Aligning Ownership Structure With Succession, Gifting, and Estate Planning Goals

Aligning ownership structure with succession, gifting, and estate planning goals means designing ownership so the next transfer works before it happens.

For a high-income Florida taxpayer, the planning question is not simply, “Should this asset be in an LLC, trust, corporation, or individual name?” The stronger question is:

Will this ownership structure still work when we gift interests, shift control, refinance, sell, die, divide assets among heirs, or bring a successor into management?

That is where many otherwise sophisticated plans break down. A structure may work for liability separation, income reporting, or probate avoidance today, but create pressure later when the family needs basis planning, estate liquidity, valuation support, successor control, or a clean exit.

The immediate answer: ownership structure should be designed around the next likely transfer event. That event may be a gift, death, sale, refinance, buyout, leadership transition, or forced liquidity decision. If the structure is not tested against that event, it may be organized but not aligned.

A strong ownership structure should be tested against the next transfer event before that event forces the decision.

Ownership structure should not be judged only by how it works today. It should be evaluated by how it performs when ownership, tax attributes, control, or liquidity must move.

Key Takeaways

Ownership structure should be tested against the next transfer event, not just the current tax return.

Lifetime gifts can move future appreciation, but they often carry over the donor’s basis to the recipient.

Transfers at death may provide a different basis result, but they can leave control, liquidity, and family governance problems unresolved.

Real estate structures need extra review because debt, depreciation, suspended losses, recapture, and exit timing can collide.

Business succession should separate leadership, voting control, economic ownership, and family fairness.

Florida’s lack of a state personal income tax makes federal planning more important, not less.

The best structure is usually not the one that minimizes one tax in one year. It is the one that preserves flexibility across ownership, tax, family, and exit decisions.

The Immediate Planning Framework

A useful ownership review starts with the next decision the family may need to make.

Structure Should Match the Next Ownership Event

A durable structure should be tested against the next likely transition, not only the current tax year.

| If the Next Event Is... | The Structure Should Answer... | Planning Friction to Test |

|---|---|---|

| Lifetime Gift | What interest is being transferred, and what tax attributes move with it? | Carryover basis Valuation Voting rights Cash flow Debt exposure |

| Death Transfer | Who receives ownership, who controls management, and what basis result is expected? | Liquidity Estate administration Successor readiness Family governance |

| Business Succession | Is the successor receiving leadership, economics, or both? | Voting control Compensation Buy-sell rights Operating authority |

| Real Estate Exit | Can the asset be sold without creating avoidable conflict or tax concentration? | Depreciation recapture Unrecaptured Section 1250 gain NIIT Debt payoff |

| Refinance or Capital Call | Who is responsible for guarantees, reserves, and future contributions? | Unequal liquidity Lender consent Family disagreement |

| Equalization Among Heirs | Does equal ownership actually produce fair outcomes? | Illiquidity Management burden Buyout needs Asset concentration |

The next likely transfer event should determine which ownership risks need to be tested first.

The same ownership structure can behave differently depending on the next event. A gift, refinance, sale, or death transfer may stress different parts of the plan.

Use the control, economics, basis, and liquidity framework to identify where your current ownership structure may need closer review.

For 2026 planning, the federal estate and gift tax basic exclusion amount is $15 million, and the annual gift tax exclusion remains $19,000 per donee. Those numbers matter, but they should not drive the structure by themselves. The more important planning issue is how ownership affects control, basis, liquidity, governance, and future tax character.

A high exemption can reduce immediate estate tax pressure. It does not remove the need to coordinate ownership.

Why Ownership Structure Is a Succession Decision, Not Just an Entity Decision

Many sophisticated taxpayers already have entities in place.

They may own rental real estate through LLCs, operating businesses through S corporations or partnerships, investment assets in taxable accounts, and family wealth through revocable trusts or other estate planning vehicles.

The issue is rarely whether an entity exists.

The issue is whether the entity still matches the family’s future transfer goals.

