What Happens During a Tax Prep + Advisory Review?

A tax prep + advisory review is a structured meeting that prepares the current tax return and uses that return to identify planning decisions that should not wait until next year.

For a high-income taxpayer, that distinction matters.

Ordinary tax preparation is backward-looking. It answers: “What happened last year, and how do we report it?”

A tax prep + advisory review answers a wider set of questions:

What happened last year?

What tax positions are we taking, and why?

What is the return revealing about future tax pressure?

Which decisions should be made before year-end, before an acquisition, before a sale, or before income spikes?

Are your business, investment, real estate, and personal tax strategies working together or working against each other?

For Florida business owners, real estate investors, and high-income professionals, the review is not just a filing conversation. It is a planning checkpoint that turns the tax return into a diagnostic tool.

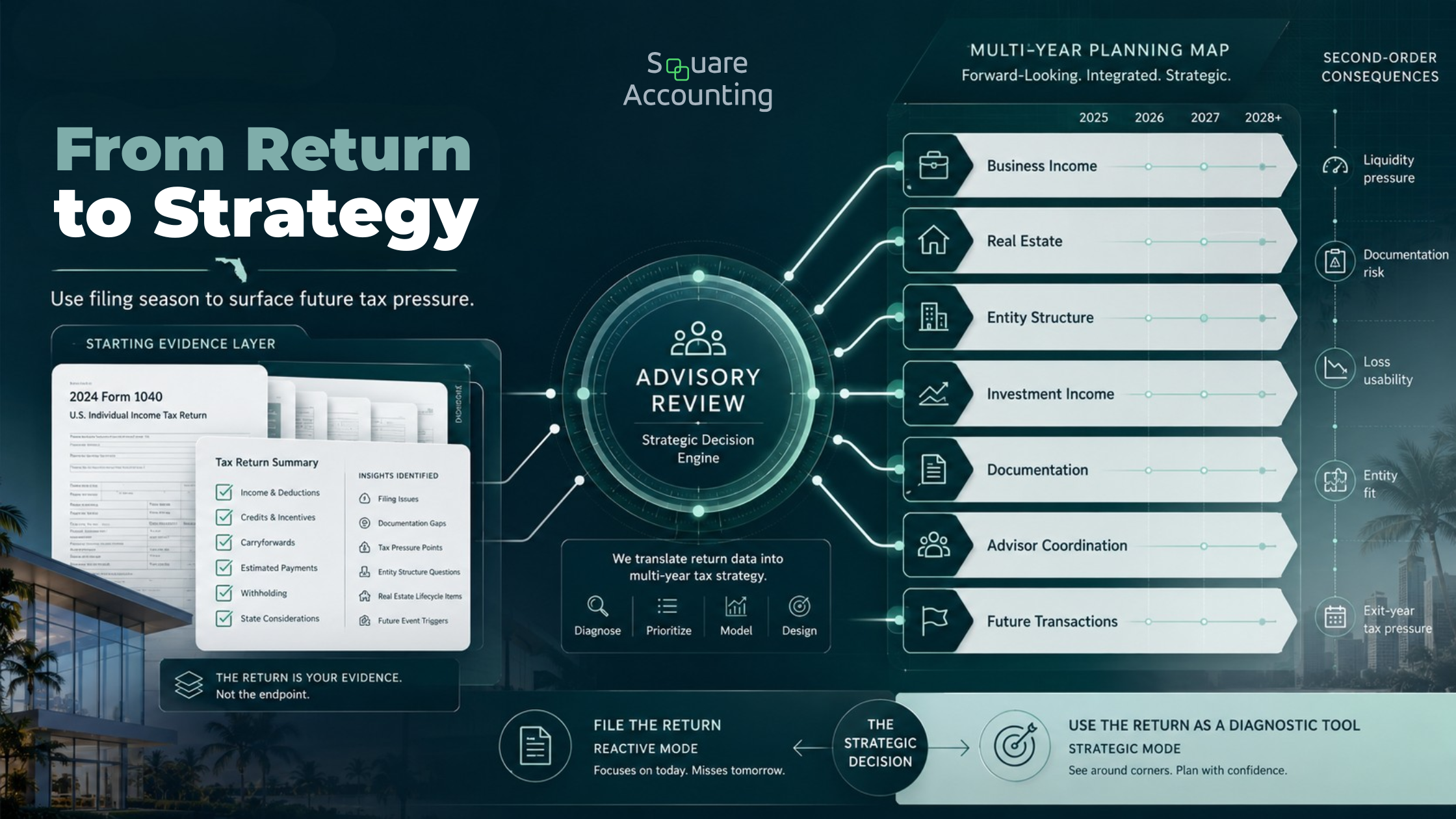

The return shows how income is being created, how deductions are being used, where cash flow is going, and where future exposure may be building. The advisory review is where those signals become decisions.

Key takeaway: A tax prep + advisory review should produce more than a completed return. You should leave with a clear view of what is being filed, what needs support, where future tax pressure is building, and which planning moves should be modeled before the next major deadline or transaction.

A tax prep + advisory review should connect today’s filing decisions to the next several years of business, investment, real estate, and exit planning.

