Audit Risk and Documentation Standards for Advanced Depreciation Strategies

Advanced depreciation strategies can be valuable, but the deduction is only as strong as the facts supporting it.

For high-income real estate investors, business owners, and Florida taxpayers with complex holdings, the real question is not simply whether a cost segregation study, bonus depreciation, Section 179 election, or repair deduction is available. The better question is whether the strategy can be defended across the full life of the asset.

Advanced depreciation planning should connect current-year deductions to the documentation, limitations, and exit consequences that determine whether the strategy holds up over time.

“A depreciation strategy should not be evaluated only by the size of the deduction. The stronger planning question is whether the position remains supported when income, ownership, financing, or exit timing changes.”

That means the documentation must support more than one tax year. It should connect acquisition records, placed-in-service dates, cost allocations, business use, entity ownership, passive activity treatment, depreciation method, and eventual exit planning.

A strong depreciation strategy does not begin with the deduction. It begins with the file that proves why the deduction belongs in the return.

Audit Risk and Documentation Standards for Advanced Depreciation Strategies: The Core Issue

The immediate answer is this:

Advanced depreciation strategies require documentation that proves five things:

Depreciation Strategy Depends on Supportable Documentation

Advanced depreciation planning should be supported before the deduction is claimed, not reconstructed after the tax position is questioned.

| Documentation Area | What Must Be Supported | Why It Matters |

|---|---|---|

| Eligibility | The asset qualifies for the depreciation treatment claimed. | Prevents deductions on ineligible property. |

| Timing | The asset was actually placed in service in the claimed year. | Supports bonus depreciation, Section 179, and MACRS timing. |

| Basis | The depreciable cost was properly calculated and allocated. | Prevents overstated depreciation. |

| Classification | The asset was assigned to the correct recovery period and property type. | Supports cost segregation and method selection. |

| Use and Limitations | The taxpayer can actually use the deduction. | Connects depreciation to passive loss, basis, at-risk, and business-use rules. |

