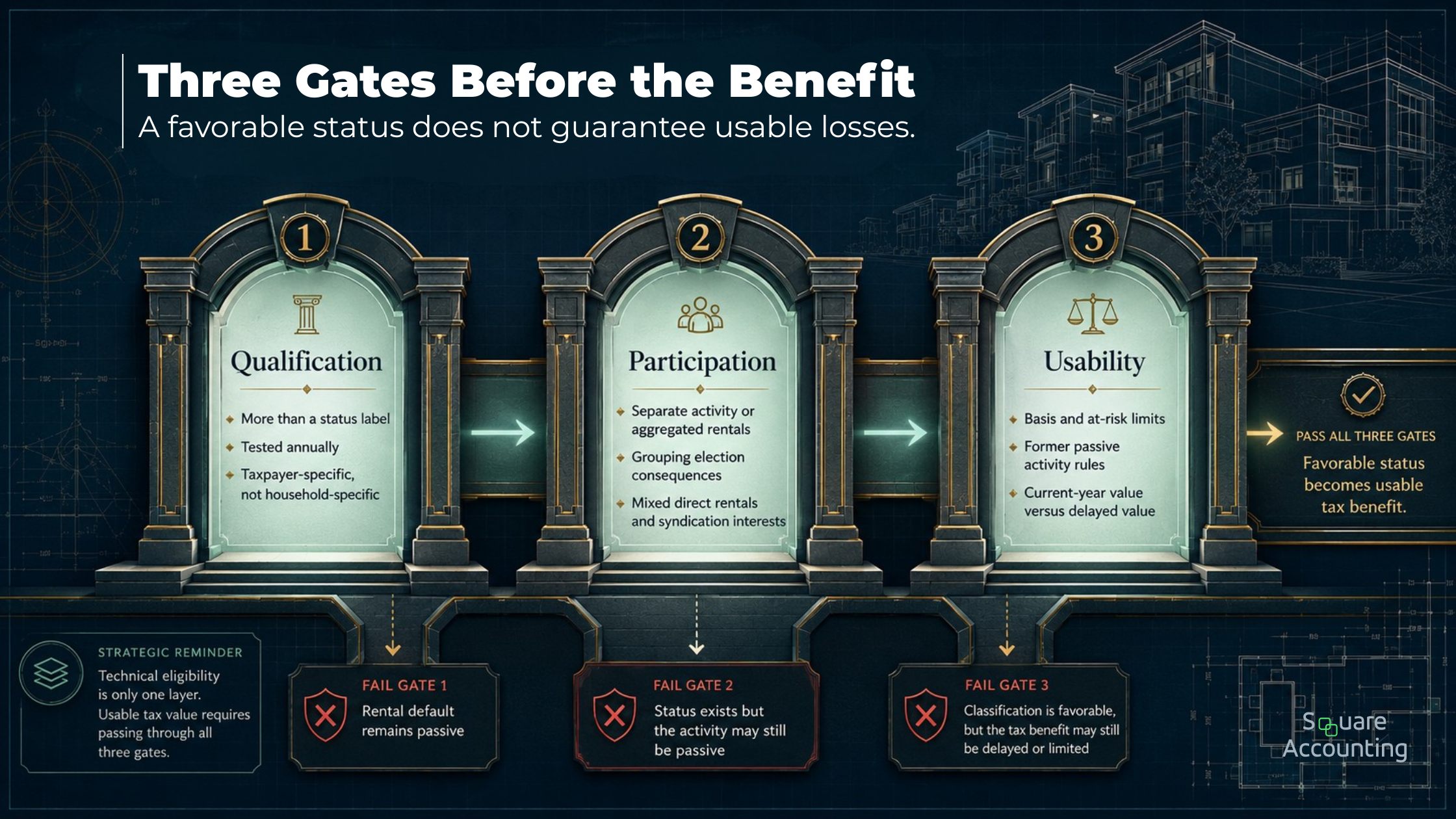

The three-gate framework: qualification, participation, usability

Many explanations of Real Estate Professional Status end after the 750-hour and more-than-half tests. For sophisticated investors, that is where the analysis starts. We use a three-gate framework because the tax outcome can fail at any one of these stages.

