Coordinating Cost Segregation Across Multiple Properties and Tax Years

Cost segregation becomes more strategic when each property is evaluated within the investor’s full tax timeline, not as a standalone deduction opportunity.

The real planning issue is not whether cost segregation works. It is when, where, and against what income it works.

Cost segregation can be valuable, but the decision is not simply, “Should we get a study?” For a high-income investor with several properties, the better question is:

Which properties should generate accelerated depreciation, in which tax years, for which taxpayer, and against what income?

That is the immediate planning issue behind coordinating cost segregation across multiple properties and tax years.

A cost segregation study can identify portions of a building or improvement project that may be classified separately from long-life real property. The IRS cost segregation audit guide emphasizes the need to allocate purchase price and project costs among land, land improvements, building components, and personal property using supportable methods. Cost segregation can apply to acquired property, newly constructed property, renovated property, and certain older properties where the original depreciation method may be corrected.

For a portfolio, the value of the study depends on more than engineering classifications. It depends on whether the deductions can be used, whether they are trapped by passive activity rules, whether they land in the right entity, and what they do to the eventual exit.

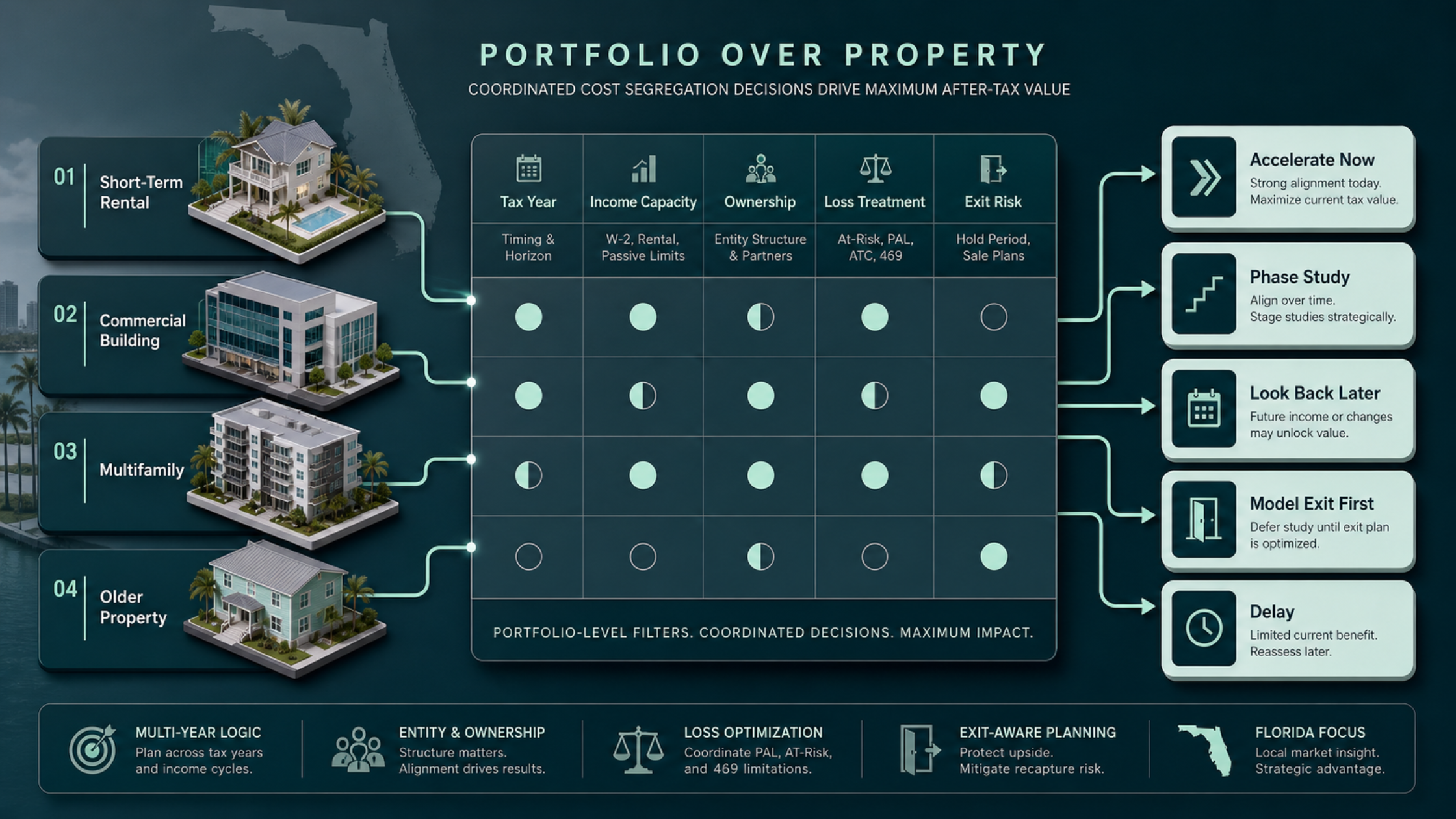

A practical starting framework looks like this:

| Planning Question | Why It Matters |

|---|---|

| Which property should be studied first? | The best candidate is not always the largest building. It is the property whose deductions can be used most efficiently. |

| Which tax year should absorb the deduction? | A deduction in a high-income year may be worth more than the same deduction in a lower-value year. |

| Who owns the deduction? | Entity structure, basis, debt allocation, and ownership determine where the deduction lands. |

| Is the loss passive or non-passive? | Passive losses may be suspended even when the depreciation calculation is correct. |

| Is bonus depreciation available or desirable? | Acceleration can be powerful, but it may reduce flexibility if it is not coordinated with income and exit plans. |

| What happens in the exit year? | Lower basis can increase taxable gain, recapture exposure, NIIT pressure, and liquidity strain. |

Cost segregation is not just a depreciation study. In a sophisticated real estate portfolio, it is a timing, classification, ownership, and exit-planning decision.

Why this matters more for high-income Florida investors

Florida real estate investors often hold concentrated portfolios: long-term rentals, short-term rentals, multifamily buildings, medical offices, warehouses, retail centers, mixed-use property, or real estate connected to an operating business.

Florida does not impose a personal income tax, which makes federal tax planning carry more of the weight for high-income residents. The Florida Department of Revenue states that Florida does not impose personal income tax, inheritance tax, gift taxes, or tax on intangible personal property. That can be favorable, but it also narrows the planning field. The biggest recurring tax questions are often federal: ordinary income, passive activity limits, NIIT, depreciation recapture, capital gains, basis, estate planning, and transaction timing.

That is why a fragmented approach is costly.

One advisor may order a cost segregation study for a newly acquired short-term rental. Another may prepare a partnership return for a commercial building. A third may discuss a 1031 exchange. Each recommendation may be reasonable in isolation, but the household does not pay tax in isolation.

