What Should I Look for in a Tax Advisor for My Real Estate Business?

Look for a credentialed advisor who understands your specific real estate business, becomes involved before major decisions are finalized, and can explain how a recommendation affects both the current return and the eventual exit.

That sounds straightforward. In practice, many investors evaluate advisors by credentials, responsiveness, or familiarity with cost segregation and 1031 exchanges. Those factors matter, but they do not establish whether the advisor can connect classification, loss usability, basis, depreciation, cash flow, ownership, documentation, and exit planning across several years.

If you already have a CPA, the question is not simply whether your returns are accurate. It is whether the relationship helps you make better tax-sensitive decisions while you still have meaningful choices.

Advisor selection becomes more useful when credentials, multi-year analysis and implementation are evaluated as one connected planning system.

“An advisor’s credential is only the entry point. We would also evaluate whether the engagement can carry each decision through current usability, implementation, tax-attribute maintenance and eventual exit.”

Key takeaways

Key takeaway: The strongest real estate tax advisor is not necessarily the person who can name the most strategies. It is the advisor who can determine which strategy fits, when it should be evaluated, whether the benefit is currently usable, and what it may create later.

Verify credentials, assigned responsibilities, and experience with a real estate model comparable to yours.

Test material recommendations across classification, current usability, cash-flow timing, exit consequences, and documentation.

Require defined decision triggers, written deliverables, implementation ownership, and post-filing tax-attribute updates.

For Florida portfolios, distinguish federal planning from Florida, local, and multistate obligations.

Use our Investment Tax Assessment to evaluate whether your current relationship covers classification, current usability, multi-year timing, and exit planning.

A three-part framework for evaluating a real estate tax advisor

We recommend evaluating the advisor across three levels:

Professional standing: Are the credentials, license status, representation rights, and assigned responsibilities clear?

Planning depth: Can the advisor connect a strategy to your facts, current tax attributes, cash flow, and expected exit?

Delivery discipline: Does the engagement identify decision triggers, deliverables, implementation owners, response standards, and follow-through?

The following framework can be used during an initial consultation or to evaluate an existing advisory relationship.

How to Evaluate a Real Estate Tax Advisory Firm

Use these questions to evaluate whether a firm offers verifiable accountability, relevant real estate depth, multi-year planning judgment, implementation ownership, and secure service standards.

| What to Evaluate | What to Ask | What a Strong Answer Should Show | Warning Sign |

|---|---|---|---|

| Credentials and Accountability | Who advises me, who reviews the work, who signs the returns, and who can represent me if an issue arises? | Verifiable credentials, assigned roles, reviewer involvement, and a defined notice or examination process. | The firm’s credentials are clear, but responsibility for your work is not. |

| Relevant Real Estate Depth | Which client, property, and transaction profiles are most comparable to mine? | Fluency in your operating model, ownership, income sources, participation, financing, and likely exits. | All real estate is discussed as though it were the same rental activity. |

| Planning-Chain Analysis | How do you determine whether a strategy creates a benefit I can actually use? | Analysis of classification, basis, at-risk exposure, passive limitations, income timing, and supporting records. | The answer focuses on the gross deduction or projected savings alone. |

| Multi-Year and Exit Modeling | How will today’s recommendation affect later income years and a sale, exchange, gift, transfer, or change in use? | Alternative scenarios, tax-attribute changes, liquidity needs, and an explicit exit review. | Depreciation or deferral is discussed without its later consequences. |

| Decision-Window Coverage | Which events should reach you before documents are signed or a transaction closes? | A trigger list covering acquisitions, ownership, improvements, financing, income changes, and exits. | Planning begins after the economic or legal terms are already fixed. |

| Execution and Coordination | What will your team deliver, and who is responsible for each next step? | Written decisions, action items, deadlines, evidence standards, and coordination with other professionals. | Recommendations remain verbal or implementation has no clear owner. |

| Service and Security | What are your response standards, review process, capacity controls, and data safeguards? | Clear communication expectations, secure systems, continuity, and transparent scope. | Sensitive records are handled casually or service expectations remain undefined. |

We would not reduce the decision to a simple score. A serious weakness in timing, loss usability, or implementation can outweigh several strengths elsewhere.

Start with credentials, but do not stop there

Credentials establish a professional baseline. They do not establish real estate specialization or strategic judgment.

The IRS currently distinguishes among preparers partly through their representation rights. Enrolled agents, CPAs, and attorneys have unlimited representation rights before the IRS, while other preparers may have more limited authority. The IRS also maintains a directory of preparers with credentials and select qualifications.

If someone presents as a Florida CPA, verify that the license is current and review available disciplinary information through the Florida Department of Business and Professional Regulation. For a professional licensed elsewhere, use the appropriate state licensing authority.

Then move beyond the credential. Ask:

Who will lead the planning relationship?

Who will prepare and review the returns?

Who maintains the property-level tax attributes?

