Signs Your Accountant Is Reacting Too Late

If your accountant starts “planning” after the year is over, the issue is not just slow communication. It usually means the planning window has already narrowed.

That does not automatically make the accountant careless or unqualified. Many accountants are excellent at compliance. They prepare accurate returns, meet deadlines, answer questions, and keep the record clean.

But high-income taxpayers often need a different level of work.

For a Florida business owner, real estate investor, professional, or family paying six figures in federal tax, the central question is not, “Was my return filed correctly?” It is, “Were the tax-sensitive decisions shaped before they became permanent?”

A reactive accountant records what happened. A strategic tax advisor helps decide what should happen, when it should happen, how it should be documented, and how today’s move affects the next several years.

Key takeaway: The clearest sign your accountant is reacting too late is that they are explaining tax consequences after you have already made the decision. A proactive planning relationship should give you three things before that point: a current-year projection, a multi-year tax map, and a clear review process before major transactions, entity changes, compensation decisions, or real estate moves.

The most valuable tax planning often happens before the return preparation process begins.

“The issue is rarely whether a tax return can be prepared correctly. The larger question is whether the decisions behind that return were reviewed while there was still room to shape them.”

We help evaluate whether your current tax process is built for multi-year decisions, not just annual filing.

Signs Your Accountant Is Reacting Too Late: A Quick Diagnostic

Use this as a practical test. One warning sign may be a communication issue. A pattern usually means your tax function is built around annual compliance instead of forward-looking planning.

When a Tax Process May Be Too Reactive

These warning signs help business owners and real estate investors identify when tax work is centered on filing the return instead of coordinating income, entities, real estate, liquidity, and future exits.

| Warning Sign | What It Usually Signals | What Better Planning Looks Like |

|---|---|---|

| You Only Hear From Your Accountant Near Filing Deadlines | The relationship is centered on return production. | Scheduled planning reviews before year-end and before major decisions. |

| Your Projection Is Mostly Based on Last Year’s Return | Current-year facts are not being modeled. | Rolling projections using actual income, estimated gains, K-1 activity, payroll, investment income, and real estate activity. |

| Real Estate Deductions Are Discussed Without an Exit Model | Depreciation is being treated as a one-year benefit. | Depreciation, basis, passive loss limits, debt, recapture exposure, and sale timing are reviewed together. |

| S Corporation Salary Is Reviewed After Payroll Closes | Compensation planning is happening after the easiest correction window. | Owner compensation, distributions, retirement plan funding, and payroll timing are reviewed before year-end. |

| Estimated Tax Surprises Are Treated as Normal | Cash flow and federal tax timing are being managed after the fact. | Quarterly projections that account for business income, capital gains, NIIT exposure, withholding, and estimated payments. |

| Entity Structure Has Not Been Revisited in Years | The structure may no longer match income, ownership, liability, or exit goals. | Entity review as income, assets, partners, payroll, and transaction plans change. |

| Your Accountant Asks for Documents but Not Your Goals | They are preparing the return, not designing the plan. | Questions about acquisitions, sale plans, liquidity needs, charitable intent, family transfers, debt, and hold periods. |

| Strategies Appear in December With Little Time to Execute | The plan may be rushed or poorly documented. | Strategy selection early enough to implement, fund, document, and coordinate. |

| Your Advisors Do Not Speak to Each Other | Tax, legal, investment, lending, and estate decisions are fragmented. | A coordinated process among the CPA, attorney, wealth advisor, lender, and internal finance team. |

| No One Has Shown You a Multi-Year Tax Map | Each year is being optimized in isolation. | A written model showing expected income, deductions, gains, entity decisions, liquidity events, and exit-year pressure. |

The goal is not to catch your accountant doing something wrong. The goal is to see whether the relationship is built for the level of complexity you now have.

For sophisticated taxpayers, the danger is rarely one missed deduction. The bigger danger is making a good business or investment decision without seeing its tax consequences early enough to adjust the structure, timing, or documentation.

We review the decisions that may still be shaped before the filing window narrows.

