When Florida Business Owners Should Upgrade From Tax Prep to Tax Planning

Florida business owners should upgrade from tax prep to tax planning when the return is no longer the main decision point.

That usually happens when your income is high, your entity structure affects your tax result, your real estate activity creates passive-loss or depreciation issues, or your business decisions today will shape the tax cost of an exit years from now.

Tax preparation answers, “What happened last year?”

The upgrade from tax prep to tax planning happens when tax outcomes are shaped by decisions made long before return season.

“A technically accurate return can still report an unmanaged outcome. The planning opportunity is to move the tax conversation upstream before compensation, entity structure, real estate activity, and exit decisions become difficult to change.”

Tax planning asks, “What should happen next, in what order, and with what consequences?”

For a high-income Florida business owner, that difference is not academic. A technically correct return can still leave you feeling like the tax result was unmanaged. The familiar moment is not, “Was the return filed correctly?” It is, “Why are we finding this out after the year is over?”

Key takeaway: Upgrade from tax prep to tax planning when your tax outcome is being determined by decisions that happen before return season: compensation, entity structure, real estate classification, depreciation timing, retirement plan design, capital gains, partner changes, or a future sale.

The upgrade is not about making taxes more complicated. It is about putting the tax conversation early enough in the decision cycle to matter.

When Florida Business Owners Should Upgrade From Tax Prep to Tax Planning: The Decision Test

Use this as a practical threshold test.

When Tax Preparation Should Become Tax Planning

Tax preparation may be enough for simple, stable facts. Planning becomes more important when income, entities, real estate, purchases, exits, or advisor coordination create timing and strategy pressure.

| Situation | Tax Prep May Still Be Enough | Upgrade to Tax Planning When... | Why It Matters |

|---|---|---|---|

| Your Income Is Stable and Simple | You have predictable income, few entities, and no major transactions. | Income is rising, uneven, or concentrated in one year. | Timing, withholding, retirement plan design, and estimated payments need coordination. |

| You Own an S Corporation or Partnership | The structure is already optimized and reviewed annually. | Compensation, distributions, QBI, or partner allocations are not being planned before year-end. | Entity structure can create or limit planning options. |

| You Own Rental Real Estate | Properties are passive, simple, and not generating major losses or gains. | You are using depreciation, cost segregation, short-term rentals, or real estate professional planning. | Classification and documentation affect whether losses are usable. |

| You Are Making Large Purchases | The purchase is operationally necessary regardless of tax treatment. | The tax deduction is driving the timing or size of the purchase. | Accelerated deductions can create future recapture, cash-flow, or financing problems. |

| You May Sell a Business or Property | No sale, recapitalization, or ownership change is expected. | An exit is possible within the next several years. | Sale structure, installment treatment, basis, recapture, and entity form need lead time. |

| You Work With Multiple Advisors | Each advisor handles a narrow issue and the issues do not overlap. | Your CPA, attorney, financial advisor, lender, and insurance team are not coordinating. | Fragmented advice often creates avoidable tax friction. |

| You Are a Florida Resident With High Federal Exposure | Your federal tax picture is straightforward. | You assumed Florida’s lack of personal income tax means less planning is needed. | Florida may reduce state income tax complexity, but federal planning remains central. |

The simplest rule is this: if your preparer can only tell you what should have been done after December 31, you have outgrown annual tax prep as your primary tax relationship.

That does not mean tax prep is unimportant. It means the preparation process is no longer sufficient by itself.

Tax Prep Records the Past. Tax Planning Changes the Order of Decisions.

Tax preparation is the compliance layer. A well-prepared return reports income, deductions, credits, depreciation, basis, payroll, estimated payments, and disclosures properly.

But tax preparation happens after most valuable decisions are already locked in.

By the time a return is prepared, you may have already:

Chosen an entity structure that no longer fits your income or exit goals

Paid yourself without reviewing reasonable compensation or retirement plan impact

Missed the window to adjust withholding or estimated payments intelligently

Bought equipment without modeling depreciation timing and cash use

Created passive losses you cannot currently use

Triggered capital gains, depreciation recapture, or NIIT exposure

Sold property or equity without reviewing allocation, basis, or installment-sale consequences

Made charitable gifts in a year when the tax value was lower than it could have been

Tax planning is not about finding a deduction in March. It is about sequencing business, investment, and personal decisions while there is still time to choose.

That sequencing matters because the best tax answer is often not the biggest current-year deduction. It is the decision that improves after-tax cash flow, protects optionality, and avoids creating a larger problem in a future year.