Who responds when a transaction or IRS notice arises?

Will the same team remain involved after filing?

A CPA may have strong accounting depth but little exposure to complex real estate. An enrolled agent may have substantial federal real estate experience. A tax attorney may be important when legal documents, disputes, or estate structures are involved but may not provide ongoing accounting, projections, or return integration.

The right structure may therefore involve a lead tax advisor who owns the planning and compliance process while coordinating with legal counsel and other specialists. The credential matters. The operating role matters more.

Confirm that “real estate experience” matches your business model

“We work with real estate clients” is not specific enough.

A long-term rental portfolio, short-term rental operation, development company, fix-and-flip business, brokerage, property-management company, and syndication can present different questions involving income character, activity classification, payroll, accounting, ownership, state filings, and exit treatment.

A high-income physician or consultant with several rentals also presents a different planning problem from a full-time operator managing properties through multiple partnerships.

One revealing question is:

Before recommending a strategy, how would you classify each part of my real estate operation, and which facts could change that classification?

A strong advisor should ask about:

how each property is used;

why it was acquired and how long it may be held;

which services are provided to occupants or customers;

who performs the work and how participation is documented;

how ownership, debt, and partner economics are structured;

whether related operating businesses exist;

which exit paths are realistically under consideration.

The advisor should not infer the federal tax result from an LLC name. Depending on ownership and elections, an LLC may be treated for federal tax purposes as a disregarded entity, partnership, or corporation. The IRS LLC guidance explains those classifications.

Holding purpose matters as well. Current federal like-kind exchange rules generally apply to qualifying real property held for business or investment, subject to their requirements, while property held primarily for sale is excluded. An advisor who starts discussing a 1031 exchange before understanding whether the property is an investment, rental, development project, or dealer property is starting with the tactic instead of the controlling facts.

The same concern applies when an advisor recommends an entity election or cost segregation study immediately after hearing “real estate business.” The recommendation may ultimately fit. The missing step is the analysis that earns the conclusion.

