Tax Preparation vs Tax Advisory: Why the Difference Matters

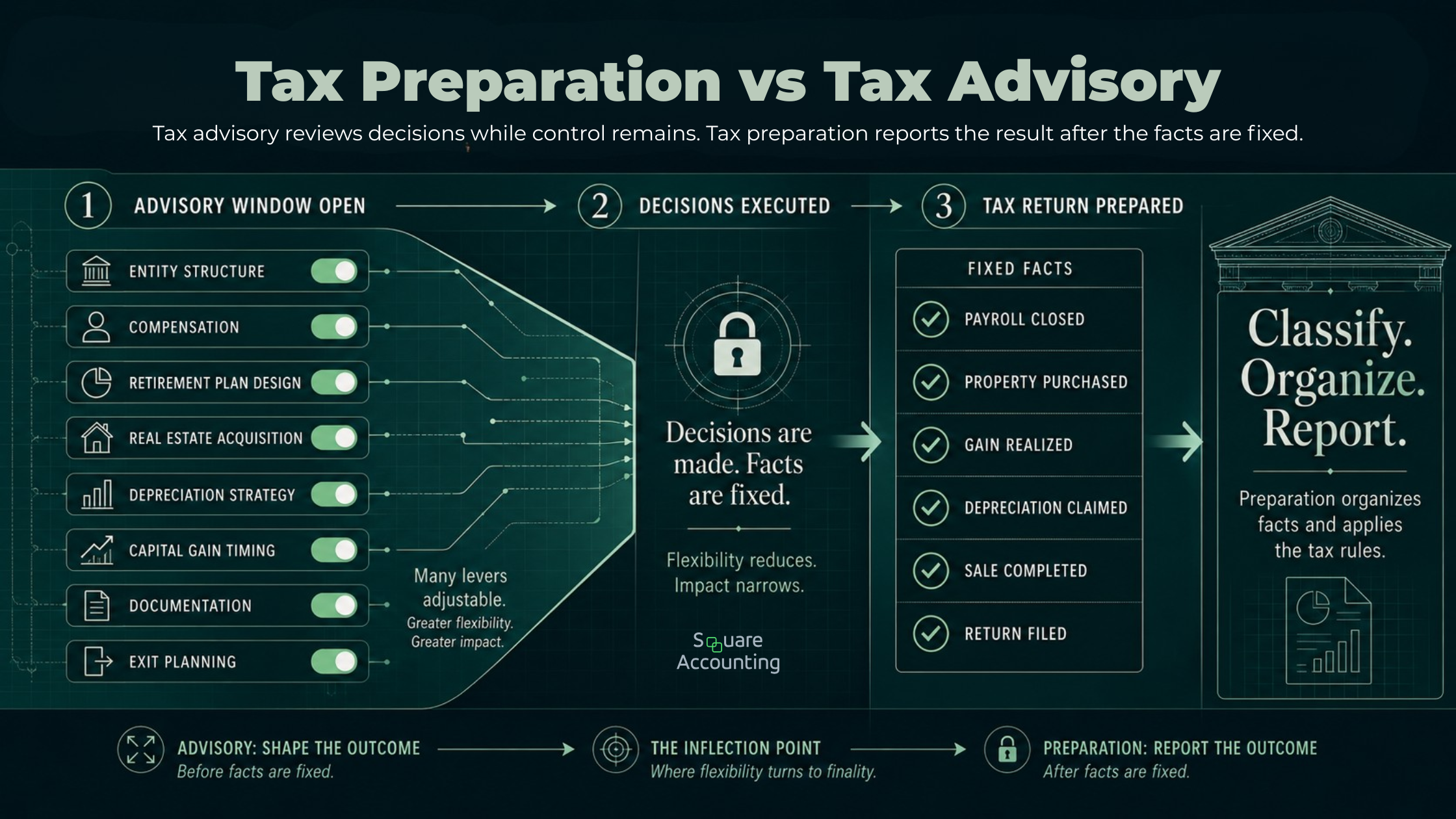

For high-income taxpayers, the difference between tax preparation and tax advisory is not just the timing of the work. It is the amount of control that remains over the tax result.

Tax preparation reports what already happened.

Tax advisory helps shape decisions before the tax result becomes fixed.

That distinction matters for Florida business owners, real estate investors, and high-income professionals because many meaningful tax outcomes are not created while the return is being prepared. They are created earlier, when there is still time to review ownership structure, compensation, real estate activity, financing, depreciation, retirement plan design, charitable planning, gain recognition, and exit timing.

A well-prepared tax return is still essential. But for taxpayers paying significant federal tax each year, accurate filing is the floor. It is not the full strategy.

Key takeaway: tax preparation is about compliance after the fact. Tax advisory is about coordinated decision-making before the fact. The stronger the taxpayer’s income, asset base, entity structure, and investment activity, the more expensive it can become to confuse one for the other.

The most important difference is timing: advisory helps shape decisions before the return simply reports them.