The tax result can fail at qualification, participation, or usability, which is why Real Estate Professional Status should be modeled as a sequence rather than a single checkbox.

For sophisticated investors, the analysis should not stop at whether the taxpayer qualifies. The more useful question is whether the status survives the next two planning gates and produces a result that is both usable and durable.

Gate 1: Did the taxpayer qualify for Real Estate Professional Status this year?

This is the annual classification test. It determines whether the taxpayer can move beyond the default rule that rental real estate is generally passive even when the owner is involved. A taxpayer who qualified last year does not carry the status forward automatically. The facts must support the status again for the current year.

This gate is especially important when the household’s work pattern is changing. A business sale, medical practice expansion, corporate role, sabbatical, relocation, or newly hired property management team can alter both the hour total and the more-than-half analysis. A plan that worked cleanly in one year may stop working the next.

The strategic point is simple: do not build a multi-year depreciation plan around a status that has only been modeled for one tax year.

Gate 2: Did the taxpayer materially participate in the relevant rental activity?

Even after the taxpayer qualifies as a real estate professional, each rental real estate interest is generally treated as a separate activity unless the taxpayer elects to treat all rental real estate interests as a single activity. Material participation is then measured at the activity level.

This is the reason many taxpayers use the rental real estate aggregation election. Without it, a taxpayer who owns several properties may qualify as a real estate professional but still fail to materially participate in one or more specific rentals when each property is tested separately. With a valid election, participation across the grouped rentals can be combined for the material participation analysis.

But aggregation is not merely an administrative convenience. It can reshape the future plan in at least three ways:

Annual loss treatment: It may make current nonpassive treatment more attainable across a portfolio.

Former passive activity tracking: Prior suspended losses may attach to the grouped activity rather than remaining economically intuitive property-by-property buckets.

Disposition flexibility: Because the grouped rentals are treated as one activity for section 469 purposes, a later sale of one property may not function like a complete disposition of the entire activity. That means the suspended-loss release analysis can differ from what the taxpayer expected if the future exit path was never modeled.

That last point is often underappreciated. The regulations and IRS guidance do not say, in plain planning language, “aggregation may reduce flexibility on a partial sale.” But that is the practical issue that follows from treating multiple rentals as a single activity while loss release generally turns on disposing of the taxpayer’s entire interest in the passive or former passive activity. We view that as a planning inference that deserves explicit modeling before the election is made.

The election also becomes more complicated when the taxpayer owns both directly managed rentals and limited partnership or syndication interests. If a taxpayer elects to aggregate rental real estate and at least one included interest is held as a limited partnership interest, the combined activity is generally treated as a limited partnership interest for material participation purposes. The regulation provides a de minimis exception when the taxpayer’s share of gross rental income from limited partnership rental interests is less than 10% of gross rental income from all rental real estate interests for the year. That exception is technical, but the planning implication is straightforward: combining direct rentals and passive syndication interests without modeling the regulatory interaction can make the material participation argument weaker, not stronger.

Our planning lens helps clarify whether your rental structure, participation facts, and hold assumptions work together.

Gate 3: If the loss becomes nonpassive, is the tax benefit actually usable?

A nonpassive classification is not the same as a currently deductible tax benefit. Other limitations can still delay, reduce, or block the expected result.

The most important checks are:

Does the taxpayer have sufficient basis?

Do the at-risk rules limit the loss?

Is the loss current-year nonpassive loss or prior-year suspended passive loss from a former passive activity?

Is the taxpayer assuming that a return classification automatically creates cash-flow value this year when it may only change the order in which tax attributes are used?

The former passive activity rule is especially important. If a rental activity was passive in an earlier year and is nonpassive in the current year, prior-year unallowed passive losses from that activity generally offset current-year net income from that same former passive activity. Any remaining prior-year unallowed loss continues to be treated as passive. That is materially different from the idea that a later Real Estate Professional Status year broadly unlocks all historic passive losses against wages or business income.

This is where tax planning often breaks. The household may be focused on “qualifying,” while the more important question is whether the expected loss is:

Characterized as nonpassive,

Allowed after basis and at-risk limitations, and

Valuable in the year the plan is supposed to matter.