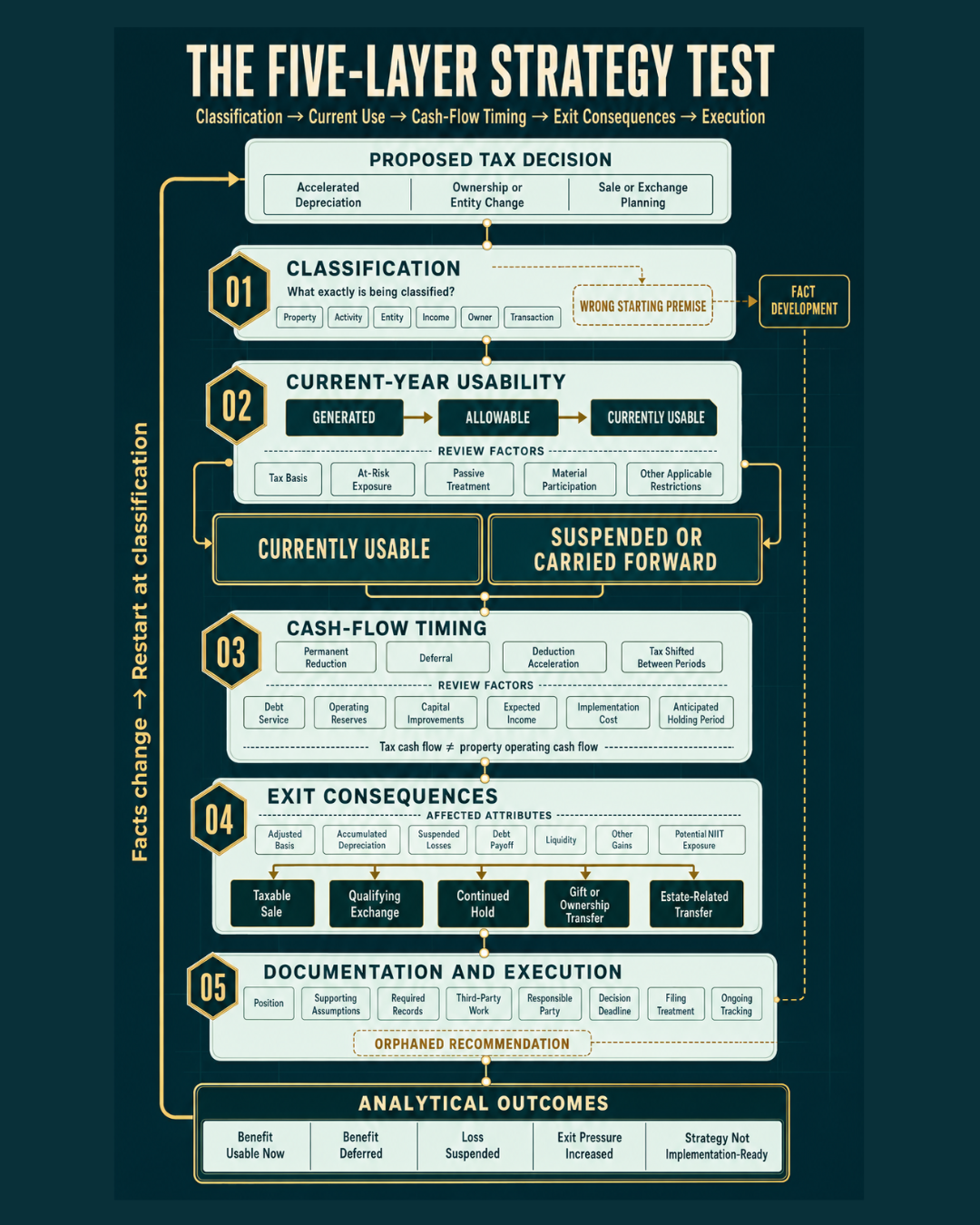

Use the five-layer strategy test

To test planning depth, ask the advisor to take one proposed strategy—accelerated depreciation, an ownership change, real estate professional treatment, or a planned exchange—and walk it through five layers.

A projected deduction becomes decision-ready only after its usability, timing, future attributes, exit consequences and implementation requirements are understood.

“Before focusing on the size of a projected benefit, we would ask the advisor to trace the recommendation through the complete decision chain. A weakness at any layer can change when the benefit is usable, how it affects cash flow or what pressure appears later.”

1. Classification

What is being classified: the property, activity, entity, income, owner, or transaction?

Who owns the asset? Who performs the work? How is the property used? Is it being held for investment, operated as a rental, or held for another purpose? Which facts would cause the analysis to change?

If the advisor cannot define the classification question, the rest of the recommendation may be built on the wrong foundation.

2. Current-year usability

If the strategy creates a deduction or loss, the next question is whether it can be used now.

That analysis may involve several gates, including tax basis, at-risk limitations, passive-activity treatment, material participation, and other restrictions. Under the framework described in IRS Publication 925, the at-risk and passive-activity rules can limit losses from rental, business, and other income-producing activities.

A strong advisor should be able to distinguish among three different outcomes:

a deduction was generated;

the deduction is allowable under the applicable rules;

the deduction produces a currently usable benefit on this taxpayer’s return.

A technically valid depreciation deduction may be suspended rather than currently usable. That may still have future value, but it changes the timing, cash-flow benefit, carrying cost, and documentation needed to evaluate the strategy.

The advisor should be able to show which limitation is controlling, what tax attribute carries forward, and which future events might change the result. “The deduction is available” is not a complete answer.

3. Cash-flow timing

Ask whether the recommendation is expected to reduce tax permanently, defer recognition, accelerate a deduction, or shift cash taxes from one period to another.

Then connect the timing to the investor’s real economics:

debt service and lender requirements;

operating reserves and capital improvements;

expected business or professional income;

future acquisitions or partner distributions;

implementation costs;

the likelihood that the property will be held long enough for the strategy to remain useful.

This is where a tax advisor should separate tax savings from tax deferral and improved tax cash flow from improved operating cash flow. Those outcomes can support different decisions.

4. Exit consequences

A current-year strategy should be modeled through more than one exit path.

What happens if the property is sold earlier than expected? What if the investor completes a qualifying exchange, changes the property’s use, gifts an interest, transfers ownership through an estate plan, or continues holding the asset?

Depending on the facts, the exit analysis may need to account for:

adjusted basis and accumulated depreciation;

suspended losses and other carryforwards;

debt payoff and available liquidity;

selling costs and other gains recognized in the same period;

potential depreciation-related gain treatment;

potential net investment income tax exposure;

the requirements and basis consequences of a like-kind exchange.

The IRS explains that a qualifying like-kind exchange can postpone recognition of gain when its requirements are met. Postponement does not make the property’s tax history disappear. The current transaction should be connected to replacement-property basis, liquidity, and the next likely exit.

The goal is not to predict one future with false precision. It is to understand how the recommendation behaves if the investor’s holding period, income, financing, or exit plan changes.

5. Documentation and execution

The final layer is practical: what has to be completed, by whom, and by when?

Depending on the strategy, support may include elections, studies, agreements, participation records, appraisals, closing statements, depreciation schedules, basis workpapers, or written tax analysis.

A complete recommendation should identify:

the position being considered;

the facts and assumptions supporting it;

the required records or third-party work;

the implementation owner;

the decision and filing deadlines;

how the position will be reflected and tracked after filing.

This prevents an otherwise sound strategy from becoming an orphaned recommendation—discussed in a meeting, partially implemented, and difficult to reconstruct later.

The five-layer test is more revealing than asking whether the advisor “does” cost segregation, real estate professional status, or 1031 exchanges. Familiarity shows exposure. The five layers reveal judgment.

