Tax Preparation and Advisory Review for Florida Business Owners: What It Includes

A tax return becomes more useful when it is reviewed as part of the owner’s broader planning system.

For many Florida business owners, tax preparation answers one question: “What do I owe for last year?”

A tax preparation and advisory review should answer a better question: “What is this return telling us before the next major decision is made?”

That distinction matters when income is high, ownership is layered, real estate is involved, or the owner’s personal return carries the full weight of several business and investment decisions. For business owners, high-income professionals, and real estate investors, the tax return is not just a filing package. It is a record of how income, deductions, debt, ownership, payroll, depreciation, distributions, and investment activity interacted during the year.

When the return is treated only as a compliance task, the conversation usually happens too late. The numbers are organized, the forms are filed, and the taxpayer moves on. But the tax return may be showing a larger issue: estimates are behind, basis is tightening, depreciation is creating future pressure, owner compensation needs review, or the current entity structure no longer fits the owner’s growth.

A strong review does not replace tax preparation. It turns tax preparation into a planning checkpoint.

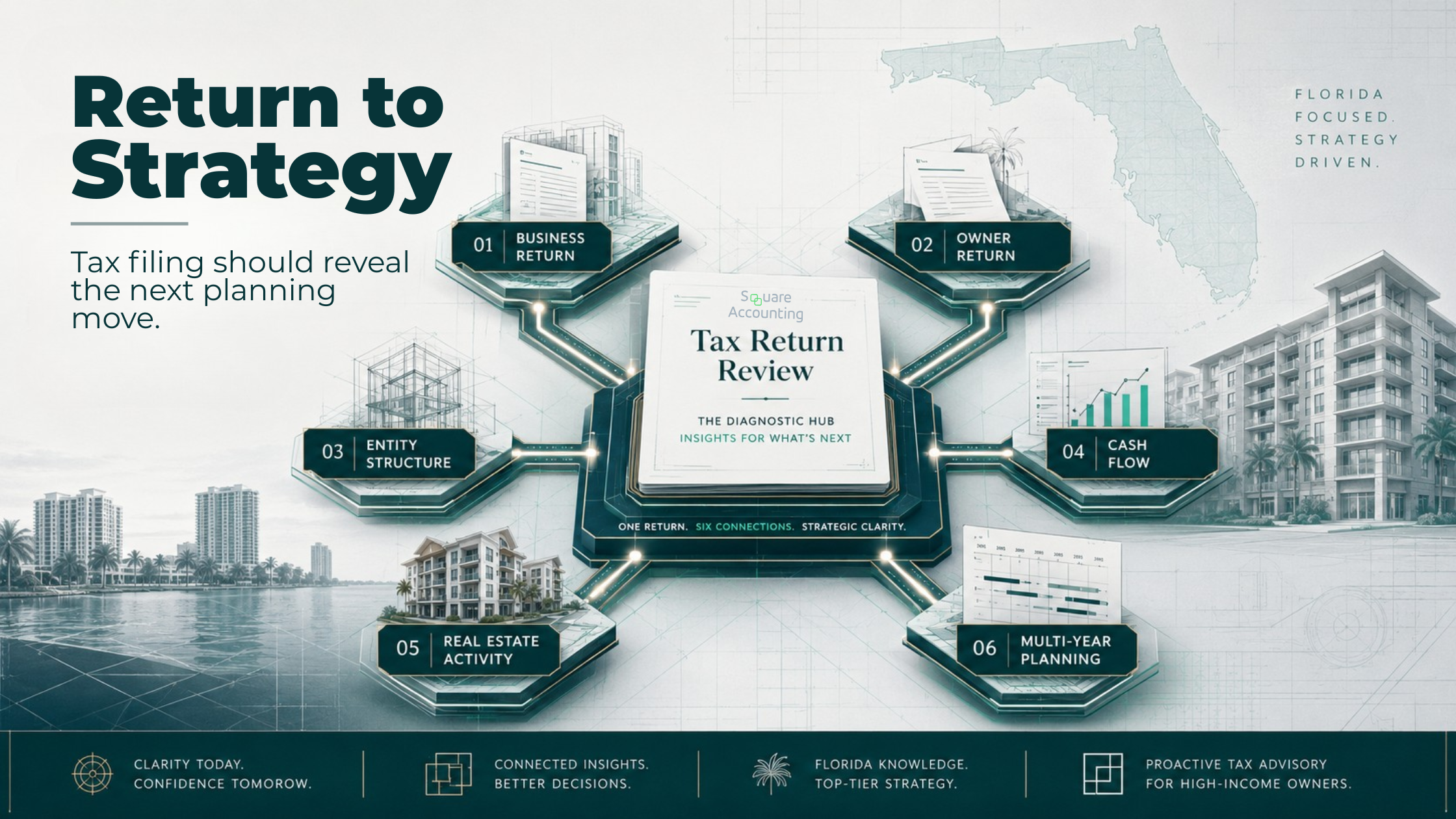

Key takeaway: A tax preparation and advisory review for Florida business owners should include accurate return preparation, but it should also connect the return to owner-level planning, cash flow, entity structure, real estate activity, estimates, documentation, and multi-year tax exposure.