An LLC can separate liability but fail to define successor control. A revocable trust can avoid probate but fail to solve business leadership. An S corporation can support payroll and operating income but create transfer restrictions if future owners are not eligible shareholders. A partnership can provide allocation flexibility but become difficult to administer if family members receive interests without understanding debt, capital accounts, or distribution policy.

That is why aligning ownership structure with succession, gifting, and estate planning goals is not a document cleanup project. It is a transfer architecture project.

The structure should make clear:

Who controls the asset.

Who receives income and appreciation.

Who bears debt and capital obligations.

What basis and tax attributes transfer.

Who can force or block a sale.

How liquidity will be created when the plan reaches a stress point.

If those answers are not coordinated, the plan may look complete but become difficult to execute.

The Control, Economics, Basis, and Liquidity Map

A strong succession-oriented ownership structure separates four planning layers that are often blended together.

1. Control

Control determines who can sell, refinance, admit new owners, approve distributions, hire management, change strategy, or amend governing documents.

For business owners, control may need to remain with the founder while economic ownership gradually shifts to children, trusts, or successors. For real estate investors, control may need to remain centralized so one heir cannot force a sale, disrupt financing, block a refinancing, or override a portfolio-level hold strategy.

Control can be handled through voting and nonvoting interests, manager-managed LLCs, shareholder agreements, buy-sell agreements, trustee powers, consent rights, or family governance documents.

The mistake is assuming ownership automatically means management should transfer.

A child, trust, or successor may be the right economic recipient but not the right decision-maker. Conversely, a key employee or family member may be the right manager but not the intended long-term owner.

That distinction should be built into the structure before gifts or transfers occur.

2. Economics

Economics determines who receives income, appreciation, losses, distributions, and sale proceeds.

This is where planning becomes more nuanced. A parent may want to transfer appreciation to children but retain income. A business owner may want a successor to participate in growth but not receive full voting power. A real estate investor may want heirs to inherit ownership but not be burdened with unexpected capital calls or personal guarantees.

The ownership structure should define whether the transferred interest includes:

Current cash flow

Future appreciation

Voting authority

Debt exposure

Capital contribution obligations

Sale proceeds

Buyout rights

Distribution preferences

Restrictions on transfer

Without that clarity, “succession planning” can become a future dispute about expectations.

A structure that gives everyone equal economics may still create unequal consequences. One heir may work in the business. Another may not. One may have liquidity to fund capital calls. Another may need distributions. One may want to hold a property for 15 years. Another may want a sale in 18 months.

The economic structure should reflect the actual family and investment reality.

3. Basis

Basis is often the hidden tax variable in succession planning.

The federal gift and estate tax system generally applies a unified framework, with credit applied against taxable lifetime gifts and any remaining credit applied at death. But income tax basis does not always follow the same planning logic.

For property received by gift, the recipient generally needs to consider the donor’s adjusted basis, the property’s fair market value at the time of the gift, and any gift tax paid. In many appreciated-asset situations, this means the recipient may take the donor’s basis for gain purposes.

For inherited property, basis is generally the fair market value on the date of death or the alternate valuation date if properly elected.

That difference can materially change the planning outcome.

A lifetime gift may reduce estate exposure but preserve built-in gain. A transfer at death may preserve estate inclusion but improve basis. The better answer depends on asset appreciation, expected estate size, projected sale timing, depreciation history, cash flow needs, and family objectives.

This is especially important for real estate. A property with low tax basis, large accumulated depreciation, or prior cost segregation may have a very different future tax profile than its current cash flow suggests.

4. Liquidity

Liquidity is what determines whether a plan can survive the real world.

A family may have substantial wealth on paper but limited cash. That is common among real estate investors, business owners, and families with concentrated closely held assets.

Liquidity planning should answer:

Who pays estate administration costs?

Who services debt if the key owner dies?

How will heirs be equalized if one receives the business and another receives investment assets?

What happens if a lender requires a refinance after ownership changes?

Can the estate or family pay tax, debt, operating costs, or buyout obligations without forcing a sale?

Are reserves adequate if Florida insurance, casualty, or property costs rise unexpectedly?

Can the structure tolerate a delayed sale, lower valuation, or market disruption?

