Self-Directed Retirement Accounts and Asset Selection Risk: A Tax Planning Framework for Investors

Self-directed retirement accounts are often marketed around access: real estate, private placements, promissory notes, tax liens, precious metals, private credit, and closely held investment vehicles. For sophisticated investors, access is not the hard part.

The hard part is asset selection.

The immediate answer is this: asset selection risk in a self-directed retirement account is the risk that an otherwise permissible alternative asset is a poor fit for the retirement wrapper after accounting for tax character, leverage, control, liquidity, valuation, and exit timing.

That distinction matters. A custodian may be willing to hold an asset. The asset may be legal. The investment thesis may even be sound. But the retirement account may still be the wrong tax location.

For high-income Florida investors, especially real estate investors and business owners, the question is rarely, “Can my IRA buy this?” The better question is, “What planning tools do I lose, what federal tax issues do I create, and what happens when this asset has to be valued, distributed, sold, or inherited?”

Florida’s lack of personal income tax makes the analysis more federal-tax concentrated, not less important. Florida does not impose a personal income tax, so the planning pressure often shifts to federal income tax, NIIT exposure, UBTI, depreciation strategy, Roth conversion timing, estate planning, and exit-year income management.

A self-directed retirement account decision should be modeled across the full asset lifecycle, not treated as a one-time acquisition question.

Before reviewing a specific asset, the better question is whether the retirement wrapper improves or weakens the lifetime tax result. The framework below shows where an otherwise permissible alternative investment can fail as a retirement account asset.

Self-Directed Retirement Accounts and Asset Selection Risk: The Quick Framework

Before placing an asset into a self-directed IRA, Roth IRA, SEP IRA, SIMPLE IRA, or other retirement structure, run it through these planning gates.

Self-Directed Retirement Account Investments Need Multiple Tax Gates

A self-directed retirement account investment should be tested before purchase, during ownership, and before exit because the wrong asset or transaction can turn tax-advantaged capital into a planning problem.

| Planning Gate | Core Question | What Can Go Wrong |

|---|---|---|

| Permitted Asset Gate | Is the asset legally allowed inside the retirement account? | The account invests in prohibited property, such as life insurance or collectibles, or indirectly owns something problematic through an entity. |

| Party and Transaction Gate | Is any disqualified person involved? | A sale, loan, lease, guarantee, service arrangement, or use of property by the wrong party can create prohibited transaction exposure. |

| Control Gate | Does the investment depend on the owner’s personal involvement? | The investor’s real estate skill, local relationships, or operational control can become the tax problem. |

| Income-Character Gate | Will the asset produce UBTI or debt-financed income? | The IRA may owe current tax even though the owner expected tax-deferred or tax-free compounding. |

| Tax-Location Gate | Are valuable outside-the-IRA tax attributes being wasted? | Depreciation, passive loss planning, 1031 exchange flexibility, capital gain treatment, and basis planning may be less useful or unavailable inside the account. |

| Liquidity and Valuation Gate | Can the account support expenses, capital calls, annual valuation, and reporting? | Illiquid assets can create forced-sale pressure, reporting uncertainty, or underfunded expense obligations. |

| Exit and Beneficiary Gate | What happens when the asset must be sold, distributed, converted, or inherited? | A good investment can become a poor tax result when RMDs, death, a business sale, or a major liquidity event compress income into the wrong year. |

A quick working rule:

Better retirement-account candidates often produce tax-inefficient ordinary income, require little owner involvement, avoid related parties, use little or no leverage, and can be valued and liquidated without drama.

Weaker retirement-account candidates often rely on depreciation, active management, related-party relationships, personal guarantees, leverage, uncertain valuation, or a long illiquid exit.

This is why self-directed retirement accounts and asset selection risk should be treated as an asset-location decision, not just an investment menu decision.

We help investors pressure-test whether an alternative asset belongs inside a retirement account before structure drives the tax result.