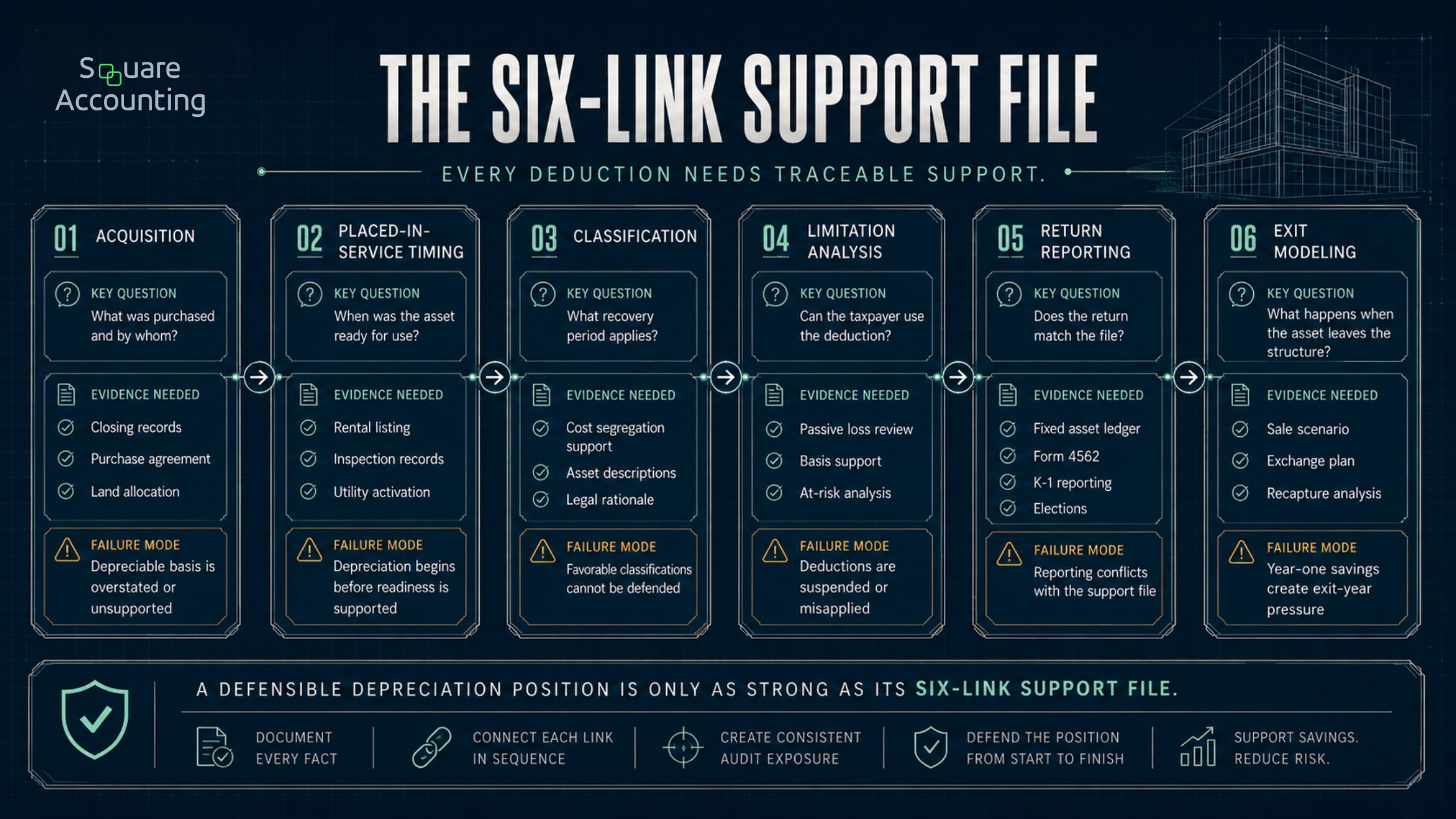

For sophisticated taxpayers, the audit risk often does not come from taking depreciation. It comes from claiming accelerated depreciation without a clean chain of support.

A deduction may be technically available, but still create planning problems if the loss is suspended, the ownership structure is inconsistent, the cost segregation study is thin, the placed-in-service date is poorly supported, or the exit-year recapture was never modeled.

The Tax Return Is Not the Documentation File

A common mistake is assuming that Form 4562, a depreciation schedule, and a cost segregation report are enough.

They are important, but they are not the whole file.

The tax return reports the position. It does not always prove the position.

A stronger depreciation file usually includes:

closing statements and purchase agreements

appraisals or allocation support for land versus depreciable property

invoices, contracts, and draw schedules

construction documents and change orders

placed-in-service support

photographs or inspection records

cost segregation study and supporting workpapers

fixed asset ledger reconciliation

entity ownership records

business-use support

passive activity and material participation support

depreciation elections and method-change documentation

disposition planning records for future sale, exchange, or transfer

The higher the deduction, the more important the chain becomes.

This is especially true when a taxpayer is accelerating deductions into a high-income year. The upfront tax benefit may be attractive, but the position should still be able to survive review several years later.

Use our review lens to identify where documentation may be thin before the position becomes part of the return.

Why Advanced Depreciation Creates Audit Sensitivity

Depreciation is not inherently aggressive. The risk increases when depreciation is accelerated, reclassified, or used to produce large losses against other income.

Several strategies can raise the level of review:

Cost segregation

A cost segregation study may reclassify parts of a building into shorter-life property. This can accelerate deductions, especially when bonus depreciation applies.

But the study must do more than produce a favorable number. It should explain the methodology, classify assets correctly, reconcile allocated costs to actual costs, and support why assets are treated as personal property, land improvements, qualified improvement property, or structural components.

A weak study often creates risk because it looks like a result-driven allocation rather than an engineering-supported tax analysis.

Bonus depreciation

Bonus depreciation can create a large first-year deduction for eligible property. Current law restored 100% bonus depreciation for certain qualified property acquired and placed in service after January 19, 2025.

That makes timing documentation more important. The file should support when the property was acquired, when it was ready and available for its intended business or income-producing use, and whether the asset qualifies.

For real estate investors, the placed-in-service date is not always the closing date. A rental property, improvement, or component may need to be ready and available for use before depreciation begins.

Section 179

Section 179 can be useful for business equipment and certain qualifying property, but it is not the same as bonus depreciation.

The deduction has eligibility rules, annual limitations, business income limitations, and special treatment for certain vehicles and property types. In partnership or S corporation structures, the deduction may also need to be analyzed at both the entity and owner level.

For high-income taxpayers, the question is not only “Can we elect Section 179?” It is also “Where should the deduction be claimed, and will the taxpayer actually benefit from it?”

Repairs, improvements, and capitalization

The repair-versus-improvement analysis is one of the easiest areas to oversimplify.

A current deduction may be available for certain repairs and maintenance. But costs that acquire, produce, improve, restore, adapt, or better property may need to be capitalized.

This distinction matters because an incorrectly deducted repair can create audit exposure, while an incorrectly capitalized item may delay a legitimate deduction.

For Florida real estate investors, this often comes up after renovations, storm-related work, insurance claims, tenant turnover, property conversions, and major building system replacements.

Partial dispositions and late depreciation adjustments

Partial disposition elections and accounting method changes can be valuable when prior assets are replaced or when a cost segregation study is performed after the original placed-in-service year.

But these strategies require careful documentation. The taxpayer should be able to show the original asset, the replacement, the remaining basis, the timing, and the return position.

A late strategy can still be valid, but the file needs to be cleaner because the tax position is reconstructing prior-year facts.

The Differentiated Planning Standard: Build a Chain of Proof

We use a simple framework for reviewing advanced depreciation strategies:

A defensible depreciation position depends on whether each support point connects cleanly to the next planning decision.

“The strongest depreciation file does not live in one document. It works like a planning sequence, where each decision must be traceable to the facts that came before it.”