A tax-efficient structure that creates liquidity pressure can become a forced-sale structure.

This is the blind spot in many plans. They move ownership but do not map the cash needed to hold, settle, unwind, or exit.

Gifting During Life vs. Transferring at Death

Lifetime gifting and estate transfers are not interchangeable. They solve different problems.

Transfer Strategy Should Match the Long-Term Objective

Each ownership transfer method can solve one planning issue while creating another. The structure should be tested before control, basis, liquidity, or family governance becomes constrained.

| Strategy | Potential Advantage | Potential Drawback |

|---|---|---|

| Lifetime Gift of Interests | Can shift future appreciation and begin succession earlier. | May carry over basis and reduce flexibility. |

| Transfer at Death | May provide a different basis result for appreciated assets. | May leave control transition unresolved. |

| Sale to Family or Trust | Can create defined economics and cash flow. | Requires valuation, documentation, and repayment discipline. |

| Gradual Transfer of Nonvoting Interests | Can shift economics while retaining control. | May create future governance tension. |

| Trust-Based Ownership | Can centralize control and preserve long-term intent. | Requires legal design that matches tax and family objectives. |

For 2026, the annual exclusion allows $19,000 per donee, but annual exclusion gifting is not a substitute for ownership design. It may help transfer modest amounts over time, but it does not automatically solve control, basis, valuation, liquidity, or successor governance.

The deeper question is not “How much can we gift?”

It is “Which interests should move, when should they move, and what tax attributes move with them?”

For a rapidly appreciating business, shifting future appreciation earlier may be a priority. For a low-basis real estate asset likely to be sold soon, preserving basis flexibility may matter more. For a family business, transferring economics without transferring leadership may be the right interim step. For a real estate portfolio, retaining centralized control may be more important than equal legal ownership.

The structure should reflect the next phase, not just the available exclusion amount.

Review how control, basis, liquidity, and governance may interact before ownership interests move.

The “Works Early, Breaks Later” Pattern

A structure often looks successful in the early years because it solves the immediate problem.

An LLC may separate liability.

A trust may avoid probate.

An S corporation may support payroll and operating income.

A partnership may allow flexible allocations.

A family entity may centralize asset management.

But the structure may break later if it was not built for the next event.

A structure can solve the first planning problem while quietly creating pressure for the year ownership must transfer or unwind.

The failure point often does not appear when the entity is formed. It appears when the structure must handle valuation, debt, control, tax attributes, and liquidity at the same time.

Year 1: The structure solves the current issue

The owner forms entities, separates assets, creates an estate plan, and begins basic tax coordination.

This can be a meaningful improvement over owning everything personally or informally. But the structure is still incomplete if it does not address future transfers.

The question at this stage is not only whether the legal structure is valid. It is whether the structure can support future gifts, successor authority, lender requirements, tax reporting, and family governance.

Year 2 to Year 5: Gifting begins

The owner starts transferring interests to children, trusts, or successors.

Now the structure must handle valuation, distributions, voting rights, income tax allocations, state law restrictions, debt guarantees, capital accounts, and documentation. If those details were not built into the operating agreement, shareholder agreement, trust document, or buy-sell arrangement, the plan becomes harder to administer.

This is where informal family assumptions often become technical tax and governance problems.

A parent may believe a child received “part of the business.” The documents may say the child received a nonvoting economic interest. The CPA may be allocating income. The estate attorney may be tracking gift values. The lender may still require the parent’s guarantee. The successor may believe leadership is implied.

If those views are not aligned, the structure starts to drift.

Exit year or death year: The hidden issues surface

The family sells a property, refinances a portfolio, transfers control, settles an estate, or negotiates a buyout.

This is where basis, depreciation history, recapture, NIIT, suspended losses, debt payoff, transfer restrictions, and liquidity pressure can collide. The Net Investment Income Tax applies at 3.8% to certain net investment income when income exceeds statutory thresholds, and the IRS describes net investment income as including categories such as interest, dividends, capital gains, rental income, royalty income, and nonqualified annuities.