“The strongest review does not treat the return as an endpoint. It uses the return as the starting point for identifying where future tax pressure may already be visible and which decisions should be sequenced before the next major deadline or transaction.”

What a Tax Prep + Advisory Review Actually Covers

During a tax prep + advisory review, we examine the current tax return, supporting records, business activity, investment activity, real estate holdings, and known future events to determine three things:

What must be filed now

What should be corrected, clarified, or documented

What planning should happen next

A strong review typically covers:

A Strong Tax Review Looks Beyond the Filed Return

A useful review connects filing accuracy with tax position quality, entity structure, real estate treatment, multi-year exposure, advisor coordination, and practical next steps.

| Review Area | What We Are Looking For |

|---|---|

| Current-Year Filing Accuracy | Income, deductions, credits, basis, estimated payments, entity reporting, and documentation. |

| Tax Position Quality | Whether key return positions are defensible and supported by the underlying facts. |

| Income Character | Ordinary income, capital gain, passive income, portfolio income, rental income, business income, and where those categories interact. |

| Entity Structure | Whether the current structure still fits income level, payroll, ownership, liability exposure, state footprint, and exit goals. |

| Real Estate Tax Treatment | Depreciation, passive activity limits, cost segregation timing, suspended losses, debt, refinancing, and sale planning. |

| Multi-Year Exposure | Income spikes, liquidity events, depreciation recapture, NIIT, retirement distributions, estate goals, and planned exits. |

| Advisor Coordination | Whether your CPA, attorney, bookkeeper, financial advisor, banker, and other advisors are working from the same facts. |

| Action Plan | What should happen before filing, after filing, before year-end, and before the next major transaction. |

The immediate deliverable is clarity around the return. The more valuable deliverable is a planning map.

For a sophisticated taxpayer, that map should not be a list of generic ideas. It should separate urgent filing issues from high-value planning decisions, then sequence those decisions around the calendar and the taxpayer’s actual financial moves.

We’ll review whether your current filing process is also surfacing the planning issues your return is already showing.

How This Differs From Standard Tax Preparation

Standard tax preparation is compliance-driven. That does not make it unimportant. Accurate filing, clean reporting, and timely submissions are foundational.

But compliance alone is not strategy.

A preparer may correctly file a return that still leaves a high-income taxpayer exposed to avoidable problems. The return may be technically accurate while still failing to address:

Whether a business owner’s entity structure still makes sense

Whether real estate losses are usable or simply accumulating

Whether depreciation is lowering tax now but creating a larger exit-year issue later

Whether a large gain will stack on top of other income and change the tax profile of the year

Whether estimated payments are aligned with current-year income

Whether tax planning is coordinated with legal, investment, and business decisions

The tax return is the record. The advisory review is the interpretation.

That difference is especially important for taxpayers who already have a CPA. The question is not whether someone can prepare the return. The question is whether the filing process is being used to surface decisions before they become expensive, compressed, or unavailable.

For a high-income taxpayer, the better question is not only, “Was my return filed correctly?”

It is, “What is this return telling us about the next three to five years?”

We help connect the return, entity structure, investment activity, and upcoming decisions into one advisory conversation.

Step 1: We Review the Tax Return as a Planning Document

The review starts with the return itself.

We look for accuracy, but also for patterns. High-income returns often reveal planning issues before the taxpayer feels them directly.

Examples include:

A business producing strong profit but inconsistent owner compensation

K-1 income arriving without enough withholding or estimated tax planning

Rental losses that look valuable on paper but are not currently usable

Large charitable gifts made without coordination around income timing

Capital gains realized in a year when income was already unusually high

Depreciation deductions taken without a clear hold-period or exit strategy

Multiple entities creating administrative complexity without enough planning benefit

This is where many tax conversations stop too early. They focus on whether an item is deductible or reportable.

We also ask whether the return is showing a mismatch.

A deduction may be allowed, but poorly timed. An entity may be valid, but outdated. A real estate loss may be real, but unusable. A tax reduction this year may create pressure in the year of sale.