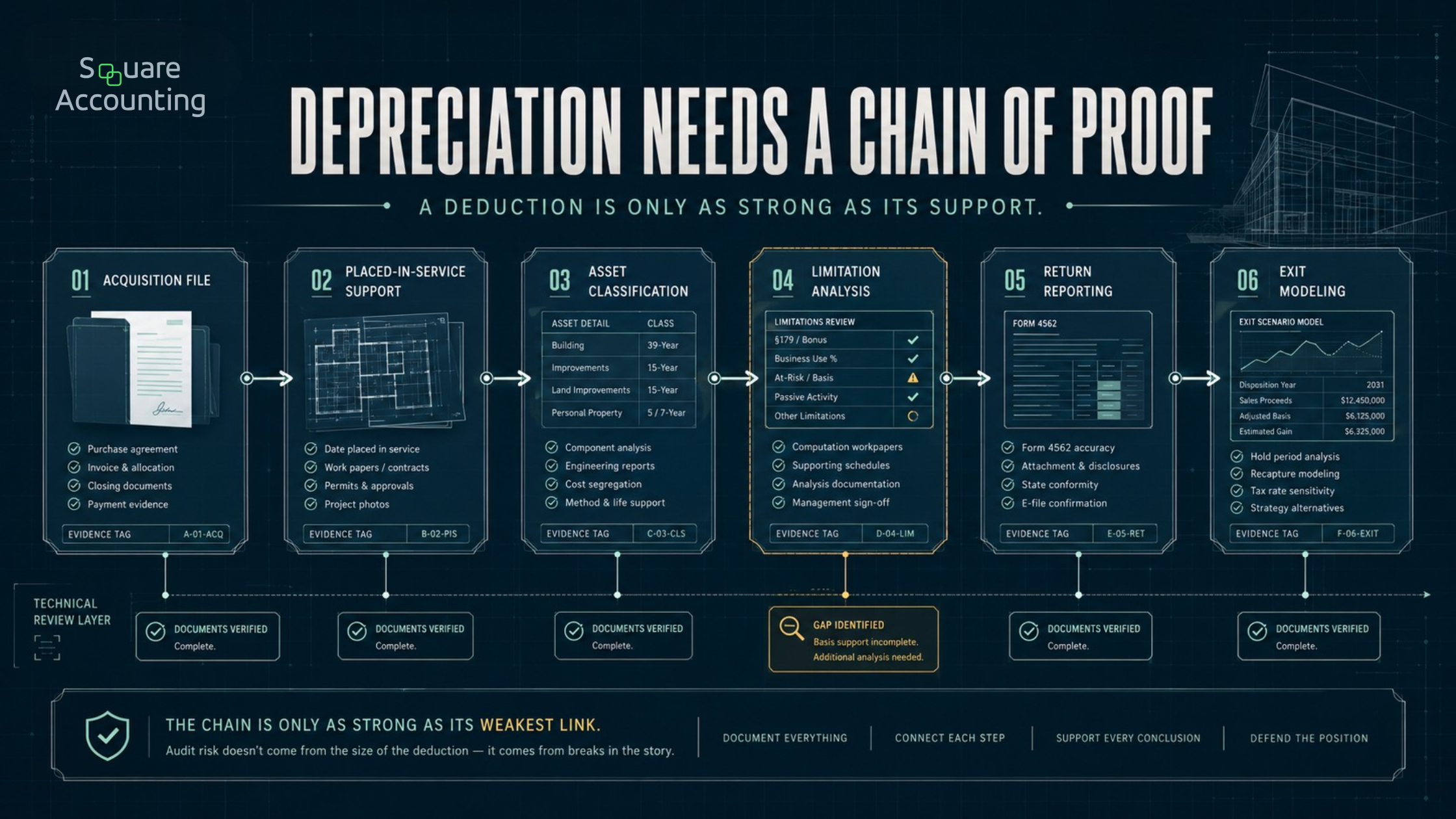

The Depreciation Chain of Proof

A defensible depreciation position should connect six links.

1. Acquisition

The file should show what was purchased, who purchased it, when it was acquired, and how the purchase price was allocated.

For real estate, this includes land versus building allocation. For portfolio purchases, it may also include allocations among multiple properties, improvements, furniture, fixtures, equipment, and intangible assets.

A closing statement alone may not be enough if the tax position depends on a more detailed allocation.

2. Placed-in-service timing

The placed-in-service date should be supported by the facts.

For rental property, that may include the date the property was ready and available for rent, listing records, management agreements, certificates of occupancy, inspection records, utility activation, or advertising.

For business equipment, that may include delivery, installation, calibration, training, or operational readiness.

This matters because depreciation generally begins when property is ready and available for its intended use, not merely when it is paid for.

3. Classification

The asset classification should be tied to legal and factual support.

For cost segregation, the study should explain why each asset belongs in its assigned class. The strongest studies are not just spreadsheets. They include methodology, engineering analysis, cost support, legal rationale, and reconciliation to actual costs.

A report that only provides final percentages without detailed support may be harder to defend.

4. Limitation analysis

The deduction should be tested against the taxpayer’s ability to use it.

This is where sophisticated planning often breaks down.

A large depreciation deduction may be limited by:

basis limitations

business income limitations for Section 179

partner or shareholder-level limitations

grouping decisions

material participation documentation

net investment income tax considerations

The depreciation strategy should be coordinated with the taxpayer’s broader income profile. A deduction that becomes suspended may still have value, but it is not the same as a deduction that offsets current high-tax income.

5. Return reporting

The tax return should match the planning file.