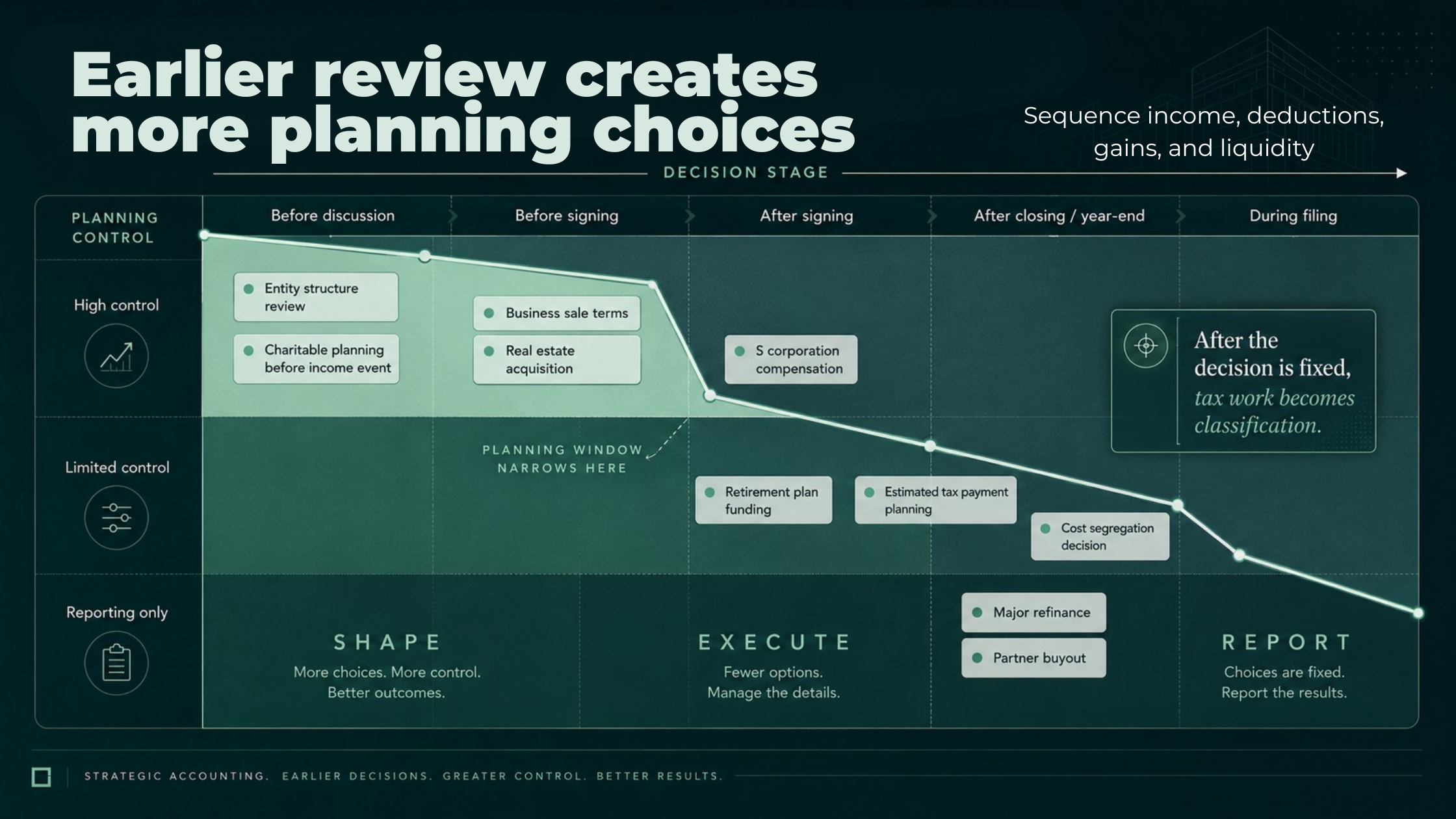

The Real Problem Is Not Late Filing. It Is Late Decision-Making.

Tax returns are backward-looking. Tax planning is forward-looking.

That distinction matters because many tax outcomes are set before a return is prepared. Once a sale closes, payroll year ends, a property is refinanced, a partner is bought out, equity is issued, or an entity election deadline passes, the accountant may have fewer meaningful options.