If those three are not modeled together, Real Estate Professional Status may be technically correct but strategically overvalued.

Once those three gates are clear, the next question is timing: how the position behaves in the acquisition year, the operating years, and the eventual exit year.

See how we connect status, participation, grouping, and future disposition in one planning sequence.

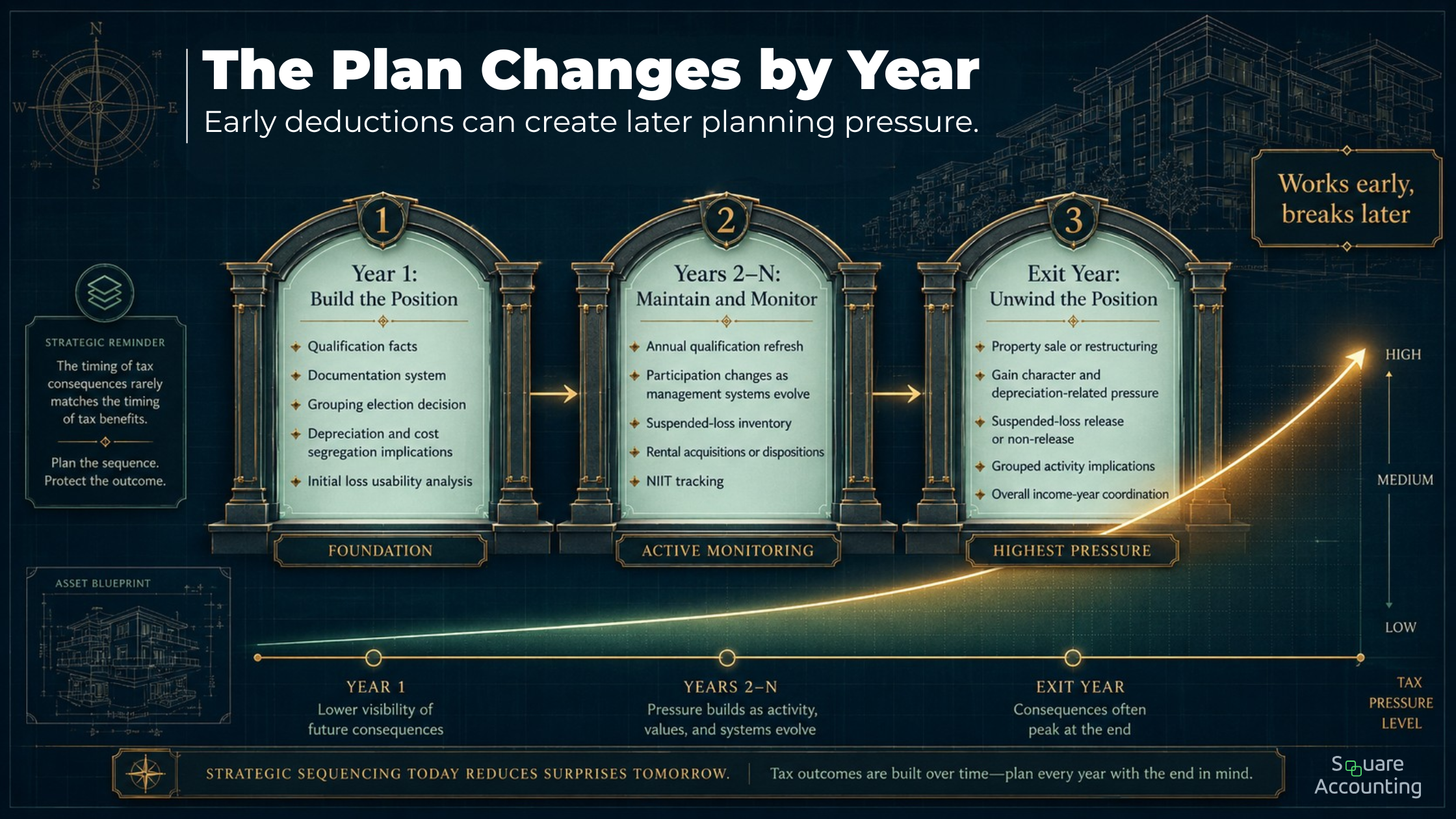

The multi-year sequence most tax plans skip

Real Estate Professional Status is usually discussed as a current-year deduction tool. For a high-income investor, that framing is too narrow. The more useful model follows the life of the strategy.