Depreciation schedules, fixed asset ledgers, Form 4562 reporting, K-1 allocations, method-change filings, and passive activity forms should tell the same story.

Inconsistent reporting creates avoidable questions.

For example, a taxpayer may have a cost segregation study showing substantial short-life property, but the fixed asset ledger may not reconcile to the return. Or the return may claim large rental losses while the participation file does not support nonpassive treatment.

The numbers and the narrative need to agree.

6. Exit modeling

The exit year should be modeled before the deduction is claimed.

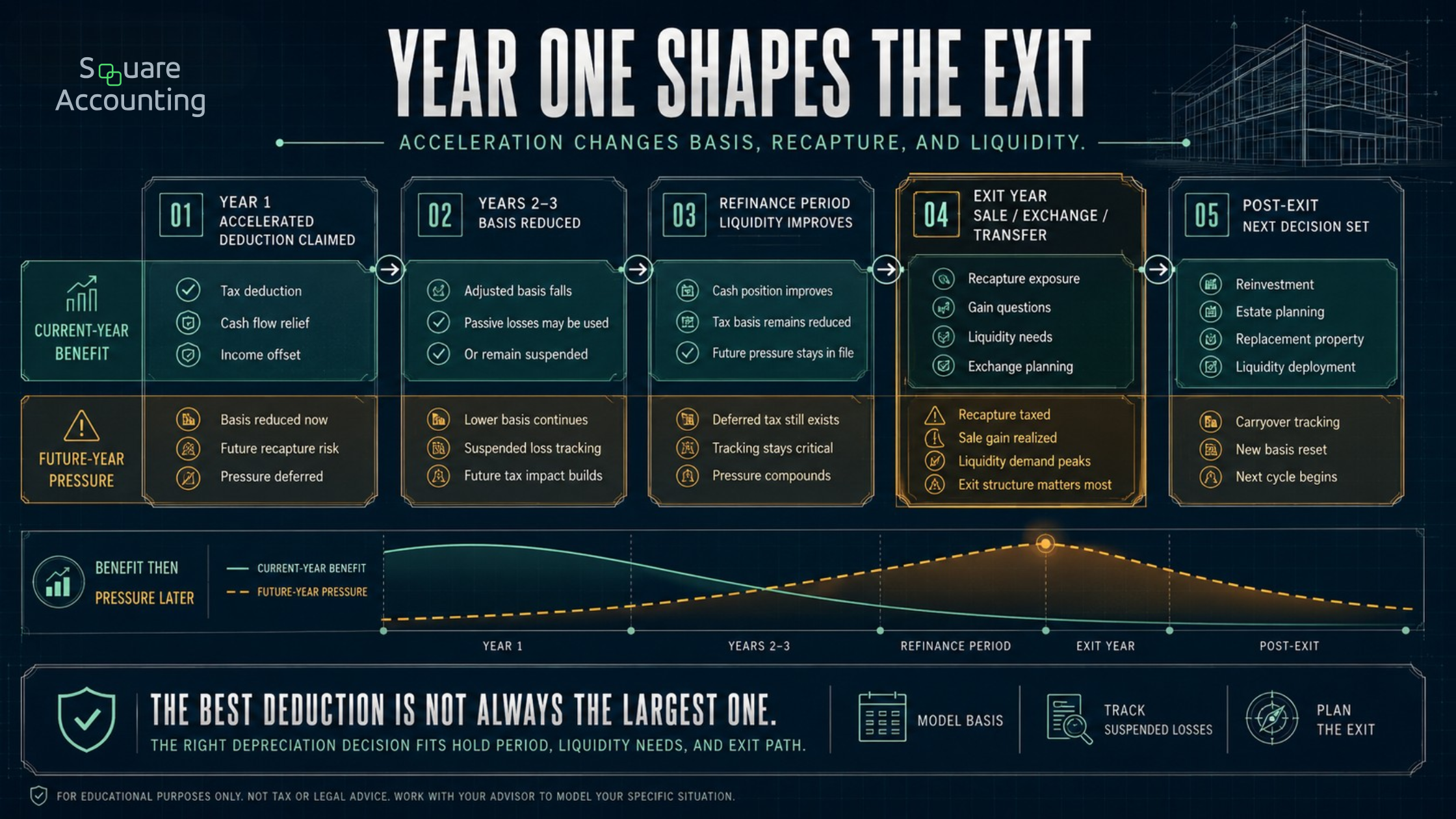

Accelerated depreciation is not free from future consequences. It changes basis. It can affect gain. It can create depreciation recapture. It can change the economics of a sale, refinance, installment sale, contribution, gift, or 1031 exchange.

This is one of the biggest blind spots in depreciation planning.

A strategy that looks excellent in year one may be less attractive if the taxpayer expects to sell in year three, refinance under tight debt coverage constraints, or transfer the asset into a broader estate plan.

The right question is not “How much depreciation can we take?” The better question is “What happens when this asset exits the structure?”

Accelerated depreciation should be modeled against realistic exit scenarios before the deduction is claimed.

“The exit year often reveals whether the original depreciation strategy was coordinated or isolated. A deduction that improves current tax cash flow may still create basis, recapture, or liquidity pressure later.”

Identify whether the documentation supports the depreciation position before it becomes part of the filed return.