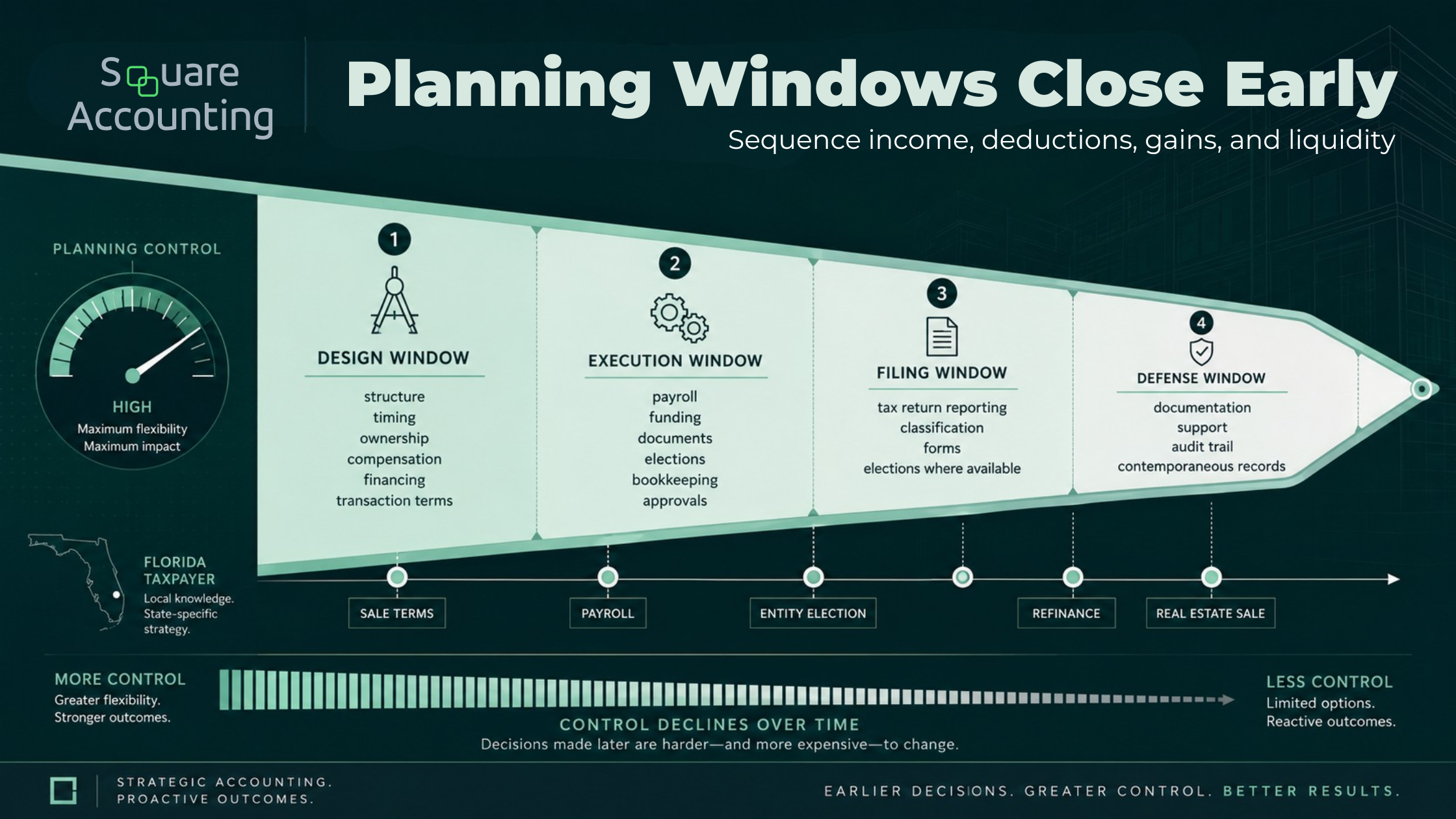

A better planning process works through four windows.

The design window is when you still control structure, timing, ownership, compensation, financing, and transaction terms.

The execution window is when the plan has to be implemented correctly. This may involve payroll, retirement plan funding, entity documents, appraisals, elections, bookkeeping, minutes, operating agreements, or closing documents.

The filing window is when the return reports the strategy. This is not where most strategic value is created.

The defense window is when documentation matters. If the facts were not created and preserved when the transaction happened, the return position may be harder to support later.

A reactive accountant spends most of their time in the filing window. A strategic tax advisor spends meaningful time in the design and execution windows.

This is why “send us your documents in February” is not enough for complex taxpayers. By February, the facts often exist. The advisor is no longer shaping them. They are classifying them.

A proactive advisor helps shape facts before they become fixed reporting items.

“This is where many high-income taxpayers misjudge the risk. By the time a transaction is ready to report, the best planning choices may already be unavailable.”

We look at projected income, gains, deductions, and timing before major decisions become fixed.

Why This Matters More Once Your Income Crosses a Certain Level

Once income rises into the mid-six figures and beyond, tax drag compounds. A missed planning opportunity is rarely limited to one line on one return.

The same decision can affect ordinary income tax, payroll tax, self-employment tax, qualified business income planning, passive activity limitations, NIIT exposure, depreciation timing, capital gain recognition, charitable deduction value, estate planning, and cash available for reinvestment.

The federal system also expects taxpayers to manage tax during the year, not only when the return is filed. The IRS explains that individuals, including sole proprietors, partners, and S corporation shareholders, generally use Form 1040-ES to figure estimated tax, and that expected adjusted gross income, taxable income, taxes, deductions, and credits should be considered.

For investors and business owners, the Net Investment Income Tax can add another layer. The NIIT applies at 3.8% to certain net investment income for individuals, estates, and trusts above statutory threshold amounts.

That is why “we will clean it up at tax time” is not a serious planning philosophy for high-income taxpayers. Sometimes it means the most valuable planning choices were never put on the table.

The Florida Factor: Tax-Friendly Does Not Mean Tax-Optimized

Florida’s lack of personal income tax is a real advantage. The Florida Department of Revenue states that Florida does not impose a personal income tax, while noting that businesses may still have filing requirements.

But tax-friendly does not mean tax-optimized.

For many Florida business owners and real estate investors, the largest exposure is still federal. A Florida resident selling appreciated real estate, operating a profitable S corporation, receiving large K-1 income, exiting a business, or holding passive investments can still face a significant federal tax bill.

The Florida planning issue is often psychological. Because there is no state personal income tax return, taxpayers may assume the planning environment is simpler than it is. In reality, the federal issues can still be layered: entity structure, payroll, NIIT, depreciation, passive losses, debt, gain recognition, estate strategy, and transaction timing.

For Florida real estate investors, the question is not only whether Florida is favorable. It is whether the federal real estate plan is coordinated across depreciation, debt, basis, passive activity status, hold period, and exit.

For Florida service business owners, the key question is whether the business structure still fits the income level, payroll model, owner compensation, retirement plan design, and eventual sale or succession plan.

Where Reactive Accounting Usually Costs the Most

Reactive accounting is most expensive where the tax result depends on facts that had to be shaped in advance.

That is why the following areas deserve more than filing-season attention.