The Florida Factor: No State Personal Income Tax Does Not Mean No Tax Strategy

Florida’s tax environment changes the planning conversation, but it does not eliminate it.

Florida’s Constitution limits taxation on the income of natural persons, which is one reason Florida residents often focus primarily on federal income tax exposure rather than state personal income tax planning.

For business owners in Orlando, Central Florida, and across the state, that creates both an advantage and a blind spot.

The advantage is obvious: a Florida resident may avoid the state personal income tax layer that owners in many other states must model.

The blind spot is more subtle: federal ordinary income tax, payroll tax, Net Investment Income Tax, capital gains tax, depreciation recapture, and estate planning concerns can still drive a large lifetime tax cost.

Florida also has business-level tax considerations. The Florida Department of Revenue administers taxes and filings that can include corporate income tax, sales and use tax, and reemployment tax, depending on the business model and facts.

For a Florida service-based business owner, the planning question is not simply, “Do we have state income tax?”

The better question is, “Which federal and business-level tax decisions are now concentrated because Florida removed one layer of state tax friction?”

That is where proactive planning becomes valuable.

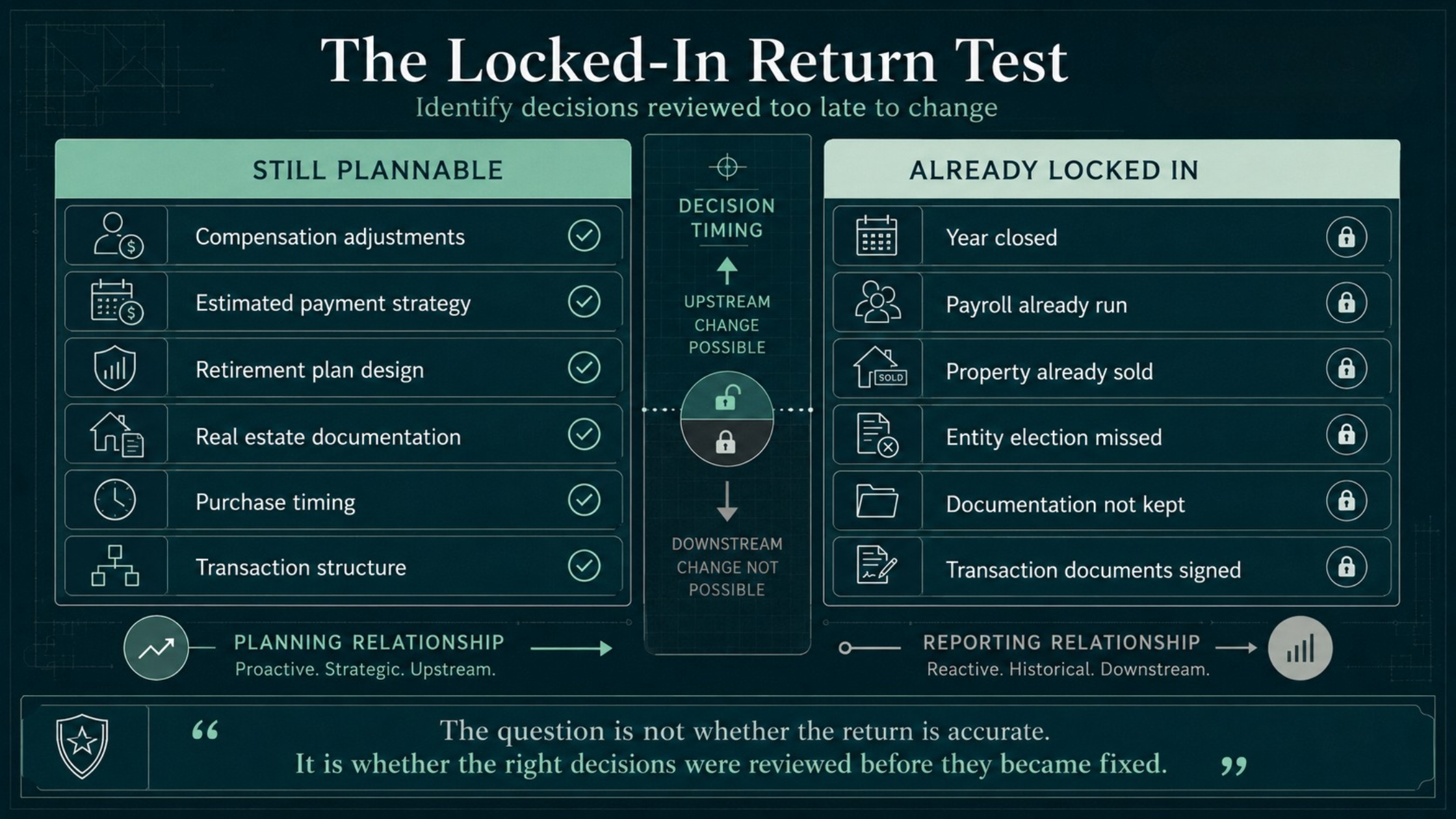

The “Locked-In Return” Test

A business owner should upgrade from tax prep to tax planning when too many tax outcomes are being decided before the tax professional sees them.

Ask these questions:

Could this year’s tax result have been materially different if decisions were reviewed earlier?

Are we discussing tax strategy before purchases, compensation changes, real estate transactions, ownership changes, or financing decisions?

Does our current advisor explain the future consequence of today’s deduction?

Are business income, real estate income, investment income, and estate planning being reviewed together?

Do we have a multi-year plan, or just a yearly filing process?

If the return only explains decisions after they are made, the relationship is reporting the outcome rather than shaping it.

“The issue is not whether the return is prepared correctly. The issue is whether the planning process has enough lead time to influence the decisions that create the return.”