Common Audit Weak Points in Advanced Depreciation Strategies

The following issues do not automatically mean a position is wrong. They do signal that the file should be reviewed before the return is finalized.

1. The cost segregation study does not reconcile to actual costs

A quality study should reconcile allocated costs to total actual costs. If the study uses estimates, sampling, or modeling, the methodology should be explained.

The risk increases when the report produces favorable classifications but does not clearly connect those classifications to invoices, plans, cost records, or engineering support.

2. The placed-in-service date is assumed, not proven

This is common with rental real estate.

A taxpayer may close on a property in December and claim depreciation for that year, but the property may not have been ready and available for rent until the following year.

The file should support readiness, not merely ownership.

3. Land value is understated

Land is not depreciable. If the land allocation is too low, building depreciation may be overstated.

For Florida properties, land value can be a meaningful part of the purchase price, especially in coastal markets, high-growth corridors, and redevelopment areas. A generic land allocation may not be enough for higher-value properties.

4. The repair position conflicts with the renovation facts

A taxpayer may deduct costs as repairs while the project records show a broader improvement, restoration, adaptation, or building system replacement.

The issue is not the label on the invoice. The issue is what the work actually did to the property.

5. Passive loss treatment is not coordinated with the depreciation plan

Large real estate depreciation deductions often create losses. For high-income investors, those losses may be passive unless an exception applies.

If the tax plan depends on using losses against W-2, business, or portfolio income, the participation file becomes part of the depreciation defense.

That may include time logs, calendars, management records, emails, contractor communications, and documentation showing who performed which activities.

6. Entity ownership and tax reporting do not match

Depreciation belongs to the taxpayer or entity that owns the property for tax purposes.

Problems arise when legal title, disregarded entity ownership, partnership reporting, debt agreements, operating agreements, and tax return reporting are not aligned.

This is especially important for real estate groups with multiple LLCs, family ownership, trusts, tiered partnerships, or properties acquired with partners.

7. The strategy ignores recapture

Accelerated depreciation may increase future recapture exposure.

For taxpayers expecting a near-term sale, the exit consequences should be reviewed before claiming the largest possible current-year deduction.

In some cases, the strategy may still make sense. In others, the better planning move may be to moderate the deduction, change sequencing, coordinate with a 1031 exchange, or prepare for the after-tax liquidity impact of a taxable sale.

Florida Planning Considerations

Florida’s lack of individual state income tax can make federal tax planning especially important for high-income residents. But it can also create a behavioral trap.

Because there may be no Florida individual income tax benefit layered on top of the federal deduction, the federal result carries most of the planning weight. That makes it even more important to model whether the depreciation deduction is usable, properly supported, and aligned with the investor’s exit plan.

Florida real estate investors should also consider the practical documentation issues created by the local market:

property insurance pressure

hurricane and storm repairs

special assessments

condominium and HOA work

short-term rental conversions

tenant turnover renovations

coastal land value allocations

rapid appreciation and refinance activity

portfolio acquisitions across multiple counties

These facts do not change the federal depreciation rules by themselves. But they do affect the records needed to support basis, repairs, improvements, casualty-related work, readiness for rent, and long-term planning.

For a Florida investor with significant real estate holdings, depreciation should be reviewed alongside cash reserves, debt structure, insurance exposure, and exit timing. A deduction that improves tax cash flow but weakens liquidity planning may not be the best strategy.

We help evaluate depreciation documentation in the context of Florida real estate facts, insurance pressure, renovations, and hold-period decisions.

Documentation Standards by Strategy

Cost Segregation Documentation

A strong cost segregation file should include:

full cost segregation report

preparer qualifications

methodology explanation

legal rationale for classifications

engineering or construction analysis

site visit notes or alternative support

photographs, plans, or asset descriptions

cost source documents

indirect cost allocation methodology

reconciliation to total project or purchase cost

fixed asset ledger updates

depreciation schedule impact

recapture modeling

The report should not be evaluated only by the tax savings estimate. It should be evaluated by how well it supports the classification.

Bonus Depreciation Documentation

A bonus depreciation file should support:

qualified property status

acquisition date

placed-in-service date

original use or used property eligibility

business or income-producing use

depreciation method

election out or reduced bonus election, if applicable

entity-level and owner-level reporting

impact on basis and future gain

With 100% bonus depreciation restored for certain qualified property acquired and placed in service after January 19, 2025, timing support is especially important.

The placed-in-service file should be strong enough to answer a simple question: what evidence shows the asset was ready and available for its intended use during the year claimed?

Section 179 Documentation

A Section 179 file should support:

qualifying property

active trade or business use

placed-in-service date

business-use percentage

taxable income limitation

annual dollar limitation

entity-level reporting

partner or shareholder-level limitation

vehicle limitations, if relevant

election details

Section 179 should be coordinated with bonus depreciation, especially when the taxpayer has multiple entities, multiple properties, or mixed active/passive activities.

Repairs and Capitalization Documentation

A repairs file should support:

the unit of property

the condition before the work

the reason for the work

invoices and scope of work

whether the work improved, restored, adapted, or merely maintained the property

building system affected

routine maintenance analysis, if applicable

treatment of replaced components

book-to-tax consistency

A practical test: if the invoice description is vague, the documentation should be stronger elsewhere.