1. Business owners with rising income

A business that has grown from profitable to highly profitable needs a different tax process.

Early accounting often focuses on bookkeeping accuracy, entity setup, payroll compliance, and return deadlines. That is appropriate at the beginning. But as income rises, the work should expand into owner compensation, retirement plan design, entity review, distribution policy, cash-flow forecasting, and multi-year income planning.

A common failure mode is leaving the original structure in place too long.

The entity that was adequate when profits were modest may no longer fit when the business has higher margins, more employees, multiple owners, or a realistic sale path. The structure may still be legally valid and still produce a poor tax result.

This is especially true for service-based businesses where much of the value is tied to owner labor, staff leverage, client contracts, recurring revenue, or goodwill. Tax planning needs to reflect how income is earned today and how value may be transferred later.

A reactive accountant may say, “The entity is already set up.” A strategic advisor asks, “Does the entity still match the business you have now and the exit you may want later?”

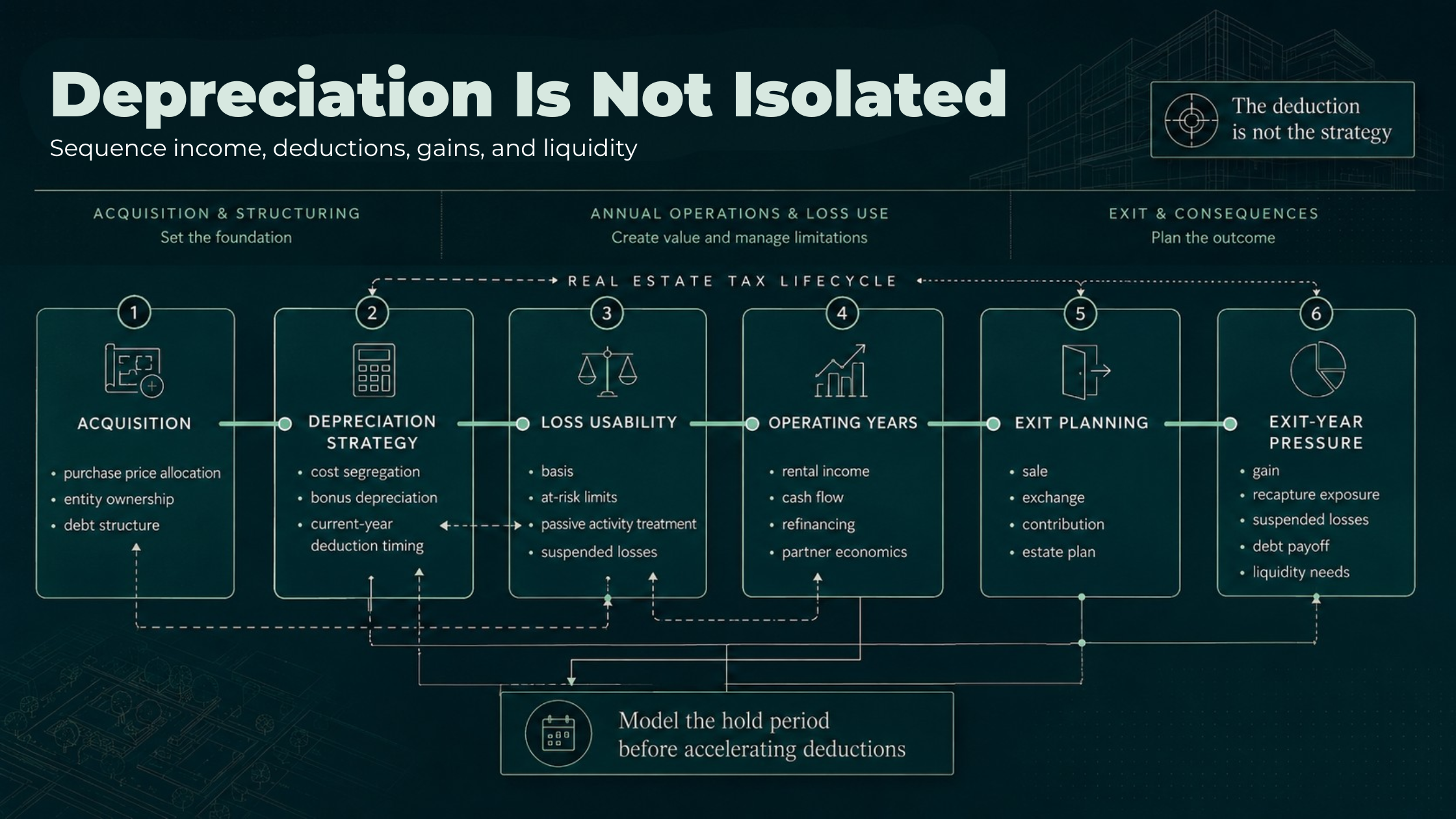

2. Real estate investors using depreciation without a long-term model

Real estate tax planning is where reactive advice can look useful in year one and still create problems later.

Cost segregation, bonus depreciation, and accelerated deductions can be valuable when used correctly. Current IRS guidance states that the One Big Beautiful Bill provides a permanent 100% additional first-year depreciation deduction for qualified property acquired, or specified plants planted or grafted, after January 19, 2025.