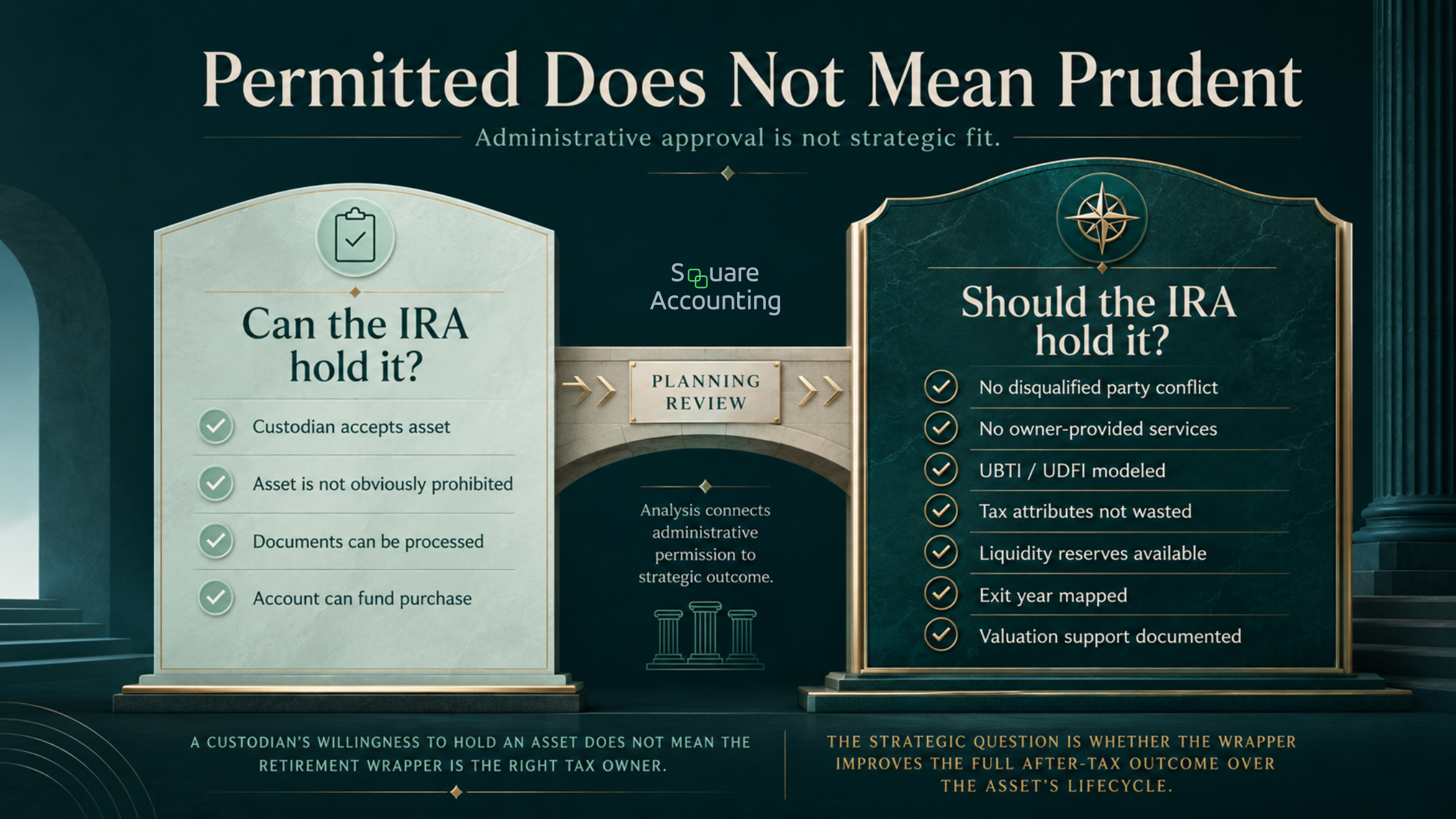

What a Self-Directed Retirement Account Actually Changes

A self-directed IRA is still an IRA. The tax wrapper does not become more flexible because the asset is private, local, real estate-based, or held through an LLC.

What changes is the investment menu. Self-directed custodians may allow assets such as real estate, private placement securities, promissory notes, tax lien certificates, precious metals, commodities, and crypto assets. But the SEC, FINRA, and NASAA have warned that self-directed IRA custodians generally do not sell investment products, provide investment advice, evaluate the quality or legitimacy of investments, or verify financial information provided for the asset.

That distinction is central.

Custodian acceptance is administrative. It is not tax approval. It is not due diligence. It is not confirmation that the transaction avoids prohibited transaction rules, UBTI, valuation issues, personal benefit concerns, or future distribution problems.

The IRS also makes clear that IRA law does not generally prohibit real estate ownership, although custodians are not required to offer every permitted investment. The same IRS guidance identifies life insurance and collectibles as investments IRA funds cannot hold, with limited exceptions for certain coins and bullion.

That creates a planning gap. An investor hears, “Yes, your IRA can buy real estate,” and assumes the strategy has been validated. In reality, the custodian may only be saying, “We can administer this asset.”

For a high-net-worth investor, that is not enough.

The asset label rarely answers the planning question; ownership, financing, control, and exit path determine whether the retirement account is the right tax owner.

“The planning gap often appears after administrative approval but before tax ownership has been tested. This visual separates what the account may be allowed to hold from whether the asset actually fits the investor’s broader tax plan.”

The Five Asset Selection Risks Sophisticated Investors Miss

1. Permissible Asset Risk

Some assets are simply not allowed in an IRA. The clearest examples are life insurance and collectibles. The IRS lists examples of collectibles such as artwork, rugs, antiques, metals, gems, stamps, coins, alcoholic beverages, and certain other tangible personal property, while also recognizing limited exceptions for specific coins and bullion.

The harder issue is indirect exposure.