The real issue is coordination.

If three properties generate accelerated depreciation in the same year, the taxpayer needs to know whether those losses can be used, whether they should be used now, whether a future sale will unwind the benefit, and whether Florida-specific holding risks could shorten the expected timeline.

Florida investors also need to pressure-test assumptions that do not appear on a depreciation schedule: insurance costs, storm exposure, reserves, special assessments, financing renewals, and property tax economics. These factors can change the hold period, and hold period is central to cost segregation planning.

Key takeaways

Coordinating cost segregation across multiple properties and tax years is a portfolio sequencing problem. The goal is not to create the largest possible deduction in the earliest possible year. The goal is to place depreciation where it produces durable after-tax value.

A deduction has to be matched with tax capacity. Capacity depends on income level, passive or non-passive classification, real estate professional status, short-term rental facts, basis, at-risk limits, and entity ownership.

Bonus depreciation increases both opportunity and timing risk. Current IRS guidance describes permanent 100% additional first-year depreciation for qualified property acquired after January 19, 2025, assuming the property and timing requirements are met. That makes coordination more important, not less important.

Passive activity rules often decide whether accelerated depreciation creates current tax value. Rental activity is generally passive unless an exception applies, and real estate professional treatment requires specific annual tests and material participation.

Exit-year modeling should happen before implementation. Cost segregation lowers basis and can affect gain character, depreciation recapture, unrecaptured Section 1250 gain, NIIT exposure, liquidity, and 1031 exchange planning.

For Florida taxpayers, federal efficiency and liquidity durability matter more than state income tax arbitrage. The planning has to reflect real estate concentration, no personal state income tax, homestead versus non-homestead economics, and property-level risk.

Continue with related planning around NIIT, passive losses, entity structure, and real estate exits.

Why multiple-property cost segregation is different from a one-property study

A single-property study answers a narrow technical question: how should that property’s depreciable basis be classified?

A multiple-property plan answers a broader strategic question: how should depreciation be deployed across the taxpayer’s full real estate system?

That system includes the household, the entities, the properties, the debt, the participation facts, and the expected exits.

A taxpayer with one rental building may compare the cost of the study against the expected first-year deduction. A taxpayer with five properties needs a different analysis:

Which properties are newly placed in service?

Which properties were acquired in prior years without a study?

Which properties have current taxable income?

Which activities produce passive income?

Which activities produce losses?

Which losses are suspended?

Which taxpayer or entity receives the deduction?

Which properties may be sold, exchanged, refinanced, gifted, or held until death?

Which years are expected to include unusually high income or capital gains?

Which properties face insurance, casualty, financing, or liquidity pressure?

A cost segregation vendor may focus on the study. We focus on the placement of the deduction.

Those are not the same job.

The study can be technically accurate and still be poorly timed. It can create a large deduction inside an entity that cannot use it. It can accelerate depreciation on a property likely to be sold before the time-value benefit matures. It can produce suspended losses that look impressive on paper but do not change current cash tax.

For a high-income investor, “How much depreciation can the study generate?” is only the first question. The more important question is, “How much of that depreciation improves the lifetime tax result after passive loss rules, NIIT, recapture, entity structure, and exit timing are modeled?”

We can help evaluate which properties, entities, and tax years deserve priority before depreciation is accelerated.

Current-law starting point: bonus depreciation makes sequencing more important

Bonus depreciation changes the scale of the planning decision.

Current IRS guidance states that, in general, the One Big Beautiful Bill provides permanent 100% additional first-year depreciation for qualified property acquired after January 19, 2025. Property still has to satisfy the relevant acquisition, placed-in-service, and qualification rules.

Cost segregation often identifies shorter-lived assets or land improvements that may be eligible for accelerated depreciation, including bonus depreciation when the requirements are satisfied. That can make the first-year deduction substantially larger.

But larger does not automatically mean better.

A high-income taxpayer needs to ask:

Will the deduction offset income currently, or will it be suspended?

Is the activity passive, non-passive, or potentially reclassified later?

Does the taxpayer expect higher-value income in a future year?

Is a sale, exchange, refinance, or ownership transfer likely?

Would electing out of bonus depreciation for selected property or classes preserve flexibility?

Are there multiple studies competing for the same tax year?

Does the deduction reduce basis before an exit that is closer than expected?

This is where year-by-year tax preparation and multi-year planning separate.

A preparer may see bonus depreciation and claim what the law allows. A strategist asks whether the current year is the right year to absorb it.

When several properties are involved, the answer may be mixed. One property may deserve full acceleration. Another may be better suited for a later look-back study. A third may justify cost segregation, but not full bonus depreciation. A fourth may not justify the complexity because the hold period is uncertain.

The law creates options. The plan chooses among them.