But the deduction itself is not the strategy.

The strategy is deciding when accelerated depreciation helps, whether the taxpayer can use the losses, how passive activity rules apply, what happens to basis, and how the plan behaves if the property is refinanced, contributed, exchanged, or sold.

A weak plan asks, “How much can we deduct this year?”

A stronger plan asks:

Will the deduction offset income at a high marginal value, or will it become suspended?

Are basis and at-risk limits being considered before passive activity limits?

Will this deduction create a better lifetime result, or only a better April result?

What happens if the property sells earlier than expected?

How does the plan interact with partner economics, debt, refinancing, or a future 1031 exchange?

What is the expected exit-year pressure from gain, recapture, suspended losses, and liquidity needs?

Real estate deductions should be modeled against the full investment lifecycle, not just the current tax year.

“The strongest real estate tax plans connect the current deduction to the future exit. A deduction that looks attractive in isolation may have a different value once suspended losses, debt, recapture exposure, and timing are modeled together.”

The passive activity and at-risk rules are central to this analysis. IRS Publication 925 explains that those rules can limit deductible losses from trade, business, rental, or other income-producing activities, and that at-risk rules are applied before passive activity rules.

If your accountant discusses depreciation without discussing classification, basis, at-risk limits, passive activity treatment, debt, and exit consequences, they may be reacting too late or too narrowly.

3. Liquidity events that are discussed after terms are set

The most expensive tax planning mistake is often calling the tax advisor after the letter of intent, purchase agreement, or sale structure is mostly decided.

That applies to selling a business, selling appreciated real estate, redeeming a partner, restructuring ownership, selling equity to a key employee, receiving earnout payments, converting debt or equity interests, or selling a professional practice.

Once the economics are negotiated, tax planning becomes more constrained.

A sale may require early analysis of asset sale versus equity sale treatment, purchase price allocation, installment treatment, rollover equity, employment or consulting agreements, escrow provisions, state sourcing, charitable planning, estate planning, and timing of other gains or deductions.

None of those decisions should be reviewed for the first time after the closing statement arrives.

The best planning often happens before the buyer or lender controls the timeline. That is when the owner still has room to evaluate structure, negotiate terms, coordinate charitable or estate planning, and avoid stacking a major gain on top of other income that could have been planned differently.

4. Estimated taxes that do not reflect the actual year

High-income taxpayers often normalize large April balances. Sometimes that is intentional. Often it is a sign that no one is actively managing current-year exposure.

For a business owner or investor, a meaningful projection should not simply annualize last year’s return. It should include current operating results, K-1 income, distributions, capital gains, rental activity, asset purchases, debt changes, charitable plans, retirement contributions, withholding, and expected estimated payments.

The IRS states that taxpayers figuring estimated tax should consider expected adjusted gross income, taxable income, taxes, deductions, and credits for the year.

A good projection answers three questions:

What are we likely to owe?

What can still be changed?

What should we avoid because it creates a worse result later?

That third question is the one weaker planning often misses.

A rushed year-end purchase, premature distribution, poorly timed bonus, or unmodeled capital gain can solve one problem while creating another. Estimated tax planning should not only prevent penalties or cash-flow surprises. It should help decide which moves are worth making while there is still time to act.

5. Interest expense, debt, and real estate financing

Debt decisions are often made for business reasons, not tax reasons. That is appropriate. But the tax consequences still need to be modeled.

For business owners and real estate investors, interest expense can affect cash flow, basis, at-risk amounts, distributable cash, investment returns, and deduction timing.

The federal business interest limitation under Section 163(j) can also affect the amount of deductible business interest expense for taxpayers to whom it applies. IRS instructions for Form 8990 describe the limitation by reference to business interest income, an applicable percentage of adjusted taxable income, and floor plan financing interest, with disallowed business interest potentially carried forward.

A reactive accountant reports the interest after the loan closes. A proactive advisor asks whether the financing structure supports the larger plan before documents are signed.

For real estate, that may include whether debt changes the ability to use losses, how refinancing proceeds fit into the ownership plan, whether an interest limitation may apply, and how leverage affects exit flexibility.

Debt can improve returns. It can also reduce planning flexibility if the tax model is built after the financing is already in place.