If the honest answer is that the return is mostly a postmortem, you do not have a planning relationship. You have a reporting relationship.

That may have been enough at one stage of the business. It usually is not enough once income, assets, and exit options become meaningful.

The locked-in return test is especially useful for owners who already have a CPA. The issue is not whether the CPA is competent. The issue is whether the engagement is designed to influence decisions before the tax year closes.

We’ll help you determine whether your current tax relationship is still built around filing or needs earlier planning involvement.

Why High-Income Service Business Owners Outgrow Annual Tax Prep

Service businesses often look simple from the outside. There may be no inventory, no complex manufacturing, and no large fixed-asset base.

But high-income service businesses can create some of the most sensitive tax planning issues because the owner’s personal labor, compensation, entity structure, and cash flow are closely connected.

A Florida consultant, physician, attorney, marketing agency owner, engineering firm owner, or professional practice owner may need to coordinate:

Owner health insurance treatment

Family employment, where appropriate and supportable

State and local exposure if services cross state lines

QBI deduction limitations and planning

Estimated tax payments and cash reserves

Buy-sell agreements and succession planning

Entity structure before a sale or partner admission

The qualified business income deduction can be valuable for eligible pass-through owners, but it has limitations tied to income, business type, wages, and qualified property. The IRS describes the deduction as allowing eligible taxpayers to deduct up to 20% of qualified business income, plus certain REIT dividends and publicly traded partnership income, subject to important limits.

That is exactly the kind of issue that should not be reviewed for the first time during return preparation.

For service-business owners, the tax return may look clean while the planning is still underdeveloped. The return can show the income, salary, distributions, pension contribution, and estimated payments accurately. It cannot retroactively decide whether those choices were coordinated well.

We can review how your entity, compensation, real estate, and income timing are interacting before another year closes.