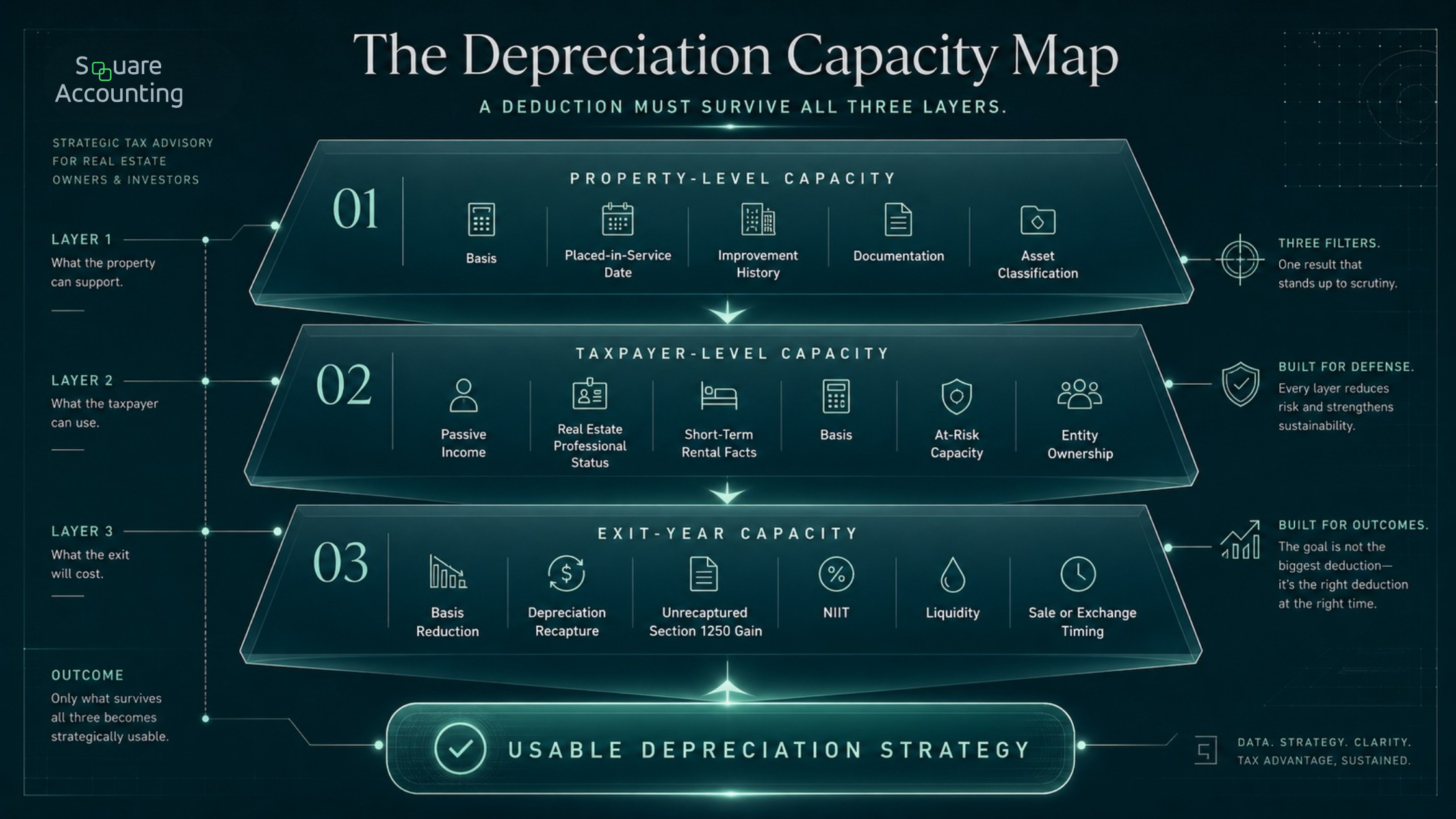

Our depreciation capacity map: the framework weaker planning often misses

Before implementing cost segregation across multiple properties, we build a depreciation capacity map.

The purpose is to determine how much accelerated depreciation the taxpayer can absorb intelligently in each tax year. It is not a spreadsheet created to admire deductions. It is a decision tool that tells us where acceleration belongs and where it may create friction.

The map has three layers.

A large depreciation deduction is only useful when the property, taxpayer, and exit-year consequences can all support it.

1. Property-level capacity

This layer asks what each property can produce.

It includes:

Purchase price allocation between land and depreciable improvements

Building type and use

Placed-in-service date

Acquisition versus construction facts

Renovation and improvement history

Prior depreciation method

Whether the property was already owned

Whether a look-back study may be available

Whether a method change may be required

Whether the study can be defended with adequate documentation

The IRS cost segregation audit guide highlights the importance of properly allocating purchase price between non-depreciable land, building, land improvements, and personal property for acquired or used property. That matters because real estate investors frequently buy assets as lump-sum transactions, then later realize the original depreciation schedule was too broad.

Property-level capacity is not simply “How large is the building?” It is “How much basis can be classified in a supportable way, and how clean is the documentation?”

A smaller property with a strong improvement history and good records may be a better planning candidate than a larger property with poor allocation support or a near-term sale risk.

2. Taxpayer-level capacity

This layer asks whether the taxpayer can actually use the deductions.

For affluent taxpayers, this is often the controlling issue.

The IRS describes passive activities as including trade or business activities in which the taxpayer does not materially participate, and rental activities are generally passive even if the taxpayer materially participates, unless a real estate professional exception applies. Real estate professional treatment requires both the more-than-half personal services test and more than 750 hours of services in real property trades or businesses in which the taxpayer materially participates.

That means the same cost segregation study can have different value for different taxpayers.

A full-time professional with W-2 income and passive rental ownership may generate losses that are suspended. A spouse who qualifies as a real estate professional and materially participates may change the treatment of certain rental losses. A short-term rental operator may fall into a different analysis depending on use, services, and participation. A passive investor may still benefit if they have passive income from other activities.

The issue is not whether the deduction exists. The issue is whether it lands where it can do work.

Taxpayer-level capacity includes:

Current and projected taxable income

Passive income sources

Passive loss carryforwards

Material participation records

Real estate professional status analysis

Short-term rental classification

Basis and at-risk capacity

Capital gain events

Roth conversion or liquidity planning

Business income from pass-through entities

Trust or estate ownership considerations

A deduction that offsets high-rate income currently may have strong value. A deduction that becomes suspended may still be useful later, but it should be modeled differently.

3. Exit-year capacity

This layer asks what the deduction creates later.

Accelerated depreciation lowers basis. Lower basis can increase gain when the property is sold. Depending on asset classification and transaction facts, a sale may involve ordinary income recapture on certain property, unrecaptured Section 1250 gain on real property depreciation, capital gain, NIIT, suspended passive loss release, and liquidity constraints.

The IRS describes unrecaptured Section 1250 gain as the portion of long-term capital gain on Section 1250 real property that is due to depreciation, and IRS Topic 409 notes that the portion of unrecaptured Section 1250 gain from selling Section 1250 real property is taxed at a maximum 25% rate.

For high-income taxpayers, NIIT also needs to be part of the exit model. The NIIT is 3.8% on the lesser of net investment income or the amount by which modified adjusted gross income exceeds the statutory threshold: $250,000 for married filing jointly or qualifying surviving spouse, $125,000 for married filing separately, and $200,000 for single or head of household filers.

This is not a reason to avoid cost segregation. It is a reason to model the unwind.

A good depreciation capacity map should answer:

What deductions are expected by property and year?

Which deductions are currently usable?

Which deductions may become suspended?

Which future years may absorb suspended losses?

Which properties are likely exit candidates?

What gain stack may be created by each exit?

Will NIIT apply in the sale year?

Will a 1031 exchange be realistic, desirable, and structurally possible?

Does the taxpayer need liquidity from the sale, or can capital stay invested?

Does the estate plan change the preferred hold period?

The map prevents a common planning mistake: optimizing Year 1 while ignoring the year the property leaves the portfolio.

See how our depreciation capacity map organizes property-level, taxpayer-level, and exit-year decisions.