A Real Estate Professional Status strategy should be tested across the full hold period because the acquisition year, operating years, and exit year raise different tax questions.

The planning issue changes as the portfolio matures. A deduction that looks efficient in Year 1 may become less flexible later if participation drops, a grouping election constrains exit options, or a sale year compresses several tax consequences into one return.

Year 1: Qualification and structural setup

The first year is where the taxpayer determines whether Real Estate Professional Status is worth pursuing at all. It is also where the planning architecture is easiest to get right and hardest to unwind later.

Year 1 should answer:

Can one taxpayer in the household genuinely satisfy the status tests?

Which real property trades or businesses create the qualifying hours?

Which rentals are expected to be materially participated in?

Should rental real estate activities be kept separate or aggregated?

Will current-year losses be usable after basis, at-risk, and passive activity rules are applied?

Is the plan relying on accelerated depreciation or cost segregation in a year when the taxpayer’s factual qualification is still uncertain?

These are not return-preparation questions. They are design questions.

Recordkeeping also matters in a different way than many taxpayers assume. The regulations allow participation to be established by reasonable means, and contemporaneous daily logs are not the only acceptable evidence. Still, the stronger planning posture is prospective documentation that reflects how the taxpayer actually operates: calendar records, project notes, emails, leasing work, repair coordination, vendor oversight, site visits, and property-management decisions.

Just as important, investor activity is not a substitute for operational participation. Reviewing financial statements, preparing personal analyses, and monitoring an investment in a nonmanagerial capacity generally do not count as participation unless the taxpayer is directly involved in day-to-day management or operations. For high-net-worth investors who are economically engaged but operationally removed, that distinction can be decisive.

A refined planning question for Year 1 is:

Are we documenting a business-operating reality, or are we trying to fit investment oversight into an operating standard?

Those are very different positions.

Year 2 and beyond: Maintain the status, but also track the loss inventory

Real Estate Professional Status is tested annually. A taxpayer can qualify in Year 1, fail in Year 2, and qualify again in Year 3. The tax plan must be able to absorb that possibility rather than assume a straight-line pattern.

The ongoing planning file should track at least four moving pieces:

Annual status qualification: Did the taxpayer still satisfy both statutory tests?

Material participation by activity or grouped activity: Did the operational facts remain consistent?

Loss inventory: Which losses are current-year nonpassive losses, which remain suspended passive losses, and which are former passive activity losses subject to narrower use?

Portfolio changes: Were properties acquired, sold, moved into a different operating model, or mixed with interests held through passthrough entities?

This is where fragmented planning becomes expensive. A taxpayer may have one advisor reviewing cost segregation, another evaluating entity structure, and another preparing the return. Without a single loss inventory and participation model, the pieces can be individually defensible but strategically disconnected.

A common pattern looks like this:

Year 1: The taxpayer qualifies, materially participates, and uses current depreciation-driven losses.

Year 2: The taxpayer still owns the properties but participation declines after hiring more management help.

Year 3: One property is sold, but the taxpayer’s grouped-activity election and suspended-loss history were never projected against the sale.

The problem is not that any single year was necessarily wrong. The problem is that the strategy was never maintained as a living multi-year tax position.

Exit year: The deduction strategy meets the disposition strategy

The sale year is where a deduction-centered Real Estate Professional Status plan is stress-tested.

A rental real estate exit can involve several distinct layers:

Appreciation gain,

Gain attributable to prior depreciation, including unrecaptured section 1250 gain concepts,

Suspended passive loss release rules,

Former passive activity mechanics,

NIIT treatment,

Timing choices around the taxpayer’s overall income picture for that year.

The strategic issue is not simply “tax on sale.” It is whether earlier deduction planning has created exit-year pressure that was never modeled. A taxpayer who accelerated depreciation may have improved the current-year tax result, but the future sale analysis must still address the character and timing of gain, the availability of suspended losses, and whether the disposition creates or fails to create the desired release event.