A private fund, LLC interest, note, or syndication may not look prohibited at the top level. But the underlying structure may involve assets, rights, debt, related parties, or operational activities that change the analysis.

The mistake is stopping at the label.

“Real estate,” “private credit,” “tax lien,” “LLC interest,” or “private placement” does not answer the tax question. The planning answer depends on what the asset owns, how it earns income, who controls it, how it is financed, and who benefits from it.

For investors who already have advisors, this is where fragmentation often appears. The investment advisor may review expected return. The custodian may review administrative eligibility. The CPA may not see the documents until after year-end. No one may be responsible for deciding whether the IRA is the right tax owner in the first place.

2. Prohibited Transaction Risk

A prohibited transaction is not about whether the investment is attractive. It is about whether the retirement account is being used improperly by the IRA owner, beneficiary, fiduciary, or another disqualified person.

The IRS describes a prohibited IRA transaction as improper use of the IRA account or annuity by the owner, beneficiary, or a disqualified person. Examples include borrowing money from the IRA, selling property to it, using it as security for a loan, or buying property for personal use with IRA funds. Disqualified persons include the IRA owner’s fiduciary and certain family members, including a spouse, ancestors, lineal descendants, and spouses of lineal descendants.

The severe consequence is often underappreciated. If the IRA owner or beneficiary engages in a prohibited transaction involving a traditional IRA, IRS Publication 590-A states that the account stops being an IRA as of the first day of that year. The account is generally treated as distributing all assets at fair market value on the first day of the year, to the extent the value exceeds basis.

That is not a small compliance adjustment. It can pull an entire account into taxable income unexpectedly.

This is where real estate investors are uniquely exposed. They know contractors. They control management companies. They may own brokerage entities, construction companies, title relationships, short-term rental platforms, or operating businesses. In taxable real estate, those connections may create an edge. Inside a retirement account, they may create self-dealing risk.

The deeper question is not, “Can the IRA invest?” It is, “Can the IRA invest without relying on the owner, the owner’s family, the owner’s credit, the owner’s services, or the owner’s related entities?”

3. Control and Custody Risk

Self-directed investors often like control. Some pursue checkbook IRA structures because they want faster execution, fewer custodian delays, and more direct management.

Control is also where the facts can turn against the taxpayer.

The Tax Court’s McNulty decision is a useful warning. The taxpayer established a self-directed IRA, directed IRA assets into a single-member LLC, had the LLC purchase American Eagle coins, and took physical possession of the coins. The court held that she received taxable distributions equal to the cost of the coins when she received physical custody.

The lesson is broader than precious metals.

The more personal control the IRA owner has over the asset, the more important it becomes to document who owns it, who controls it, who has custody, who pays expenses, who receives income, and who performs services.

A retirement account should not become a private side pocket for personally managed assets. The account must remain separate in ownership, economics, custody, and operation.

This is especially important when an IRA owns an LLC interest. The LLC may make administration easier, but it does not neutralize prohibited transaction rules. A checkbook structure can make a bad transaction easier to execute before anyone reviews it.