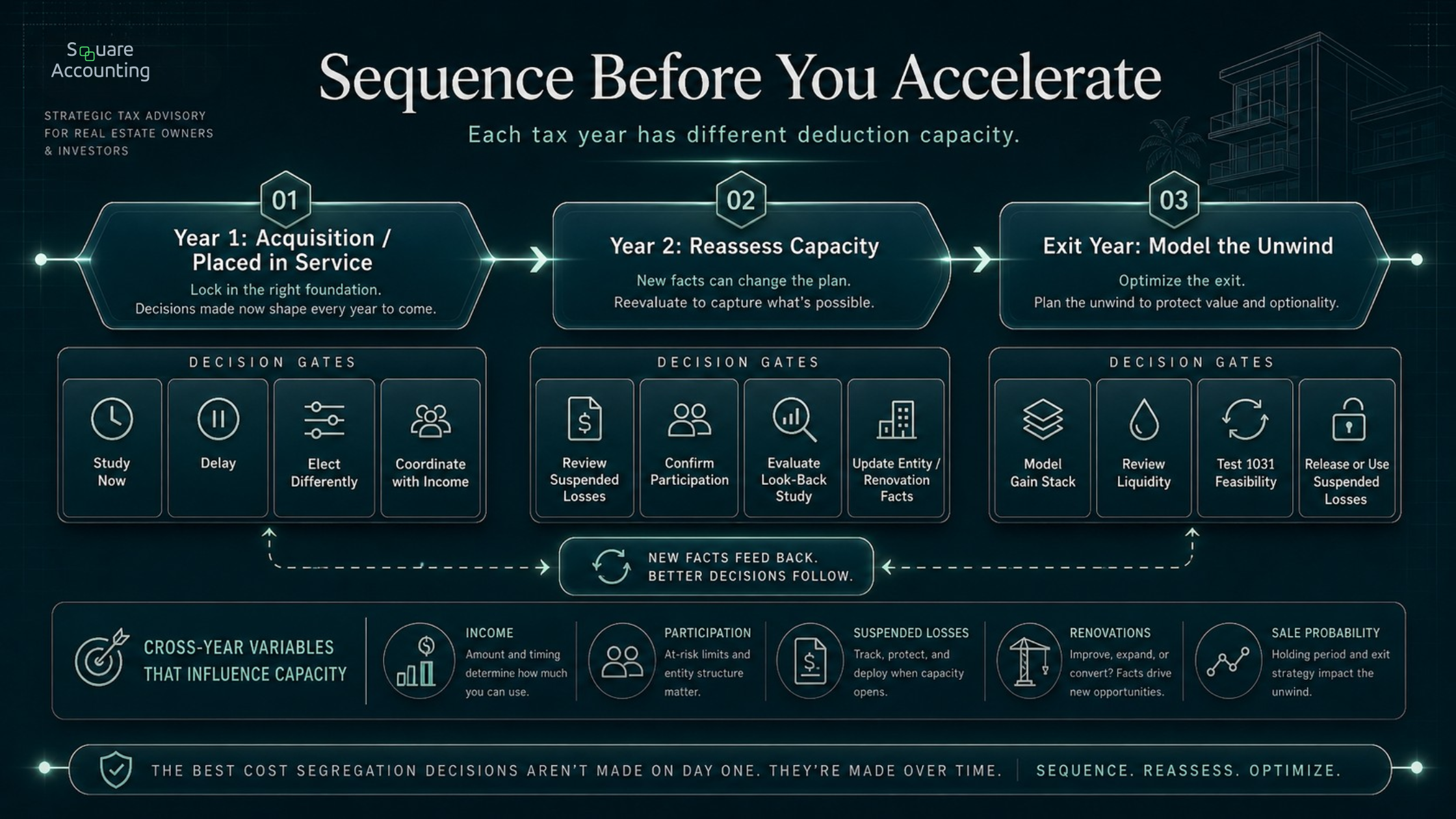

A practical Year 1, Year 2, and exit-year sequence

A strong cost segregation plan has a calendar. It does not begin and end with the study date.

The best depreciation decision may change as income, participation, suspended losses, renovations, and sale probability become clearer.

Year 1: Identify deduction opportunity, but do not rush implementation

In the acquisition or placed-in-service year, the team should identify whether cost segregation is appropriate, estimate the likely depreciation benefit, and compare that benefit against the taxpayer’s current-year tax capacity.

For example, a Florida investor may acquire two short-term rentals and one commercial building in the same year. The default impulse is to study all three and accelerate as much as possible.

That may be correct.

But it may not be.

If the taxpayer expects a higher-income year next year because of a business sale, large bonus, carried interest event, Roth conversion, partnership income spike, or planned disposition, the better answer may be sequencing. One study may be completed now. Another may be delayed. A third may be completed now but paired with a different depreciation election.

Year 1 should produce a decision matrix:

| Decision | Planning Question |

|---|---|

| Study Now | Is there enough current-year income capacity to use the deduction? |

| Study Later | Will a future year produce a better tax result? |

| Look-Back Later | Was an older property depreciated too broadly, and will a catch-up deduction be better timed later? |

| Elect Out or Moderate Acceleration | Would full acceleration create too much basis reduction or suspended loss? |

| Do Not Study | Is the hold period too short or the benefit too uncertain? |

The best Year 1 decision may be action, delay, or selective acceleration.

Year 2: Reassess income classification and suspended loss position

Year 2 is where facts become clearer.

The investor now knows whether the rental activity operated as expected, whether short-term rental participation records are strong, whether real estate professional status was realistic, whether passive losses were suspended, and whether other properties produced passive income.

This is also when renovation plans, insurance costs, financing terms, and cash reserves become more visible.

Year 2 planning should ask:

Did Year 1 depreciation create usable deductions or suspended losses?

Are suspended losses likely to be used soon?

Did the taxpayer’s participation profile improve or weaken?

Did the entity structure support the expected result?

Did renovations create new assets that should be separately analyzed?

Is a look-back study on an older property now attractive?

Has a property moved from long-term hold to possible sale?

This is often the year where the tax plan should be updated, not simply repeated.

A cost segregation strategy that made sense at acquisition may need adjustment after operations reveal the true economics.

Exit year: Model the tax stack before signing the contract

The exit year should not be the first time the taxpayer asks what cost segregation did to basis.

Before a sale, exchange, contribution, installment structure, or ownership transfer, the team should model the tax stack:

Capital gain

Unrecaptured Section 1250 gain

Ordinary income recapture on certain components

NIIT

Suspended passive loss release

Debt payoff and cash available after closing

1031 exchange feasibility

State tax exposure for out-of-state property

Partnership allocation consequences

Estate or gifting alternatives

The key question is not “Will there be recapture?” The better question is “What is the full unwind if we sell in this tax year, and what alternatives exist before the contract fixes the facts?”

For Florida investors, exit timing can be driven by non-tax factors. Insurance renewals, storm risk, reserves, local rental rules, financing resets, and buyer demand can move a property from “long-term hold” to “sell now.” The depreciation plan should be durable enough to handle that possibility.

Where passive activity planning, real estate professional status, and short-term rentals collide

Cost segregation is most valuable when accelerated depreciation can offset income that would otherwise carry a meaningful federal tax cost.

For many investors, the limiting factor is not depreciation law. It is classification.

Passive investor

A passive investor may benefit from cost segregation if the portfolio or household has passive income that can absorb the losses. That passive income may come from other rentals, partnerships, operating businesses in which the taxpayer does not materially participate, or future property dispositions.