For real estate owners, the exit year may also bring depreciation recapture and unrecaptured Section 1250 gain considerations. For business owners, the transition year may involve compensation, redemption payments, installment sale planning, debt release, goodwill, or buyer due diligence.

The problem is not always that the original structure was wrong.

The problem is that it was never stress-tested against the year when ownership has to move, unwind, or convert into cash.

We can help evaluate whether your ownership structure still fits your next transfer, exit, refinancing, or succession event.

Real Estate Ownership Requires Extra Coordination

Real estate succession planning is different from passing down marketable securities.

A rental property or real estate partnership interest may carry:

Depreciation history

Debt and guarantees

Suspended passive losses

Cost segregation history

1031 exchange history

Refinance exposure

Capital improvement obligations

Insurance and reserve needs

Potential depreciation recapture

Unrecaptured Section 1250 gain considerations

NIIT exposure for high-income taxpayers

Management and leasing obligations

Unequal liquidity needs among heirs

This means ownership structure should be reviewed before major planning moves, not after.

For example, gifting part of an LLC that owns appreciated real estate may shift future appreciation. But it may also transfer an interest with embedded debt, low basis, future capital calls, and limited marketability. If the family expects a sale in the next few years, the income tax consequences may matter more than the estate tax savings.

A real estate structure should be tested against at least three timelines:

The hold timeline: Can the family continue owning and operating the asset?

The transfer timeline: Can interests be gifted or inherited without governance problems?

The exit timeline: Can the asset be sold, refinanced, exchanged, or restructured without creating avoidable tax concentration or family conflict?

For Florida real estate investors, this is especially important because wealth is often concentrated in a few illiquid assets. A family may be asset-rich but not liquid enough to absorb insurance changes, major casualty repairs, refinancing pressure, or a forced buyout.

The ownership structure should not assume that the intended hold period will always survive the operating environment.

Continue reviewing how entity structure, basis, NIIT, recapture, and Florida real estate concentration can affect long-term planning.

Business Succession: Ownership Does Not Equal Leadership

For closely held businesses, succession planning often fails because ownership and leadership are treated as the same issue.

They are not.

A child may be ready to own economics but not ready to run the company. A senior employee may be capable of leading operations but not intended to inherit family wealth. A spouse may need income protection but not management responsibility. Multiple children may need equal economic treatment but different control rights.

A better structure distinguishes:

Voting interests

Nonvoting interests

Management roles

Compensation arrangements

Buy-sell rights

Transfer restrictions

Redemption terms

Key-person risk

Estate equalization

Successor accountability

For a high-income business owner, the succession question is not only “Who gets the company?”

It is also:

Who can make decisions?

Who receives income?

Who bears risk?

Who can sell?

Who must be bought out?

Who signs debt or guarantees?

Who has employment rights versus ownership rights?

What happens if the founder dies before the transition is complete?

The tax structure should support the operating reality, not override it.

A common failure mode is transferring ownership before the company has a leadership transition plan. Another is keeping control too centralized for too long, leaving the business dependent on one person while the estate plan assumes continuity.

Ownership should be designed to support a staged transition, not a sudden handoff.

Portability Helps, But It Does Not Replace Structure

Married taxpayers often assume portability solves the estate tax issue.

Portability can be valuable. It may allow a surviving spouse to use a deceased spouse’s unused exclusion if the proper election is made on a timely filed estate tax return.

But portability does not solve every planning issue.

It does not automatically:

Create liquidity

Preserve GST planning

Resolve family governance

Fix basis problems

Protect a business from operational disruption

Equalize inheritances

Address state law restrictions

Coordinate real estate debt and guarantees

Decide who controls a closely held entity

Portability is a federal estate tax tool. It is not a complete succession plan.

For sophisticated families, the risk is not only paying estate tax. The risk is that a surviving spouse or next generation inherits a structure that is technically intact but strategically fragile.

Florida-Specific Planning Considerations

Florida changes the planning conversation in several ways.

Florida’s constitution limits state taxes on estates, inheritances, and the income of natural persons, which means federal income, estate, gift, GST, and NIIT planning often carry more of the strategic weight for Florida residents.