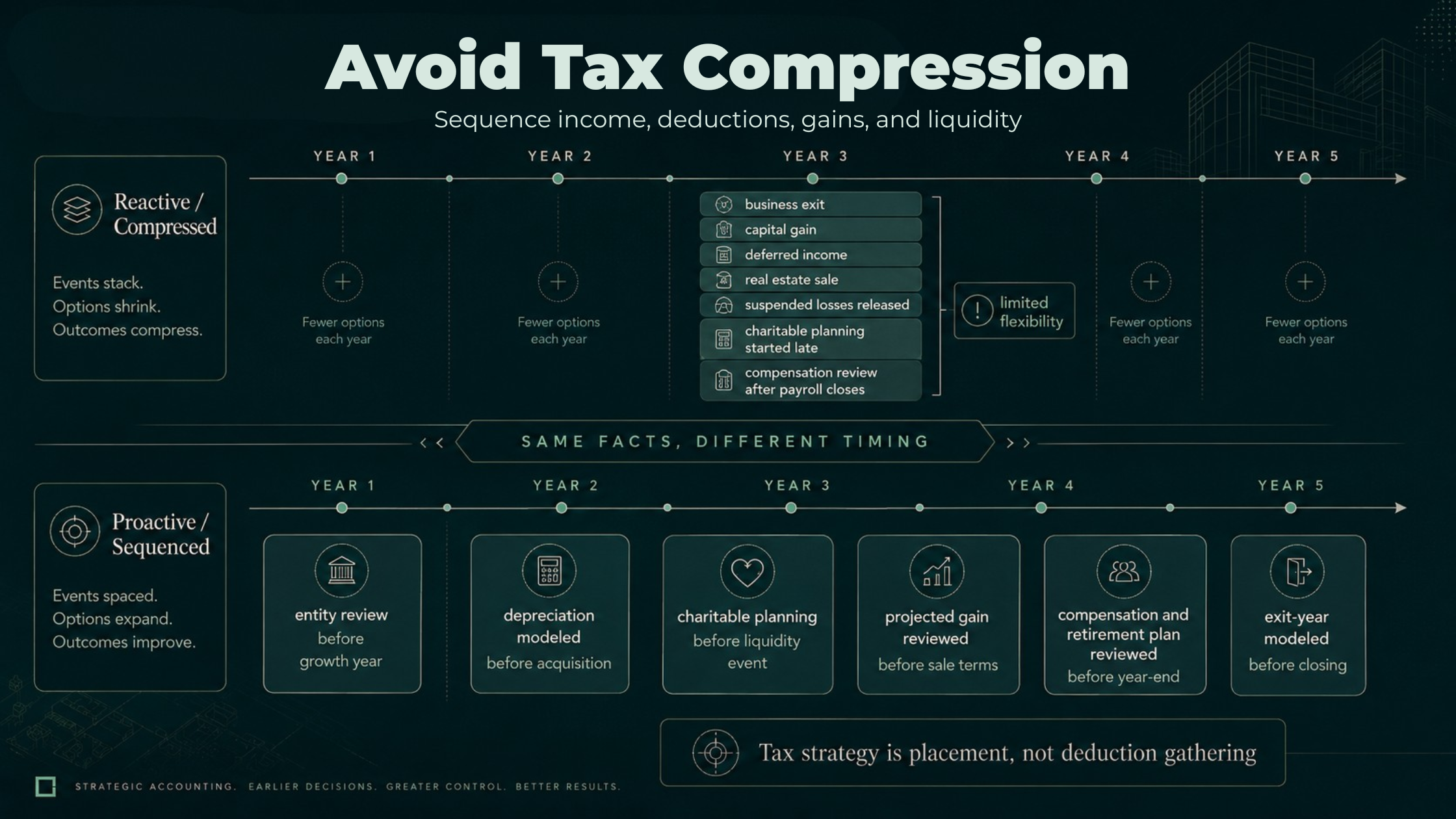

The Non-Obvious Failure Mode: Tax Compression

Most generic tax advice treats each year as separate.

Sophisticated taxpayers need to watch for tax compression.

Tax compression happens when income, gains, deductions, losses, ownership changes, and liquidity events are pushed into the wrong years or stacked into the same year without enough planning flexibility.

For example:

A real estate investor accelerates depreciation in a year when the loss cannot be used efficiently.

A business owner defers income into a year that later includes a major capital gain.

A taxpayer sells appreciated property before charitable planning or estate planning is coordinated.

An S corporation owner waits until December to review salary, retirement plan funding, and distributions.

A business exit closes in the same year as other large investment gains.

Suspended losses become available in a year when they offset lower-value income than expected.

A refinancing creates liquidity but narrows future restructuring options.

Tax compression occurs when valid decisions combine into a weaker lifetime tax result.

“The planning risk is not always visible in a single transaction. It appears when several reasonable decisions collide in the same tax year without a coordinated multi-year model.”

Each individual decision may be technically defensible. The combined timing may still produce a weaker lifetime result.

This is where real tax strategy differs from deduction gathering. The question is not, “Can we reduce this year’s tax bill?” The better question is, “Where should income, deductions, gains, losses, ownership, and liquidity sit across the next several years?”

A strategic advisor manages tax compression before it happens. A reactive accountant explains it after the return is already telling the story.

We review how today’s tax decisions may affect a future sale, refinance, exchange, or liquidity event.

Reactive Accountant vs. Strategic Tax Advisor

A diagnostic table tells you what to notice. This comparison tells you what kind of work product you should expect.