“A tax return can be accurate and still reflect decisions that were never reviewed early enough. The question is not whether preparation matters; the question is whether advisory entered the process while there was still room to shape the outcome.”

Tax Preparation vs Tax Advisory: The Practical Difference

The simplest way to compare tax preparation vs tax advisory is to ask one question:

Are we reporting decisions that already happened, or are we reviewing decisions while they can still be changed?

Tax Preparation vs. Tax Advisory

Tax preparation focuses on accurate reporting after the year closes. Tax advisory focuses on improving tax-sensitive decisions before the facts become fixed.

| Area | Tax Preparation | Tax Advisory |

|---|---|---|

| Primary Purpose | File accurate tax returns. | Improve tax-sensitive decisions before filing. |

| Timing | After the year closes. | Before and during the year. |

| Main Inputs | Tax documents and completed transactions. | Projected income, entities, investments, goals, liquidity, timing, and open decisions. |

| Core Question | “How do we report this correctly?” | “What should be reviewed before this becomes fixed?” |

| Typical Output | Filed returns, tax due or refund, required forms. | Planning model, recommendations, decision sequence, implementation priorities. |

| Best Use Case | Compliance and reporting. | Multi-year tax efficiency and decision support. |

| Main Risk If Missing | Errors, missed forms, penalties, incomplete documentation. | Missed planning windows, avoidable tax compression, weak structure, poor sequencing. |

Tax preparation is backward-looking by design. It gathers W-2s, 1099s, K-1s, brokerage statements, closing statements, payroll records, depreciation schedules, charitable receipts, and business financials. The work is necessary because the taxpayer needs accurate returns and defensible reporting.

Tax advisory is different. It looks at what may happen next and asks whether the tax result can still be shaped. That may include income projections, entity review, compensation planning, basis analysis, passive loss review, depreciation modeling, estimated tax planning, sale timing, or coordination with estate and investment advisors.

The distinction is not that preparation is basic and advisory is advanced. The distinction is that they solve different problems.

Preparation solves a reporting problem.

Advisory solves a decision problem.

We review whether tax-sensitive decisions are being addressed while there is still room to shape structure, timing, and documentation.