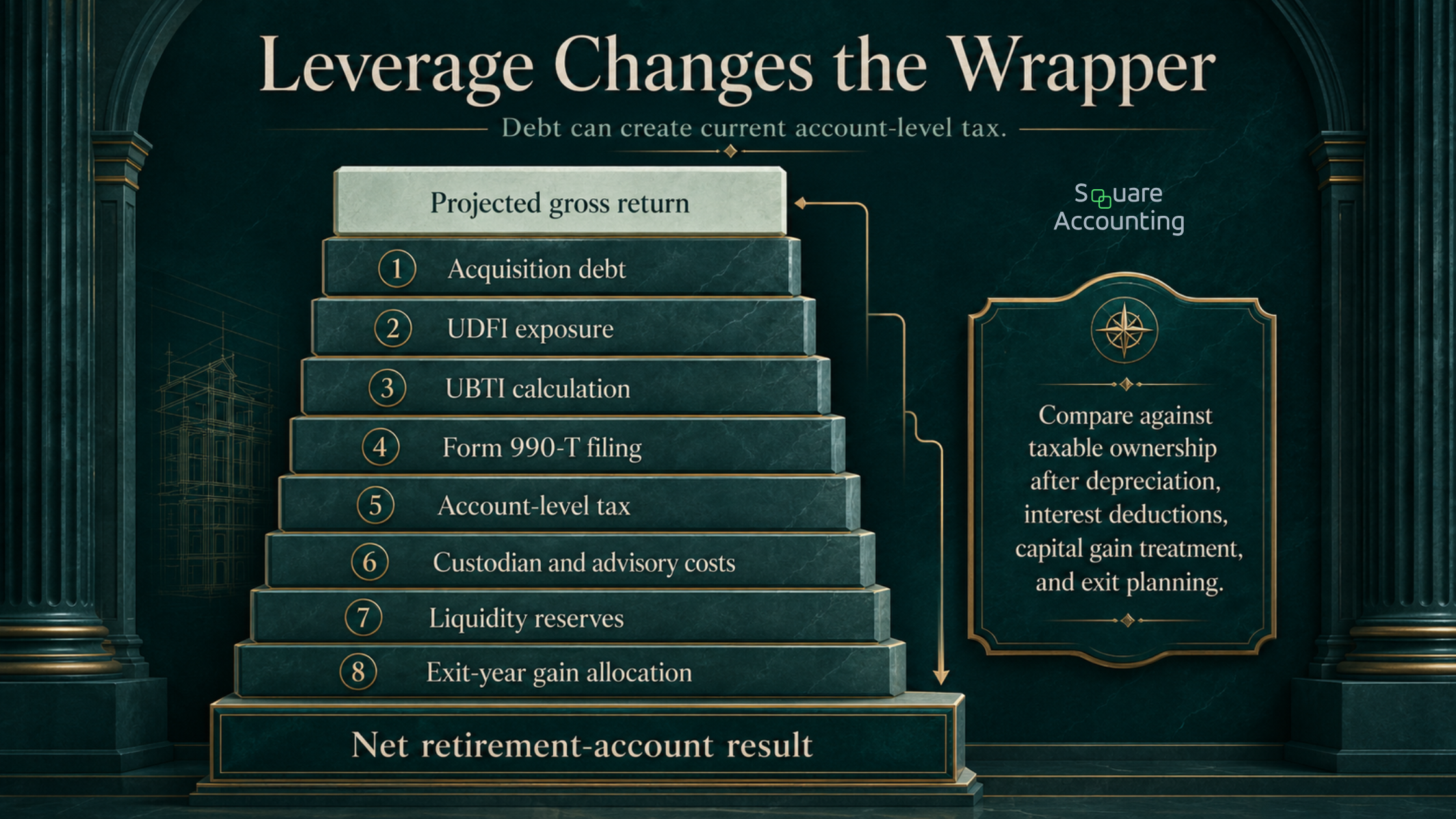

4. UBTI and Debt-Financed Income Risk

Many investors assume IRA income is automatically tax-deferred or tax-free. That is not always true.

When a tax-exempt account earns unrelated business taxable income or income from debt-financed property, the account may owe current tax. IRS Publication 598 explains that debt-financed property generally means income-producing property with acquisition indebtedness during the year, and that unrelated debt-financed income is computed by applying a debt-to-basis percentage to income from the property. A percentage of gain may also be included when debt-financed property is sold.

This matters for leveraged real estate, private funds, operating businesses, and certain partnerships.

A debt-free rental property inside an IRA may have one profile. A leveraged value-add property may have another. A fund that uses subscription lines, property-level debt, or operating leverage may pass through UBTI. A short-term rental structure with service-heavy operations may need separate review.

Leverage should be modeled after account-level tax, administrative friction, liquidity reserves, and exit-year consequences, not just projected investment return.

The issue is not whether leverage is automatically disqualifying. The issue is whether the IRA still produces the better after-tax result once the full friction stack is visible.

The 2025 Form 990-T instructions state that trustees for IRAs, SEP IRAs, SIMPLE IRAs, Roth IRAs, and certain other accounts with $1,000 or more of unrelated trade or business gross income must file Form 990-T, and each account is treated as a separate trust for UBTI purposes.

That does not automatically make the investment wrong. It means the after-tax return must be modeled correctly.

For sophisticated investors, the failure mode is usually not ignorance of UBTI as a concept. It is underestimating how UBTI interacts with leverage, depreciation limitations inside the account, state filing questions, custodian administration, K-1 timing, estimated tax payments, and exit-year gain.

5. Tax-Location Risk

This is the failure mode many self-directed IRA discussions miss.

An asset can be legal, compliant, profitable, and still belong outside the retirement account.

Real estate is the clearest example. Outside a retirement account, real estate may create depreciation deductions, interest deductions, passive loss planning opportunities, cost segregation benefits, capital gain treatment, installment sale planning, 1031 exchange potential, and basis planning at death.

Inside a traditional IRA, those benefits can be muted, unavailable to the individual owner, or converted into a different tax character. The IRA owns the property. The individual generally does not personally deduct depreciation or losses from IRA-owned property. Later traditional IRA distributions are generally taxed under retirement distribution rules, not as direct sales of the underlying property.

That may be a poor trade for a Florida investor who already has a coordinated depreciation, passive activity, and exit strategy in taxable ownership.

The key question is not “Which account avoids tax today?” It is “Which owner produces the best lifetime after-tax result after acquisition, income, refinancing, sale, distribution, death, and beneficiary taxation?”

That is tax-location risk.

We can review the tax-location trade-offs before an IRA-owned asset creates avoidable liquidity, valuation, or UBTI issues.