Grouping elections are central here. If rental properties were aggregated into one activity, and the taxpayer later sells only one property, the tax analysis may differ from the taxpayer’s intuitive view that “I sold the asset, so the suspended losses should free up.” The complete-disposition rule generally turns on disposing of the entire interest in the passive or former passive activity, not merely selling one property that happens to sit inside a broader grouped activity.

A better exit-year model asks:

What gains are expected on the sale?

What portion relates to prior depreciation?

Which suspended losses, if any, are available because the relevant activity has been disposed of in full?

How does the aggregation election affect that conclusion?

What NIIT analysis applies to the sale and to any operating income in the same year?

This is the point where Real Estate Professional Status stops being a classification question and becomes a portfolio sequencing question.

We look beyond the deduction year to the grouping, gain, and suspended-loss issues that can surface later.

Short-term rentals: a different classification path, not a Real Estate Professional Status shortcut

Short-term rentals deserve separate treatment because they are often discussed beside Real Estate Professional Status as though they are variations of the same strategy. They are not.

For section 469 purposes, an activity involving customer use of property is not treated as a rental activity if the average period of customer use is seven days or less. A separate exception can apply when the average period of customer use is 30 days or less and significant personal services are provided.

That matters because a short-term rental that falls outside the rental-activity definition is analyzed differently from a long-term rental that remains inside the rental bucket. The passive outcome then turns on material participation under the applicable non-rental activity rules, rather than on Real Estate Professional Status removing the default passive treatment of rental real estate.

For Florida investors, this distinction is practical. A portfolio may contain:

Long-term residential rentals,

Seasonal or vacation rentals,

A short-term rental with substantial owner involvement,

A syndication interest or other passive real estate exposure.

Those assets may look similar on a balance sheet but behave very differently under the passive activity rules. Treating them as one generic “real estate strategy” can produce the wrong tax conclusion.

The planning error is not merely using the wrong label. It is building a depreciation, loss, or exit plan around the wrong classification path. Short-term rental treatment can be useful, but it should not be used as a substitute for analyzing whether the activity actually meets the customer-use and participation rules that drive the tax result.

We help distinguish when Real Estate Professional Status, short-term rental treatment, or a different sequencing issue deserves attention.

NIIT: nonpassive is not the final answer

The Net Investment Income Tax requires its own analysis. The NIIT applies at a 3.8% rate to certain net investment income of individuals, estates, and trusts whose income exceeds the statutory thresholds. Rental income and gain from real estate can fall within that framework depending on the facts.

Real Estate Professional Status can matter for NIIT, but it does not automatically resolve the issue. Treasury regulations provide a safe harbor for certain real estate professionals. In general, a real estate professional who participates in a rental real estate activity for more than 500 hours in the current year, or for more than 500 hours in any five of the prior ten taxable years, can treat qualifying gross rental income and disposition gain from that activity as derived in the ordinary course of a trade or business for this purpose. The same regulations also state that failing the safe harbor does not necessarily end the analysis; the taxpayer may still establish a non-NIIT result under other applicable provisions.

This creates a planning tension that is often missed:

A taxpayer may satisfy the Real Estate Professional Status tests.

The rental activity may be nonpassive for section 469 purposes.

The NIIT conclusion may still require a separate safe-harbor or ordinary-course analysis.

Those are not interchangeable determinations. They are related, but not identical.

For exit planning, we separate three questions:

What is the character of the gain, including depreciation-related character?

What suspended or former passive losses interact with the sale?

What portion of the income or gain remains inside the NIIT framework?

A reader who already has a CPA should care about this separation. Many tax plans are “correct” in their passive activity treatment but incomplete in their NIIT modeling, especially when rental income, sale gain, and a large non-real-estate income year converge.

Common misuse and oversights sophisticated taxpayers still make

1. Treating 750 hours as the whole test

The 750-hour requirement is only one part of the status analysis. The taxpayer must also perform more than half of all personal services in real property trades or businesses in which they materially participate. For a high-income taxpayer with substantial non-real-estate work, that first test can be the actual constraint.