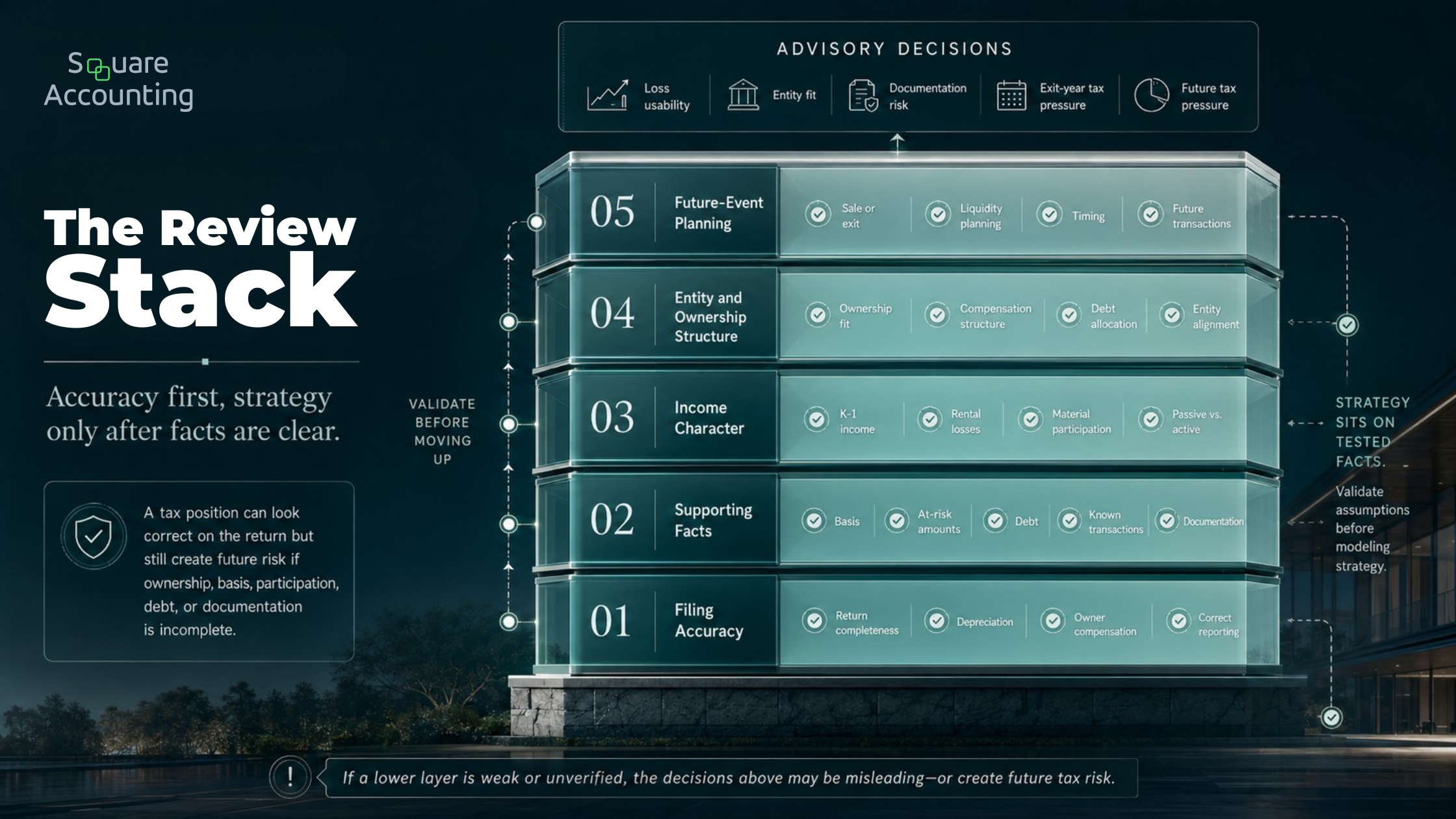

The return is not just a compliance document. It is the first layer of evidence.

Step 2: We Clarify the Facts Behind the Numbers

A tax return is only as strong as the facts behind it.

During the review, we clarify the assumptions that drive tax treatment. That may include ownership percentages, debt allocation, material participation, basis, at-risk amounts, entity elections, rental use, business purpose, related-party activity, and documentation.

This matters because tax planning can break down when the numbers are correct but the facts are incomplete.

The quality of an advisory review depends on whether the facts beneath the return can support the planning decisions above it.

“Before a strategy is modeled, the review has to test the assumptions underneath the return. That sequence helps separate real planning opportunities from positions that need better support, better documentation, or more careful classification.”

For a real estate investor, the return may show rental losses. The advisory question is not simply whether the losses exist. The better questions are:

Are the losses passive or nonpassive?

Are they currently usable?

Is there enough basis and at-risk amount?

Are suspended losses being tracked properly?

Is the taxpayer’s level of activity documented?

What happens if the property is sold, refinanced, contributed, converted, or exchanged?

For a business owner, the same principle applies. A company may show strong profit, but the review should ask whether compensation, distributions, retirement plan design, entity structure, debt, and exit goals are aligned.

This is one of the most common places where advisory value appears. A return can be arithmetically correct while still resting on facts that need better support.

Step 3: We Identify Tax Pressure Points

A useful advisory review separates small filing issues from meaningful tax pressure.

For high-income taxpayers, pressure usually builds in predictable places:

Ordinary income increasing faster than planning capacity

Business profit flowing through without adequate withholding or estimated tax payments

Capital gains stacking on top of already high income

Passive losses accumulating without a release strategy

Depreciation reducing current tax while increasing future recapture exposure

Entity structures remaining unchanged after the business has outgrown them

Investment income becoming subject to additional federal tax layers

Out-of-state activity creating filing or sourcing issues that are easy to miss from Florida

One example is the Net Investment Income Tax. Current IRS guidance states that a 3.8% NIIT applies to individuals, estates, and trusts with net investment income above applicable threshold amounts. It may apply to interest, dividends, certain rents, passive activity income, and gains from property dispositions, depending on the facts.

That makes income character and timing important for high-income investors. The advisory question is not just “Do you owe NIIT?”

It is, “Are your investment income, rental activity, business income, and gain recognition being managed together?”

A Florida taxpayer with no state personal income tax may still have a meaningful federal layering problem if investment gains, rental income, passive activity income, and business profit converge in the same year.

Step 4: We Connect the Current Return to Future Events

The best tax planning is often done before the event, not after it.