The Real Estate Problem: Expertise Can Create Risk

Many Florida investors are drawn to self-directed retirement accounts because they know real estate better than public markets.

That expertise can be valuable. It can also create the facts that make the structure fragile.

A Florida investor may want to use an IRA to buy:

A rental property near an existing portfolio

A private note secured by a local development

A membership interest in a syndication managed by a familiar sponsor

A tax lien certificate

A short-term rental property

A small commercial building leased to a known operator

A debt position in a project where the investor has informal influence

Each option has a different risk profile.

A passive, third-party-managed, debt-free asset with independent valuation and no personal use may be easier to support. A property that needs owner supervision, related-party contractors, personal guarantees, frequent capital infusions, leasing decisions, or hands-on management is far more fragile.

The investor’s edge is often control. The IRA’s tax compliance depends on separation.

That tension should be addressed before funding the account. Otherwise the investor may buy a “retirement asset” that cannot be operated the way the investor normally creates value.

Traditional vs. Roth: Asset Selection Is Not the Same

The same asset can produce very different planning results in a traditional self-directed IRA versus a Roth self-directed IRA.

Traditional self-directed IRA

A traditional IRA can defer tax. Deferral can be useful, but it is not the same as permanent tax savings.

A traditional self-directed IRA may fit assets that produce tax-inefficient ordinary income, do not require leverage, do not depend on owner services, and do not give up valuable tax benefits outside the IRA.

It may be less attractive for assets that already receive favorable long-term capital gain treatment, depreciation shelter, 1031 exchange potential, or basis planning outside the IRA.

The traditional IRA also creates future distribution pressure. Traditional, SEP, and SIMPLE IRA owners generally must begin required minimum distributions under current IRS rules once they reach the applicable RMD age, and IRS guidance currently states that IRA RMDs begin at age 73. Because RMD rules can change and birth-year details matter, the RMD year should be verified before modeling an illiquid self-directed asset.

That matters because a traditional IRA holding illiquid real estate or a private fund interest may not have enough cash to satisfy required distributions without an in-kind distribution, partial sale, outside liquidity planning, or an unfavorable liquidation.

Roth self-directed IRA

A Roth self-directed IRA can be powerful for high-growth assets because qualified distributions may be tax-free, and IRS guidance states that Roth IRA owners can leave amounts in the Roth IRA as long as they live.

That does not make every high-growth private asset a Roth candidate.

Roth accounts still face prohibited transaction rules, UBTI exposure, valuation problems, liquidity constraints, and concentration risk. A private asset inside a Roth is only attractive if the structure survives scrutiny and the account can carry the asset through the full holding period.

For high-income investors, Roth self-directed planning often intersects with conversion strategy. That means valuation, income timing, liquidity to pay conversion tax, charitable planning, business-sale timing, and estate objectives should be coordinated before the asset appreciates significantly.

The trap is assuming “high upside” automatically means “Roth.” Sometimes it does. Sometimes the better answer is taxable ownership with depreciation, capital gain treatment, or estate basis planning.

NIIT Layering: A Federal Issue Florida Investors Should Not Ignore

Florida’s lack of personal income tax does not eliminate federal investment tax complexity.

The net investment income tax applies at 3.8% to individuals, estates, and trusts with net investment income above applicable thresholds. For individuals, the IRS lists thresholds of $250,000 for married filing jointly or qualifying surviving spouse, $125,000 for married filing separately, and $200,000 for single or head of household.

This does not mean every IRA decision is a NIIT decision. Retirement distributions and net investment income have their own rules.

But asset location affects the broader income stack. A high-income Florida taxpayer may have taxable brokerage income, passive rental income, business income, capital gains, Roth conversions, partnership K-1s, retirement distributions, and a real estate exit in the same multi-year window.

The self-directed IRA decision should be modeled inside that stack, not beside it.

A technically attractive SDIRA investment can still create pressure if it forces distributions in a year when the taxpayer is also selling a business, recognizing depreciation recapture from a property sale, exercising equity compensation, or completing a Roth conversion. The issue is not the account in isolation. It is the combined income calendar.

A Better Asset-Location Test for Self-Directed Retirement Accounts

We use a practical framework before deciding whether an asset belongs inside a self-directed retirement account.

1. What type of return does the asset produce?

Ordinary income, interest, capital appreciation, tax-sheltered rental income, qualified dividends, and operating business income are not equivalent.

A private note producing ordinary interest may be a better retirement account candidate than a real estate asset that would otherwise generate depreciation deductions and long-term capital gain treatment outside the account.

The first step is to identify the return type before choosing the owner.

2. What tax attributes are being sacrificed?

For real estate, this is often the central question.

If the investor can use depreciation, cost segregation, passive activity planning, real estate professional status, 1031 exchange planning, charitable strategies, or basis planning outside the retirement account, IRA ownership may reduce flexibility.

The retirement account may solve one tax problem while creating another.