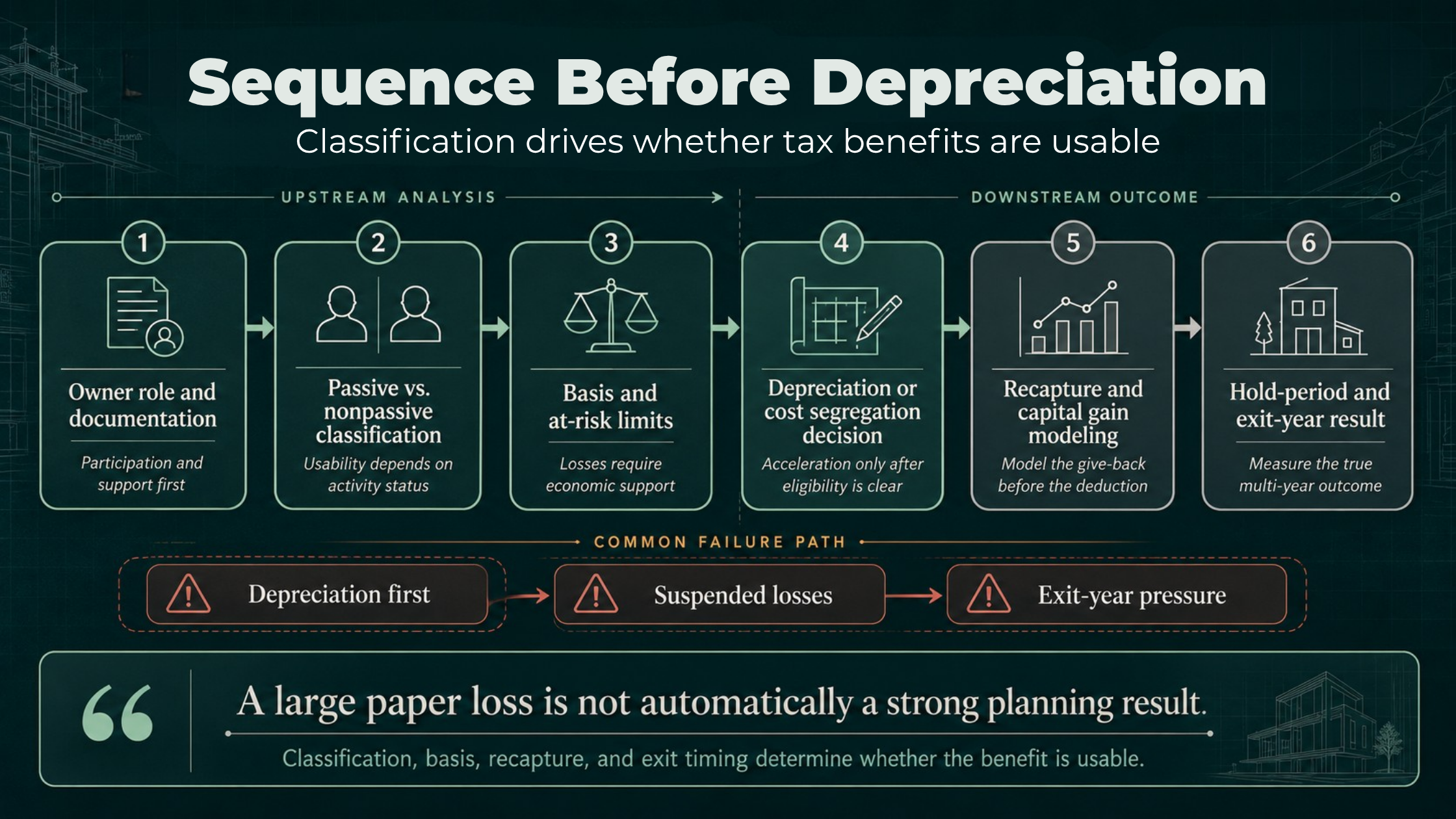

Real Estate Investors Should Upgrade Earlier Than They Think

Real estate investors often assume tax planning begins with depreciation. It does not.

It begins with classification.

The same property can produce very different tax outcomes depending on whether the activity is passive or nonpassive, whether the owner materially participates, whether a real estate professional position is supportable, whether short-term rental rules are involved, and whether losses are limited by basis, at-risk rules, or passive activity rules.

The IRS generally treats rental activity as passive even if the taxpayer materially participated, unless the real estate professional rules apply. IRS Publication 925 also addresses passive activity and at-risk rules that can limit deductible losses.

This is where many high-income investors get surprised. They may complete a cost segregation study, create a large paper loss, and then discover that the loss is suspended because the activity classification was not planned first.

That is not a deduction problem. It is a sequencing problem.

A better planning order is:

Determine the owner’s role and documentation position.

Review passive, nonpassive, and short-term rental treatment.

Model basis, at-risk limitations, and income needed to absorb losses.

Decide whether cost segregation or accelerated depreciation fits the plan.

Model the exit year, including recapture and capital gain exposure.

Coordinate real estate strategy with business income, investment income, and estate planning.

Depreciation strategy is strongest when it follows classification, basis, and exit modeling rather than leading the analysis.

“A large paper loss is not the same as a usable planning result. The investor’s role, documentation, basis, and exit timeline determine whether the strategy improves after-tax wealth across the full hold period.”

Depreciation can improve current-year tax efficiency, but it is not free. IRS Publication 946 explains depreciation for business and income-producing property, while IRS Publication 544 addresses the tax rules that apply when property is disposed of.

The planning question is not, “Can we create a deduction?”

The better question is, “Will this deduction improve after-tax wealth across the hold period and exit?”