But if there is no passive income, accelerated depreciation may increase suspended losses.

Suspended losses are not worthless. They may offset future passive income or may be released in a qualifying disposition. But they are not equivalent to current tax reduction.

For a passive investor, the planning question is:

Do we want to create passive losses now, and do we have a credible path to using them?

If the answer is no, the strategy may still be valid, but it should be framed as future tax inventory, not current cash-flow relief.

Real estate professional

Real estate professional status can materially change the value of cost segregation because qualifying rental real estate losses may avoid passive treatment when the taxpayer also materially participates in the relevant activities.

The requirements are not casual. The IRS requires both a more-than-half personal services test and more than 750 hours of services in qualifying real property trades or businesses in which the taxpayer materially participates.

For high-income households, this is often a spouse-level or business-owner planning question. The taxpayer with the highest income is not always the taxpayer with the best participation profile.

If the cost segregation strategy depends on real estate professional treatment, the plan should address:

Who is expected to qualify?

Which activities are being grouped?

Are the records contemporaneous and specific?

Does the taxpayer materially participate?

Does the ownership structure align with the claimed treatment?

Are there W-2, professional, or business commitments that undermine the time tests?

Will the position still be supportable next year?

A large deduction supported by weak participation facts creates risk. The classification plan has to be built during the year, not after the return is being prepared.

Short-term rental operator

Short-term rentals are common in Florida planning discussions because they can involve different passive activity analysis than traditional long-term rentals. They also create operational facts that matter: average rental periods, services provided, guest turnover, management agreements, and participation.

A short-term rental cost segregation strategy should not start with the depreciation study. It should start with operations.

We want to know:

Who performs the work?

What services are provided?

How often are guests turning over?

What does the management agreement say?

How are hours tracked?

Is the activity owned directly, through a disregarded entity, through a partnership, or through another structure?

Is the goal current loss use, long-term cash flow, or exit flexibility?

Short-term rental classification is not created by calling the property a short-term rental. The facts have to support the intended treatment.

Older properties: when a look-back study can be more valuable than a new acquisition study

Cost segregation is not limited to newly acquired property.

An older property may have been depreciated too broadly for years. If the facts support a different classification, a look-back cost segregation study may identify depreciation that should have been accelerated earlier. Depending on the situation, implementation may involve an accounting method change and a Section 481(a) adjustment.

That can be valuable because it may allow the taxpayer to bring missed depreciation into the current planning year rather than amending multiple prior-year returns.

The key is timing.

A look-back study may be attractive when:

The taxpayer has an unusually high-income year.

Passive income is available to absorb losses.

Real estate professional treatment is supportable.

Short-term rental facts now create better deduction usability.

An older property has significant remaining basis.

The property is expected to be held long enough for the timing benefit to matter.

Records are strong enough to support the reclassification.

The study can be coordinated with repairs, improvements, or partial disposition analysis.

A look-back study may be less attractive when:

The deduction will simply become suspended.

The property is likely to be sold soon.

Documentation is weak.

The taxpayer expects a higher-value year later.

The entity structure may change.

The study creates complexity without a clear use case.

Older properties can be a planning asset. They can also be a distraction if the deduction is not matched to a year that can use it.

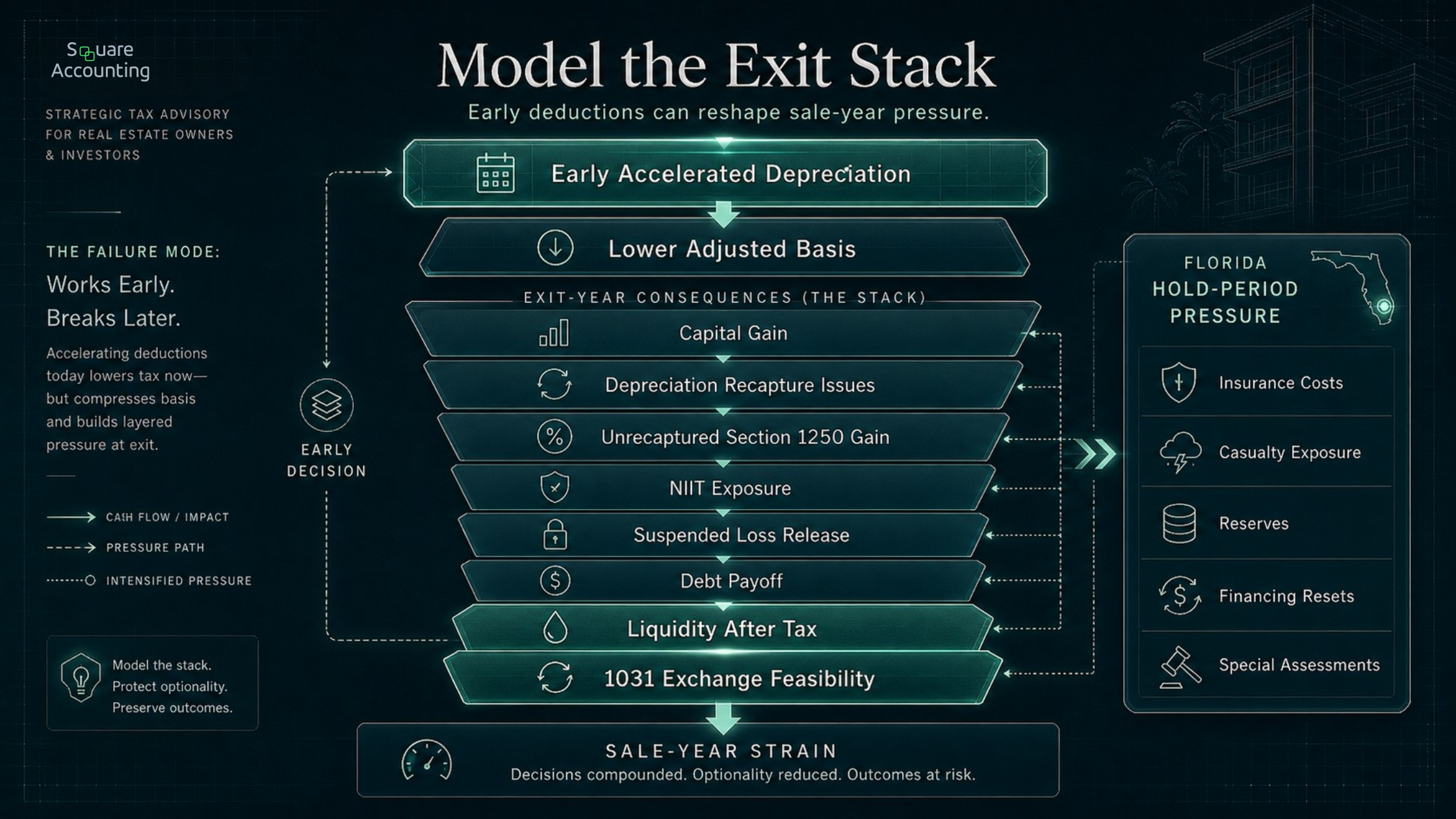

Exit-year pressure: the “works early, breaks later” pattern

The most common weakness in deduction-first cost segregation planning is that it measures the front-end benefit but not the unwind.