But Florida is not “simple” just because it has no state personal income tax.

Homestead needs special attention

Florida homestead can affect creditor protection, property tax treatment, and transfer planning.

For estate planning, the devise restrictions are especially important. Florida law provides that homestead is not subject to devise if the owner is survived by a spouse or minor child, except that it may be devised to the spouse if there is no minor child.

That means a homestead residence should not be treated like an ordinary investment asset in the estate plan.

Ownership changes, trust transfers, marital planning, and inheritance design should be coordinated with Florida counsel. A structure that appears tax-efficient may create legal or family-transfer issues if homestead rules are not considered.

Save Our Homes portability can influence relocation planning

Florida’s Save Our Homes assessment limitation and portability rules can influence decisions around moving, downsizing, or changing residences. Florida Revenue explains that eligible owners may be able to transfer all or part of the Save Our Homes benefit from an old homestead to a new homestead, lowering the assessment and potentially the taxes for the new homestead.

For high-net-worth families, this is not merely a property tax detail.

It can affect whether a residence is retained, sold, gifted, moved into trust, or repositioned as part of a broader estate plan. It can also affect liquidity and cash flow planning if a move changes the property tax profile of the family’s primary residence.

Real estate concentration increases exit pressure

Many Florida taxpayers hold significant wealth in real estate. That concentration can magnify planning mistakes.

If ownership is divided among heirs without liquidity planning, the family may face a forced sale. If property-level insurance costs rise, the intended hold period may shorten. If casualty repairs require capital, some heirs may want to contribute while others want out. If one property must be sold selectively, the tax consequences may fall unevenly across the ownership group.