See how a tax return can identify planning collisions before the next tax year moves too far forward.

What Is Included in a Tax Preparation and Advisory Review?

A tax preparation and advisory review for Florida business owners includes the preparation of required tax returns, but it should also include a structured review of the facts behind the return.

The immediate deliverable is the filed return. The more valuable deliverable is clarity.

A meaningful review should help the owner understand what drove the tax result, what changed from the prior year, what could create risk, and what should be addressed before the next tax year is already in motion.

At a practical level, the review should include:

A Business Tax Review Should Go Beyond Return Preparation

A stronger review connects the tax return to entity structure, owner compensation, real estate activity, cash flow, investment income, and multi-year planning decisions.

| Review Area | What It Should Address |

|---|---|

| Return Preparation | Accurate preparation of business and owner-level returns. |

| Entity Structure | Whether the current structure still fits income, ownership, risk, financing, and growth. |

| Owner Compensation | Salary, distributions, draws, guaranteed payments, payroll, and retirement plan coordination. |

| Estimated Taxes | Whether payments and withholding match income timing and current-year expectations. |

| Deductions and Documentation | Whether expenses are properly classified, supported, and consistent with the business model. |

| Real Estate Activity | Rental income, depreciation, passive activity limits, basis, debt, and disposition planning. |

| Investment Income | Capital gains, interest, dividends, K-1s, liquidity events, and timing concerns. |

| Cash Flow Planning | Whether tax payments are aligned with the owner’s actual liquidity. |

| Multi-Year Strategy | How current-year decisions may affect future income, exits, and flexibility. |

| Advisory Action Items | What should be addressed after filing, before year-end, or before a major transaction. |

The review should not feel like a generic checklist. It should feel like a financial debrief. The return shows what happened. The advisory review explains what those facts mean.

For sophisticated taxpayers, the advisory portion is often where the real value appears.

Tax Preparation Looks Back. Advisory Review Looks Forward.

Tax preparation is historical. It organizes what already happened.

Advisory review is interpretive. It asks what those facts suggest about the next year, the next transaction, and the owner’s broader financial plan.

That difference is important because many tax problems do not begin as obvious mistakes. They begin as separate decisions that were never reviewed together.

A business owner increases profit but does not adjust estimated taxes. A real estate investor accelerates depreciation without reviewing the likely holding period. An S corporation owner takes distributions without tracking basis and compensation together. A high-income professional sells investments in the same year as a business income spike. A partnership allocates income without giving enough attention to capital accounts, debt allocation, and owner-level tax impact.

Each item may be reasonable on its own. The issue is the collision between them.

A tax preparation and advisory review should identify those collisions before they become expensive, confusing, or difficult to unwind. This is especially important for owners who already have advisors, because fragmented advice can still leave gaps when no one is reviewing the full tax picture from business return to personal return.

Why Florida Business Owners Need a Different Type of Review

Florida’s lack of individual state income tax can create a false sense of simplicity.

For many Florida taxpayers, the federal return carries most of the income tax burden. That makes federal planning especially important for business owners, real estate investors, and high-income households. The absence of Florida personal income tax does not eliminate the need to coordinate federal income tax, payroll tax, self-employment tax, capital gains tax, net investment income tax, depreciation, passive activity rules, and entity-level filings.

Florida business owners may also face state and local issues that do not show up as personal income tax planning. Depending on the business and entity type, this can include sales and use tax, reemployment tax, corporate-level tax filings, documentary stamp tax, property tax, local tax registrations, or industry-specific compliance.

The advisory review should not force Florida into every answer. It should focus on where Florida materially changes the planning conversation:

whether federal tax planning is carrying the full weight of the owner’s income tax exposure

whether the business has Florida sales or use tax considerations

whether real estate decisions are affected by Florida property tax, insurance, debt, repairs, and holding period pressure

whether residency, domicile, or remote work creates filing issues outside Florida

whether a Florida-based business owner has income sourced to other states

whether entity structure still fits the owner’s risk, growth, and future transfer goals

For Florida taxpayers with significant federal tax exposure, the absence of state income tax is not the end of planning. It is one reason federal planning needs to be more intentional.