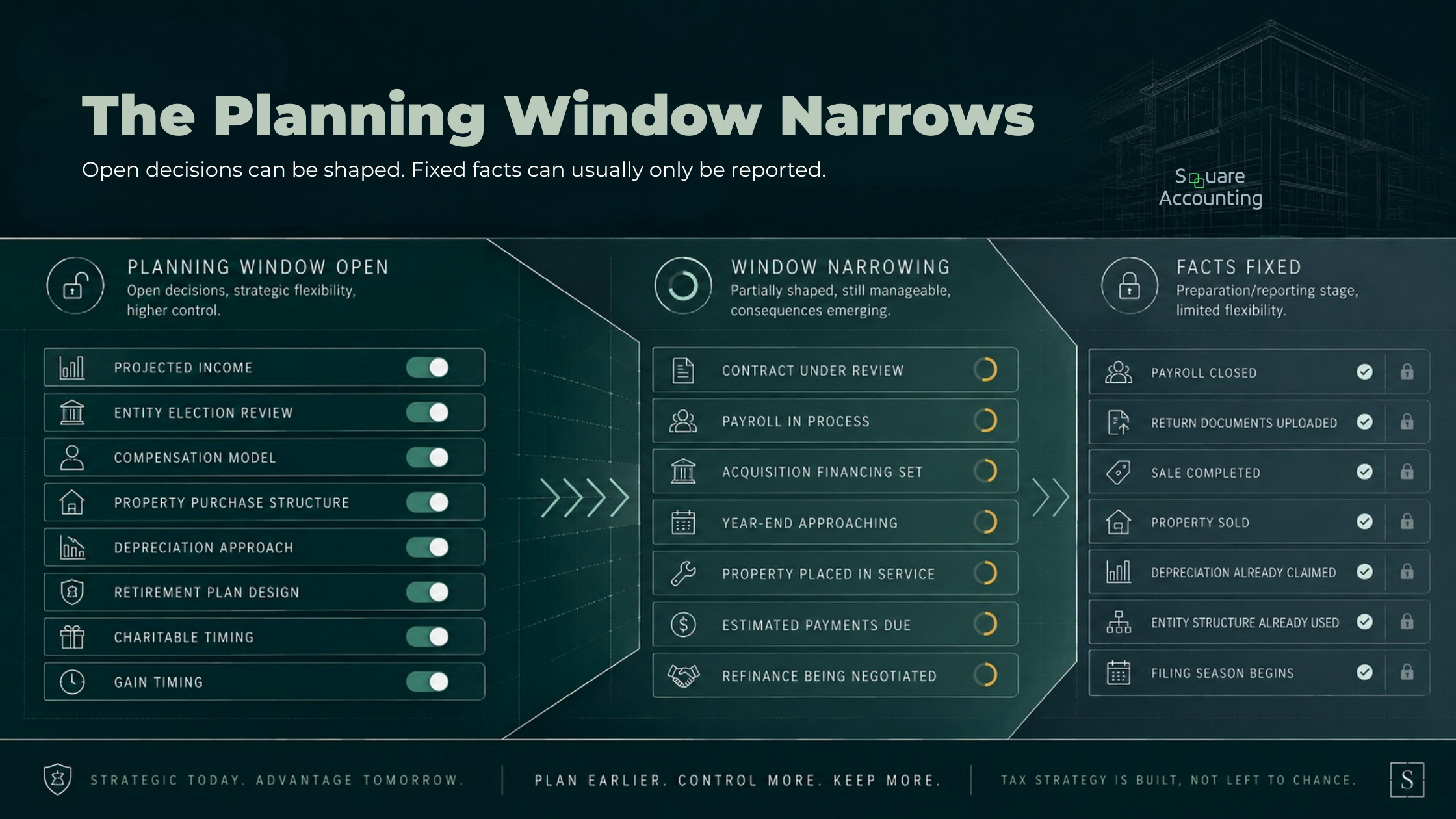

Why Preparation Alone Often Feels Reactive

Many high-income taxpayers do not have a tax preparation problem. They have a timing problem.

Their return may be accurate. Their documents may be organized. Their CPA may be technically competent. But the conversation begins after the most important decisions have already been made.

By filing season, the business already paid payroll. The property already closed. The entity election deadline may have passed. The capital gain already occurred. The charitable gift may have been made without coordination. The equipment may have been purchased without modeling income, basis, or business use. The rental loss may exist on paper but may not be currently usable. The sale may have been negotiated without reviewing installment treatment, depreciation recapture, suspended losses, or future liquidity needs.

That is why sophisticated taxpayers often feel disappointed even when the return is prepared correctly.

The problem is not always the quality of the filing. The problem is that the preparer was asked to create strategy after the planning window had already narrowed.

Preparation can classify, calculate, document, and file. It usually cannot rewrite a closed transaction.

Preparation can report completed activity, but advisory creates more value when tax-sensitive decisions are reviewed before they harden into facts.

“This is where many high-income taxpayers feel the gap between accurate filing and strategic planning. The earlier a decision is reviewed, the more options remain for structure, timing, documentation, and coordination.”

We help identify where preparation may be handling issues that should be reviewed earlier through advisory planning.

The Return Is the Evidence, Not the Strategy

A tax return is not just a form. It is a record of prior decisions.

For a business owner, the return reflects entity structure, owner compensation, distributions, retirement plan design, payroll timing, expense classification, accountable plan documentation, owner benefits, and capital investments.

For a real estate investor, the return reflects acquisition structure, debt placement, depreciation choices, passive activity treatment, grouping decisions, basis, at-risk exposure, repairs versus improvements, and sale timing.

For a high-income professional, the return reflects compensation structure, equity events, investment income, charitable planning, retirement contributions, residency, and liquidity decisions.

The return matters because those facts must be reported correctly. But advisory matters because the facts themselves often determine whether the taxpayer has options.

A return can show the tax result. It rarely explains whether the result was the best available result.

What Tax Advisory Actually Includes

Tax advisory is not simply a longer tax meeting or a year-end checklist. For sophisticated taxpayers, meaningful advisory work has to connect projections, structure, timing, documentation, and implementation.

The purpose is not to chase every possible deduction. The purpose is to decide which tax moves fit the taxpayer’s facts, risk tolerance, cash flow, and long-term plan.

Current-Year Projection

A current-year projection estimates where the taxpayer is likely to land before the year is over.

For a Florida business owner, that may include wages, S corporation income, distributions, payroll, retirement contributions, equipment purchases, estimated tax payments, and expected cash flow.

For a real estate investor, it may include rental income, operating expenses, depreciation, passive losses, short-term rental activity, K-1s, refinance activity, and expected sales.

For a high-income professional, it may include bonus income, equity compensation, investment gains, charitable gifts, retirement contributions, and estimated tax payments.

The point is not only to avoid a surprise balance due. The point is to identify which decisions are still open.

A projection that arrives after December may explain the problem. A projection prepared early enough may help change the outcome.

Multi-Year Modeling

A single-year tax reduction is not always the best tax result.

Accelerated depreciation may reduce current income but increase gain or recapture pressure later. A lower S corporation salary may reduce payroll tax but weaken retirement plan contributions or create reasonable compensation concerns. A Roth conversion may increase current tax but improve future flexibility. A large charitable gift may be more valuable in one year than another depending on income, gains, and liquidity.

Tax advisory should model the current year in context.

That means asking:

Will this deduction be usable this year?

Does it create a future tax cost?

Does it improve cash flow or only shift tax into another year?

What happens if income rises, falls, or compresses into an exit year?

Does the strategy still work if the taxpayer sells, refinances, hires employees, or changes residency?

High-income taxpayers often lose tax efficiency when each year is planned in isolation. Advisory should connect the years.

Entity and Ownership Review

Entity structure is not a one-time decision. It should be revisited as the taxpayer’s business, assets, family, and exit goals evolve.