Reactive Accountant vs. Strategic Tax Advisor

The difference is not only technical skill. It is whether the tax process is centered on filing last year’s return or coordinating decisions before they shape the next return.

| Reactive Accountant | Strategic Tax Advisor |

|---|---|

| Focuses on filing the return. | Focuses on decisions before the return exists. |

| Reviews documents after year-end. | Reviews projected income and planned transactions during the year. |

| Answers isolated questions. | Builds a coordinated position across entities, assets, and years. |

| Looks mainly for deductions. | Weighs deductions against basis, passive limits, liquidity, recapture, and exit plans. |

| Works mostly from historical data. | Uses projections, scenarios, and decision triggers. |

| Treats tax as annual compliance. | Treats tax as a multi-year capital allocation issue. |

| Minimizes this year’s tax bill. | Evaluates after-tax outcomes over time. |

| Rarely coordinates with other advisors. | Integrates legal, investment, estate, lending, and transaction decisions. |

This distinction matters because many excellent CPAs are strong compliance professionals. They may not be structured, staffed, or engaged to provide advanced planning.

That does not always mean you need to replace your CPA. In many cases, the better solution is adding a higher-level advisory layer that coordinates with the existing preparer.

The key is making sure someone owns the future-facing tax strategy. If no one owns it, it usually does not happen.

Questions to Ask Before You Decide Your Accountant Is the Problem

Before making a change, ask direct questions. The answers will show whether the issue is expertise, role fit, communication, capacity, or simply the absence of a formal planning process.

Ask:

What tax decisions do I need to make before year-end?

What decisions should I involve you in before I sign anything?

What are the next three years likely to look like if nothing changes?

How will this year’s deductions affect a sale, refinance, exchange, or liquidity event?

Are any losses limited by basis, at-risk rules, passive activity rules, or other loss limitations?

How are we accounting for NIIT exposure?

Does my entity structure still match my income, assets, payroll, ownership, and exit goals?

What should my attorney, wealth advisor, lender, or internal finance team know before they act?

What strategies are we intentionally not using, and why?

The last question is important. Advanced planning is not about using every available strategy. It is about knowing which strategies fit the facts, which create bad trade-offs, and which should be avoided.

A strong advisor should be able to explain both the recommendation and the restraint behind it.

What a Proactive Multi-Year Tax Plan Should Include

A useful tax plan for a high-income business owner or real estate investor should not be a generic checklist. It should be a working model that changes as the facts change.

At minimum, it should include the following.

A current-year tax projection

This should be reviewed before year-end and updated when facts materially change. It should include business income, wages, K-1s, capital gains, rental activity, deductions, withholding, estimated payments, and known transaction activity.

The projection should not stop at the expected tax bill. It should identify what can still be changed and what decisions are no longer available.

A multi-year income map

This shows likely income by category over the next several years. Ordinary income, capital gain, rental income, business income, interest, dividends, retirement income, and liquidity event proceeds are not all planned the same way.

The map should also identify years where income may be unusually high or low. Those years often create planning opportunities, but only if they are visible early.

Entity and compensation review

For business owners, the plan should evaluate entity structure, owner salary, distributions, retirement plan options, fringe benefits, accountable plans, and future sale flexibility.

This review should happen before payroll and contribution windows close, not after the return is already being assembled.

Real estate activity analysis

For investors, the plan should address depreciation, grouping, passive activity status, material participation, at-risk amounts, debt, refinancing, basis, suspended losses, and expected hold period.

The analysis should also ask how today’s deductions affect tomorrow’s sale, exchange, refinance, or estate plan.

Exit-year modeling

Every major asset should be viewed through a future exit lens. That includes business equity, rental property, partnership interests, and concentrated investment positions.

Exit-year modeling should account for timing, character, liquidity, installment possibilities, suspended losses, debt payoff, transaction costs, charitable planning, estate planning, and the interaction with other income in the same year.

Advisor coordination

Tax planning often fails when each advisor solves only their piece.

The attorney drafts. The lender finances. The wealth advisor invests. The CPA files. The business owner signs.

A proactive tax plan identifies where those decisions collide before they collide.

Documentation standards

Many tax positions depend on facts. Those facts are easier to document when they are fresh.

Documentation may include participation records, valuation support, board or member approvals, compensation support, loan documents, closing statements, grouping elections, appraisals, charitable substantiation, and contemporaneous business purpose.

Waiting until audit defense is needed is not a planning process.

We help align tax planning with entity structure, real estate activity, liquidity events, and advisor coordination.

When Popular Tax Advice Backfires

Some strategies are valuable in the right fact pattern and unhelpful in the wrong one.

Accelerated depreciation can be powerful, but not if the losses are unusable, the hold period is short, or the exit consequences are ignored.

An S corporation can improve payroll tax planning in the right circumstances, but not if reasonable compensation, payroll timing, retirement plan design, distributions, and basis are mishandled.

A C corporation may fit certain reinvestment or exit goals, but it can create double-tax issues if future distributions or sale structure are not modeled.

A 1031 exchange can defer gain, but it can also move a taxpayer into replacement property that does not match liquidity needs, debt tolerance, estate goals, or risk profile.

Charitable planning can be effective, but only if it is coordinated before the income event, with the right asset, timing, structure, and documentation.

Late advice tends to focus on whether a strategy is available. Better advice asks whether the strategy improves the total after-tax outcome.

That is the standard sophisticated taxpayers should expect.

The Best Time to Bring in Tax Strategy

The best time to bring in tax strategy is before a material decision, not after a tax bill.