“Repairs” is not a conclusion. It is a position that should be supported by facts.

Partial Disposition Documentation

A partial disposition file should support:

asset removed or retired

replacement asset

original basis or reasonable basis reconstruction

accumulated depreciation

date of disposition

method used to determine remaining basis

election timing

coordination with capitalization of replacement property

This can be particularly relevant when older building systems are replaced after a cost segregation study or major renovation.

The Planning Question Beneath the Surface

Most taxpayers ask:

How much depreciation can we claim?

The better planning question is:

How much depreciation should we claim, in this structure, in this year, with this exit plan, and with this documentation?

That shift matters.

A high-income taxpayer with strong current-year income, long-term ownership intent, sufficient basis, nonpassive treatment, and clean documentation may benefit from a more aggressive acceleration strategy.

A taxpayer with passive limitations, uncertain holding period, weak records, near-term sale plans, or fragmented entity reporting may need a different approach.

The strategy is not just about deduction size. It is about deduction durability.

When a Depreciation Strategy Can Backfire

Advanced depreciation can create problems when it is implemented without a full planning review.

The deduction is large but unusable

If passive loss, basis, or at-risk limitations apply, the deduction may be suspended. That does not necessarily make the strategy bad, but it changes the expected value.

A suspended deduction should be planned intentionally, not discovered after the return is prepared.

The study increases future ordinary income exposure

Cost segregation can move certain property into shorter-life categories. That may accelerate deductions, but it can also affect recapture treatment on sale.

If the investor expects to sell soon, exit-year modeling should be part of the initial analysis.

The property is refinanced after aggressive depreciation

Depreciation reduces tax basis, not loan balance. A refinance may improve liquidity, but it does not erase future gain or recapture exposure.

Investors should avoid confusing debt proceeds with tax-free economic gain. The long-term tax result still needs to be modeled.

The documentation depends on memory

Depreciation positions are often reviewed years after the work was done. By then, contractors may be unavailable, invoices may be unclear, property managers may have changed, and ownership teams may not remember the details.

The best time to document the position is when the facts are fresh.