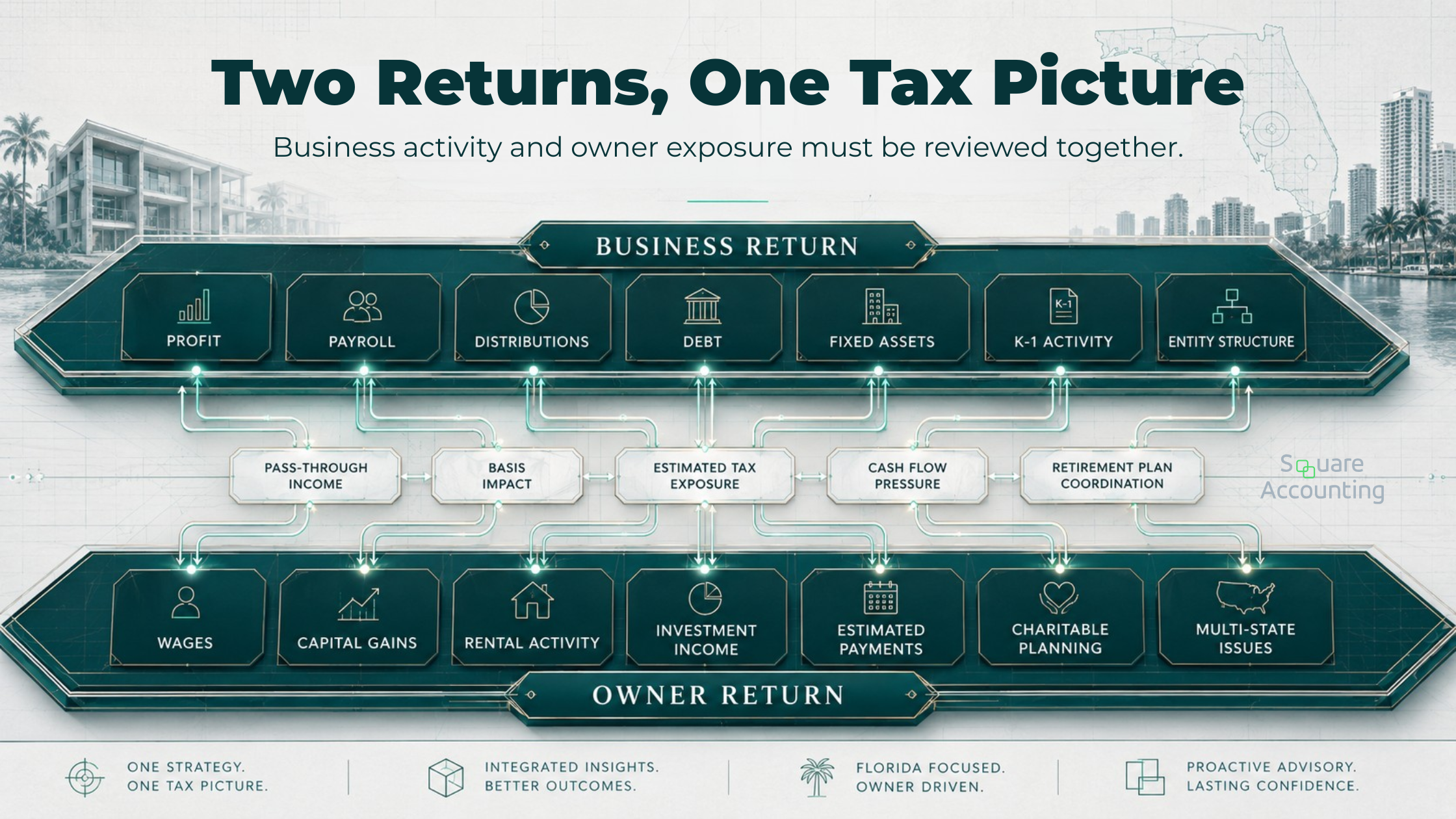

The Return Should Be Reviewed at Two Levels

A sophisticated review should look at both the business return and the owner’s personal return.

That is where many fragmented advisory relationships break down.

The business return may look clean on its own. The personal return may look accurate on its own. But the real planning question is how the two interact.

For example, an S corporation return may show profit, officer compensation, distributions, retirement contributions, shareholder loans, and retained earnings. The owner’s personal return may show wages, pass-through income, capital gains, charitable deductions, rental losses, investment income, estimated payments, and K-1 activity from other investments.

Reviewing either return alone may miss the planning picture.

The advisory review should connect them because the owner does not experience tax in separate silos. The owner experiences one total tax result, one cash flow reality, and one set of future planning constraints.

The owner’s real tax position often appears only when the business return and personal return are reviewed together.

“This is where a standard preparation process can become too narrow. The filing may be accurate, but the planning picture is incomplete if business-side facts are not connected to the owner-level tax result.”

Review where entity structure, estimates, basis, depreciation, and cash flow may need closer attention.

What We Look For in the Business Return

The business return should be reviewed for more than income and deductions.

A strong advisory review should evaluate the relationship between taxable income, book income, cash flow, balance sheet activity, owner withdrawals, payroll, debt, fixed assets, and entity structure.

The key question is not simply whether the business return is complete. The key question is whether the return reveals anything that should change how the owner manages the next year.

Important review areas include:

Entity Structure

The review should ask whether the current entity structure still fits the owner’s income level, risk profile, ownership plan, financing needs, and future exit.

An LLC, S corporation, partnership, or C corporation may have been reasonable when the business started. That does not mean it remains the best fit after income growth, new owners, real estate acquisitions, financing, succession planning, or a possible sale.

The issue is not whether the entity is “good” or “bad.” The issue is whether the structure still supports the taxpayer’s current facts.

A structure that works for annual filing may still create friction elsewhere. It may complicate a future sale, limit retirement plan design, create payroll issues, affect self-employment tax treatment, make ownership transfers more difficult, or leave real estate and operating risk too closely connected.

This is why entity review belongs inside an advisory discussion, not just at formation.

Owner Compensation and Distributions

For S corporation owners, compensation and distributions should be reviewed together.

A salary that is too low may create compliance risk. A salary that is too high may create unnecessary payroll tax cost or reduce planning flexibility. Distributions should also be reviewed against basis, cash flow, retained earnings, debt, and the owner’s personal tax picture.