The pattern usually looks like this:

The investor acquires multiple properties.

Cost segregation studies generate large early deductions.

Losses offset income or become suspended.

Basis is reduced.

Insurance, debt, market, partnership, or liquidity pressure causes an earlier sale.

The sale year brings gain recognition, depreciation recapture issues, NIIT exposure, and a tight decision window.

The taxpayer discovers that the original plan did not model the exit.

That is the “works early, breaks later” problem.

The exit year shows whether early depreciation created durable value or shifted pressure into a later transaction.

The issue is not that cost segregation failed. The issue is that it was treated as a one-year tactic.

A more durable strategy models at least three exit paths before implementing the study:

| Exit Path | Planning Concern |

|---|---|

| Taxable Sale | Basis reduction, gain character, NIIT, liquidity after tax, and suspended loss release. |

| 1031 Exchange | Replacement property availability, taxpayer identity, debt replacement, timing, and asset classification. |

| Hold or Transfer | Estate planning, basis strategy, cash flow durability, and whether accelerated depreciation still fits the long-term plan. |

For Florida investors, this modeling should include a stress case. What happens if the property is sold earlier because insurance costs rise, a storm causes disruption, reserves become inadequate, financing resets, or local economics change?

A cost segregation strategy that only works under the original hold-period assumption is fragile.

We can review how cost segregation may interact with basis, recapture, NIIT, liquidity, and a future sale or exchange.

Entity structure can either preserve flexibility or trap the plan

Cost segregation deductions do not float freely around a household. They belong to a taxpayer, entity, and activity.

That makes entity structure central.

A single-member LLC may be simple and administratively efficient, but it may not provide the same allocation flexibility as a partnership. A partnership may allow special allocations, but those allocations must be supported by the governing documents, capital accounts, economic arrangement, and tax rules. An S corporation may create basis and distribution constraints. A trust-owned property may raise different NIIT, distribution, and estate planning questions. A property owned by one entity may not easily share deductions with income generated elsewhere.

This is where sophisticated taxpayers often discover a structural problem too late.

The cost segregation study may be right, but the ownership structure may be wrong for the intended use.

Before the study is implemented, the planning team should confirm:

Which taxpayer owns the property for tax purposes?

Which return will report the depreciation?

Does the owner have basis and at-risk capacity?

Is debt allocated in a way that supports the intended deduction?

Are losses passive or non-passive to the owner?

Will allocations among partners be respected?

Does the structure preserve 1031 exchange flexibility?

Could a future sale, gift, estate transfer, or recapitalization be complicated by the current ownership design?

Entity planning should happen before the depreciation decision, not after it.

Florida-specific planning considerations

Florida context should sharpen the planning. It should not be decorative.

For Florida taxpayers, the main question is how federal tax strategy interacts with real estate-heavy portfolios, liquidity risk, property tax economics, and shorter-than-expected hold periods.

Federal planning carries more weight

Because Florida does not impose a personal income tax, the planning conversation often moves quickly to federal tax character and timing. The Florida Department of Revenue confirms that Florida does not impose personal income tax.

That means a cost segregation decision should be coordinated with federal issues such as:

Passive activity limitations

Real estate professional status

Short-term rental classification

NIIT

Capital gains

Depreciation recapture

Unrecaptured Section 1250 gain

Basis planning

1031 exchange strategy

Estate and gift planning

Partnership allocations

The absence of state personal income tax does not make cost segregation less valuable. It makes the federal plan more central.

Homestead and non-homestead economics can influence hold/sell decisions

Cost segregation usually applies to income-producing property, not a personal residence. Still, Florida homestead economics can affect the broader portfolio decision.

The Florida Department of Revenue explains that a Florida homestead exemption may reduce taxable value by as much as $50,000 and qualifies the home for the Save Our Homes assessment limitation; the Department also notes that some or all of the assessment difference may be portable to a new Florida homestead.

This matters because a Florida taxpayer may be deciding among several moves:

Keep a homestead and buy additional rental property.

Convert a former residence to rental use.

Sell a non-homestead investment property.

Move from one Florida homestead to another.

Rebalance capital between personal and rental real estate.

Hold a rental property because non-tax economics remain attractive.

Sell a rental property because insurance, assessments, or reserves changed the risk profile.

Cost segregation does not determine those choices. But those choices determine whether the expected hold period still supports the cost segregation strategy.

Insurance and casualty risks affect the durability of the plan

A depreciation strategy assumes the property remains in the plan long enough for the time-value benefit to matter.

In Florida, that assumption deserves scrutiny.

Insurance premiums, deductibles, storm exposure, reserve requirements, lender demands, association assessments, and casualty disruptions can change cash flow and liquidity. They can also change the investor’s willingness to hold.

That creates a tax planning issue. If the cost segregation model assumes a long hold, but the property is financially fragile, the plan may be over-accelerating deductions before an early exit.

We do not treat insurance and casualty risk as separate from tax planning. They influence timing, liquidity, debt service, reserve policy, and exit probability. Those variables determine whether accelerated depreciation is being placed into a durable strategy.

Short-term rental markets require operational discipline

Florida short-term rentals can create strong revenue opportunities, but the tax treatment depends on facts.

A cost segregation strategy built around short-term rentals should coordinate:

Local and platform-level operating facts

Management agreements

Average rental periods

Guest services

Participation records

Ownership structure

Financing and reserves

Exit options

Passive or non-passive treatment

The tax result should follow the operations. If the operations do not support the intended classification, the depreciation plan may be too aggressive for the facts.

Common misuses and oversights sophisticated taxpayers still make

1. Ordering studies on every property without ranking deduction value

Not every property should be studied immediately.

The better process ranks properties by strategic value:

Basis available for reclassification

Documentation quality

Current income absorption

Passive or non-passive treatment

Expected hold period

Sale or exchange likelihood

Entity ownership

Basis and at-risk capacity

Renovation history

Florida-specific cash-flow risks

Potential interaction with other properties

The first study should not automatically be the newest acquisition or the largest building. It should be the property whose deductions can be used most intelligently.

2. Ignoring suspended passive losses

A large passive loss may look useful, but if it is suspended, it does not produce the same current-year value as a deduction that offsets income now.

Suspended passive losses may still be valuable. They may offset future passive income or be released in a qualifying disposition. But that is a different planning profile.

The oversight is treating all depreciation as equal.