A CPA may correctly report the IRA’s activity and still miss the larger issue: the wrong taxpayer owned the asset.

3. Does the asset need the owner’s involvement?

A retirement account-owned asset should not depend on the IRA owner’s personal labor, personal credit, related-party contracts, informal management, or emergency funding.

Ask:

Who signs contracts?

Who negotiates financing?

Who approves repairs?

Who manages the asset?

Who pays expenses?

Who receives income?

Who can use the property?

Who guarantees debt?

Who controls the entity?

Who supports valuation?

If the honest answer keeps pointing back to the IRA owner, spouse, children, parents, operating company, or family office, the structure needs deeper review.

4. Will leverage create current tax?

Leverage can improve returns, but it can also create UDFI or UBTI inside a retirement account.

The after-tax model should include account-level tax, financing restrictions, nonrecourse borrowing terms, custodian costs, tax preparation costs, and exit-year UBTI.

The comparison should not be “leveraged real estate inside an IRA versus taxable cash.” It should be “leveraged IRA ownership after UBTI and friction costs versus taxable ownership after depreciation, financing deductions, capital gain treatment, and exit planning.”

Those are different calculations.

5. Can the account support the full capital lifecycle?

A retirement account-owned asset must be supported by retirement account assets. Repairs, capital calls, insurance, taxes, legal fees, management fees, custodian fees, and professional costs should be anticipated before closing.

That means the account needs reserves.

This is where illiquid assets become dangerous. A property that looks attractive at acquisition can become a compliance problem when it needs capital and the IRA has no cash. The investor may be tempted to advance funds personally, delay maintenance, use a related party, or force a sale.

A reserve plan is not administrative housekeeping. It is part of the tax strategy.

6. What happens in the exit year?

A large sale, Roth conversion, RMD year, business exit, estate event, or beneficiary distribution period can change the result.

The exit year should be modeled before acquisition, not after the offer arrives.

A strong investment can become a weak tax result when liquidity, valuation, and income recognition converge in the same planning window.

Exit planning should not begin when the buyer appears or the distribution deadline arrives. The calendar below shows why SDIRA asset selection needs to be tested against the owner’s broader income timeline.

For traditional IRA assets, the exit question is not only “What will the asset sell for?” It is also:

Will the sale produce UBTI or UDFI?

Will proceeds be trapped inside a traditional IRA and taxed later as distributions?

Will the sale year overlap with other income events?

Will RMDs force liquidity before the investment thesis matures?

Can the asset be valued if it is distributed in kind?

What happens if the owner dies while the asset is illiquid?

Beneficiary planning is especially important. IRS Publication 590-B explains that many designated beneficiaries who are not eligible designated beneficiaries must fully distribute inherited IRA assets within 10 years. For illiquid private assets, that rule can turn a long-term investment into a compressed beneficiary income problem.

Our planning resources connect SDIRA decisions with depreciation, NIIT, entity structure, and exit-year tax pressure.

If the IRA Already Owns the Wrong Asset: Unwind Planning

Many investors do not ask these questions until after the self-directed account has already acquired the asset.

When that happens, the goal is not to panic. The goal is to stop creating new facts and evaluate the least damaging path forward.

A practical unwind review usually starts with four questions.

First, has a prohibited transaction already occurred? If there has been personal use, related-party leasing, personal guarantees, owner-provided services, or personal payment of expenses, the facts need to be reconstructed carefully.

Second, does the account have unreported UBTI or UDFI? If the asset used leverage or operated through a pass-through entity, prior-year K-1s, debt schedules, and Form 990-T obligations should be reviewed.

Third, can the asset be independently valued? A stale sponsor estimate, original purchase price, or informal appraisal may not be enough for distribution, conversion, estate, or RMD planning.

Fourth, what is the least disruptive exit? The answer may be a sale, a restructuring, an in-kind distribution, a staged liquidation, a Roth conversion strategy, or simply tighter compliance controls going forward.

Unwind planning often costs less than continuing a fragile structure until the exit year. The earlier the issue is identified, the more planning options usually remain.

We can evaluate whether your current self-directed retirement account structure aligns with your broader Florida tax plan.

When a Self-Directed Retirement Account Can Make Sense

A self-directed retirement account may be strategically useful when several conditions are present:

The asset is passive from the IRA owner’s perspective.

No disqualified person is on the other side of the transaction.

The asset does not require personal guarantees, owner labor, related-party services, or informal owner support.

Leverage is absent or the UBTI cost has been modeled.

The asset produces tax-inefficient income that benefits from retirement account shelter.

The account has enough liquidity to pay expenses and future obligations.

Valuation can be supported independently.

The exit timing fits the owner’s retirement, estate, and beneficiary plan.

A Roth structure or Roth conversion has been modeled where appropriate.

This can be a better fit for certain private credit strategies, passive fund interests, and cleanly structured alternative investments than for hands-on real estate projects.