For Florida real estate investors, that question becomes even more important when a portfolio includes rentals, short-term rentals, development activity, or properties held in different entities. A strategy that works for one property can create basis, financing, or exit-year pressure in another.

We’ll help assess whether classification, basis, passive-loss limits, and exit-year pressure are aligned before depreciation strategy drives the decision.

The NIIT Layer Many Owners Miss

High-income Florida business owners who also invest in real estate or taxable portfolios need to watch the Net Investment Income Tax.

The IRS states that NIIT applies at 3.8% to the lesser of net investment income or the amount by which modified adjusted gross income exceeds the statutory threshold. The listed thresholds include $250,000 for married filing jointly or qualifying surviving spouse, $200,000 for single or head of household, and $125,000 for married filing separately.

NIIT planning is often missed because it sits between categories. It is not just a business issue, not just an investment issue, and not just a real estate issue.

It can be affected by:

Passive rental income

Capital gains

Portfolio income

Business income levels

Roth conversion timing

Installment sale structure

Gain harvesting or loss harvesting

Real estate professional classification

Charitable planning

Trust and estate income

A tax preparer may calculate NIIT correctly. A tax strategist asks whether the income mix, timing, and classification could have been managed differently before the tax year closed.

For a high-income owner, the NIIT layer can also change how a good idea is sequenced. Selling an appreciated asset, converting retirement assets, harvesting gains, or shifting rental activity classification may each be reasonable in isolation. Combined in the same year, they can create a different tax result than expected.

We can help connect business income, real estate activity, investment income, and advisor input into a more deliberate planning sequence.

The Most Common Failure Mode: One-Year Optimization

The most expensive tax mistakes are rarely caused by ignoring deductions. They are often caused by optimizing one year while damaging the next five.

This happens when the tax conversation starts with a narrow question: “How do we reduce this year’s bill?”

That question is understandable. It is not complete.

A better question is: “What does this year’s tax move do to next year’s cash flow, future borrowing capacity, basis, recapture exposure, retirement plan commitments, and exit options?”

Buying assets mainly for the deduction

A business owner buys equipment in December to reduce taxable income. The deduction helps this year, but the purchase strains cash flow, reduces borrowing flexibility, or creates recapture exposure if the asset is sold or business use changes.

Under current IRS guidance, certain qualified property acquired after January 19, 2025 may be eligible for 100% additional first-year depreciation, subject to the detailed timing and eligibility rules.

That makes planning more important, not less. A larger available deduction increases the need to ask whether the timing, financing, and future exit consequences make sense.

Using cost segregation without an exit model

Cost segregation may be valuable for a real estate investor with the right income profile, documentation, and holding period.

But if a sale, refinance, ownership change, or 1031 exchange is possible in the near term, the analysis should not stop at the first-year deduction. Depreciation, basis, suspended passive losses, recapture, debt paydown, and sale structure all affect the ultimate result.

A cost segregation study can improve timing. It does not eliminate the need to model the unwind.

Electing S corporation status without compensation planning

An S corporation can be useful, but it is not a set-it-and-forget-it structure.

Reasonable compensation, payroll compliance, distributions, retirement plan contributions, shareholder basis, health insurance treatment, accountable plans, and future sale structure all need review.

The mistake is treating the election as the strategy. The election is only the container. The planning value depends on how the owner operates inside that container.

Treating retirement plans as a deduction instead of a design decision

A retirement plan is not just a year-end deduction. Plan selection affects employee costs, owner contribution capacity, cash-flow commitments, payroll systems, compliance obligations, and long-term wealth location.

For a high-income owner, the wrong plan can be too small to matter, too expensive to maintain, or too rigid for the business’s cash flow.

The right plan design starts with income, payroll, staffing, age demographics, owner goals, and liquidity. The deduction is the result, not the starting point.

Looking at business and real estate separately

A high-income owner may operate a service business, own rental real estate, invest through taxable brokerage accounts, and hold assets in trusts or family entities.

If each advisor looks at only one piece, the plan can work in isolation and fail in combination.

A real estate loss strategy can collide with business income timing. A retirement contribution can affect cash needed for an acquisition. A property sale can push income into a year already shaped by business growth. A business exit can expose years of uncoordinated entity decisions.

That is the core reason to upgrade. Not because the return is complicated, but because the decisions are connected.