A tax prep + advisory review should surface future events that could change the taxpayer’s position. These may include:

Selling a business

Selling appreciated real estate

Refinancing investment property

Buying additional rental property

Moving from W-2 income to business ownership

Bringing in a partner

Changing entity structure

Exercising equity compensation

Entering retirement or semi-retirement

Relocating to or from Florida

Transferring wealth to the next generation

This is where the return becomes a forecasting tool.

A real estate investor considering a sale, for instance, needs more than a rough gain estimate. The IRS describes capital gain as selling an asset for more than adjusted basis, which makes basis tracking central to the analysis.

But a strategic review goes further. It considers depreciation history, suspended losses, debt payoff, state tax exposure if the property is outside Florida, potential exchange planning, estate goals, and what the cash will be used for after the sale.

The planning issue is rarely only “sell or hold.”

It is:

What tax cost appears in the sale year?

What losses, if any, may be released?

What recapture or gain character issues should be modeled?

What happens to liquidity after debt payoff and tax?

Does the taxpayer need replacement property, cash, debt reduction, diversification, or estate flexibility?

What planning windows close once the contract is signed?

This is the difference between reviewing a completed transaction and planning around a decision before it hardens.

Step 5: We Review Entity Structure Against Current Reality

Entity structure is not a one-time decision.

A structure that made sense when a business was generating $300,000 of profit may not fit when profit is $1.5 million, ownership has changed, payroll has expanded, debt has increased, or a sale is possible. Those figures are only examples. The point is that structure should be reviewed when the facts change.

During the review, we look at whether the structure still supports the taxpayer’s goals. This may involve:

Multi-entity real estate structures

Holding company arrangements

Management companies

Asset protection coordination with legal counsel

State filing obligations

Exit or succession planning

The goal is not to create complexity. The goal is to remove unnecessary friction.

A structure can fail in several ways. It can create avoidable payroll tax issues. It can obscure basis tracking. It can make real estate losses harder to analyze. It can increase bookkeeping burden without improving after-tax results. It can also work for operations but create problems when a partner exits or a buyer performs due diligence.

For Florida taxpayers, state income tax may not be the main issue. Florida Department of Revenue guidance states that Florida does not impose personal income tax, inheritance tax, gift taxes, or tax on intangible personal property, while also noting that Florida residents and businesses may be subject to other taxes and fees.

That is useful context, but it does not make entity planning simple. Florida business owners still need to consider federal income tax, payroll tax, sales and use tax where applicable, reemployment tax, corporate income tax where relevant, property tax, liability exposure, financing, and multistate issues if they operate or invest outside Florida.

Florida residency can simplify part of the tax picture. It does not replace planning.

We can help identify which business tax decisions should be modeled before income, payroll, or entity changes become fixed.