A Florida service business may start as a simple LLC, later elect S corporation treatment, add employees, acquire real estate, create related entities, bring in family members, or prepare for a sale. Each step can affect payroll, owner compensation, distributions, basis, retirement planning, liability separation, succession, and transaction structure.

The preparation question is, “Which return do we file?”

The advisory question is, “Does this structure still fit what the taxpayer is trying to do next?”

That is a more important question for a growing business than for a static one.

Real Estate Activity and Loss Review

Real estate is one of the clearest areas where preparation and advisory diverge.

A preparer can report rental income, expenses, depreciation, and passive losses. An advisor reviews whether the structure and documentation support the intended tax treatment.

A large real estate loss may look valuable, but the actual benefit depends on basis, at-risk exposure, passive activity treatment, material participation, grouping, and the taxpayer’s other income. The order matters. A loss can be mathematically real and still be limited.

For a Florida real estate investor, the better question is not only, “Can we depreciate this property?”

The better question is:

Will this depreciation or loss produce usable current tax value, and what does it do to the exit?

That question forces the analysis to move beyond the first-year deduction.

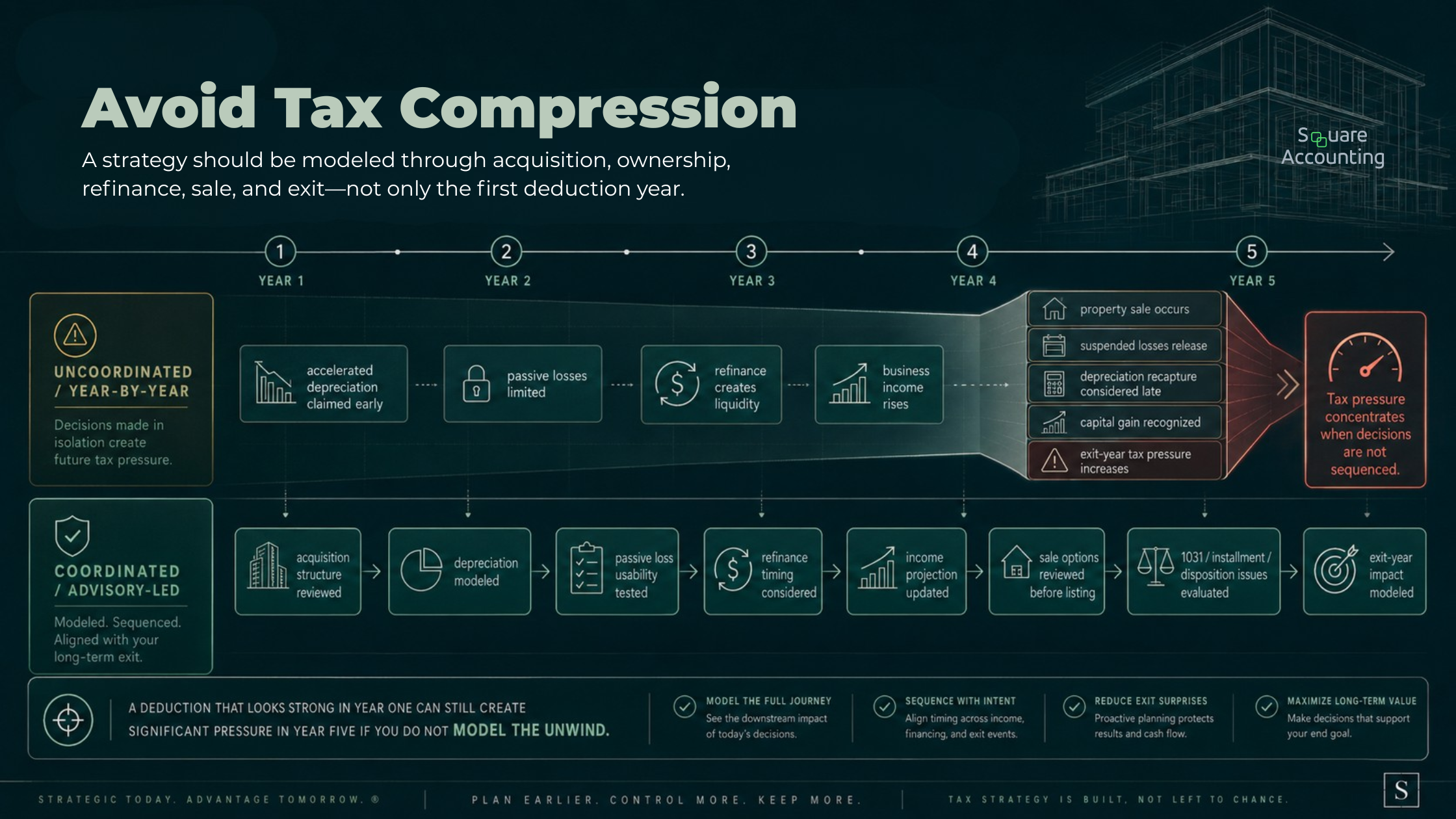

Exit and Recapture Planning

Many taxpayers focus on deductions during ownership and wait too long to model the exit.