For partnerships, guaranteed payments, draws, allocations, and self-employment tax treatment need careful review.

This is not just payroll mechanics. It affects retirement contributions, financing, estimated taxes, cash reserves, and the owner’s long-term planning options.

A common failure mode is reviewing compensation as a single-year number. A stronger review asks whether compensation supports the owner’s broader plan: retirement contributions, lending, cash flow, reasonable compensation support, and predictable tax payments.

Deductions and Classification

A tax review should examine whether expenses are properly classified, supported, and consistent with the taxpayer’s business model.

The question is not simply “Can we deduct this?”

Better questions include:

Is this ordinary and necessary for this business?

Is the documentation strong enough?

Is this a repair, improvement, capital asset, personal expense, or mixed-use item?

Does this deduction create a loss that is limited elsewhere?

Does accelerating this deduction create future tax pressure?

Does the deduction match the owner’s risk tolerance and documentation quality?

For high-income taxpayers, deduction quality matters as much as deduction amount.

A weak deduction may create more friction than value. A properly supported deduction that fits the business facts can be valuable. The advisory review should distinguish between the two.

Fixed Assets and Depreciation

Depreciation is one of the most important review areas for real estate investors and asset-heavy business owners.

The review should look at placed-in-service dates, asset classification, bonus depreciation, Section 179, listed property, repairs versus improvements, cost segregation, partial dispositions, and future recapture exposure.

This is where shallow planning often backfires.

Accelerating depreciation may reduce current-year taxable income, but it can also change the future planning picture. It may affect passive loss limitations, future depreciation availability, taxable gain on sale, depreciation recapture, debt-driven exit pressure, and the urgency of replacement property planning.

A strong review does not treat depreciation as a one-year savings tool. It asks whether the depreciation strategy fits the holding period, financing plan, income profile, passive activity position, and likely exit.

For Florida real estate investors, this is especially important because the income tax analysis may be federal, but the investment decision is often shaped by Florida-specific realities: insurance costs, property taxes, repairs, debt terms, rental demand, and whether the property will be held, refinanced, exchanged, gifted, or sold.

Balance Sheet and Basis

For pass-through business owners and real estate investors, the balance sheet can reveal issues that the income statement does not.

Debt, capital accounts, distributions, contributions, retained earnings, shareholder loans, partner basis, and property basis can all affect whether losses are deductible, whether distributions are taxable, and whether future exits create surprise income.

A return can be technically prepared while still leaving basis questions unresolved.

That is a problem because basis is often where tax planning becomes real. It can affect loss deductibility, distribution treatment, gain recognition, partner allocations, S corporation shareholder planning, and whether a transaction produces the tax result the owner expected.

An advisory review should identify those issues early. Waiting until a sale, refinance, ownership transfer, or IRS notice is usually when the options are narrower.

What We Look For in the Owner’s Personal Return

The personal return is where business, investment, real estate, and family financial decisions come together.

For high-income Florida taxpayers, this often includes wages, pass-through income, rental activity, capital gains, K-1s, retirement contributions, charitable giving, estimated taxes, itemized deductions, investment income, and sometimes multi-state filings.

The review should examine:

whether income was concentrated in one year

whether estimated taxes were aligned with actual income

whether capital gains could have been timed, offset, or planned more deliberately

whether rental losses are usable, suspended, or likely to become usable later

whether retirement contributions were coordinated with business income and payroll

whether charitable planning was reactive or intentional

whether K-1s created hidden tax exposure or basis issues

whether withholding and estimates matched real cash flow

whether the return shows a recurring issue that should be addressed before year-end

This is especially important when the taxpayer has multiple income streams.

A business owner who also owns real estate, receives K-1s, sells investments, and makes large charitable gifts does not have a simple tax profile. The return needs to be reviewed as one integrated financial picture.

This is also where the review can help a taxpayer who already has an advisor. The issue may not be that the current advisor is wrong. The issue may be that the business, investment, legal, and tax decisions are not being reviewed together at the right time.