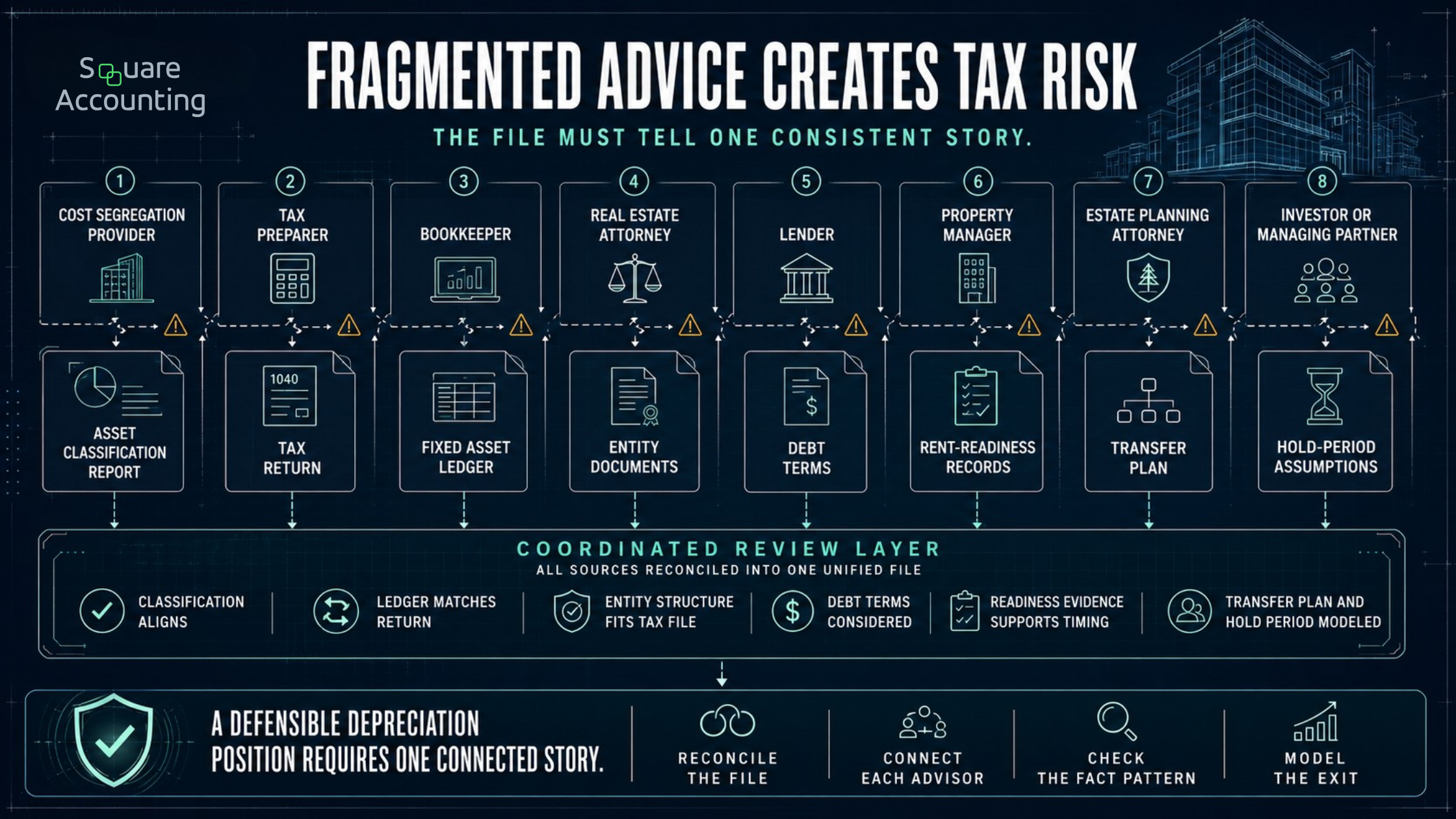

Advisor Coordination Matters

Advanced depreciation planning usually involves more than one advisor.

A strong process may include:

tax advisor

cost segregation engineer

bookkeeper

real estate attorney

lender

property manager

estate planning attorney

investment sponsor or managing partner

The risk is not only that one advisor makes a mistake. The bigger risk is that each advisor sees only one part of the transaction.

Advanced depreciation planning becomes stronger when each advisor’s work supports the same tax position, ownership structure, and exit assumption.

“For higher-net-worth investors, documentation risk often comes from fragmentation rather than a single technical error. The planning file should reconcile the study, ledger, entity documents, debt assumptions, participation support, and exit model before filing.”

For example:

The cost segregation provider may focus on classification.

The tax preparer may focus on reporting.

The attorney may focus on entity structure.

The lender may focus on debt terms.

The estate attorney may focus on transfer goals.

The investor may focus on current-year tax savings.

Depreciation strategy sits in the middle of all of those decisions.

That is why the planning file should be coordinated before filing, not reconstructed after an IRS notice.

Clarify whether the cost segregation, bookkeeping, tax reporting, entity structure, and exit plan are telling the same story.

A Practical Pre-Filing Review Checklist

Before claiming a significant advanced depreciation position, review the following:

Do we have acquisition and closing records?

Is land value separately supported?

Is the placed-in-service date documented?

Does the cost segregation report reconcile to actual cost?

Are asset classifications explained with legal and factual support?

Are depreciation schedules updated and consistent with the return?

Have bonus depreciation and Section 179 elections been reviewed?

Are passive loss, basis, and at-risk limitations modeled?

Is material participation documentation needed?

Does the entity structure match the reporting?

Have repair versus improvement positions been reviewed?

Are partial disposition opportunities or risks addressed?

Has depreciation recapture been modeled under likely exit scenarios?

Does the strategy still make sense if income declines?

Does the strategy still make sense if the property sells earlier than expected?

If the answer to several of these questions is unclear, the issue is not necessarily that the strategy should be abandoned. It may mean the strategy needs stronger support before it is reported.

How We Think About Depreciation for High-Income Florida Taxpayers

For sophisticated taxpayers, depreciation should not be treated as a one-year deduction project.

It should be part of a broader tax architecture.

That architecture should answer:

What income are we trying to offset?

Is the loss usable this year?

What documentation supports the position?

What happens if the property is sold?

What happens if the property is exchanged?

What happens if ownership changes?

What happens if the taxpayer no longer qualifies for nonpassive treatment?

What happens if insurance, debt, or cash flow pressure changes the hold period?

The strongest depreciation strategies are not always the most aggressive. They are the ones that align tax savings with facts, documentation, cash flow, ownership, and exit planning.

Depreciation Planning Requires More Than the Right Calculation

Most real estate investors focus on how much they can depreciate. The more important question is whether that deduction will actually reduce their tax bill — and the answer is not always yes.

A correct depreciation calculation can still be limited or eliminated by passive activity rules, basis restrictions, at-risk limitations, and business income caps. Getting the math right is necessary, but it is not sufficient. Depreciation planning has to account for the taxpayer's full income picture, entity structure, and the year the deduction is expected to land.

For larger commercial properties, a cost segregation study is the strongest available support for reclassifying building-related costs into shorter-life asset categories. It is not always legally required, but it provides the documentation foundation that matters when positions are later reviewed. The same discipline applies to recordkeeping more broadly. Closing statements, purchase agreements, land and building allocation support, invoices, construction records, placed-in-service documentation, depreciation schedules, and repair records should be organized and maintained as a permanent part of the property file — not reconstructed when they are needed.

Florida investors operate under the same federal depreciation rules as everyone else, but the context is different. No state income tax means the federal result carries the full weight of the tax outcome. Rapid appreciation, rising insurance costs, storm repair exposure, and casualty risk all make federal depreciation planning and exit modeling more consequential in Florida than in states where tax liability is split across multiple layers. The rules are the same. The stakes are higher.

Recapture planning deserves the same attention as the deduction itself. Bonus depreciation reduces taxes today, but it increases gain and recapture exposure when the property is eventually sold, exchanged, or transferred. For investors who may not hold long term, the multi-year result can look significantly different from the first-year benefit. The decision to accelerate depreciation should follow a modeled exit path — not precede one.