Step 6: We Examine Real Estate Decisions Beyond Depreciation

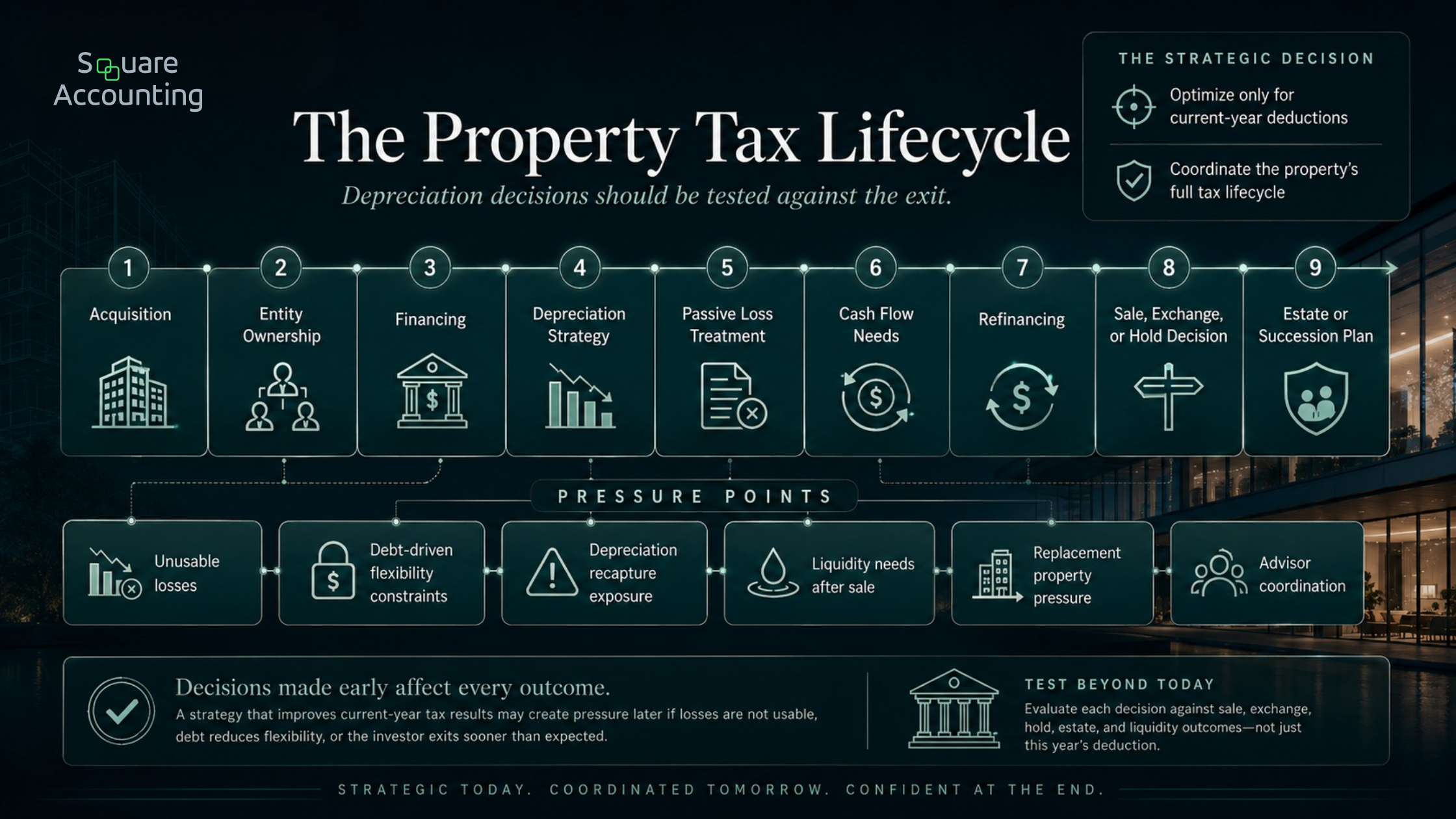

For real estate investors, tax planning often gets reduced to depreciation.

Depreciation matters. Cost segregation can matter. But depreciation is only one part of the real estate tax lifecycle.

A serious review looks at the full chain:

Acquisition

Entity ownership

Financing

Passive loss treatment

Cash flow needs

Refinancing

Sale, exchange, or hold decision

Estate or succession plan

The failure mode is easy to miss: a taxpayer may optimize for current-year deductions while ignoring the exit year.

Real estate tax planning is strongest when current deductions are evaluated against cash flow, loss usability, debt, and eventual unwind pressure.

“Depreciation is only one point in the ownership cycle. The more useful question is how each decision changes the investor’s flexibility when the property is refinanced, sold, exchanged, held long term, or transferred.”

That can create a distorted picture. The investor feels tax-efficient during the hold period but faces pressure when the property is sold, losses are released, debt is repaid, depreciation is recaptured, or replacement property cannot be identified on acceptable terms.

A tax prep + advisory review should not ask only, “Can we reduce tax this year?”

It should also ask:

What happens when this property exits the portfolio?

Are we creating deductions the taxpayer can actually use?

Are losses trapped, usable, or likely to be released later?

Does the depreciation strategy match the expected hold period?

Is the investor’s real estate activity passive, active, or mixed?

Would a sale improve liquidity but damage the broader tax plan?

Is the taxpayer using debt in a way that helps cash flow but creates future tax pressure?

Would estate planning change the preferred hold, sell, or exchange decision?

This is where shallow planning can backfire. A cost segregation study may create strong deductions, but if the taxpayer cannot use the losses, plans to sell sooner than expected, or needs a clean exit, the strategy needs more modeling.

Good real estate tax planning connects today’s depreciation to tomorrow’s unwind.

We review how depreciation, passive losses, debt, and sale timing may affect the next stage of your real estate plan.

Step 7: We Look for Advisor Fragmentation

Many high-income taxpayers already have advisors. That does not guarantee coordination.

A taxpayer may have:

A CPA preparing the return

A financial advisor managing investments

An attorney drafting entities or estate documents

A bookkeeper maintaining records

A banker financing acquisitions

An insurance advisor managing risk

Each advisor may be competent. The problem is that no one may be responsible for integrating the tax consequences across the full picture.

A tax prep + advisory review helps identify where advice may be fragmented.

Examples include:

The attorney creates entities, but the tax reporting does not match the intended structure

The investment advisor harvests gains without checking business income projections

The business owner funds a retirement plan without coordinating cash flow and payroll

The real estate investor pursues depreciation without considering passive loss limits

The taxpayer makes charitable gifts without aligning them with income spikes

A sale is negotiated before tax modeling is done

A bookkeeper codes activity in a way that obscures basis, loan activity, owner draws, or capital expenditures

The issue is rarely bad advice. More often, it is uncoordinated advice.

This is also why a tax prep + advisory review should be useful even when the taxpayer already has a CPA. The role of the review is not to criticize the existing advisor relationship. It is to make sure the return, records, entities, investments, and future events are being read together.

We help clarify which tax issues should be coordinated with your CPA, attorney, bookkeeper, investment advisor, or other professionals.

Step 8: We Discuss Risk, Documentation, and Defensibility

Tax strategy must be supportable.

The IRS states that Circular 230 governs practice before the IRS by setting mandatory rules of conduct for tax professionals engaging with the IRS on taxpayers’ behalf, including standards of competency, diligence, and ethical behavior.

A tax prep + advisory review should therefore include a practical discussion of documentation and risk.

That does not mean every position is conservative by default. It means the taxpayer should understand:

What position is being taken

What facts support it

What records should be retained

What assumptions are being made

Where judgment is involved

What the downside could be if challenged

Whether legal counsel should be involved

Sophisticated taxpayers do not need fear-based advice. They need clear risk classification.