We can review a proposed real estate tax decision across current usability, cash-flow timing, documentation, and plausible exit paths.

Test the process before testing the tactics

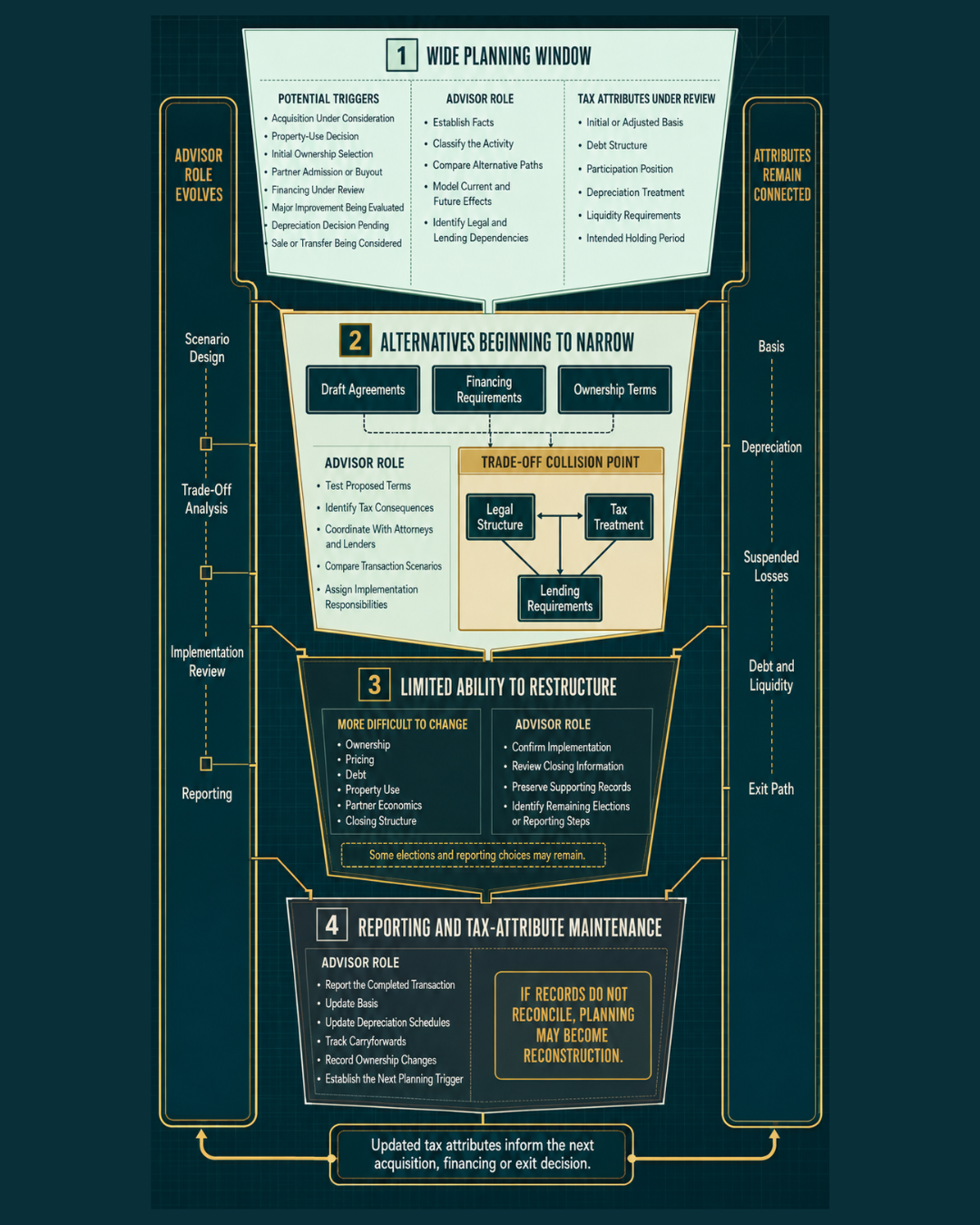

Real estate planning often loses value when the advisor first learns about a transaction after the economic and legal terms are fixed.

The better question is not, “How many meetings are included?” It is, “Which events trigger a planning review, and how early do you need to know?”

Common decision triggers may include:

entering an acquisition or sale process;

selecting or changing ownership;

admitting, buying out, or transferring an interest to a partner;

placing property in service or changing its use;

approving substantial improvements;

changing financing or making a significant distribution;

considering accelerated depreciation;

evaluating a taxable sale, exchange, gift, or estate transfer;

experiencing a significant change in business or professional income.

Early involvement allows the advisor to compare credible alternatives; later involvement may shift the work toward implementation, reporting or reconstruction.

“We would not expect every event to receive the same level of analysis. The planning system should distinguish decisions that may preserve meaningful alternatives from events that primarily require implementation, reporting and tax-attribute updates.”