That is a costly sequencing mistake.

Depreciation may improve current cash flow, but it can also affect gain recognition when the property is sold. A refinance may improve liquidity, but it can also change risk, basis planning, and future flexibility. A 1031 exchange may defer gain, but it must be considered before the sale process is too far along. Suspended passive losses may become relevant at disposition, but the timing and structure of the sale matter.

For a real estate investor, advisory should connect:

acquisition structure

debt placement

cost segregation

bonus depreciation where available

passive activity limitations

basis and at-risk exposure

refinance plans

sale timing

suspended losses

estate and succession goals

A current-year deduction may improve cash flow, but the stronger analysis follows the strategy through the eventual sale or unwind.

“Real estate strategy should not stop once the acquisition-year deduction is calculated. The more useful question is whether the strategy still works when income rises, passive losses accumulate, debt changes, and the property is eventually sold.”

The point is not that depreciation, exchanges, or entity planning are good or bad in isolation. The point is that each decision changes the next decision.

A strategy that looks strong in year one may create pressure in the exit year if no one modeled the unwind.

We review projected income, open decisions, and timing issues before the tax result becomes harder to shape.

The Florida Context: Why Advisory Still Matters Without State Income Tax

Florida’s lack of individual income tax can make planning feel simpler, but it does not make planning optional.

Florida residents can still face federal income tax, payroll tax, self-employment tax, capital gains tax, net investment income tax exposure, depreciation recapture, passive loss limitations, estate and gift planning considerations, and multi-state filing issues when income crosses state lines.

Florida business owners may also have entity-level, payroll, sales tax, or multi-state considerations depending on how the business operates. A Florida resident who owns rental property, operates in another state, hires remote employees, receives K-1 income, or sells appreciated assets may still need coordinated tax planning.

For many Florida high-income taxpayers, the largest planning layer is federal. That makes timing even more important.

The advisory work often centers on:

business structure and compensation

S corporation salary and distribution planning

retirement plan design

real estate depreciation and passive loss strategy

capital gain timing

charitable planning

installment sale and exit modeling

multi-state income exposure

estate and ownership alignment

documentation that supports tax positions

Florida may reduce one layer of state income tax planning. It does not remove the need to coordinate the federal result.

We help Florida business owners and investors connect federal tax planning with entity, real estate, income, and multi-state considerations.

Where Tax Preparation Ends and Advisory Begins

Tax preparation answers:

“How do we report this correctly?”

Tax advisory asks:

“Should this have been structured differently before we got here?”

That difference becomes clearer when applied to specific planning areas.

Compensation

A preparer reports wages, distributions, guaranteed payments, or self-employment income based on the records.

An advisor reviews whether compensation is aligned with entity structure, payroll taxes, retirement plan goals, owner cash flow, lending needs, and reasonable compensation expectations.

For an S corporation owner, the issue is not simply whether salary should be high or low. Too little salary can create risk. Too much salary may reduce available distributions or limit flexibility. The right answer depends on profit level, role, industry, payroll history, retirement goals, and documentation.

Preparation reports the compensation.

Advisory evaluates the compensation before payroll closes.

Retirement Plans

A preparer reports retirement contributions that were made.

An advisor evaluates which retirement plan design fits the owner’s income, age, employee base, cash flow, administrative tolerance, and long-term tax goals.

A high-income owner with consistent profits may need more than a default retirement account. But a more advanced plan may create funding commitments, employee coverage issues, or cash flow constraints.

The advisory question is not, “Can we deduct a contribution?”

The advisory question is, “Which plan design fits the business and the owner’s future income pattern?”

Real Estate Depreciation

A preparer reports depreciation based on records and schedules.

An advisor evaluates whether cost segregation, bonus depreciation where available, repair classifications, capitalization decisions, and disposition planning fit the investor’s broader tax picture.

A depreciation study may create a large deduction. That does not automatically mean the deduction is currently usable. Passive loss limits, basis, at-risk rules, and material participation can change the result.

The deeper question is whether depreciation creates durable tax efficiency or simply shifts pressure into a later year.

Capital Gains

A preparer reports the sale.

An advisor reviews sale timing, payment structure, installment treatment, charitable planning, 1031 exchange options, basis, suspended losses, depreciation recapture, net investment income tax exposure, and cash needs before closing.

Once the agreement is signed and the closing occurs, flexibility may be limited.

That is why gain planning belongs before the transaction, not after the closing statement arrives.

Documentation

A preparer requests documents to support the return.

An advisor helps identify what documentation should exist before the return is prepared.

That distinction matters. Business purpose, mileage, material participation, short-term rental records, accountable plan reimbursements, shareholder basis, loans, improvements, and related-party arrangements are easier to support when documentation is built during the year.

After-the-fact reconstruction may be possible in some cases, but it is rarely the strongest process.