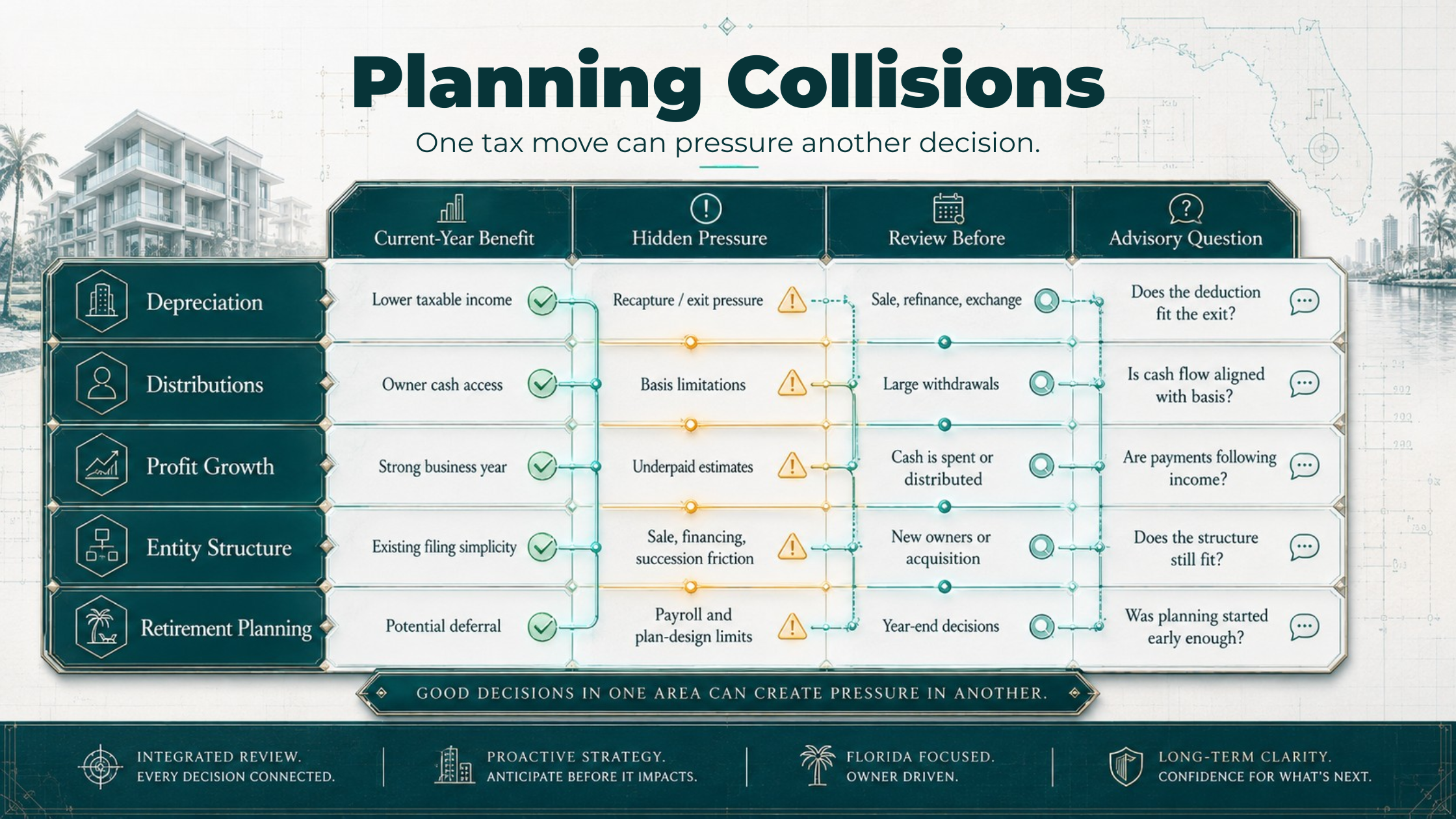

The Advisory Review Should Identify Planning Collisions

The most valuable part of the review is often not finding a missed deduction. It is identifying a collision between decisions that were made separately.

A planning collision occurs when one decision produces a favorable result in one area but creates pressure somewhere else.

A strong advisory review looks for the points where separate tax decisions start to work against each other.

“The risk is rarely one isolated tax item. The more important issue is whether current-year decisions are creating pressure in basis, cash flow, exit planning, estimated taxes, or owner compensation.”

Common examples include:

Depreciation vs. Exit Strategy

A real estate investor may use depreciation to reduce current income, but future sale planning may expose depreciation recapture, gain recognition, debt issues, suspended losses, and replacement property pressure.

The review should ask: Does the depreciation strategy match the likely exit?

If the owner expects to hold the property long term, accelerate deductions, refinance, exchange, or sell within a shorter window, the tax strategy may need to be different. The issue is not whether depreciation is useful. The issue is whether the depreciation plan fits the exit plan.

Distributions vs. Basis

An owner may take cash out of a business because the business has liquidity. But taxable basis may not support those distributions in the same way the bank balance appears to support them.

The review should ask: Are distributions being reviewed against basis, not just cash?

This matters for S corporation owners, partners, and real estate investors because cash flow and taxable basis do not always move together. Debt, losses, prior distributions, capital contributions, and ownership allocations can all change the answer.

Profit Growth vs. Estimated Taxes

A business may have a strong year, but estimates may still be based on the prior year or a lower income period.

The review should ask: Are tax payments following actual income timing?

This is one of the most practical benefits of an advisory review. It helps the owner avoid being surprised by a large balance due when cash has already been spent, reinvested, distributed, or used for debt service.

Entity Structure vs. Owner Goals

An entity may work for annual compliance but fail to support succession, sale planning, asset protection coordination, financing, or multi-owner complexity.

The review should ask: Is the entity structure still aligned with the next stage of the business?

This becomes more important when the owner is adding partners, buying real estate, hiring employees, considering a sale, gifting interests, or separating operating assets from investment assets.

Retirement Planning vs. Payroll Decisions

A business owner may want larger retirement contributions, but payroll, entity type, employee census, plan design, timing, and cash flow can limit what is available.

The review should ask: Were retirement planning options considered early enough?

Many retirement planning opportunities depend on decisions made before the return is being finalized. If the conversation starts only after year-end, the taxpayer may still have options, but the strongest options may require earlier design and coordination.