Some issues are compliance problems. Some are planning trade-offs. Some are documentation gaps. Some are timing decisions. Some are legal questions. Some are not worth pursuing because the administrative burden outweighs the expected benefit.

A good review separates them.

Step 9: We Build the Post-Filing Action Plan

The review should not end with “Your return is ready.”

A useful tax prep + advisory review produces next steps. Depending on the taxpayer, those may include:

Adjusting estimated tax payments

Changing payroll withholding

Reviewing entity structure

Cleaning up bookkeeping categories

Tracking basis more carefully

Modeling a future property sale

Evaluating retirement plan design

Reviewing owner compensation

Planning charitable giving around income timing

Preparing for a business sale

Coordinating with legal or investment advisors

Scheduling mid-year and year-end planning reviews

The most important part is timing.

Some actions belong before filing. Some belong immediately after filing. Some belong before the next year-end. Some must happen before a transaction is signed.

The review should make that timing clear.

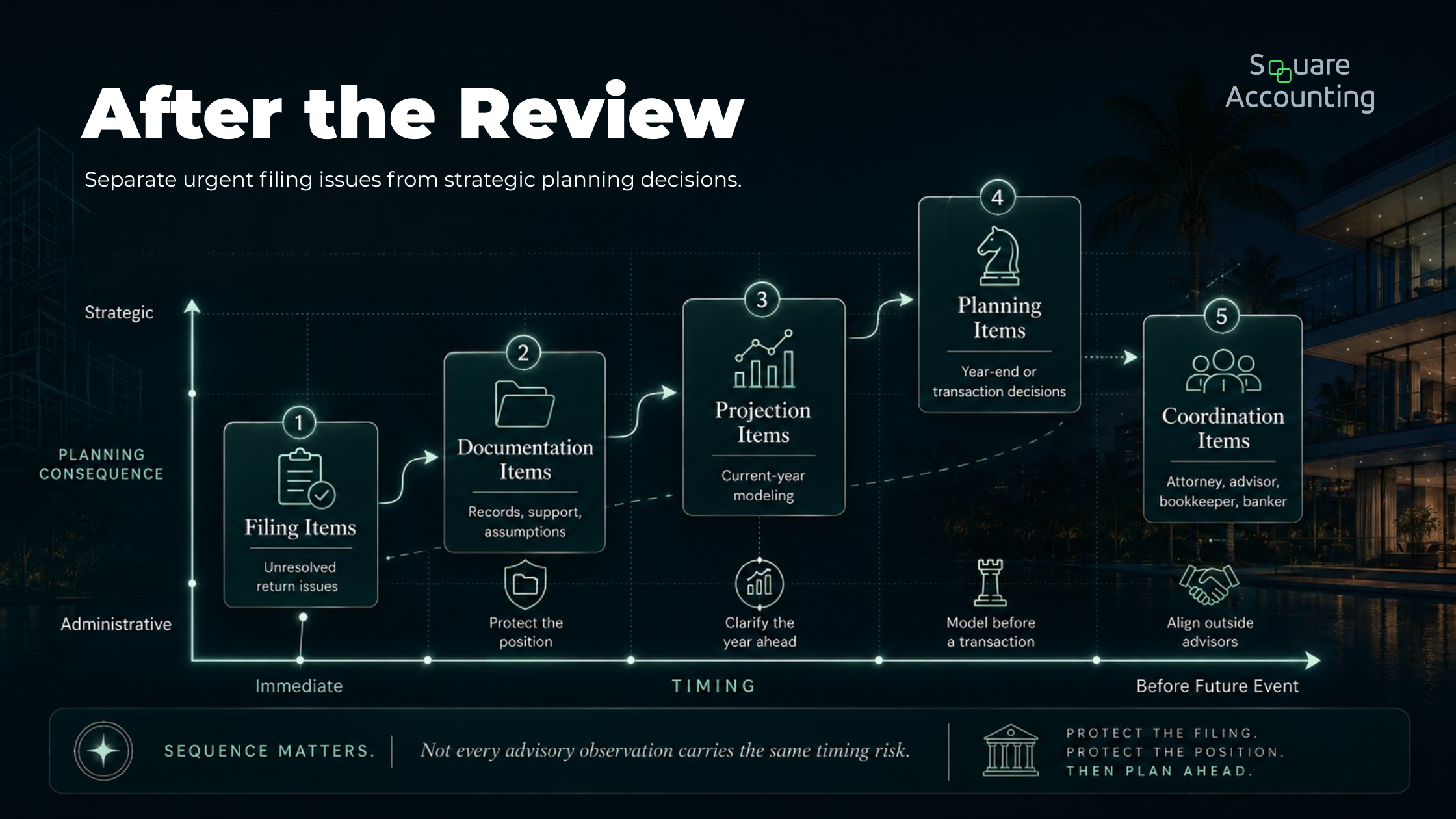

A simple way to think about the output is this: filing items protect the current return, documentation items protect the position, projection items clarify the year ahead, and planning items improve decisions before they become fixed.

What You Should Bring to a Tax Prep + Advisory Review

For high-income taxpayers, the most useful information is often broader than a standard tax organizer.