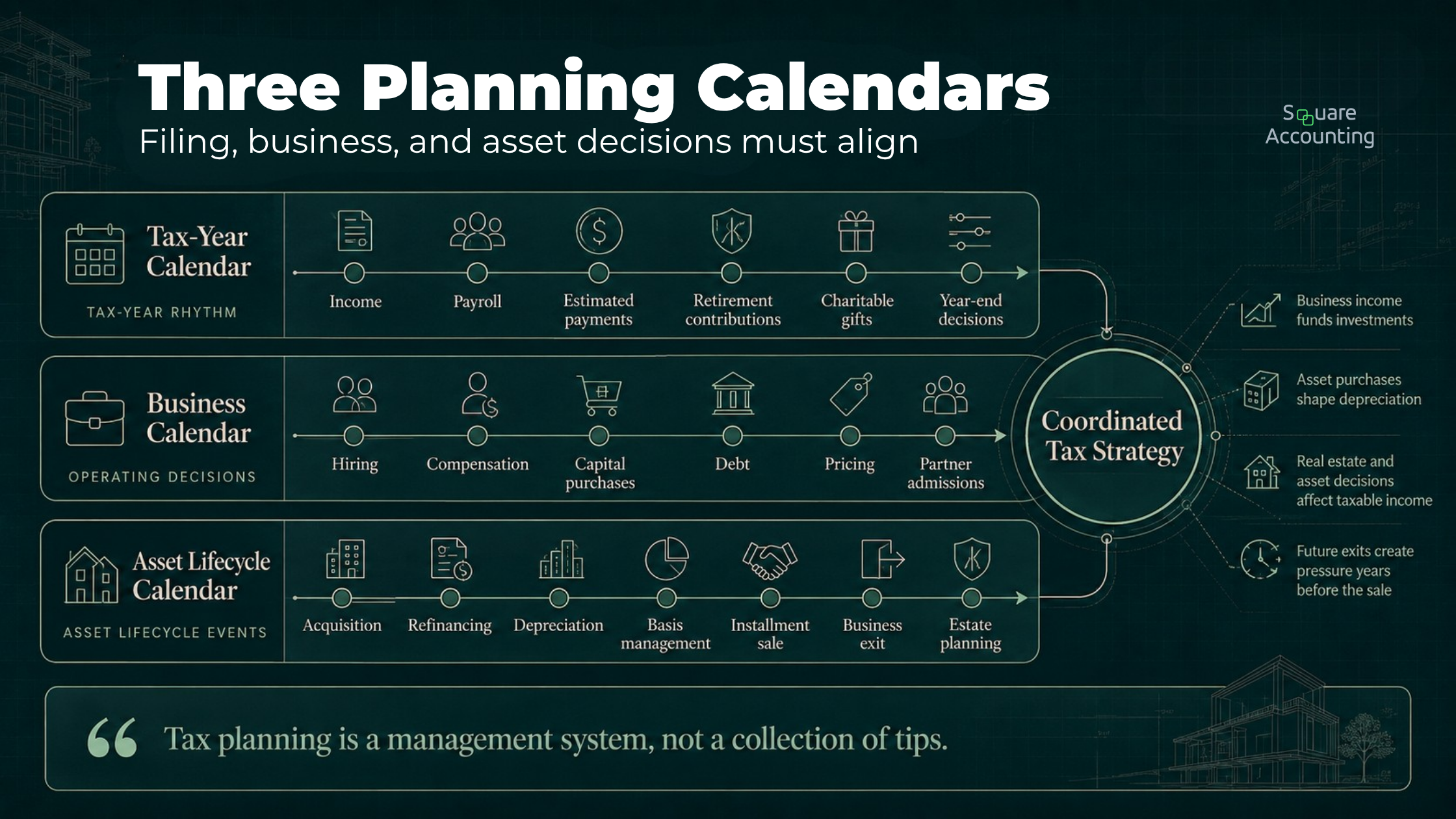

A Better Framework: The Three Calendars of Tax Planning

Most tax prep relationships operate on one calendar: the filing calendar.

Strategic tax planning works across three calendars.

Strategic tax planning connects the filing calendar to the business calendar and the asset lifecycle calendar.

“Most tax prep relationships operate around deadlines. High-income owners need a planning rhythm that also tracks compensation changes, capital purchases, real estate activity, financing, and exit readiness.”

1. The tax-year calendar

This includes income, deductions, payroll, estimated payments, retirement contributions, charitable gifts, and year-end decisions.

This calendar matters, but it is the shortest planning window. It is where many tactics live. It is rarely where the highest-value structure decisions begin.

2. The business calendar

This includes hiring, compensation, capital purchases, debt, pricing, entity changes, partner admissions, new locations, and cash-flow management.