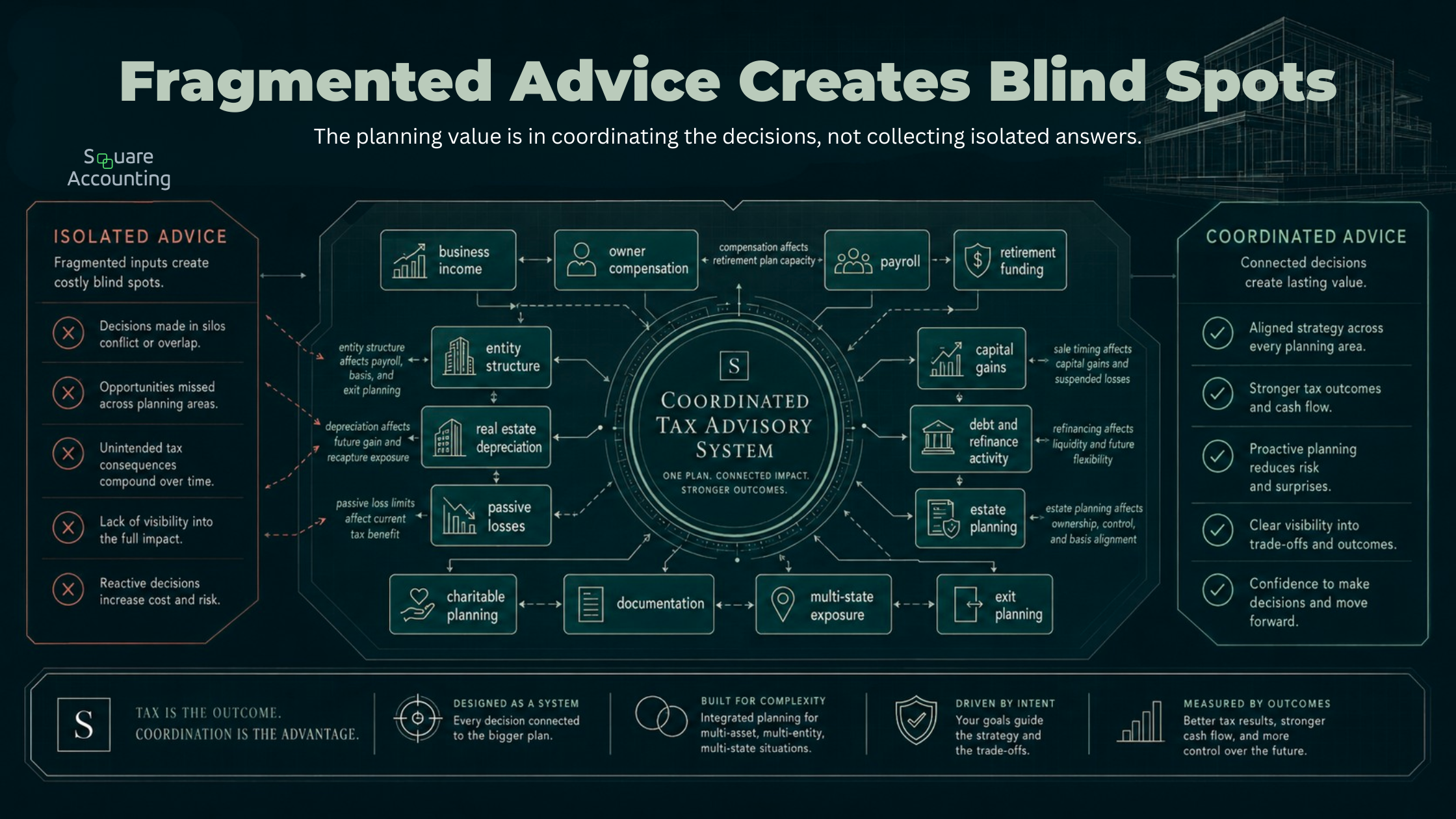

The Advisory Failure Mode Sophisticated Taxpayers Miss

Many taxpayers think the problem is that their CPA did not find enough deductions.

Often, the deeper problem is that no one is coordinating the tax consequences across years.

A business owner may have a strong retirement plan but weak entity structure.

A real estate investor may have strong depreciation planning but no exit model.

A high-income professional may have strong investment management but no tax coordination around equity compensation, charitable giving, or real estate losses.

A family may have estate documents, but the ownership structure may not align with basis planning, control, succession, or liquidity goals.

The failure mode is fragmented advice.

Each advisor may be competent within their lane, but no one may be modeling how the pieces interact:

business income

payroll

retirement funding

depreciation

passive losses

capital gains

debt

estate planning

charitable planning

entity structure

liquidity events

multi-state exposure

Sophisticated taxpayers may receive strong advice in separate areas, but weak results when no one models how those decisions interact.

“This is the advisory gap sophisticated taxpayers often miss. The issue is rarely one missing tactic; it is the absence of a coordinated planning system that tests how each decision changes the next.”