Useful items may include:

Prior-year federal tax returns

Current-year income documents

Business financial statements

General ledger or bookkeeping access

Payroll reports

K-1s

Real estate closing statements

Debt schedules

Depreciation schedules

Entity documents

Estimated tax payment records

Brokerage tax reports

Retirement plan information

Charitable giving records

Known upcoming transactions

Prior tax planning memos, if any

The point is not paperwork for its own sake. The point is judgment.

A closing statement may change basis. A debt schedule may change risk. An operating agreement may affect allocations. A payroll report may reveal compensation issues. A depreciation schedule may show future recapture pressure. A calendar of upcoming transactions may determine whether a strategy is still available.

Tax preparation looks backward. Advisory work needs visibility into what is coming.

What High-Income Taxpayers Should Expect to Walk Away With

A strong review should leave you with more than a completed return.

You should understand:

What is being filed

Why key positions were taken

Where the return shows planning pressure

Which items require better documentation

Whether estimated taxes need to change

What decisions should be made before year-end

Which strategies are worth modeling

Which popular tactics may not fit your facts

Whether your current structure still supports your goals

Which advisors need to be brought into the next conversation

You should also know what not to do.

That may be the most overlooked value of advisory work. Not every deduction is worth chasing. Not every entity structure is worth maintaining. Not every tax-saving idea improves after-tax wealth.

A tax strategy should serve the larger financial plan, not compete with it.

The Non-Obvious Risk: Optimizing the Wrong Year

The biggest weakness in reactive tax planning is that it optimizes the year already over.

That can create poor decisions for high-income taxpayers.

A business owner may accelerate deductions in a year when the larger issue is next year’s income spike. A real estate investor may focus on cost segregation without considering whether losses are usable. A professional may defer income without realizing that the next year may include a liquidity event. A taxpayer may avoid tax today only to create a more compressed tax problem later.

This is why we look at the current return in context.

The right question is not, “How low can we make this year’s tax bill?”

The better question is, “How do we reduce lifetime tax drag while preserving flexibility, liquidity, and defensibility?”

That is a different standard.

It also changes the advice. Sometimes the better strategy is not the one that produces the lowest current-year tax. It may be the one that keeps income smoother, protects liquidity, preserves basis, avoids trapping losses, or keeps an exit strategy open.

Why Florida Taxpayers Still Need Advanced Planning

Florida’s lack of personal income tax is valuable, but it can create a false sense of simplicity.

For Florida business owners and investors, the major planning issues are often federal, multistate, or transaction-driven. A Florida taxpayer may still face complex federal income tax issues, payroll tax decisions, NIIT exposure, passive activity limitations, depreciation recapture, corporate or partnership reporting, sales and use tax obligations, and tax consequences from out-of-state investments.

Florida also attracts relocating business owners, retirees, investors, and high-income professionals. Residency, domicile, asset location, and source income can become important when another state is involved.

That is why Florida planning should not be framed only as “no state income tax.” The stronger question is how Florida fits into the taxpayer’s overall tax architecture.

For an Orlando business owner, that may mean reviewing payroll, entity structure, sales tax exposure, retirement plan design, and future sale planning. For a Florida real estate investor, it may mean coordinating in-state property, out-of-state property, debt, depreciation, loss limitations, and exit strategy.

The Florida advantage is real. It works best when it is integrated into a broader plan.

When a Tax Prep + Advisory Review Is Especially Important

A review is useful every year, but it becomes especially important when something changes.

You should prioritize an advisory-level review if:

Your income has increased materially

You pay six figures in federal tax

You own multiple rental properties

You receive multiple K-1s

You are considering a real estate sale

You are planning a business sale or acquisition

You operate through an S corporation or partnership

You have large capital gains

You are relocating to Florida

You have out-of-state business or investment activity

You are unsure whether your advisors are coordinating

You feel like tax planning only happens after the year is over

The more moving parts you have, the less useful a purely transactional filing process becomes.

The review is especially valuable when the next decision has not happened yet. Once a property closes, a gain is realized, an entity is formed, a contract is signed, or a distribution is taken, the planning options may narrow.

What Happens After the Review?

After the review, the return may be finalized, revised, or held pending additional information.

The advisory items are then separated into practical categories:

Filing items:

What must be resolved before the return is submitted.

Documentation items:

What records should be gathered or improved.

Projection items:

What needs to be modeled for the current year.

Planning items:

What decisions should be made before year-end or before a transaction.

Coordination items:

What should be discussed with legal counsel, investment advisors, bookkeepers, or other professionals.

A useful review converts observations into sequenced action items so timing, documentation, projections, and coordination are handled in the right order.

“Not every issue uncovered in the review carries the same timing risk. Grouping the work by filing, documentation, projection, planning, and coordination helps identify what needs attention now, what should be modeled, and what needs outside advisor input.”

This keeps the process from becoming a long list of disconnected ideas.

The goal is not to overwhelm the taxpayer with possibilities. The goal is to identify the decisions that matter most, assign timing to them, and avoid letting next year’s tax problem become visible only after next year is already over.

Final Thoughts: What Happens During a Tax Prep + Advisory Review?

What happens during a tax prep + advisory review is simple on the surface: the return is reviewed, questions are answered, and filing decisions are made.