These are the issues that generic tax preparation often misses because they sit between tax filing, planning, legal structure, investment strategy, and cash flow.

Use our advisory lens to think through where entity structure, estimates, basis, depreciation, and cash flow may need closer review.

What Documents Should Be Reviewed?

A tax preparation and advisory review should be built on complete, organized information.

For a Florida business owner or investor, the document list may include:

business profit and loss statement

balance sheet

general ledger

payroll reports

owner compensation records

bank and credit card statements when needed

loan statements

fixed asset schedules

depreciation reports

closing statements for real estate purchases or sales

refinance documents

K-1s

1099s

W-2s

brokerage tax forms

retirement contribution records

charitable contribution records

prior-year tax returns

estimated tax payment history

entity formation documents when structure is being reviewed

operating agreements or shareholder agreements when allocations or ownership rights matter

prior advisory notes, projections, or year-end planning summaries if they exist

The goal is not to collect paperwork for its own sake. The goal is to make sure the review is based on the facts that actually drive tax outcomes.

Incomplete information can make the return look cleaner than the underlying situation really is. That is why bookkeeping quality, payroll records, loan activity, basis schedules, and real estate closing documents matter. They help connect the filed return to the economic reality behind it.

What the Advisory Conversation Should Cover

The advisory conversation should turn return findings into decisions.

For sophisticated taxpayers, that conversation should not be limited to whether the return is ready to file. It should cover what the return suggests about the next planning cycle.

Key questions include:

What changed from the prior year?

Which income streams created the most tax pressure?

Were any deductions unusually large, sensitive, or poorly documented?

Did real estate activity create losses, suspended losses, or future recapture exposure?

Did the business generate enough cash to support the tax cost?

Are estimated taxes aligned with the current year?

Should the entity structure be revisited?

Are retirement contributions being optimized within the taxpayer’s facts?

Are any planning opportunities dependent on action before year-end?

Are there issues that should be coordinated with an attorney, financial advisor, payroll provider, lender, or bookkeeper?

This is where the review becomes practical.

A good advisory review should produce action items, not just observations.

The best action items are specific enough to guide the next step. “Consider tax planning” is too vague. A stronger advisory note might identify that estimates need to be recalculated after a profit increase, basis schedules should be updated before another distribution, a cost segregation decision should be reviewed against the investor’s exit timeline, or payroll should be revisited before retirement plan contributions are modeled.

What This Review Is Not

A tax preparation and advisory review is not a promise to reduce tax.

It is not a search for aggressive deductions.

It is not a one-size-fits-all checklist.

It is not a replacement for legal, investment, or insurance advice.

It is also not the same as a full-year tax planning engagement. A review may reveal issues that require deeper planning, but the review itself is the diagnostic step. It identifies what needs attention, what can be addressed now, and what should be planned before future transactions occur.

That distinction matters.

Some issues can be corrected during preparation. Some can be addressed before filing. Some need to be planned prospectively. Some require coordination with other advisors. Some are simply warnings about how current-year decisions may affect future years.

This is why a review should be clear about scope. The return may reveal the issue. Solving the issue may require a separate planning project, a legal document review, updated bookkeeping, payroll changes, retirement plan analysis, or transaction modeling.

When Business Owners Benefit Most From This Type of Review

A tax preparation and advisory review is especially useful when the taxpayer has complexity that does not fit cleanly into a basic filing process.

This includes Florida business owners and investors who:

earn $250,000 or more annually

own an S corporation, partnership, or multiple LLCs

have real estate investments

receive multiple K-1s

expect a large income year

recently bought, refinanced, exchanged, or sold property

are considering cost segregation

have significant depreciation deductions

are planning a business sale or ownership transition

have growing payroll

are behind on estimated taxes

have multi-state activity

are unsure whether their current CPA relationship is proactive enough

want tax planning connected to long-term wealth decisions

The more moving parts a taxpayer has, the more important the review becomes.

The review is also useful for owners who feel their tax process is technically accurate but strategically thin. That is a common concern among high-income taxpayers. The return gets filed, but no one explains what the return is warning them about.

The Failure Mode: Filing an Accurate Return That Teaches You Nothing

The most common failure is not an incorrect return.

The most common failure is an accurate return that does not lead to better decisions.

A return can be accurate and still miss the planning value hidden in the facts. It can report income correctly without explaining why estimates failed. It can report depreciation correctly without discussing future recapture. It can report pass-through income correctly without analyzing whether the entity structure still makes sense. It can report rental losses correctly without discussing whether those losses are usable. It can report distributions correctly without explaining what basis looks like going forward.

That is the gap this review is designed to close.

Accuracy is the baseline. Insight is the value.

The deeper failure is that missed insight compounds. A small basis issue can become a distribution problem. A depreciation decision can become an exit-year problem. A payroll decision can limit retirement planning. A strong income year can turn into a cash flow problem when estimated taxes were not updated. A real estate acquisition can create complexity that the owner’s old entity structure was never designed to handle.

The return should not just tell the owner what happened. It should help the owner see what is starting to happen.

What a Strong Final Deliverable Should Include

After the review, the taxpayer should understand more than the amount due or refunded.