This is where advisory should add value. It should not merely answer isolated tax questions. It should help determine whether the answers work together.

Why Year-End Planning Is Often Too Late

Year-end planning is useful. It is not a substitute for full-year advisory.

By November or December, some decisions may still be available: estimated payments, charitable planning, retirement contributions, certain payroll adjustments, gain and loss harvesting, equipment purchases, and some timing decisions.

But other decisions may already be fixed:

entity formation

ownership percentages

loan structure

acquisition terms

closing dates

payroll history

real estate use

material participation records

documentation of business purpose

sale agreements

capital improvements

related-party arrangements

For high-income taxpayers, the best planning often happens before the visible tax event.

Before the property is purchased.

Before the business changes compensation.

Before the contract is signed.

Before the exit is negotiated.

Before the year becomes too compressed.

Year-end planning can still matter. But advisory should not wait until year-end to begin.

How to Know Whether You Are Receiving Advisory or Only Preparation

A taxpayer can have a CPA and still not have an advisory relationship.

The clearest sign is timing.

The relationship is likely preparation-focused if:

most communication begins after tax documents are available

the main annual question is whether all forms have been uploaded

there is little discussion of projected income before year-end

real estate purchases are reviewed only after closing

entity structure is rarely revisited

compensation is reported but not modeled

depreciation is calculated but not connected to exit planning

passive losses are reported but not strategically reviewed

estimated taxes are based mostly on prior-year figures

retirement planning is limited to contribution reporting

there is no multi-year view of income, liquidity, and tax pressure

The relationship is more advisory-focused if:

projections are reviewed before year-end

open decisions are discussed before execution

business, real estate, investment, and estate planning are coordinated

large transactions are modeled before closing

recommendations include trade-offs, not just deductions

documentation is addressed before filing season

planning considers both current tax savings and future tax cost

the taxpayer has a forward-looking planning calendar

The difference is not whether the advisor is helpful. The difference is whether the advice arrives while the taxpayer can still act.

We help identify whether your current tax relationship is centered on completed filings or forward-looking decision support.

A Better Framework: Compliance, Planning, Advisory

For high-income taxpayers, the conversation is clearer when tax support is viewed in three levels.

Level 1: Compliance

Compliance is the accurate filing of required returns and forms. It includes tax preparation, classification, reporting, reconciliations, and documentation.

This level is essential. Without compliance, planning has no foundation.

Level 2: Planning

Planning focuses on known decisions within a defined time period.

That may include year-end planning, estimated tax planning, retirement contributions, depreciation choices, gain timing, entity elections, or compensation review.

Planning is more proactive than preparation, but it may still be event-specific.

Level 3: Advisory

Advisory connects tax decisions to the taxpayer’s business, investments, liquidity, estate plan, risk tolerance, and future transactions.

It asks:

What is likely to happen over the next several years?

Where could income compress into one year?

Which deductions create future costs?

Which entity structures may become inefficient as the business grows?

Which losses may not be currently usable?

What happens if the business sells, refinances, expands, or slows down?

What records will be needed if the position is questioned later?

Which strategy should be avoided because it does not fit the taxpayer’s broader plan?

This is where tax strategy becomes a decision system rather than a seasonal service.

When Tax Advisory Matters Most

Tax advisory matters most when income, timing, entity structure, or asset activity creates options.

That often includes:

business owners with growing profits

S corporation owners

real estate investors with multiple properties

short-term rental owners

taxpayers considering cost segregation

investors with suspended passive losses

professionals with high compensation or equity income

taxpayers with large capital gains

owners preparing for a business sale

taxpayers receiving K-1 income

families with trusts or estate planning goals

taxpayers with multi-state income

owners adding employees or retirement plans

investors refinancing or selling appreciated property

The common thread is not income alone. It is the number of decisions that can affect the tax result before the return is prepared.

The more moving parts a taxpayer has, the more preparation depends on decisions that were made months or years earlier.

What a Strong Tax Advisory Process Should Produce

Good advisory should make decisions clearer.

It should not leave the taxpayer with vague ideas, disconnected suggestions, or a list of deductions with no implementation plan.

A strong process may produce:

a current-year tax projection

a multi-year income and tax model

an entity structure review

compensation recommendations

retirement plan options

real estate activity analysis

depreciation and disposition planning

estimated tax payment guidance

documentation checklist

transaction timing review

planning calendar

implementation priorities

The best advisory work also identifies what not to do.

Not every deduction is worth pursuing. Not every entity election improves the result. Not every cost segregation study creates usable value. Not every retirement plan fits the employee base. Not every transaction should be accelerated or deferred.

Tax advisory is valuable because it applies judgment to timing, structure, cash flow, risk, and long-term consequences.

The Real Question Is Not “Which Service Do I Need?”

Most high-income taxpayers need both.

They need tax preparation because the return must be filed accurately.

They need tax advisory because the return is only the final step in a much larger financial cycle.

A better question is:

Are tax decisions being reviewed early enough to affect the outcome?