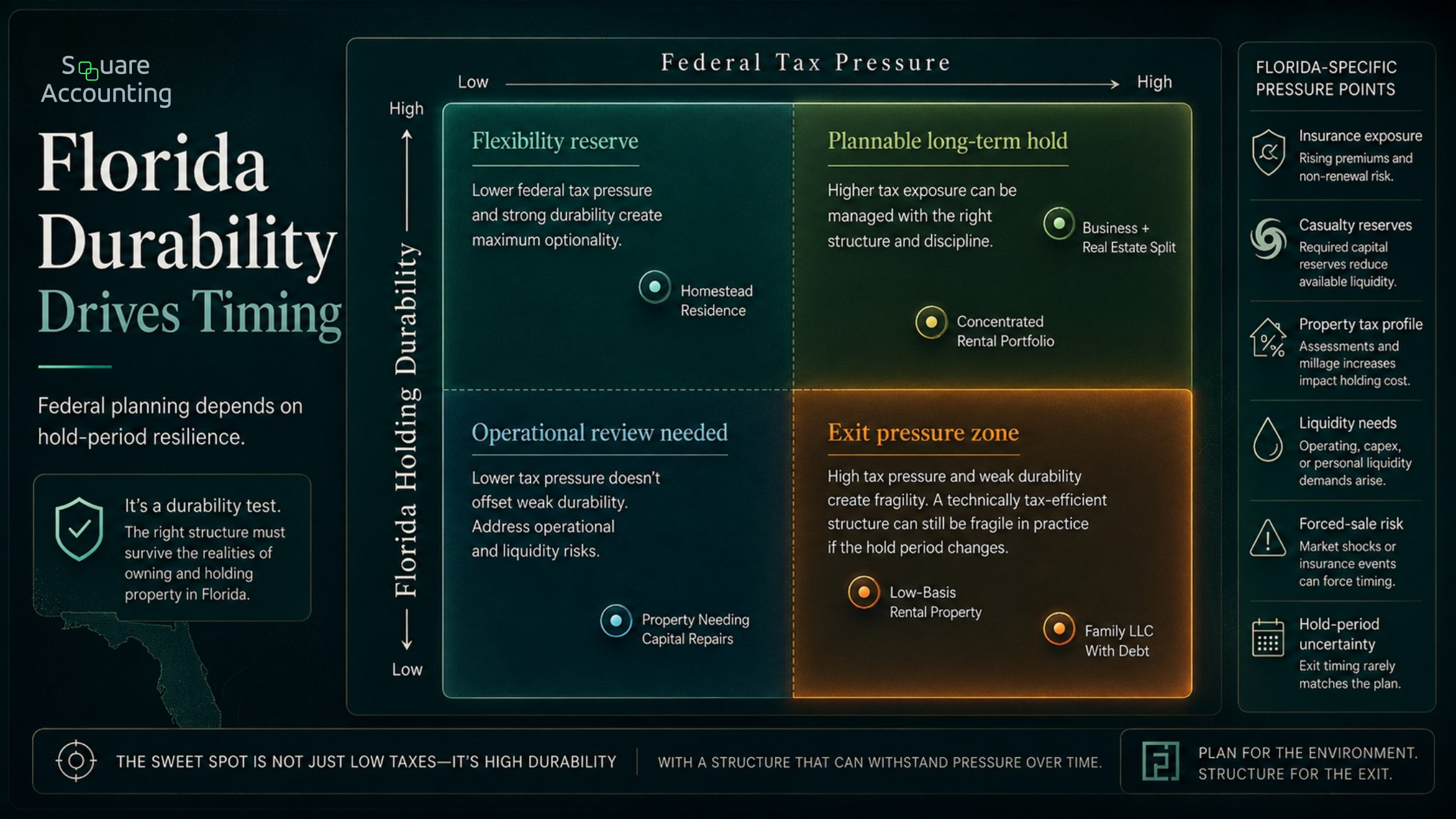

This is where federal tax planning and Florida holding durability intersect.

A structure that works for a long-term hold strategy may not work if Florida operating realities shorten the hold period. A plan that assumes assets will remain together may struggle if liquidity pressure forces selective sales. A gifting strategy that looks efficient during stable years may create friction if heirs inherit interests in assets that need capital, refinancing, or repairs.

The structure should anticipate those pressure points before ownership is transferred.

Florida’s no-state-income-tax environment does not remove the need to test liquidity, property risk, and exit timing.

“Florida-specific planning should not stop at income tax treatment. Real estate concentration, homestead rules, insurance exposure, and liquidity needs can all change the timing and durability of the ownership plan.”

Common Misuses and Oversights

Mistake 1: Treating annual gifting as a full estate plan

Annual exclusion gifts can be useful, but they are usually not enough for meaningful business or real estate succession planning.

They do not determine who controls the asset, how income is allocated, whether basis is preserved, or what happens when an asset is sold. They also do not replace valuation, governance, or liquidity planning.

For sophisticated taxpayers, the question should not stop at how much can be transferred each year. The more important question is whether the transferred interest advances the long-term ownership design.

Mistake 2: Gifting low-basis assets without modeling the future sale

A gift can be efficient from an estate tax perspective and inefficient from an income tax perspective.

If the asset is likely to be sold soon, preserving basis flexibility may be more valuable than shifting ownership immediately. This is especially important with appreciated real estate, concentrated stock, or business interests with significant built-in gain.

The future sale timeline should be part of the gifting analysis. If the family is already considering an exit, recapitalization, or liquidity event, the structure should be modeled before interests move.

Mistake 3: Separating assets legally but not strategically

Many owners create multiple LLCs but never coordinate them.

The result may be legal separation without succession clarity. One entity may hold real estate. Another may hold operations. Another may hold management rights. Another may own equipment. But the estate plan may not clearly define who controls each entity, how cash moves, or how heirs are treated.

Structure without coordination is not strategy.

The governing documents should be reviewed together, not as isolated files.

Mistake 4: Ignoring debt and guarantees

Real estate and business ownership often includes debt.

A transfer of ownership may affect lender consent, guarantees, refinancing, debt allocations, or estate liquidity. A family may inherit equity but also inherit practical financing constraints.

Debt should be part of the succession map.

This includes debt maturity dates, personal guarantees, related-party loans, capital call expectations, refinancing risk, and whether successors have the financial strength to support the ownership they receive.

Mistake 5: Assuming equal ownership creates fairness

Equal ownership does not always create fairness.