Not every event requires a lengthy analysis, and not every tax decision must be completed before closing. The advisor should know which facts are time-sensitive and establish a trigger early enough to preserve realistic alternatives.

Ask the firm to describe its normal planning cycle. A credible process should connect:

prior-return and tax-attribute review;

current-year income and cash-flow projections;

transaction-triggered analysis;

year-end implementation and documentation;

return preparation and review;

post-filing updates to basis, depreciation, carryforwards, and the next planning calendar.

This is what separates a proactive CPA relationship from periodic access to a preparer.

Make sure the advisor can integrate real estate with the rest of your tax picture

For a high-income business owner or professional, the real estate return cannot be planned in isolation.

The advisor should understand how the portfolio interacts with business entities, owner compensation, retirement contributions, estimated payments, capital events, charitable planning, and family wealth transfers. That does not mean every strategy should be combined. It means the interactions should be evaluated before anyone assumes that a real estate deduction will offset another category of income.

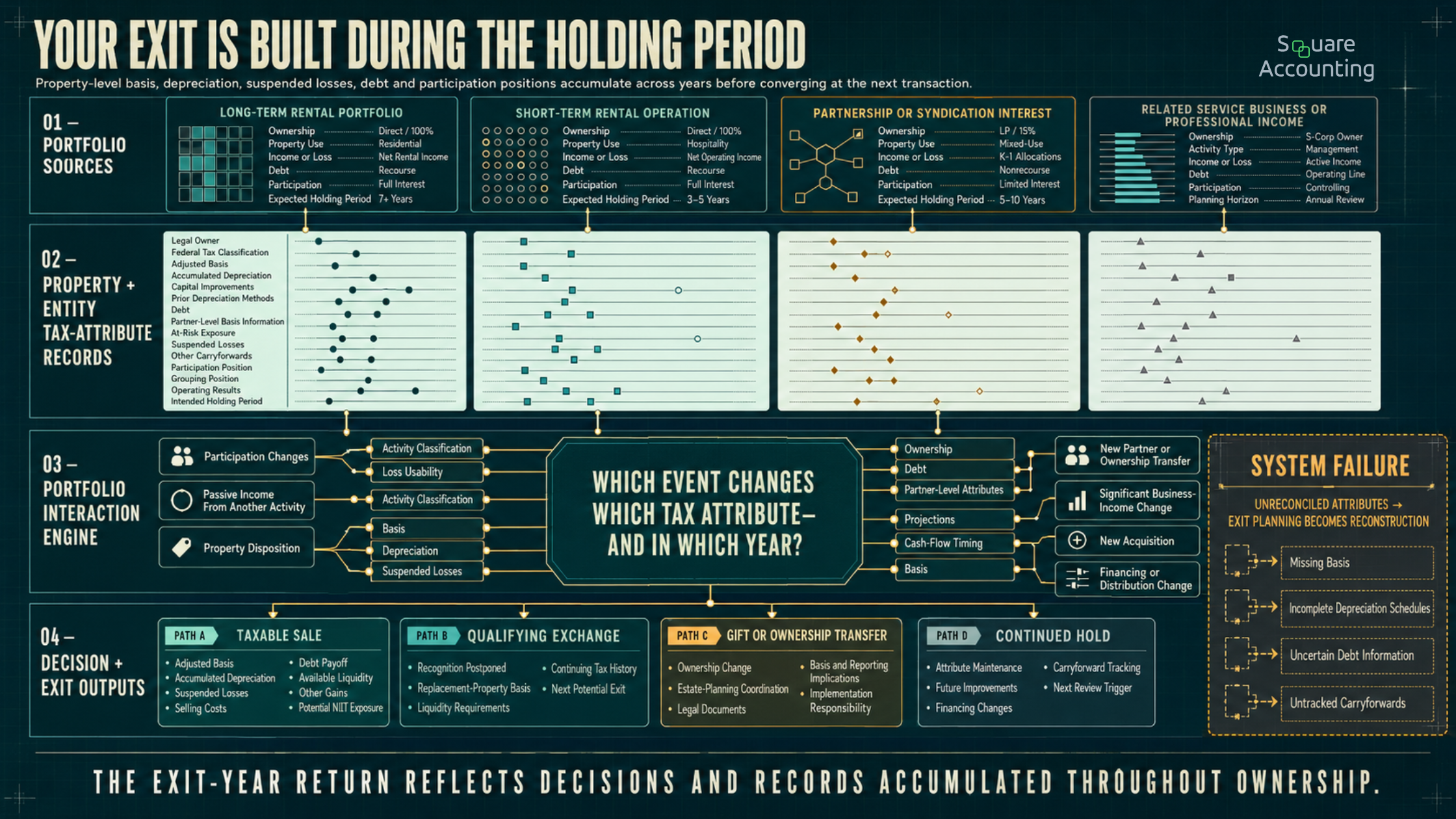

The same principle applies across the portfolio. Property-level planning should roll into a tax-attribute map that tracks, where relevant:

legal ownership and federal tax classification;

adjusted basis and accumulated depreciation;

capital improvements and prior depreciation methods;

debt, partner-level basis information, and at-risk exposure;

passive losses and other carryforwards;

material-participation and grouping positions;

operating results and expected income;

intended holding period and plausible exit paths.