A strong deliverable should include:

completed tax returns

a summary of major tax drivers

explanation of unusual or sensitive items

estimated tax recommendations

planning issues identified during preparation

documentation concerns, if any

entity or compensation items to revisit

real estate or investment planning observations

owner-level tax considerations

recommended next steps before the next tax year progresses too far

For business owners with higher income, the most useful deliverable is often the advisory summary. It creates a bridge between compliance and planning.

That summary does not need to be long. It needs to be clear. The owner should leave the process understanding the major drivers of the return, the issues that require follow-up, and the decisions that should not wait until the next filing deadline.

We can review whether your current filing process is also producing clear planning action items.

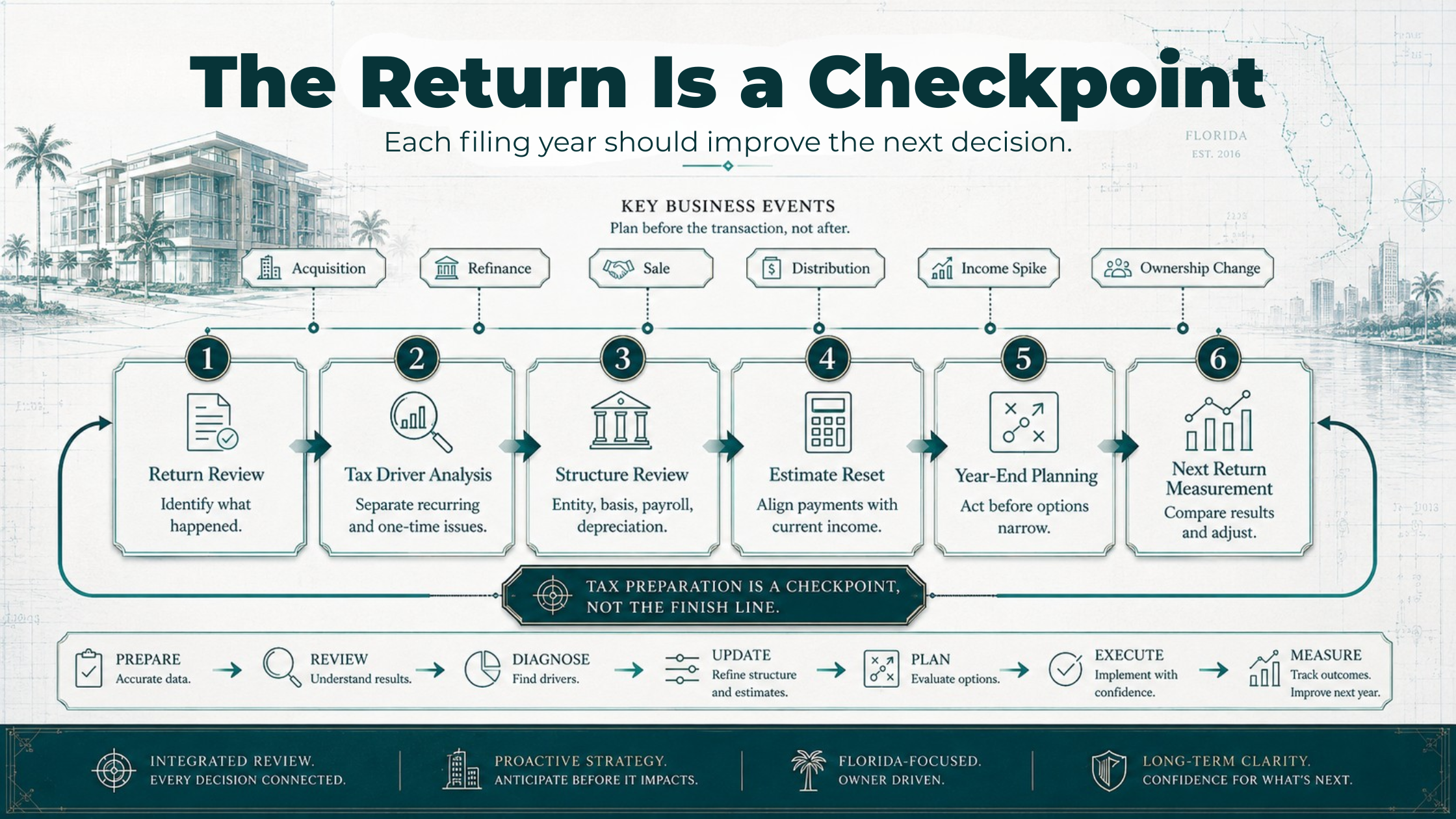

How This Fits Into Multi-Year Tax Planning

Tax planning is most effective when it is not compressed into filing season.

The tax return should feed into a broader planning cycle:

Prepare and review the return.

Identify the major tax drivers.

Separate one-time issues from recurring issues.

Review entity, compensation, basis, depreciation, and cash flow.

Update estimated taxes.

Plan before major transactions occur.

Revisit strategy before year-end.

Use the next return to measure what changed.

Each return should sharpen the next year’s planning decisions.

“The purpose of the cycle is not to make filing season longer. It is to make each return more useful by converting the prior year’s facts into current-year planning decisions.”