The best candidates are usually boring from a compliance perspective. They may still be economically attractive, but they do not require the owner to bend retirement account rules to make the deal work.

When We Would Slow Down or Redesign

We would be cautious with any proposed self-directed retirement account investment involving:

Property the investor or family wants to use personally

A tenant, borrower, sponsor, contractor, broker, or manager connected to the IRA owner

Personal guarantees

Owner-managed repairs, leasing, operations, or bookkeeping

Capital calls the IRA cannot fund

Heavy leverage

Short-term rentals with service-heavy operations

Sponsor-provided valuations without independent support

Closely held business interests involving control, compensation, or board influence

Real estate where depreciation, cost segregation, 1031 planning, or exit structuring is central to the tax strategy

Investments promoted primarily through the tax benefits of the account rather than the asset’s standalone economics

None of these facts automatically means the strategy fails. They mean the investor should not proceed based only on custodian acceptance or sponsor confidence.

A redesign may involve using taxable ownership, changing the entity structure, reducing debt, selecting a Roth instead of a traditional account, keeping more liquidity in the IRA, using a different asset class, or sequencing the investment after a Roth conversion or exit event.

The wrong answer is to treat the IRA as a convenient funding source without modeling the full tax lifecycle.

The Florida Planning Lens

Florida’s lack of personal income tax can make retirement and investment planning more attractive, but it does not make asset selection simpler.

For Florida real estate investors, the main planning considerations are usually federal:

Ordinary income versus long-term capital gain

Depreciation and depreciation recapture

Passive activity limitations

Real estate professional status

NIIT exposure

Roth conversion timing

UBTI and UDFI

Required distributions

Estate and beneficiary distribution planning

Exit-year income compression

The Florida-specific issue is often behavioral, not statutory.

Investors may know the market, sponsor, manager, borrower, contractor, tenant, or property personally. That local proximity can increase the temptation to influence operations, provide services, advance cash, personally inspect or improve property, or rely on related-party relationships.

A strong local edge should not become personal involvement that undermines the retirement account structure.

For many Florida investors, the better structure may be taxable real estate ownership with a coordinated depreciation and exit plan, while the retirement account holds assets whose tax character and operational profile are better suited to the wrapper.

A Practical Pre-Investment Checklist

Before funding a self-directed retirement account investment, answer these questions in writing:

What asset is being purchased, and what does it actually own underneath?

Is the asset prohibited, or does it hold prohibited property?

Are any disqualified persons involved now or likely to become involved later?

Does the investment involve personal use, family use, related-party services, or related-party compensation?

Will the account use debt?

Could the asset generate UBTI or UDFI?

Who will manage the asset?

Who will pay expenses?

Does the IRA have enough liquidity for reserves, tax filings, and capital calls?

How will annual valuation be supported?

What tax benefits would be available if the asset were held outside the retirement account?

Would taxable ownership allow depreciation, cost segregation, passive loss planning, 1031 exchange planning, installment sale treatment, charitable planning, or basis planning?

What happens if the asset must be sold, distributed, or valued during an RMD year?

What happens if the owner dies while the asset is illiquid?

How does this investment fit the owner’s multi-year income, Roth conversion, charitable, estate, and business exit plan?

The purpose of the checklist is not to make the structure unnecessarily complex. It is to force the right decision before the retirement account becomes locked into a bad tax location.

Self-Directed IRAs and Real Estate: The Right Question Is Rarely Asked

A self-directed IRA can legally own real estate in Florida — but whether it should is a separate question, and the one that matters more. IRA law does not prohibit real estate ownership, but it does prohibit personal use, related-party dealings, personal guarantees, and owner-provided services. Add UBTI exposure, valuation requirements, liquidity constraints, and custodian limitations, and the structure requires more discipline than most investors anticipate before committing.

The Roth versus traditional question follows the same pattern. A Roth self-directed IRA can be powerful for high-growth assets — qualified distributions may be tax-free, and no required minimum distributions apply during the owner's lifetime. But the prohibited transaction rules, UBTI risk, valuation obligations, and liquidity constraints apply equally. The tax structure changes; the compliance burden does not.

Debt inside a self-directed IRA is not automatically disqualifying, but it can generate unrelated debt-financed income, making part of the gain taxable inside the account. Leveraged real estate held in a retirement account needs to be modeled after financing costs, custodial fees, tax preparation, reserve requirements, and exit consequences — not before a decision is made to use leverage, but before a decision is made to use the account at all.

The most common mistake is framing the analysis around what the account is permitted to hold rather than what it should hold. Retirement account ownership needs to be compared against taxable ownership, Roth conversion strategy, depreciation planning, estate timing, and exit planning across the investor's full federal tax profile. For many high-income investors, the depreciation benefits available in taxable ownership — cost segregation, bonus depreciation, stepped-up basis at death — outperform the tax-free growth narrative of a self-directed Roth when the full picture is modeled. The account can buy the asset. That is rarely the question worth asking first.