Exit-year pressure is the accumulated result of how ownership decisions, tax attributes, liquidity and supporting records were managed throughout the holding period.

“Property-level records become strategically useful when they roll into a maintained portfolio map. We would use that map to determine which events change loss usability, liquidity requirements or the analysis of a future sale, exchange or transfer.”

These attributes do not remain isolated. A change in participation, passive income elsewhere, a disposition, a new partner, or a shift in business income may change how a recommendation performs. The advisor should update the map rather than rebuilding it when a property is already under contract.

If the information cannot be reconciled, sale or exchange planning can become a reconstruction project. That is often when an investor discovers that the prior returns were filed correctly but the portfolio was never managed as a connected tax system.

If your real estate portfolio sits alongside an operating business or professional income, our Business Tax Planning Review can examine how real estate decisions interact with entities, compensation, estimated payments, and longer-term plans.

Look for an advisor who can coordinate without overstepping

Sophisticated real estate planning is usually a team process.

The tax advisor should be able to identify tax dependencies and coordinate with:

real estate and estate-planning counsel;

lenders and debt advisors;

qualified intermediaries;

valuation and cost-segregation professionals;

property managers and bookkeepers;

investment and insurance advisors.

Coordination does not mean the tax advisor replaces those professionals. It means the team understands where one decision creates consequences for another discipline.

An attorney may recommend an ownership structure for liability or estate-planning reasons. A lender may impose different ownership or guarantee requirements. The tax advisor may identify reporting, basis, allocation, or exit consequences. If those conversations occur separately, the investor is left to absorb the conflict after documents have been drafted.

A useful question is:

When legal, lending, estate, and tax objectives conflict, how do you document the trade-off and help the team reach a decision?

A strong coordination process should produce more than a group email. It should identify the decision, the unresolved dependencies, the responsible professional, the deadline, and the effect on the larger plan. That is especially important when ownership structure and succession planning overlap.

Require Florida knowledge where it changes the analysis

Florida’s individual-income-tax environment can simplify one part of the state analysis for many natural persons, but it does not make Florida real estate tax planning simple.

Federal rules often drive income classification, depreciation, passive-activity treatment, basis, gain recognition, and exit planning. Florida and local rules may still matter through:

documentary stamp tax on deeds and certain financing documents;

transient-rental and local-option taxes;

tangible personal property reporting;

Florida entity and corporate filing exposure;

county and municipal requirements;

income and gain sourced to states where other properties are located.

Ownership circumstances may also require a separate federal withholding review, distinct from the Florida and local analysis.

The Florida Department of Revenue maintains current guidance for documentary stamp tax. Other Florida and local obligations should be reviewed against the guidance applicable to the specific activity and jurisdiction. An Orlando or Central Florida investor with short-term rentals may also face local administration that differs from the obligations of a long-term landlord.

This is where local knowledge should be specific. “Florida has no individual income tax” is not a planning analysis. The advisor should be able to identify which federal, state, county, municipal, and out-of-state issues actually apply to the portfolio.

Physical proximity can help with relationships, but it is not a substitute for depth. A nearby generalist is not automatically a stronger fit than a remote advisor with relevant Florida experience, secure systems, responsive service, and a reliable coordination process.

We can assess which federal, Florida, local, and multistate considerations may be relevant to your portfolio and upcoming decisions.

Evaluate the engagement, not just the advisor’s knowledge

A technically strong advisor can still be a poor operational fit. Before signing, review what the engagement actually requires the firm to do.

The scope should clarify:

which individuals, entities, trusts, returns, and states are included;

whether planning is included or separate from compliance;

which projections and estimated-payment calculations will be prepared;

which events trigger additional analysis;

who maintains basis, depreciation, and carryforward schedules;

who performs the work and who reviews it;

how notices and examinations are handled;

response and turnaround expectations;

client document responsibilities and deadlines;

how additional projects are approved and priced.

Then ask what you will receive during the year. Depending on the engagement, useful outputs may include a current-year projection, a multi-year scenario comparison, a property-level tax-attribute schedule, a planning calendar, an implementation log, and an exit analysis before a disposition.

The point is not to require the same package from every firm. It is to make sure that “proactive planning” has a defined output.

Transparent pricing does not require the lowest fee or a particular billing model. It requires a clear relationship among scope, responsibility, deliverables, and cost. Compensation tied to the size of a refund remains a preparer warning sign identified by the IRS.

Data handling also belongs in the evaluation. Ask about the secure portal, access controls, multifactor authentication, staff training, vendor oversight, retention procedures, and written information-security process used to protect client data.