One child may work in the business. Another may not. One heir may want long-term real estate ownership. Another may need liquidity. One may be willing to sign guarantees. Another may not. One may understand the asset. Another may only see a distribution stream.

Equal ownership can become unequal burden.

Fairness may require different assets, different rights, buyout options, preferred returns, governance protections, or life insurance coordination.

Mistake 6: Letting the tax plan outrun the family plan

A technically efficient structure can still fail if the family cannot operate it.

If the next generation does not understand the structure, if decision rights are unclear, or if liquidity is inadequate, the plan can create conflict. Tax strategy should support continuity, not create a structure that only the original owner understands.

This is especially important when a plan relies on trusts, nonvoting interests, valuation concepts, installment sale arrangements, or entity restrictions. The structure should be administrable by the people who will inherit it.

A Better Review Process: Test the Structure Against Future Events

A strong ownership review should not begin with documents. It should begin with scenarios.

We would stress-test the structure against questions such as:

What happens if the owner dies this year?

What happens if the business is sold in three years?

What happens if one heir wants cash and another wants to hold?

What happens if a property must be sold earlier than expected?

What happens if insurance or debt service changes the hold period?

What happens if a gifted interest is later involved in a divorce, creditor issue, or family dispute?

What happens if a key successor is not ready to lead?

What happens if federal estate tax is not the biggest issue, but income tax basis is?

What happens if one entity has liquidity and another has tax pressure?

What happens if the family needs to unwind a structure that was designed only for holding?

This type of review often reveals whether the current structure is truly aligned or merely organized.

A practical review should connect the estate documents, operating agreements, tax returns, debt schedules, depreciation history, insurance profile, ownership ledger, and family succession goals. If those items are reviewed separately, the plan may miss the points where they interact.

The purpose is not to make the structure more complex. It is to make the structure easier to execute when the next major event occurs.

We can help review how control, basis, liquidity, and governance may interact before ownership interests move.

Core Strategies for Structuring Business & Real Estate Assets

Gifting Interests Before a Sale

Only after modeling the numbers. Gifting right before a sale can trigger valuation, basis, and assignment-of-income issues. Always analyze the expected sale year, built-in gains, depreciation, and the recipient’s tax profile first. Timing is everything; transfers made years before a transaction are vastly more effective than last-minute moves.

The 2026 Estate Exemption Myth

Planning is still required. Even with high federal exclusion amounts, estate planning is about more than just tax mitigation. Your structure directly impacts asset basis, succession control, creditor exposure, and exit flexibility—issues that matter deeply even if you do not expect an estate tax liability.

Revocable Trusts vs. Business Succession

A trust is rarely enough on its own. While excellent for probate avoidance, true business succession requires operating agreements, buy-sell terms, voting control, and management transition plans. Your trust must be intentionally coordinated with your corporate documents, not managed in a silo.

Separating Real Estate from Operations

Keep them apart, but connected. Mixing operational risk and real estate in one entity exposes your property to unnecessary liability. However, separating them requires tight coordination of leases, cash flow, and tax classifications to avoid creating new vulnerabilities or financing hurdles.

When to Review Your Structure

Before major milestones, not just annually. Review your ownership structure prior to gifting, refinancing, adding partners, selling assets, or changing estate plans. For complex portfolios, a proactive, multi-year review framework is always better than waiting for a crisis or a transaction.

If your wealth is concentrated in a business, real estate portfolio, or family entity, we can help evaluate whether the structure supports the next transfer.

Conclusion

Aligning ownership structure with succession, gifting, and estate planning goals is not about choosing one perfect entity.

It is about coordinating ownership, control, economics, basis, liquidity, and family governance before a transfer event forces the issue.

For high-income Florida taxpayers, the stakes are often concentrated in closely held businesses, real estate portfolios, appreciated assets, and family entities. The tax result depends not only on what is owned, but how it is owned, when it is transferred, who controls it, and what happens when the plan reaches an exit, death, refinancing, or leadership transition.

The best structure should preserve flexibility. It should support the family’s business and investment goals. It should account for federal tax exposure, Florida property realities, basis outcomes, liquidity needs, and long-term succession objectives.