Conclusion: Asset Selection Is a Tax Strategy Decision

Self-directed retirement accounts can be useful for sophisticated investors, but flexibility is not the strategy.

The strategy is choosing the right asset, in the right account, with the right structure, over the right time horizon.

For high-income Florida investors, Self-Directed Retirement Accounts and Asset Selection Risk should be analyzed as part of a multi-year tax plan. A good investment can become a poor retirement account asset if it wastes depreciation, triggers UBTI, creates prohibited transaction exposure, depends on personal involvement, or forces a bad exit year.

The planning standard should be higher than “the custodian allows it.”

Before moving private real estate, notes, fund interests, or alternative assets into a self-directed account, model the tax location, transaction flow, liquidity path, valuation support, and exit year. That is where the real planning decision sits.

We work with Florida investors who want retirement account decisions coordinated with real estate, business income, and multi-year exit planning.

Self-Directed Retirement Account Asset Selection FAQs

Key questions for investors evaluating whether alternative assets belong inside a self-directed retirement account, taxable ownership, or another planning structure.

How should we decide whether an asset belongs inside a self-directed retirement account or in taxable ownership?

Start with the asset’s tax character, not the account’s flexibility. We compare what the asset produces inside the retirement wrapper against what it could produce outside it. A private note generating ordinary interest may fit differently than real estate that could create depreciation, cost segregation benefits, passive loss planning, capital gain treatment, or 1031 exchange flexibility. The key question is whether the IRA improves the lifetime after-tax result or simply hides today’s income while sacrificing better planning tools later.

What due diligence should happen before a self-directed IRA invests in a private placement or fund?

The review should go beyond sponsor materials and custodian acceptance. We would want to understand the underlying assets, use of leverage, expected income character, related-party involvement, valuation process, liquidity terms, capital call obligations, and whether the fund may pass through UBTI. For high-income investors, the issue is not only investment quality. It is whether the retirement account can own the position cleanly through acquisition, reporting, income recognition, exit, and beneficiary planning.

Why can a strong real estate operator be a poor fit for IRA-owned real estate?

Real estate operators often create value through control, relationships, speed, and hands-on judgment. Those strengths can create risk when the owner’s retirement account owns the asset. If the investment depends on the owner’s labor, credit, management company, family relationships, contractors, or informal influence, the structure may become fragile. IRA-owned real estate generally needs cleaner separation than taxable real estate. The investor’s edge should not require facts that make the retirement account look like a personal operating vehicle.

How much liquidity should a self-directed retirement account keep outside the alternative asset?

The right reserve level depends on the asset’s expense profile, but the account should have enough liquidity to support the full holding period, not just the purchase. That includes custodian fees, tax preparation, insurance, legal costs, repairs, capital calls, valuation costs, and possible tax at the account level. Illiquidity becomes dangerous when the owner is tempted to advance personal funds, use related parties, delay required expenses, or sell under pressure. Reserve planning is part of compliance, not just cash management.

When does leverage make a self-directed IRA investment less attractive?

Leverage can improve investment returns, but inside a retirement account it may also create unrelated debt-financed income or other UBTI exposure. The issue is not whether debt is always bad. It is whether the after-tax, after-cost result still justifies IRA ownership once account-level tax, financing limits, custodian administration, filing requirements, reserves, and exit-year consequences are included. Leveraged real estate inside an IRA should be compared against taxable ownership with depreciation, interest deductions, capital gain treatment, and exit planning.

What should we review if a self-directed IRA already owns a questionable asset?

The first step is to stop creating new facts and reconstruct what has already happened. We would review whether there has been personal use, related-party involvement, personal guarantees, owner-provided services, personal payment of expenses, unreported UBTI, or unsupported valuations. From there, the planning focus becomes containment and exit design. The answer may involve tighter controls, independent valuation, sale planning, restructuring, an in-kind distribution, or broader income-year coordination.

How does self-directed IRA planning affect a future business sale or real estate exit?

A self-directed retirement asset can create pressure when it collides with another major income event. A business sale, large real estate disposition, Roth conversion, RMD year, or beneficiary transition can compress taxable income into a narrow window. The IRA asset may also be illiquid, hard to value, or difficult to sell at the right time. We prefer to model the exit year before acquisition so the retirement account does not force a bad sale, poorly timed distribution, or avoidable income spike.

What is the Florida-specific risk with local private deals inside an IRA?

For Florida investors, the risk is often proximity. A local sponsor, borrower, contractor, property manager, tenant, or operating partner may be someone the investor knows or influences. That familiarity can make due diligence easier, but it can also increase prohibited transaction and control risk. The account should not rely on personal relationships, informal management, related-party services, or owner intervention to make the deal work. Florida’s lack of personal income tax does not reduce the need for clean federal tax structure.