It is not equal if one deduction reduces current tax and another waits for a future event.

3. Treating real estate professional status as a checkbox

Real estate professional status is not a label. It is an annual factual position supported by time, activity, material participation, and records.

If the cost segregation plan depends on real estate professional treatment, the planning must address the hours, the activities, the grouping approach, the taxpayer performing the work, and the documentation standard.

This is especially important for high-income professionals and business owners. A taxpayer who earns substantial income outside real estate may face a more difficult more-than-half personal services analysis than they expect.

4. Forgetting the exit-year tax stack

A deduction is only one side of the plan.

The exit year may include capital gain, unrecaptured Section 1250 gain, ordinary income recapture on certain components, NIIT, suspended passive loss release, and debt-related liquidity issues.

The taxpayer may still come out ahead. But that conclusion should come from modeling, not from assuming early deductions always dominate later costs.

5. Using rule-of-thumb allocations

Cost segregation should be supportable.

The IRS cost segregation audit guide emphasizes quality, documentation, and proper allocation methods. For acquired or used real property, the guide specifically notes that studies should properly allocate purchase price among non-depreciable land, building, and personal property based on value at the date of purchase.

For sophisticated investors, weak allocations are not worth the friction. A defensible study is part of the strategy.

6. Missing repairs, improvements, and partial disposition planning

Cost segregation should be coordinated with tangible property rules, repair versus capitalization analysis, improvement planning, and partial disposition opportunities.

The IRS tangible property regulations apply to taxpayers who acquire, produce, or improve tangible real or personal property, including individuals, partnerships, corporations, S corporations, and LLCs filing business or rental schedules. The IRS also describes the regulations as providing a framework for distinguishing deductible repairs from capital improvements.

This matters during renovation years.

A property may have:

New capitalized improvements

Deductible repairs

Retired components

Partial asset disposition questions

New assets eligible for shorter recovery

Placed-in-service timing issues

Documentation requirements

A cost segregation study that ignores the improvement history may miss planning value or create avoidable classification problems.

7. Coordinating too late

Cost segregation is often discussed near year-end or after the return is already being prepared.

That is late.

By then, participation hours are mostly fixed, income is largely known, acquisition documents are closed, entity structure is set, renovations may be complete, and sale decisions may already be underway.

Better planning starts before acquisition, before renovation, before placing the property in service, and before a major exit year.

The earlier the planning starts, the more levers remain available.

How to decide which property should be studied first

A useful ranking process starts with five questions.

1. Which property has the strongest deduction potential?

This includes depreciable basis, land allocation, asset mix, improvement history, placed-in-service timing, and documentation quality.

A high-value building with poor records may be less attractive than a smaller property with clean acquisition documents and clear improvement detail.

2. Which taxpayer or entity owns the deduction?

The deduction has to land where it can be used.

A study inside the wrong entity may create less value than a smaller study in an entity with better income absorption, basis, or participation facts.

3. Which year has the highest absorption capacity?

The strongest year may involve high ordinary income, passive income, capital gains, non-passive rental treatment, or a planned liquidity event.

A deduction in the wrong year can become suspended or underused.

4. Which property is least likely to be sold soon?

The shorter the expected hold period, the more carefully the exit-year unwind should be modeled.

A property with uncertain insurance, financing, or market durability may not be the best first candidate for aggressive acceleration.

5. Which study can be defended cleanly?

Technical support matters.

A study with strong records, qualified analysis, and clear allocations is more useful than an aggressive estimate that creates audit friction.

When the best answer may be “not yet”

Not every cost segregation opportunity should be used immediately.

“Not yet” may be the right answer when:

The taxpayer has no current path to using passive losses.

The property may be sold soon.

A higher-income year is expected.

The entity structure is likely to change.

A spouse may qualify as a real estate professional next year but not this year.

Short-term rental operations are not yet mature enough to support the intended classification.

Renovations may materially change the asset mix.

Full bonus depreciation would create excessive basis reduction before a likely exit.

A look-back study would be better used in a later year.

The expected hold period is too uncertain.

This is not hesitation. It is sequencing.

The best plan may involve studying one property now, delaying another, using a look-back method later, preserving flexibility through elections where available, and modeling the exit before the deduction is claimed.

Cost segregation is most valuable when it supports the asset strategy. It is less useful when it forces the tax plan to chase a deduction that the portfolio cannot absorb cleanly.

Start a focused review of your real estate portfolio, depreciation timing, passive loss position, and exit assumptions.

Cost Segregation Planning Questions Florida Real Estate Investors Should Ask

Cost segregation is not a one-size-fits-all depreciation strategy. For Florida real estate investors, the value often depends less on whether a study is technically available and more on whether the timing, income profile, entity structure, and exit plan support the deduction.

Before moving forward, investors should evaluate how cost segregation fits into the broader portfolio plan.

Can cost segregation be done on multiple properties in the same year?

Yes. Multiple cost segregation studies can be completed in the same tax year.

However, that does not mean every study should be implemented the same way or at the same time. The better question is whether the taxpayer can actually use the accelerated deductions currently.

For example, a portfolio owner may have several qualifying properties, but the tax result can vary depending on:

Current-year income capacity

Passive activity loss limitations

Real estate professional status

Entity ownership structure

Suspended loss carryforwards

Expected hold period

Future sale or exchange plans

In some cases, completing several studies in one year may create a strong current-year benefit. In others, phasing studies across multiple tax years may produce a more efficient result by matching deductions to income more carefully.

The planning should not stop at “How much depreciation can we accelerate?” It should also ask, “When will the deduction create the best tax result?”

Is cost segregation still useful if the property has been owned for several years?

Often, yes.

A property does not always need to be newly purchased for cost segregation to be relevant. If a property has been depreciated too broadly in prior years, a look-back cost segregation study may allow the owner to correct depreciation classification and capture missed deductions.

This can be especially important for investors who purchased property years ago but never reviewed whether components should have been separated into shorter-life asset classes.

The value of a look-back study depends on several factors, including:

Remaining depreciable basis

Quality of purchase and improvement documentation

Prior depreciation method

Current-year tax capacity

Passive loss limitations

Whether the property is expected to be held long enough for the timing benefit to matter

A look-back analysis can be valuable, but it should be modeled carefully. The goal is not simply to create a larger deduction. The goal is to determine whether the catch-up depreciation improves the investor’s multi-year tax position.

Should every Florida rental property get a cost segregation study?

No.

Cost segregation can be a powerful planning tool, but not every Florida rental property is a strong candidate. The decision depends on the property, the taxpayer, and the long-term plan.

A study may be worth considering when the property has enough depreciable basis, the investor can use the deductions efficiently, and the expected hold period supports the strategy.

It may be less attractive when the property has a short expected hold period, limited basis, minimal income absorption, or a likely exit that could reduce the benefit of accelerated depreciation.