This cycle is especially important for Florida business owners and real estate investors because large federal tax outcomes can be driven by timing, structure, documentation, basis, and exit planning.

The return is not the end of the process. It is the evidence base for the next planning decision.

A multi-year view also changes how tax savings are evaluated. The best result is not always the lowest tax in the current year. Sometimes the better strategy is the one that preserves flexibility, avoids future recapture pressure, supports financing, keeps basis clean, coordinates with estate or succession goals, and gives the owner more control over timing.

That is the difference between tax preparation and tax strategy.

We help turn return findings into practical planning items for compensation, estimates, depreciation, basis, and business structure.

Tax Preparation and Advisory Review for Florida Business Owners: The Bottom Line

Tax preparation and advisory review for Florida business owners should include more than filing forms.

It should connect the tax return to the owner’s business structure, cash flow, compensation, real estate activity, investment income, estimated taxes, deductions, documentation, basis, and long-term planning goals.

For sophisticated taxpayers, the value is not only in knowing what happened last year. The value is in understanding what last year reveals about the next three to five years.

A well-prepared return keeps the taxpayer compliant.

A well-reviewed return helps the taxpayer make better decisions before the next transaction, distribution, acquisition, sale, or income spike creates another layer of tax exposure.

Schedule a focused review of your return, entity structure, estimates, cash flow, and planning priorities before the next major decision.

Tax Preparation and Advisory Review FAQs

Key questions for Florida business owners evaluating whether their tax return is simply being prepared or being used as a planning tool for income, cash flow, entity structure, estimates, and future transactions.

How is an advisory review different from simply asking a CPA to prepare the return?

A standard preparation process is usually focused on organizing last year’s information and filing the required forms accurately. An advisory review uses that same return as a diagnostic tool. We look at what the return reveals about income timing, estimated taxes, entity structure, compensation, depreciation, basis, real estate activity, and owner-level exposure. The difference is not just more conversation. It is a different purpose. The return is still prepared, but it is also used to identify planning issues that may affect the current year, the next transaction, or the owner’s broader financial position.

What should a business owner expect to learn from the review?

The owner should understand what drove the tax result, which items were unusual, which issues may need follow-up, and where current-year planning should begin. For a sophisticated taxpayer, the most useful insight is often not a missed deduction. It is seeing how different decisions interacted: distributions with basis, depreciation with exit strategy, profit growth with estimates, or payroll with retirement planning. A strong review should leave the owner with clearer tax drivers and practical next steps, not just a completed return and a balance due.

When should a Florida business owner start this process?

The review is most useful before filing, but the planning value should continue after the return is complete. Before filing, we can identify return issues, documentation gaps, estimated tax concerns, and planning items that should be understood before the return is finalized. After filing, the findings should become current-year action items. This matters because many planning decisions are easier to address before a major transaction, income spike, distribution, property sale, refinance, or year-end deadline. Waiting until the next filing season can narrow the available options.

Can this type of review help if the return was already prepared accurately?

Yes, because accuracy and planning value are not the same thing. A return can be technically correct and still fail to explain what the numbers mean. For example, it may report pass-through income correctly without addressing whether estimated taxes are aligned with current income. It may report depreciation correctly without discussing recapture pressure or future sale planning. It may report distributions correctly without explaining basis implications going forward. The review is valuable when it helps the owner understand what the return is warning them about.

Why does this matter if the business owner already has a CPA or advisor?

Many high-income owners have advisors, but the advice may still be fragmented. One advisor may focus on filing, another on investments, another on legal structure, and another on payroll or bookkeeping. The issue is not always poor advice. The issue is whether someone is connecting the business return, personal return, entity structure, cash flow, real estate activity, estimates, and long-term planning goals. An advisory review helps identify where those pieces are not moving together, especially when the owner has multiple entities, K-1s, real estate, or investment income.

What makes this review especially important for real estate investors?

Real estate can create tax results that look favorable in the current year but create future pressure. Depreciation, cost segregation, passive activity limits, debt, basis, refinancing, suspended losses, and exit planning all interact. The advisory review should ask whether the real estate strategy fits the investor’s actual plan: hold, refinance, exchange, gift, or sell. This matters because a deduction-focused approach may miss the future impact of depreciation recapture, gain recognition, debt relief, or replacement property timing. The review should connect current-year tax benefits with the likely exit path.

How should estimated taxes be handled in an advisory review?

Estimated taxes should be reviewed against actual income timing, not just last year’s result. A business owner may have a strong year, receive uneven income, take large distributions, sell an asset, or generate K-1 income that changes the owner-level tax picture. The review should identify whether tax payments and withholding are keeping pace with current-year expectations. This is less about predicting perfectly and more about avoiding avoidable surprises. For high-income taxpayers, the cash flow impact of underpaying during the year can be more disruptive than the tax calculation itself.

What is the clearest sign that tax preparation is too reactive?

The clearest sign is that the return gets filed but nothing changes. If the owner does not understand the major tax drivers, why estimates were off, whether basis is being tracked, how depreciation affects future exits, or which planning items need attention before year-end, the process may be too reactive. A strong tax preparation and advisory review should turn the return into a planning conversation. The owner should leave with more clarity about the next year, not just confirmation that last year was filed.