2. Counting economic attention as operational participation

Being deeply engaged with a portfolio is not the same as materially participating in an activity. Reviewing reports, comparing yields, analyzing refinancing options, and monitoring returns may be commercially important, but investor activity generally does not count unless the taxpayer is directly involved in day-to-day management or operations.

3. Using spouse hours incorrectly

On a joint return, one spouse must independently satisfy the Real Estate Professional Status tests. The other spouse’s service hours do not help with the more-than-half or 750-hour tests. Spousal participation can matter when testing material participation in the activity, but that is a separate step.

4. Making the aggregation election reflexively

Aggregation can make material participation more achievable across a rental portfolio, but it can also reshape former passive activity tracking, syndication interactions, and future disposition analysis. The election should be modeled against the portfolio’s likely hold and exit path, not made simply because it seems to support the deduction in the current year.

5. Assuming prior suspended losses automatically unlock later

When a formerly passive rental activity becomes nonpassive, prior-year suspended losses generally offset current-year net income from that same former passive activity first. Remaining prior suspended losses generally continue to be treated as passive losses. A later year of qualification does not automatically convert the entire historic passive-loss inventory into a broad shelter against unrelated nonpassive income.

6. Ignoring basis and at-risk limitations

Even when an activity is nonpassive, basis and at-risk rules can still limit the loss. A planning memo that says “the taxpayer qualifies” but does not test whether the anticipated loss is actually allowed in the intended year is incomplete.

7. Treating short-term rentals and Real Estate Professional Status as the same strategy

Short-term rental classification can create a different path to nonpassive treatment, but it is driven by the customer-use rules and material participation. It does not make the taxpayer a real estate professional, and it should not be used as a substitute for the status analysis where the taxpayer’s portfolio also contains traditional rentals.

8. Failing to model the exit year before claiming the deduction year

Depreciation-heavy planning can be valuable, but the sale year may involve unrecaptured section 1250 gain concepts, NIIT, gain timing, and suspended-loss release rules that interact differently depending on prior grouping and participation decisions. The relevant question is not only whether a deduction is available today. It is whether the cumulative plan remains efficient and flexible when the property is eventually refinanced, restructured, or sold.