For a Florida business owner, this calendar often determines the tax result before the return is ever prepared.

A planning relationship should be close enough to the business calendar to catch decisions while they are still adjustable.

3. The asset lifecycle calendar

This includes real estate acquisitions, refinancing, depreciation, basis management, installment sales, business exits, estate planning, and wealth transfer.

This is where sophisticated tax planning often creates the most value. The goal is not only to reduce this year’s tax. The goal is to reduce avoidable tax drag across the ownership period.

When these three calendars are not coordinated, planning becomes reactive. When they are coordinated, tax strategy becomes part of business strategy.

When Tax Prep Is Still Enough

Not every business owner needs a full advisory relationship.

Tax prep may be enough when:

Income is modest or highly predictable

There is one simple entity

There are no major real estate holdings

There are no expected ownership changes

There is no near-term business sale or property sale

The owner does not need help with timing, structure, or coordination

The tax result is not materially affected by decisions made before year-end

For those taxpayers, a competent preparer may provide exactly what is needed.

But that is not the profile of most high-income Florida owners paying six figures in federal tax, managing multiple entities, buying real estate, or considering a future exit.

What a Real Tax Planning Relationship Should Include

Upgrading from tax prep to tax planning should not mean paying more for a longer meeting in March.

A serious planning relationship should include a forward-looking review of the decisions that drive tax cost.

That typically includes:

Multi-year income modeling. Not just what income was last year, but what income is likely over the next several years and which years may carry unusual pressure.

Entity structure review. LLC, S corporation, partnership, and C corporation decisions should be evaluated based on current income, cash flow, risk, ownership, financing, and exit goals.

Owner compensation planning. Salary, distributions, guaranteed payments, payroll taxes, retirement contributions, and reasonable compensation should be reviewed together.

Real estate tax strategy. Passive activity treatment, material participation, real estate professional status, cost segregation, depreciation, refinancing, and exit planning should be coordinated.

NIIT and capital gain planning. Investment income, rental income, business income, and gain events should be modeled together.

Retirement and wealth-location planning. The plan should consider where wealth is accumulating: inside the business, inside qualified plans, in real estate, in taxable accounts, or in estate planning structures.

Exit-readiness planning. If a sale is possible, tax planning should begin years before a letter of intent.

Quarterly tax check-ins. High-income owners should not discover the year’s tax result after the year is over.

The most important deliverable is not a binder of ideas. It is a coordinated sequence of decisions.

A useful planning relationship should also show trade-offs. A recommendation without the downside is not strategy. It is a tactic waiting to be misunderstood.

We’ll review the decisions already shaping your tax result and identify where earlier coordination may be needed.

The Consultation Should Not Start With “How Much Can You Save Me?”

A better first question is: “Where are my tax outcomes already being determined before anyone reviews them?”

A useful planning consultation should review:

Last two years of tax returns

Current year profit and loss

Entity structure and ownership

Payroll and owner compensation

Retirement plan setup

Real estate schedule and depreciation reports

Expected acquisitions or dispositions

Estimated payments and cash reserves

Business sale or succession timeline

Current advisor team and where coordination is missing

This is how a consultation moves from generic deduction talk to actual strategy.

For sophisticated owners, the goal is not a list of tax tips. The goal is to identify leverage points.

The right conversation should make the owner feel more oriented, not more dazzled. It should clarify what is already working, what is exposed, what needs documentation, and what needs to be sequenced before the next major decision.

The Right Time to Upgrade Is Before the Big Event

Many business owners wait until something major happens.

They sell a property.

They receive an offer for the business.

They have a record income year.

They buy a large building.

They add a partner.

They move assets into a trust.

They change payroll.

They expand into another state.

By then, some of the best planning options may be reduced or gone.

The better time to upgrade is when any of these events becomes likely, not when the documents are already signed.

For Florida business owners, the best tax planning often happens in the quiet period before the transaction. That is when entity structure, income timing, compensation, depreciation, financing, and exit terms can still be shaped.

This is also when advisor coordination matters most. The attorney may be drafting documents. The lender may be setting covenants. The financial advisor may be planning liquidity. The CPA may be waiting for year-end records. If those conversations are not connected, the tax result can be determined by decisions no one reviewed together.

We can help evaluate tax structure, timing, and advisor coordination before a sale, partner change, or major transaction becomes difficult to unwind.