Conclusion: Depreciation Should Be Defensible Before It Is Valuable

Audit risk and documentation standards for advanced depreciation strategies should be reviewed before the return is filed, not after a question arrives.

A cost segregation study, bonus depreciation deduction, Section 179 election, repair deduction, or partial disposition can all be valuable. But each one should fit into a documented, multi-year plan.

For high-income Florida taxpayers and real estate investors, the real opportunity is not simply accelerating deductions. It is building a depreciation strategy that can support current tax efficiency, future liquidity, audit readiness, and exit planning at the same time.

If your depreciation strategy depends on large deductions, multiple entities, real estate activity classification, or a future sale or exchange, a pre-filing review can help identify whether the position is supported before it becomes part of the return.

If the strategy depends on large deductions, multiple entities, or exit planning, review the support before the return is filed.

Advanced Depreciation Documentation FAQs

Key questions for real estate investors and business owners evaluating cost segregation, bonus depreciation, Section 179, placed-in-service timing, passive loss limits, and exit-year exposure.

What makes an advanced depreciation position more likely to draw IRS attention?

An advanced depreciation position becomes more sensitive when the deduction is large, accelerated, or used to create losses against other income. The issue is not depreciation by itself. The issue is whether the file supports the full position: acquisition cost, land allocation, placed-in-service timing, asset classification, business use, and limitation analysis. We would pay closer attention when cost segregation, bonus depreciation, Section 179, repair deductions, or partial dispositions materially change taxable income. The stronger the deduction’s impact, the more important it is for the documentation to show a clear chain from facts to return reporting.

How should a cost segregation report be reviewed before it is used on a tax return?

A cost segregation report should be reviewed for support, not just savings. We would look for methodology, preparer qualifications, asset descriptions, cost sources, allocation logic, legal rationale, and reconciliation to the purchase price or project cost. A report that produces favorable classifications without explaining how those classifications were determined may create avoidable risk. For sophisticated investors, the better question is whether the study can be understood and defended years later, especially if the property is sold, exchanged, refinanced, or reviewed in connection with passive loss or recapture planning.

What records help support the placed-in-service date for rental real estate?

Placed-in-service support should show when the property was ready and available for its intended rental use. Useful records may include listing history, lease availability, management agreements, inspection records, certificates of occupancy, utility activation, repair completion records, photographs, and communications with contractors or property managers. Closing on a property is not always enough. For Florida investors acquiring or renovating property near year-end, this distinction can matter because the depreciation start date depends on readiness for use, not simply ownership or payment timing.

Can a depreciation deduction be technically correct but still poorly planned?

Yes. A depreciation deduction can be calculated correctly and still be strategically weak if it is unusable, poorly timed, or disconnected from the exit plan. For example, accelerated depreciation may create a loss that is suspended by passive activity, basis, or at-risk limitations. It may also reduce basis and increase future recapture exposure if the property is sold sooner than expected. We would not evaluate the deduction only by year-one tax reduction. We would also review whether the deduction fits the taxpayer’s income profile, ownership structure, liquidity needs, and likely holding period.

How do passive activity rules affect advanced depreciation planning?

Passive activity rules can determine whether a large real estate depreciation deduction produces current tax value or becomes suspended. This is especially important for high-income taxpayers who expect depreciation to offset W-2 income, business income, or portfolio income. The depreciation file should therefore connect to the participation file. Time logs, calendars, management records, contractor communications, and activity grouping decisions may become part of the broader support. A depreciation strategy that ignores passive loss treatment may look strong on paper but fail to produce the expected current-year result.

Why should depreciation recapture be reviewed before claiming accelerated deductions?

Depreciation recapture should be reviewed because accelerated deductions can change the after-tax economics of a later sale, exchange, or transfer. The current-year deduction reduces basis, and that can affect gain recognition when the property exits the structure. This does not mean accelerated depreciation is automatically a poor choice. It means the benefit should be modeled against realistic exit scenarios. If a property may be sold in the near term, contributed to a new structure, exchanged, or transferred as part of estate planning, the recapture profile should be understood before the deduction is claimed.

What Florida real estate facts can make depreciation documentation more important?

Florida facts often create documentation pressure because property activity can move quickly. Insurance claims, hurricane repairs, tenant turnover renovations, condominium work, HOA assessments, short-term rental conversions, refinance activity, and coastal land values can all affect the depreciation file. These facts do not create separate federal depreciation rules, but they can affect basis support, repair-versus-improvement analysis, land allocation, placed-in-service timing, and exit planning. For higher-value Florida properties, generic documentation may not be enough to support a position that materially changes federal taxable income.

How should multiple advisors coordinate around a depreciation strategy?

The tax advisor, cost segregation provider, bookkeeper, attorney, lender, property manager, and estate planning advisor may each see a different part of the transaction. The risk is that the depreciation strategy becomes fragmented. We would want the study, fixed asset ledger, entity structure, operating documents, participation file, debt plan, and exit assumptions to tell the same story. Coordination matters most before the return is filed. Once a position is reported, it is harder to reconstruct facts, correct inconsistent records, or explain why the deduction fit the broader tax plan.