You should involve a tax strategist before buying or selling real estate, signing a letter of intent, changing entity ownership, hiring or promoting key employees into ownership, refinancing major assets, making large equipment or improvement purchases, changing compensation, moving assets into trusts or family entities, selling a business, creating or terminating partnerships, making large charitable gifts, or taking unusually high income in one year.

For Florida business owners and investors, this is especially important because the state income tax environment can feel simple while the federal profile remains complex.

A practical rule works well: if a decision changes income, ownership, debt, asset basis, payroll, liquidity, or exit timing, it should be reviewed before it is signed.

Conclusion: The Clearest Sign Your Accountant Is Reacting Too Late

The clearest sign your accountant is reacting too late is simple: they are explaining tax consequences after you have already made the decision.

For high-income taxpayers, that is not enough.

You need a planning process that identifies tax-sensitive decisions before they harden, models the effect across multiple years, coordinates with your other advisors, and separates good strategy from short-term deduction chasing.

A strong tax return reports what happened. A strong tax plan helps shape what happens next.

We help Florida business owners and investors assess whether their tax planning is happening early enough.

Strategic Tax Planning FAQs

Key questions for high-income taxpayers, Florida business owners, and real estate investors evaluating whether their tax process is proactive, coordinated, and aligned with future decisions.

How can I tell whether my CPA is doing tax planning or only tax preparation?

Look at when the conversation happens and what the conversation covers. Tax preparation usually starts with document collection and ends with a filed return. Tax planning starts earlier, before income, payroll, real estate activity, financing, entity structure, or transaction terms become fixed. We would expect a planning process to include current-year projections, decision timing, multi-year modeling, and questions about goals, not just requests for forms. For high-income taxpayers, the issue is not whether the return is accurate. The issue is whether the major decisions were reviewed while there was still room to shape them.

What should a proactive accountant ask before year-end?

A proactive accountant should ask about decisions, not only documents. That includes expected income, K-1 activity, capital gains, real estate purchases or sales, compensation changes, large deductions, charitable plans, financing, ownership changes, and upcoming liquidity events. The better questions are forward-looking: what may happen before year-end, what decisions are still open, and what should be avoided because it creates a worse result later. For sophisticated taxpayers, year-end planning should not feel like a scramble. It should narrow priorities, confirm execution steps, and identify which planning windows are still available.

What does it mean to outgrow your accountant?

Outgrowing an accountant does not necessarily mean the accountant is doing poor work. It may mean your facts have become more complex than the service model was designed to handle. A business with rising income, multiple entities, real estate activity, K-1s, debt, payroll, and possible exit planning needs more than accurate annual filing. We usually look for signs that the relationship is still centered on compliance while the taxpayer now needs scenario modeling, advisor coordination, transaction review, and multi-year tax strategy. The mismatch is often about role, timing, and scope.

Why should real estate depreciation be reviewed before filing season?

Depreciation can affect more than the current-year tax bill. For real estate investors, the value of accelerated deductions depends on whether losses can be used, how passive activity rules apply, whether basis and at-risk limits matter, and what happens in a sale, refinance, exchange, or estate plan. If depreciation is reviewed only when the return is prepared, the advisor may be classifying facts rather than shaping the plan. We want the depreciation decision connected to hold period, debt, liquidity, suspended losses, and exit-year pressure before the reporting position is selected.

How do I know if my advisor team is too fragmented?

A fragmented advisor team usually shows up when each professional answers their own question without anyone modeling the combined result. The attorney drafts, the lender finances, the wealth advisor invests, and the CPA files, but no one connects the tax consequences across the full decision. Warning signs include last-minute tax review of signed documents, inconsistent assumptions between advisors, no shared view of upcoming transactions, and no multi-year map. We would expect proactive planning to identify where legal, tax, investment, lending, and estate decisions may collide before the taxpayer commits.

What makes a tax projection useful for a high-income taxpayer?

A useful projection does more than estimate what will be owed. It should show what is driving the liability, what can still be changed, and what decisions may create second-order problems. For high-income taxpayers, that means modeling current business income, wages, K-1s, gains, rental activity, deductions, withholding, estimated payments, and known transactions. It should also distinguish between a cash-flow issue and a strategy issue. A projection that simply updates the expected tax bill is helpful, but incomplete. The planning value comes from identifying remaining choices before they close.

When should a Florida business owner involve tax strategy before a transaction?

A Florida business owner should involve tax strategy before signing or materially committing to a transaction that changes income, ownership, debt, payroll, liquidity, asset basis, or exit timing. That includes business sales, partner buyouts, ownership changes, refinancing, key employee equity, major asset purchases, compensation changes, and charitable planning tied to a liquidity event. Florida’s lack of personal income tax can make the state environment feel simpler, but the federal tax profile may still be complex. We want tax review early enough to influence structure, timing, documentation, and advisor coordination.

What questions reveal whether tax advice is truly strategic?

Good questions force the conversation beyond filing status and deductions. Ask what decisions need to be made before year-end, what should be reviewed before anything is signed, how this year’s deductions affect a future sale or refinance, whether losses are limited, how NIIT exposure is being considered, and whether the entity structure still fits current income and exit goals. Also ask which strategies are being intentionally avoided and why. A strong answer should explain trade-offs, timing, documentation, and future consequences, not just the immediate tax effect.