The practical test is simple: after a planning meeting, do you know what was decided, what remains unresolved, who owns each action, and when the issue will be reviewed again?

Our Tax Prep + Advisory Review can help determine whether planning triggers, deliverables, implementation ownership, and follow-through are defined in your current engagement.

Ask questions that reveal judgment

Use the initial consultation to learn how the advisor thinks, not to collect a list of services.

Which client, property, and transaction profiles are most comparable to mine?

What records would you review before recommending a strategy?

How do you determine whether a generated deduction or loss will be usable now?

What facts would cause you to recommend against cost segregation or accelerated depreciation?

How do you evaluate real estate professional status, material participation, grouping, and supporting records?

How do you model depreciation through a taxable sale, qualifying exchange, gift, or estate transfer?

Which decisions should reach you before a contract is signed or a transaction closes?

How do you track basis, debt, depreciation, and suspended losses across several properties and entities?

What written deliverables will I receive, and who will implement and review each recommendation?

How do you coordinate with attorneys, lenders, qualified intermediaries, and other specialists?

Which Florida, local, and multistate exposures would you screen for?

How are disagreements, notices, examinations, data security, and continuity after filing handled?

Listen to the questions the advisor asks in return. If a structure or strategy is recommended before the advisor understands the returns, entities, debt, depreciation schedules, participation, income pattern, liquidity needs, and intended holding period, the process may be too shallow.

Also ask when the advisor would say no. Judgment is often clearer in the strategies an advisor declines, narrows, or delays than in the strategies listed on a website.

Watch for these real estate tax advisor red flags

One imperfect answer does not necessarily make an advisor a poor fit. We would be more concerned by a pattern such as:

Strategy-first advice: A favorite entity, depreciation method, or exchange is recommended before the facts are understood.

Classification shortcuts: The advisor treats an LLC name, rental label, or investor description as the tax conclusion.

Deduction-only analysis: The discussion focuses on the gross deduction without testing basis, at-risk exposure, passive treatment, or current usability.

Exit blindness: Accelerated depreciation or deferral is recommended without modeling basis, future gain, liquidity, suspended losses, or alternate exit paths.

Timing failure: The advisor learns about acquisitions, ownership changes, financing, or sales only after the documents are signed.

Tax-attribute gaps: Depreciation schedules, adjusted basis, debt information, or carryforwards cannot be reconciled across entities and properties.

Coordination gaps: Ownership or estate changes are recommended without legal and lending input, or no one owns implementation.

Over-certainty: The advisor promises guaranteed outcomes, permanent tax elimination, or an “audit-proof” position.

Operational ambiguity: Review responsibility, response standards, written deliverables, and notice support remain unclear.

Weak data practices: Sensitive information is exchanged or retained through channels that do not match the risk of the records involved.

The most expensive failure is not always an incorrect return. It may be a valid strategy used in the wrong year, a deduction that cannot yet be used, an election made without an exit model, or a transaction reviewed only after the investor’s alternatives have narrowed.

The real selection test: can the advisor protect optionality?

Sophisticated real estate tax planning is not a contest to produce the largest immediate deduction. It is a process for improving decisions while credible alternatives still exist.

Consider an investor who owns a profitable service business, several rentals, and a property that may be sold within the next few years. A shallow review might identify accelerated depreciation and estimate the deduction.

A stronger review would ask:

Is the activity classified correctly?

Could the resulting loss be used currently?

Which limitation, if any, would suspend it?

How would the deduction change adjusted basis and later sale analysis?

Is the expected holding period long enough for the timing benefit to make sense?

Is a taxable sale, qualifying exchange, gift, or longer hold genuinely plausible?

How would the exit interact with other income and liquidity needs?

What records and implementation steps would be required?

The advisor may still recommend full acceleration. The better conclusion may be a narrower approach, different timing, or no change. The point is not that one answer is always correct. It is that the recommendation should remain useful under more than one realistic future.

This is the standard readers can apply even if they already have a CPA. Ask the current advisor to walk one major decision through the five layers and identify the next planning window. If the relationship can do that consistently, the planning function may already be present. If it cannot, the gap is more specific than “I need a new accountant.”

The gap is decision coverage.

Conclusion: choosing a tax advisor for your real estate business

What should you look for in a tax advisor for your real estate business? Start with verified credentials and experience that matches your real estate model. Then test whether the advisor can connect classification, current deduction usability, cash-flow timing, documentation, and exit consequences across your entire tax picture.

The right engagement should also have a working system: defined decision triggers, current and multi-year projections, maintained tax attributes, written implementation responsibilities, coordination with other professionals, transparent scope, secure data handling, and follow-through after filing.

For a high-income Florida investor or business owner, that is the difference between hiring someone to report real estate activity and engaging an advisor who can help shape tax-sensitive decisions while there is still room to act.