Conclusion: The Upgrade Is Really From Filing to Strategy

When Florida business owners should upgrade from tax prep to tax planning depends less on the size of the return and more on the number of decisions affecting the outcome.

If your tax bill is large but predictable, your structure is current, your real estate is simple, and no major transaction is coming, tax preparation may be enough.

But if your income, entity structure, investments, real estate, and exit options are starting to interact, annual tax prep is too narrow.

The return will still need to be prepared. But the real value comes before that, when decisions can still be made in the right order.

That is the point of upgrading: to stop treating tax as an annual filing event and start treating it as a multi-year business and wealth strategy.

Tax Planning vs. Reactive Tax Preparation FAQs

Key questions for Florida business owners, high-income taxpayers, and real estate investors evaluating whether their current tax process is proactive enough for income, entities, investments, and future transactions.

How do I know whether my current CPA relationship is too reactive?

A reactive relationship usually shows up in timing, not technical quality. Your return may be accurate, but the planning conversation happens after compensation, purchases, real estate activity, estimated payments, or ownership decisions are already locked in. For a high-income Florida owner, the key question is whether your advisor is helping shape decisions before year-end or mainly explaining the result afterward. We look for signs that business income, entity structure, real estate, investment income, and exit goals are being reviewed together rather than handled as separate filing issues.

What should a Florida business owner review before year-end?

Before year-end, the focus should be on decisions that can still be changed. That may include owner compensation, estimated payments, retirement plan design, asset purchases, charitable giving, real estate activity classification, and expected gain events. The point is not to force deductions into December. It is to decide whether the year’s income, cash flow, and future plans support the move. We would rather see a smaller current-year benefit that fits the broader plan than a larger deduction that creates cash-flow strain, recapture exposure, or future planning pressure.

Can tax planning still help if the current-year return is already being prepared?

Yes, but the value is usually different. Once the year has closed, many structure, payroll, depreciation, and timing decisions cannot be redesigned for that year. A tax-preparation review can still identify reporting issues, carryforwards, documentation needs, and planning themes for the next cycle. The more valuable work is often using the current return as a diagnostic tool. We can see where outcomes were locked in too late, where advisors were not coordinated, and which decisions should move earlier in the calendar going forward.

Why do real estate tax strategies sometimes fail for high-income investors?

They often fail because the deduction is evaluated before the investor’s classification, income profile, basis, and exit plan are understood. A cost segregation study or accelerated depreciation strategy can create a large paper loss, but that does not mean the loss is currently usable. Passive activity rules, material participation, real estate professional positioning, at-risk limits, and basis can all affect the result. We also want to understand what happens at sale, refinance, or ownership change. A real estate tax strategy should be modeled across the hold period, not judged only by first-year tax impact.

What does Florida change about tax planning for high-income owners?

Florida changes the emphasis more than the need. The absence of state personal income tax can simplify one layer of planning, but it does not remove federal ordinary income tax, payroll tax, capital gains, NIIT, depreciation recapture, or business-level tax considerations. For many Florida owners, the planning conversation becomes more concentrated around federal strategy, entity structure, cash flow, and exit readiness. We also look at whether services, employees, sales, or investments create obligations beyond a simple Florida-only footprint.

What should be coordinated before a business sale or partner change?

Before a sale or partner change, the tax review should not wait for final documents. Entity structure, basis, compensation, distributions, debt, depreciation, installment possibilities, allocation issues, and advisor roles can all affect the outcome. The earlier review is not only about reducing tax. It is about avoiding terms that create unnecessary friction later. We want the attorney, tax advisor, financial advisor, and owner looking at the same transaction logic before the structure becomes difficult to unwind.

How does tax planning help when I already have multiple advisors?

Multiple advisors can be valuable, but fragmentation is a common risk. One advisor may focus on legal documents, another on investment management, another on lending, and another on tax filing. Each recommendation may make sense inside its own lane while creating conflict in the full picture. Tax planning helps connect those decisions across the business calendar, tax-year calendar, and asset lifecycle calendar. We are looking for coordination points: where income timing, liquidity, documentation, entity structure, and exit planning need to be reviewed together.

What makes a tax planning recommendation worth acting on?

A useful recommendation should explain both the benefit and the trade-off. For sophisticated owners, the question is not simply whether a strategy reduces current-year tax. It is whether the move fits cash flow, documentation, entity structure, financing needs, real estate plans, retirement goals, and possible exit events. A recommendation worth acting on should also be sequenced. It should clarify what needs to happen first, what depends on another decision, and what future consequence should be monitored.