If the answer is no, the taxpayer may be relying on a preparation process to solve an advisory problem.

That is where frustration usually begins.

Conclusion: Tax Preparation Reports the Result. Tax Advisory Helps Shape It.

Tax preparation vs tax advisory is not a debate over which service matters. Both matter.

The problem occurs when taxpayers expect preparation to deliver results that only advisory can create.

For Florida business owners, real estate investors, and high-income professionals, the most important tax decisions often happen before the return exists. They happen when income is being earned, entities are being formed, properties are being acquired, payroll is being run, debt is being structured, depreciation is being planned, and exits are being negotiated.

Once those facts are fixed, the tax return mostly reports them.

A stronger tax relationship starts earlier. It connects preparation, planning, and advisory into one coordinated process, so tax strategy is not limited to what can still be changed after the year is over.

We review preparation, planning, and advisory together so major tax decisions are not limited to filing season.

Tax Advisory Relationship FAQs

Key questions for high-income taxpayers, Florida business owners, and real estate investors evaluating whether their tax relationship is built around filing accuracy, forward-looking advisory, or both.

What should a tax advisory relationship include beyond filing the return?

A tax advisory relationship should create a structured planning process before filing season begins. For sophisticated taxpayers, that usually means reviewing projected income, entity structure, compensation, retirement plan design, real estate activity, depreciation, estimated payments, and known transaction timing. The value is not just a list of ideas. The value is deciding which tax moves fit the taxpayer’s cash flow, documentation, risk tolerance, and multi-year goals. We would expect advisory to produce clearer priorities, not vague suggestions that arrive after the return is already being prepared.

Can a CPA prepare returns without providing real tax advisory?

Yes. A CPA can prepare accurate tax returns without operating as a forward-looking tax advisor. Preparation focuses on reporting completed activity correctly. Advisory focuses on reviewing decisions before they become fixed. The difference usually shows up in timing. If the relationship begins when documents are uploaded, it may be preparation-focused. If projected income, entity structure, compensation, real estate activity, gains, losses, and open decisions are reviewed during the year, it is more advisory-driven. The credential matters, but the process matters more.

When should a high-income taxpayer start tax advisory work?

Tax advisory should begin before the decision that creates the tax result. That may be before a property closes, payroll is finalized, a business changes compensation, an entity election is considered, a capital gain is triggered, or an exit is negotiated. Waiting until year-end may still allow some planning, but it can also leave important decisions already fixed. For high-income taxpayers, timing is often the difference between evaluating options and simply reporting consequences. We view the best advisory work as decision support, not seasonal cleanup.

Why does tax advisory matter if my tax return is already accurate?

An accurate return tells us the facts were reported correctly. It does not tell us whether the facts were structured well. A taxpayer can have a clean return and still miss planning windows, create avoidable tax compression, underuse real estate losses, misalign compensation, or fail to model exit-year consequences. Preparation protects compliance. Advisory reviews whether the decisions behind the return are coordinated. For high-income business owners and investors, the concern is often not whether last year was filed correctly. It is whether next year is being shaped early enough.

How does tax advisory help real estate investors avoid short-term thinking?

Real estate tax planning can look attractive when viewed only through first-year deductions. Advisory adds the next layer: whether depreciation is usable, whether passive loss rules limit the benefit, how basis and at-risk exposure affect the result, and what happens when the property is refinanced or sold. A strong advisory process connects acquisition, depreciation, cash flow, documentation, and disposition. The goal is not to avoid every future tax cost. The goal is to understand the trade-offs before a strategy creates pressure in a later year.

What questions should a business owner ask before assuming they have tax advisory?

A business owner should ask whether projected income is reviewed before year-end, whether compensation is modeled before payroll closes, whether entity structure is revisited as the business grows, and whether retirement planning is coordinated with cash flow and employee realities. They should also ask whether recommendations include implementation steps and trade-offs. If the conversation is mostly about forms, uploads, and what happened last year, the relationship may be preparation-centered. Advisory should help the owner make better tax-sensitive decisions before those decisions are locked into the return.

How does Florida residency change the tax advisory conversation?

Florida residency may reduce one state income tax layer, but it does not remove the need for advisory planning. Florida high-income taxpayers still need to coordinate federal income tax, payroll tax, self-employment tax, capital gains, passive losses, depreciation, entity structure, and multi-state exposure where applicable. For many Florida business owners and investors, the federal planning layer carries the largest tax consequences. Advisory should focus on where the real planning decisions remain: income timing, structure, compensation, real estate activity, documentation, and exit planning.

What makes tax advisory different from receiving occasional tax tips?

Occasional tax tips are usually isolated. Advisory should be coordinated. A tip may address one deduction, one entity choice, or one year-end move. Advisory asks whether that move fits the taxpayer’s broader income pattern, cash flow, asset structure, future sale plans, and documentation. This matters because a strategy can look reasonable in isolation but create friction elsewhere. For sophisticated taxpayers, the value is not simply more ideas. It is better sequencing, better prioritization, and fewer disconnected decisions.