But for high-income Florida taxpayers, the real value is deeper.

The review should reveal what the tax return says about your business, investments, structure, timing, risk, documentation, and future tax exposure. It should connect the current filing season to the next several years of decisions.

That is the difference between preparing a return and managing a tax strategy.

For business owners, real estate investors, and high-income professionals, tax preparation should not be the end of the conversation. It should be the point where the planning becomes clearer.

Is a tax prep + advisory review the same as tax planning?

No. Tax preparation focuses on filing the return. Tax planning focuses on future decisions. A tax prep + advisory review connects both by using the current return to identify planning opportunities, risk, documentation gaps, and next steps.

When should a tax prep + advisory review happen?

It can happen during tax season, but the most valuable planning usually happens before year-end or before a major transaction. A tax-season review can identify issues, but some strategies may no longer be available once the year has closed.

Is this only for business owners?

No. It is also valuable for real estate investors, high-income W-2 professionals, executives with equity compensation, retirees with significant investment income, and taxpayers with multiple advisors or entities.

What makes this different from asking my CPA a few questions?

The difference is structure. A true advisory review is not a casual Q&A. It is a coordinated review of the return, facts, planning windows, risks, future decisions, and advisor coordination needs.

Does Florida’s lack of personal income tax make planning less important?

No. It changes the planning environment, but it does not eliminate federal tax, entity issues, payroll tax, real estate tax consequences, NIIT, multistate exposure, documentation risk, or exit planning.

We’ll use your current return and known future events to identify filing items, documentation needs, projections, and planning priorities.

Tax Prep + Advisory Review FAQs

Key questions for high-income taxpayers, business owners, and real estate investors evaluating whether the tax return is being used only for filing or as a planning document for future decisions.

How do I know whether my tax return is being used as a planning document?

A return is being used as a planning document when the conversation moves beyond whether the numbers are correct. We should be looking at what the return reveals about income character, entity structure, estimated tax pressure, real estate losses, depreciation, basis, and future events. For a high-income taxpayer, the return should help identify what decisions need attention before year-end, before a sale, or before income changes. If the process ends once the return is filed, the advisory value is probably limited.

Can an accurate tax return still miss meaningful planning issues?

Yes. A return can be technically accurate and still fail to address future tax pressure. For example, it may properly report business profit without questioning whether the entity structure still fits. It may show rental losses without determining whether they are usable. It may include depreciation without modeling what happens in the exit year. Accuracy is the foundation, but advisory work asks whether the current-year filing is aligned with the taxpayer’s broader business, investment, liquidity, and exit goals.

What should a high-income taxpayer ask during a tax prep + advisory review?

The strongest questions are not only about deductions. We would ask: What is driving my tax exposure this year? Which items are timing issues versus permanent issues? Are any losses trapped or deferred? Are my estimated payments aligned with current income? Does my entity structure still fit my income, payroll, ownership, and exit goals? What planning decisions need to happen before year-end or before a transaction? The goal is to leave with a prioritized decision list, not a collection of disconnected tax ideas.

What makes a tax prep + advisory review valuable for a real estate investor?

For real estate investors, the value is in connecting the full lifecycle of the property. The review should look at acquisition, entity ownership, financing, depreciation, passive loss treatment, cash flow, refinancing, and the eventual sale, exchange, or hold decision. A shallow review may focus only on current-year deductions. A stronger review asks whether those deductions are usable, how debt affects future flexibility, whether depreciation creates exit-year pressure, and how a sale or refinance could affect the broader tax plan.

How should Florida residency factor into the advisory review?

Florida residency may simplify part of the planning environment, but it does not eliminate the need for advanced tax review. We would still look at federal income tax, business tax issues, payroll decisions, real estate tax consequences, investment income, multistate activity, and out-of-state property or business interests. For Florida taxpayers, the advisory question is not simply whether the state tax environment is favorable. It is how Florida fits into the taxpayer’s overall structure, income sources, transaction plans, and long-term strategy.

What signs suggest my current tax process is too reactive?

A process is likely too reactive if planning discussions happen only after the year has closed, after a property sale, after a large gain, or after an entity decision has already been made. Other signs include recurring estimated tax surprises, unclear basis tracking, unused or suspended losses, disconnected advisors, and no clear year-end planning cadence. For high-income taxpayers, the issue is not just whether the return gets filed. It is whether the process identifies planning windows before they narrow.

How should advisor coordination be handled during the review?

Advisor coordination should start with shared facts. The tax return, entity documents, bookkeeping, investment activity, real estate records, and known future events need to be read together. We may identify items that should be discussed with an attorney, financial advisor, bookkeeper, banker, or other professional. The review should clarify who needs to be involved and why. The goal is not to replace existing advisors. It is to reduce the risk that competent advice is being delivered in disconnected pieces.

How should planning items be prioritized after the return is reviewed?

Planning items should be grouped by timing and consequence. Filing items need attention before the return is submitted. Documentation items protect the position being taken. Projection items help clarify the year ahead. Planning items should be addressed before year-end or before a major transaction. Coordination items may require input from legal, investment, bookkeeping, or banking advisors. This prioritization matters because not every issue has the same urgency. A useful review separates what is interesting from what is decision-critical.