Important planning variables include:

Property type

Building basis

Improvement history

Passive or non-passive treatment

Investor income profile

Entity structure

Debt and liquidity position

Sale, refinance, or 1031 exchange plans

Florida’s lack of personal income tax makes federal tax planning especially important. But it does not make every study worthwhile. The analysis should focus on whether cost segregation supports the investor’s broader tax and portfolio strategy.

How does cost segregation interact with a 1031 exchange?

Cost segregation can affect the tax modeling around a future 1031 exchange.

A 1031 exchange may defer gain, but it does not eliminate the need to understand basis, depreciation history, gain character, debt replacement, taxpayer identity, and replacement property timing.

When cost segregation is used before an exchange, the investor should understand how accelerated depreciation may affect:

Adjusted basis

Future gain exposure

Depreciation recapture considerations

Replacement property planning

Debt replacement requirements

Portfolio flexibility after the exchange

The exchange may still be beneficial, but the planning should be coordinated. Cost segregation should not be reviewed in isolation from the investor’s expected exit path.

For Florida real estate investors building long-term portfolios, the better question is not only whether the current property qualifies. It is whether the depreciation strategy still works when the property is sold, exchanged, refinanced, or transferred.

Does Florida’s lack of state income tax make cost segregation less valuable?

Not necessarily.

Florida’s no-personal-income-tax environment changes the focus of the analysis. Since Florida does not impose a personal income tax, the value of cost segregation is usually driven primarily by federal tax outcomes.

Those outcomes may include:

Current deduction use

Passive loss treatment

Real estate professional status

Net investment income tax exposure

Capital gain planning

Depreciation recapture

Basis management

Exit-year liquidity

For some investors, the absence of state income tax may reduce one layer of potential tax benefit. For others, federal planning remains significant enough that cost segregation can still be a meaningful part of the strategy.

The key is modeling the federal impact across multiple years, not just the first-year deduction. A strong cost segregation strategy should account for how the deduction works during the hold period and how it may affect the eventual exit.

Conclusion: cost segregation should be part of a coordinated multi-year tax plan

Coordinating cost segregation across multiple properties and tax years is not about maximizing depreciation in isolation. It is about placing deductions where they improve the taxpayer’s multi-year result.

For high-income Florida real estate investors, that means integrating the study with passive activity rules, real estate professional status, short-term rental operations, bonus depreciation, entity structure, basis, NIIT, depreciation recapture, unrecaptured Section 1250 gain, liquidity, and exit planning.

The strongest plan often uses sequencing rather than speed.

One property may deserve an immediate study. Another may be better suited for a look-back analysis. A third may warrant cost segregation but not full acceleration. A fourth may be a poor candidate because the exit risk is too high.

The goal is not to turn every property into a current-year deduction. The goal is to build a depreciation strategy that still makes sense when the property is refinanced, renovated, restructured, sold, exchanged, gifted, or held long term.

That is the difference between reactive tax work and coordinated multi-year planning.

Bring your current properties, entities, and expected holding periods into a coordinated multi-year tax planning conversation.

Cost Segregation Planning FAQs

Key questions for real estate investors evaluating accelerated depreciation, loss usability, entity ownership, and exit-year planning.

How should investors prioritize cost segregation studies across a real estate portfolio?

We would not start by ranking properties only by size or purchase price. A better prioritization looks at which property has supportable basis reclassification, which taxpayer or entity owns the deduction, whether the loss can be used currently, and whether the expected hold period supports acceleration. A smaller property with strong documentation, usable losses, and a stable hold period may deserve priority over a larger property that is likely to be sold soon or owned through an entity that limits deduction value.

What makes accelerated depreciation valuable in the year it is claimed?

Accelerated depreciation is most valuable when it offsets income the taxpayer can actually reduce in that year. That requires more than a cost segregation study. We would look at passive activity treatment, real estate professional status, short-term rental facts, basis, at-risk capacity, entity ownership, and projected income. A deduction that becomes suspended may still have future value, but it is not the same as a deduction that reduces current taxable income. The planning question is whether the tax year has enough capacity to absorb the depreciation intelligently.

Can suspended passive losses still be part of a good cost segregation plan?

Yes, but they need to be treated as future tax inventory rather than immediate tax relief. Suspended passive losses may become useful if the taxpayer later has passive income, sells an activity in a qualifying disposition, or changes the structure or participation profile in a way that improves usability. The mistake is assuming that a large depreciation number automatically creates current value. We would want to know when, how, and against what future income those suspended losses are expected to be used.

What should be modeled before using cost segregation on a property that may be sold?

Before accelerating depreciation on a possible sale candidate, we would model the exit-year stack. That includes basis reduction, capital gain, depreciation recapture issues, unrecaptured Section 1250 gain, NIIT exposure, suspended passive loss release, debt payoff, and liquidity after tax. The key issue is not whether cost segregation is technically available. It is whether the time-value benefit of the deduction survives a shorter hold period. A strategy that works under a long-hold assumption may look very different if the property is sold earlier.

How should Florida short-term rental owners approach cost segregation differently?

For Florida short-term rental owners, the depreciation study should follow the operating facts, not lead them. We would first evaluate who performs the work, what services are provided, how management agreements are structured, how participation is tracked, and whether the intended tax treatment is supportable. Short-term rentals can create planning opportunities, but classification depends on facts. If the goal is to use accelerated depreciation currently, the participation and operational records need to support that position before the deduction strategy is built around it.

Why does entity ownership matter when coordinating cost segregation?

Cost segregation deductions belong to a taxpayer, entity, and activity. They do not automatically offset income elsewhere in the household. We would review which entity owns the property, which return reports the depreciation, whether the owner has basis and at-risk capacity, how debt is allocated, and whether losses are passive or non-passive to that owner. A technically sound study can still create limited value if the deduction lands in the wrong structure or cannot be matched with the income it was expected to offset.

What Florida-specific issues should be considered before accelerating depreciation?

Florida’s lack of personal income tax makes the federal planning result especially important, but property-level economics still matter. We would consider insurance costs, casualty exposure, reserves, association assessments, financing pressure, and whether those factors could shorten the expected hold period. Homestead and non-homestead economics may also influence broader hold/sell decisions, especially when capital is being reallocated between personal and investment real estate. Cost segregation should be coordinated with those realities because a depreciation plan depends heavily on how long the property remains in the portfolio.

When might delaying a cost segregation study be the better planning decision?

Delay may make sense when the taxpayer cannot currently use passive losses, expects a higher-income year, may restructure ownership, is still developing participation facts, or may sell the property soon. It may also be appropriate when renovations will materially change the asset mix or when full acceleration would reduce basis before a likely exit. We do not view delay as inaction. In a multi-property portfolio, timing is part of the strategy. The better result may come from sequencing studies across tax years rather than accelerating everything immediately.