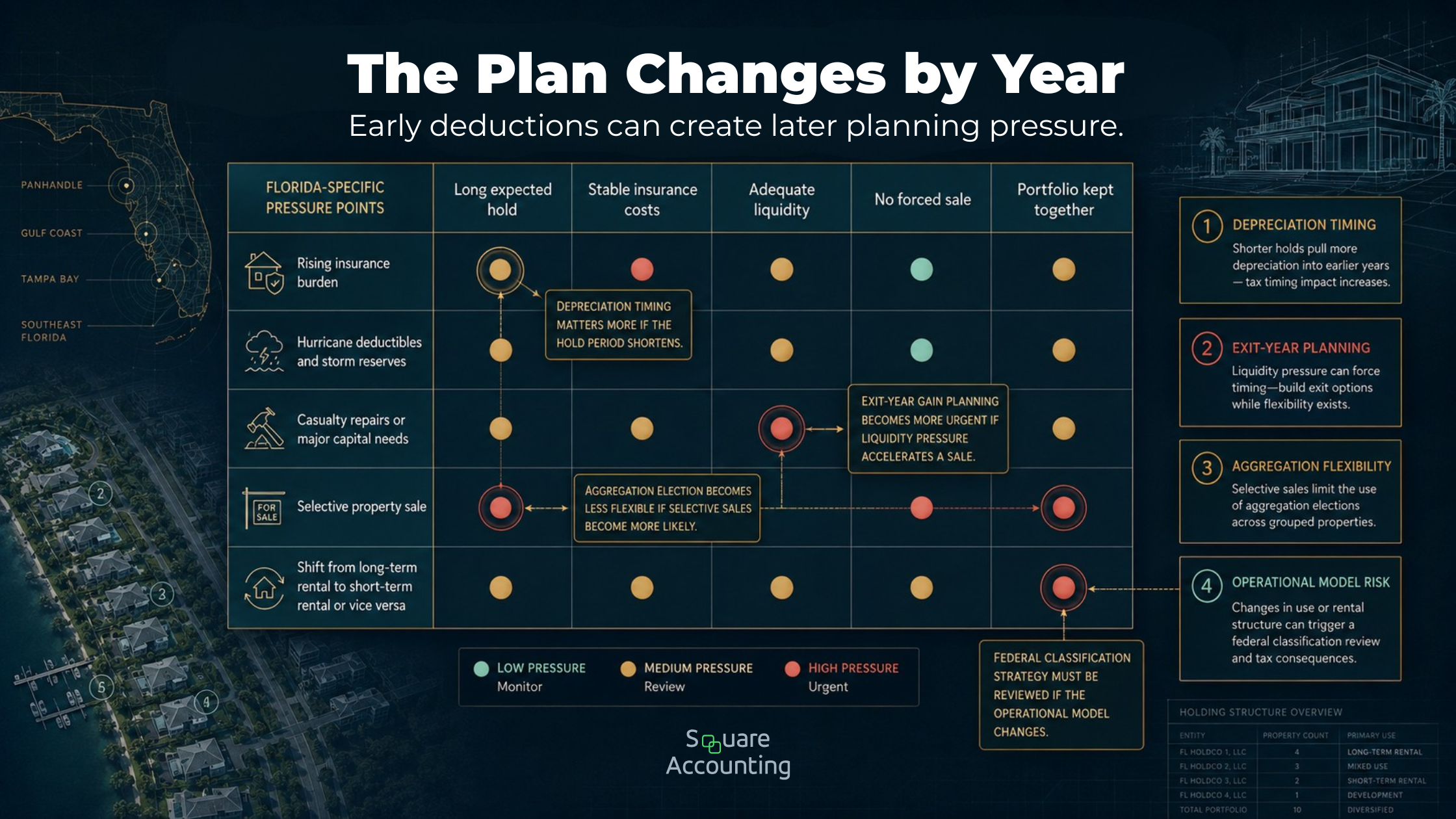

Florida-specific planning: why federal classification is only half the story

For Florida taxpayers, Real Estate Professional Status sits inside a broader real estate balance-sheet strategy.

Florida does not impose a personal income tax, which means federal tax planning often has an outsized role in the income-tax model. That can make section 469 classification, current-year loss usability, NIIT treatment, and sale-year gain character more consequential in the overall planning conversation.

At the same time, Florida investors should not confuse federal income-tax treatment with Florida property-tax economics. Homestead property receives a distinct assessment framework, while non-homestead residential property follows a different statutory regime. Those rules do not determine Real Estate Professional Status, but they can influence household liquidity, hold-versus-sell thinking, and how an investor compares principal-residence economics with rental-property economics.

Florida also adds operating variables that can disrupt a tax strategy built on a clean multi-year hold assumption. Insurance structure, hurricane deductibles, storm-related capital needs, and casualty-repair timing can all affect liquidity planning and, in some cases, the practical decision to keep or dispose of a property. Those are not Real Estate Professional Status rules, but they are relevant when the tax plan depends on a specific hold period or a specific exit year.

A federal tax strategy is more durable when it is stress-tested against the operating realities that may change a Florida investor’s hold period or exit plan.

These Florida-specific pressures do not rewrite the Real Estate Professional Status rules, but they can change the life of the strategy. When operating risk alters the expected hold period, the tax model should be revisited with the same discipline as the investment model.

This is especially important when a taxpayer’s plan relies on:

Front-loaded depreciation benefits,

An aggregation election that assumes the portfolio will be held as a block,

A projected sale year tied to income smoothing,

Or rental cash flow that may need to support larger reserves than originally modeled.

A tax strategy that assumes a seven-year hold can become less coherent if insurance pressure, capital needs, or storm-related repairs move the property into a two-year sale decision. The tax answer may still be technically correct, but the strategy may no longer match the asset.

Bring the full picture so we can evaluate classification, loss timing, NIIT, and likely exit pressure together.

Conclusion: Real Estate Professional Status belongs inside a coordinated plan

Real Estate Professional Status can be a meaningful planning tool for high-income real estate investors, but only when the facts support it and the broader plan is coherent.

The better question is not, “Can we claim Real Estate Professional Status?” It is:

Does this classification improve the taxpayer’s multi-year after-tax position once we account for material participation, grouping choices, current loss usability, NIIT, depreciation character, and the eventual exit?