A well-designed ownership structure does more than move assets.

It makes the next transfer easier to execute.

Ownership Structure, Succession, and Estate Planning FAQs

Key questions for high-net-worth families, business owners, and real estate investors aligning ownership structure with gifting, succession, control, basis, liquidity, and long-term transfer goals.

How do we know if our ownership structure is misaligned with succession goals?

A structure may be misaligned if it answers today’s liability or tax reporting needs but does not clearly answer who controls the asset, who receives the economics, who bears debt, and what happens during a gift, death, refinance, sale, or buyout. We would look for gaps between the legal documents, tax reporting, family expectations, and operating reality. The warning sign is not always a technical defect. It is often a structure that works while the founder is active but becomes difficult to execute when ownership has to move.

What documents should be reviewed together before transferring ownership interests?

The article points to a coordinated review of estate documents, operating agreements, shareholder agreements, trust terms, tax returns, debt schedules, depreciation history, insurance profile, ownership ledgers, and family succession goals. Reviewing those items separately can miss the friction points. For example, the estate plan may transfer an interest, but the operating agreement may restrict control, the debt agreement may require consent, and the tax history may carry built-in gain or depreciation issues. The value is in seeing where the documents interact.

Can we transfer economic ownership while keeping control?

Often, that is one of the main reasons to review ownership structure before gifts or succession events. The article discusses voting and nonvoting interests, manager-managed LLCs, trustee powers, consent rights, and governance documents as ways control and economics may be separated. The key is that the structure must clearly define what the recipient receives. A child, trust, or successor may receive appreciation or cash flow without receiving management authority. That can support continuity, but only if the documents, tax reporting, and family expectations are aligned.

Why does basis matter so much in ownership transfer planning?

Basis affects the income tax result when an asset is later sold. The article emphasizes that lifetime gifts and transfers at death can produce different basis outcomes. A lifetime gift may shift future appreciation but preserve built-in gain for the recipient. A transfer at death may create a different basis result but may leave control or liquidity issues unresolved. For appreciated real estate, business interests, or concentrated assets, basis planning can materially affect whether a transfer improves the family’s overall position or simply moves a future tax issue.

What should Florida real estate owners test before adding heirs to an LLC?

Florida real estate owners should test whether the heirs can handle the asset’s economics, not just receive ownership. The article highlights debt, guarantees, depreciation history, suspended losses, insurance exposure, capital calls, refinancing pressure, and potential exit-year tax issues. Adding heirs to an LLC may seem orderly, but the structure should clarify who controls sales, who funds reserves, who signs guarantees, who receives distributions, and what happens if one heir wants liquidity while another wants to hold.

How can equal inheritance create unequal tax or liquidity outcomes?

Equal ownership can become an unequal burden when heirs have different roles, cash needs, risk tolerance, or willingness to manage an asset. One heir may work in the business or understand the real estate portfolio. Another may only want distributions. One may be willing to support a capital call or guarantee. Another may need a buyout. The article frames fairness as more than equal percentages. Fairness may require different assets, different rights, buyout terms, governance protections, preferred economics, or liquidity planning.

How does Florida homestead fit into ownership and estate planning?

Florida homestead should not be treated like a standard investment asset. The article notes that homestead may affect creditor protection, property tax treatment, and transfer planning, including restrictions when a surviving spouse or minor child is involved. For high-net-worth families, that means ownership changes, trust planning, marital planning, and inheritance design need to be coordinated carefully. A structure that appears efficient for tax or administrative reasons may create legal or family-transfer friction if Florida homestead rules are not considered.

When should ownership structure be reviewed before a major event?

The article supports reviewing ownership structure before gifts, refinances, new partners, major property acquisitions, sales, estate document updates, leadership transitions, or significant family changes. The best time is before the event forces decisions. Once a sale is pending, a lender requires action, or a succession issue becomes urgent, flexibility may be limited. We would stress-test the structure against likely scenarios first: death, exit, refinance, buyout, family disagreement, liquidity pressure, or a successor who is not ready to lead.