Planning next step: If an acquisition, ownership change, depreciation decision, sale, exchange, or portfolio transition is approaching, use our Investment Tax Assessment to review the decision before the tax, legal, and financing consequences become difficult to change.

If an acquisition, ownership change, depreciation decision, sale, exchange, or portfolio transition is approaching, we can evaluate it before key terms become difficult to change.

Florida Real Estate Tax Planning

Frequently Asked Questions About Choosing a Real Estate Tax Advisor

Use these questions to evaluate whether an advisory relationship can support the decisions, tax attributes, and potential exit paths across your real estate portfolio.

How often should I meet with a real estate tax advisor?

We would set the cadence around decision windows rather than a fixed number of meetings. A relatively stable portfolio may need periodic projection, implementation, and post-filing reviews, while more transactional activity may require contact before an acquisition, financing change, ownership transfer, major improvement, sale, or exchange. The more important test is whether the engagement defines which events trigger review, how early the advisor should be involved, and what gets updated afterward. A calendar without event triggers can still be reactive; event access without regular tax-attribute maintenance can remain fragmented.

What should I expect during an initial consultation with a real

estate tax advisor?

We would expect the first meeting to be diagnostic, not a strategy pitch. The advisor should ask about property use, holding purpose, ownership, debt, participation, partner economics, related businesses, income patterns, liquidity, and realistic exit paths. The conversation should also clarify who leads planning, who prepares and reviews returns, what records are needed, which decisions require advance notice, and what written deliverables follow. If a structure, election, or depreciation strategy is recommended before those facts are understood, the consultation has revealed a process weakness, even if the tactic could eventually be appropriate.

What records should a real estate tax advisor review before

making recommendations?

We would expect the relevant prior returns, entity agreements, closing statements, depreciation schedules, basis workpapers, debt information, improvement history, carryforward schedules, participation records, operating results, and documents for planned transactions. The exact request should follow the decision being evaluated. More importantly, the advisor should explain which records control the analysis, whether the portfolio’s tax attributes reconcile, and how missing information affects the recommendation. Collecting a large document package is not the same as converting it into a reliable classification, usability, cash-flow, and exit analysis.

Should my real estate tax advisor also prepare my tax returns?

Not necessarily, but responsibility must be explicit. A separate strategist and return preparer can work effectively if they share positions, assumptions, elections, basis information, depreciation schedules, carryforwards, implementation owners, and deadlines. An integrated firm may reduce handoffs, but integration alone does not establish planning depth. We would focus on who converts the recommendation into return reporting and who updates the affected tax attributes afterward. If each professional assumes the other owns implementation, a technically sound recommendation can become an orphaned strategy that is difficult to support or reconstruct later.

How can I tell whether my current CPA is proactive enough for my

real estate portfolio?

We would ask the current CPA to walk one live or recent decision through classification, current-year usability, cash-flow timing, exit consequences, and documentation. Then ask which upcoming event should trigger the next review, what assumptions could change the conclusion, who owns implementation, and how the affected tax attributes will be maintained. Accurate returns and responsive answers are valuable, but they do not by themselves demonstrate decision coverage. This test helps identify whether the missing function is engagement scope, transaction timing, multi-year modeling, coordination, or something more fundamental in the advisory relationship.

Does my real estate tax advisor need to be located in Florida?

Not necessarily. We would prioritize whether the advisor can distinguish federal planning from the Florida, county, municipal, and multistate considerations that actually affect the portfolio. That may include transaction taxes, transient-rental obligations, tangible personal property reporting, entity exposure, local administration, and income or gain connected to properties in other states. Physical proximity can help coordination, but it does not replace relevant experience, secure systems, or responsive service. Ask the advisor to identify the jurisdictions they would screen, the facts that drive that review, and how local specialists would be coordinated when needed.

Should I hire a CPA, enrolled agent, or tax attorney for real

estate tax planning?

We would choose based on the work required rather than treating one credential as universally superior. Credentials and representation rights establish an important baseline, but the engagement still needs real estate-specific planning depth and clearly assigned responsibilities. A CPA or enrolled agent may lead ongoing planning, compliance, projections, and IRS matters, while a tax attorney may be important when legal documents, disputes, or estate structures are involved. For a sophisticated portfolio, the stronger arrangement may be a lead tax advisor who maintains the planning system and coordinates with counsel and other specialists when the decision requires them.

When should I involve a tax advisor in a property sale or 1031

exchange?

We would involve the advisor before the economic and legal terms are finalized, while a taxable sale, qualifying exchange, continued hold, gift, or other transfer can still be compared realistically. The review may need to connect adjusted basis, accumulated depreciation, suspended losses, debt payoff, selling costs, liquidity, other gains, potential net investment income tax exposure, and the next likely ownership or exit path. The objective is not to assume that an exchange or another strategy is preferable. It is to understand the trade-offs before the contract, ownership, financing, and closing process narrow the available choices.