The answer may be yes. It may also be yes for one year and less compelling for the next. That is why Real Estate Professional Status belongs inside a coordinated planning system rather than being treated as a standalone tax tactic.

The strongest plans integrate:

Qualification,

Activity classification,

Loss inventory,

Documentation,

NIIT analysis,

Property-level hold and sale assumptions,

And enough flexibility to adapt when the real estate plan changes.

That is where Real Estate Professional Status becomes strategically useful: not as a status to chase, but as one component in a tax plan that holds together from acquisition through exit.

We can examine whether your current real estate tax position is coordinated across acquisition, operation, and exit.

Real Estate Professional Status Planning FAQs

Key questions for high-income real estate investors evaluating loss usability, aggregation, syndications, cost segregation, Florida property durability, and multi-year tax strategy.

Can Real Estate Professional Status still matter if my portfolio already produces strong cash flow?

Yes. The value is not limited to portfolios generating large current losses. We would still evaluate how the status affects depreciation-driven deductions, grouping choices, future suspended-loss treatment, NIIT analysis, and the tax character of a later sale. A profitable portfolio can still have timing mismatches between taxable income, depreciation, and liquidity. The question is whether the classification improves the portfolio’s multi-year tax efficiency without narrowing flexibility when assets are refinanced, restructured, or sold.

If I qualify in one year but not the next, does that damage the strategy?

It can change the strategy materially, but it does not automatically invalidate prior-year treatment. Real Estate Professional Status is tested annually, so the planning model should expect that qualification may vary with work patterns, management delegation, acquisitions, or business demands. If qualification drops away in a later year, rental activities may revert to passive treatment unless another classification path applies. We would focus on how that shift affects current losses, suspended-loss accumulation, and the taxpayer’s expected sale or restructuring timeline.

Should I aggregate rental activities if I plan to sell properties selectively over time?

That is exactly where the aggregation election deserves more scrutiny. Aggregation can support material participation across a portfolio, but it may also reduce the clarity of property-by-property exit planning. If the grouped rentals are treated as one activity, selling a single property may not create the same suspended-loss release result the taxpayer expected from a complete disposition framework. We would compare the annual tax benefit of aggregation with the likelihood of partial sales, staggered exits, or changing investment priorities.

How should syndication interests be viewed alongside directly managed rentals?

They should not be treated as economically similar assets for participation planning simply because both are real estate exposures. Directly managed rentals may support an operational participation argument, while syndication or limited partnership interests often sit in a different posture. Mixing them into a broader grouping analysis can create complications, especially where the material participation standards become less favorable. We would separate investment exposure from operational involvement before deciding whether the broader rental structure supports the intended tax position.

Does a large cost segregation study make Real Estate Professional Status more valuable?

Potentially, but only if the deduction is actually usable and the broader position is supportable. A larger depreciation benefit can magnify the importance of status, material participation, basis, at-risk limits, and documentation. It can also increase the cost of getting the sequencing wrong. We would test whether the projected deduction fits the taxpayer’s current-year income profile, whether it depends on a fragile participation position, and how the accelerated depreciation affects eventual exit-year gain analysis.

How should Florida investors think about Real Estate Professional Status when insurance or reserve needs are rising?

The tax position should be tested against the operating plan, not in isolation. If insurance costs, catastrophe reserves, or major capital needs shorten an expected hold period or force liquidity decisions sooner than planned, the tax strategy may need to be revisited. A deduction-focused model that assumes a long, stable hold can become misaligned when the asset’s risk profile changes. We would connect the federal tax classification to the property’s durability as an investment, including whether future sale timing remains realistic.

Can a Real Estate Professional Status plan be technically correct but strategically weak?

Yes. A taxpayer may satisfy the formal tests and still have a plan that is poorly coordinated. Examples include qualifying in a year when the expected losses are limited elsewhere, making an aggregation election without modeling exit flexibility, or treating nonpassive status as though it automatically resolves NIIT. We would call that strategically weak because the tax classification is being evaluated separately from cash flow, sale timing, loss inventory, and portfolio structure. The stronger approach is integrated rather than merely technically compliant.